By The RX Index Research Team · Last verified: March 28, 2026 · Reviewed against IRS Publication 502, IRS Wellness FAQ, FSAFEDS eligibility rules, and official provider payment pages. Updated monthly. · Editorial standards

FSA & HSA FOR GLP-1 — 2026 COMPLETE GUIDE

Can I Use My FSA for GLP-1? Yes — Here's Exactly When It Works (2026 Rules)

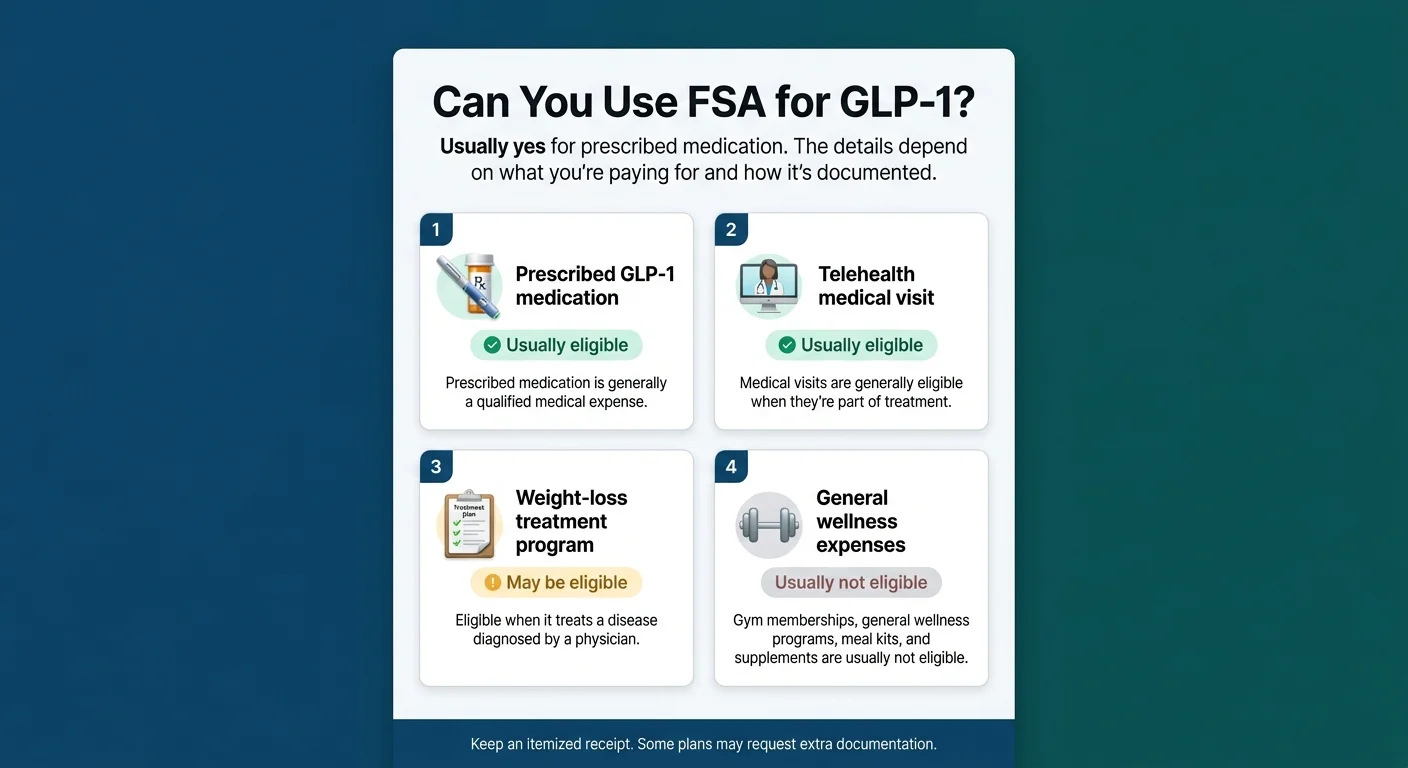

Usually yes. Prescribed GLP-1 medication is generally a qualified medical expense under IRS rules. For weight-loss-related claims specifically, the IRS requires the expense to be treatment for a disease diagnosed by a physician — and your plan administrator may ask for an itemized receipt or a Letter of Medical Necessity.

But “usually yes” isn't what you're really here for. You want to know: will your FSA actually cover your GLP-1 — and what happens if you swipe your card and it gets declined? That happens more than you'd think, and it almost never means you're ineligible. It means the payment system hit a friction point.

What actually causes denials isn't the medication. It's missing paperwork: a receipt that isn't itemized, a weight-loss prescription without a documented diagnosis, or a plan administrator who wants a Letter of Medical Necessity you never requested. This guide closes every gap.

What's FSA-eligible for GLP-1 depends on the expense type and how it's documented. Source: The RX Index, 2026.

Quick Reference: Can You Use FSA for This GLP-1 Expense?

| GLP-1 Expense | FSA/HSA Eligible? | Key Requirement |

|---|---|---|

| Prescription GLP-1 (brand-name) | ✅ Usually yes | Valid prescription for a diagnosed condition (IRS Pub 502) |

| Prescription GLP-1 (compounded) | ⚠️ May be reimbursable | Prescription + itemized receipt + LMN strongly recommended |

| Telehealth consultation / doctor visit | ✅ Usually yes | Part of a medical treatment plan |

| Weight-loss program tied to diagnosed disease | ⚠️ Depends | Letter of Medical Necessity often required (FSAFEDS) |

| Shipping / handling on eligible expense | ✅ Eligible with itemized receipt | Must appear on an itemized receipt for an eligible expense |

| General wellness program, gym, meal kits | ❌ Usually no | Not treatment for a diagnosed disease under IRS rules |

| Late fees | ❌ No | Not qualified medical expenses |

Disclosure: Some links on this page are affiliate links. If you purchase through these links, we may earn a commission at no extra cost to you.

What Does the IRS Actually Require for GLP-1 to Be FSA Eligible?

The IRS rule is simpler than most people expect.

Under IRS Publication 502, you can use FSA or HSA funds for “the costs of diagnosis, cure, mitigation, treatment, or prevention of disease,” which includes prescribed medicines and drugs. GLP-1 medications — whether Wegovy, Zepbound, Ozempic, Mounjaro, or a compounded version — are prescription drugs. When prescribed to treat a medical condition, they generally qualify.

Here's the critical distinction for weight loss: the IRS separately says that weight-loss expenses are medical expenses only when the weight loss is treatment for a specific disease diagnosed by a physician. The IRS wellness FAQ gives examples such as obesity, diabetes, hypertension, and heart disease. Weight loss for general health or appearance does not qualify.

The IRS does not care which GLP-1 brand you use. It cares about one thing: is this prescribed medication treating a diagnosed medical condition?

What You Need for Your GLP-1 to Be FSA/HSA Eligible

A prescription from a licensed provider

No prescription, no eligibility. This applies whether you’re filling at a retail pharmacy or through an online telehealth provider.

A documented medical diagnosis

Your provider needs an actual condition in your medical chart — obesity, type 2 diabetes, or another diagnosed disease. The diagnosis is what makes the expense “medical” rather than “wellness.” Other diagnoses may also qualify, but the documentation standard is set by your clinician and your plan administrator.

A Letter of Medical Necessity (recommended for weight-loss claims)

Not every plan requires one for the medication itself. But for weight-loss prescriptions, many FSA administrators will ask for it — either upfront or during review. Getting one during your initial consultation prevents problems later.

What Does NOT Qualify

- ✗ Weight loss without a documented medical diagnosis — even if a doctor prescribed the medication

- ✗ “Wellness clinic” prescriptions where no actual diagnosis is documented in your chart

- ✗ Non-prescription supplements marketed as GLP-1 alternatives

- ✗ Gym memberships, meal delivery, and fitness programs (very rare exceptions with a specific LMN)

“My FSA says I have to prove I medically need GLP-1.” — r/SemaglutideCompound That's exactly right. If your provider documents a real condition and writes a real prescription, you're covered. If the prescription comes without a diagnosis, your FSA administrator has every right to reject the claim.

If you have a diagnosed condition like obesity or type 2 diabetes and a valid prescription, you very likely qualify. The next step is choosing a provider who documents everything properly.

Check Eligibility on Ro (FDA-Approved GLP-1) →Do You Need a Letter of Medical Necessity for GLP-1?

Not always — but getting one is cheap insurance against a denial.

When you probably don't need one:

- Your GLP-1 is prescribed for type 2 diabetes

- You're filling a standard prescription at a retail pharmacy

- Your FSA plan doesn't specifically require LMN for prescription medications

When you should plan on having one:

- GLP-1 prescribed for weight loss (even with documented obesity)

- Using a telehealth platform or bundled weight-loss program

- Your FSA administrator flags the charge for review

- You're using compounded medication

Our recommendation: Ask your provider for an LMN during your initial consultation. If your administrator later requests one, you'll already have it. It takes minutes and costs nothing.

What the LMN Should Include

- Your name and date of birth

- Your medical diagnosis (with ICD-10 code if available)

- A statement that GLP-1 medication is medically necessary to treat the diagnosed condition

- The specific medication prescribed

- Expected duration of treatment

- Prescriber's signature, credentials, and contact information

“The biggest thing you need to make sure of is what your FSA requires for reimbursement.” — r/glp1 Every administrator has slightly different documentation preferences. A quick call to HR or your benefits administrator before you pay can save you from a denial later.

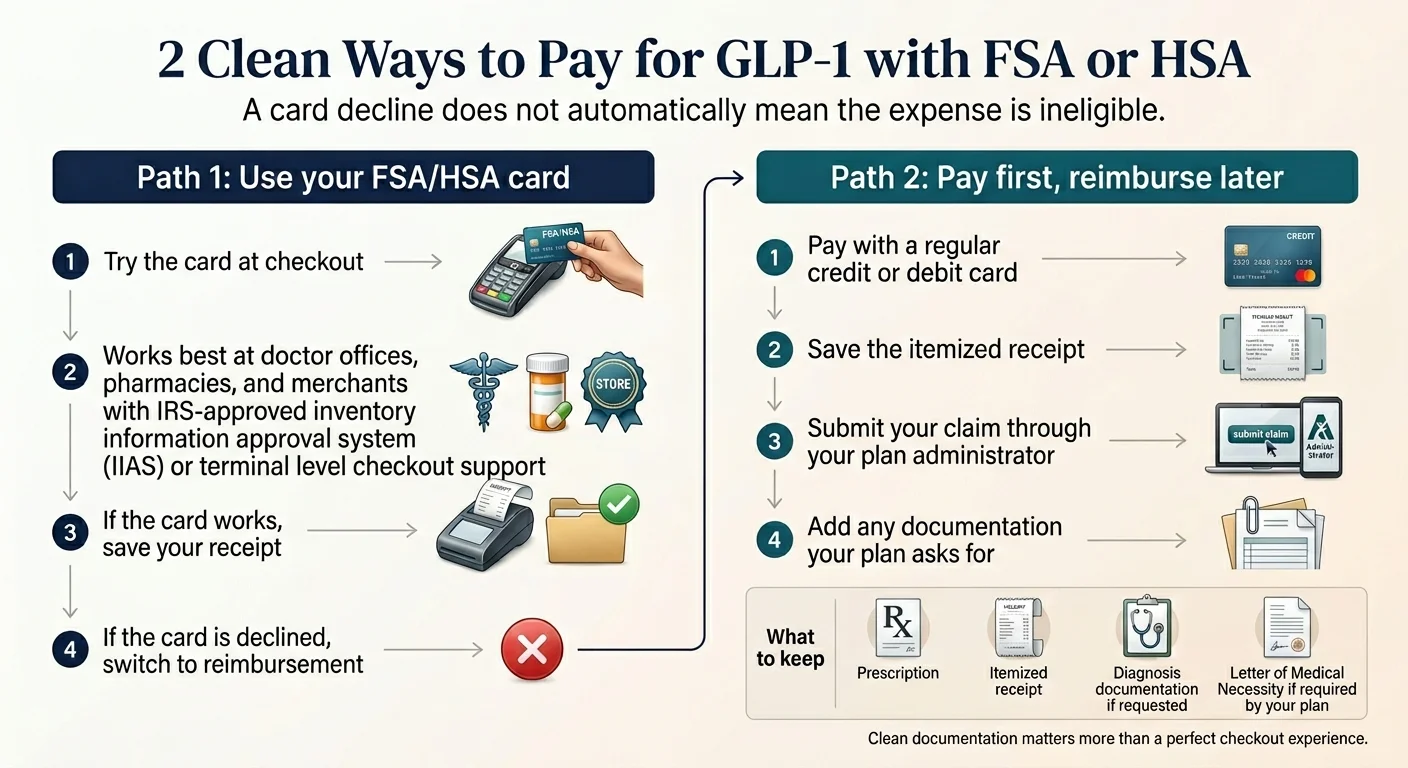

Can You Use Your Actual FSA Card, or Do You Need Reimbursement?

This is the question most guides skip — and the one that matters most at checkout.

“Is there a website where I can get Semaglutide with my actual FSA debit card and not have to submit a claim?” — r/Semaglutide

Honest answer: sometimes the card works, but reimbursement is often the more reliable route with online GLP-1 providers.

FSA debit card purchases work best where the merchant can auto-substantiate eligible medical expenses through an IRS-approved system such as IIAS (Inventory Information Approval System). Many retail pharmacies have this built in. Online telehealth platforms often don't — which means the card transaction may get flagged, held, or declined even when the expense is perfectly eligible. HealthEquity FSA Card Guide

A card decline does not mean the expense is ineligible. It means the system couldn't auto-verify it. The fix is straightforward — pay with a regular card and submit for reimbursement.

Two clean paths for using FSA/HSA funds for GLP-1. A card decline does not mean the expense is ineligible. Source: The RX Index, 2026.

Path A — Try your FSA/HSA card at checkout

If it processes, you're done. If it gets flagged, you'll receive a documentation request — upload your LMN and itemized receipt. Works best at retail pharmacies and merchants with IIAS systems.

Path B — Pay with a regular card, then submit for reimbursement

Download your itemized receipt from the provider. Submit through your FSA/HSA administrator's portal with your LMN and receipt. More steps, but rarely fails when your documentation is clean. This is the standard path for most online GLP-1 providers.

How to Use Your FSA or HSA to Pay for GLP-1 (Step by Step)

Check Your Account

Log into your benefits portal or call HR. Confirm: Do you have an FSA, HSA, or both? What's your current balance? When does your plan year end? Does your plan allow a carryover or grace period?

Get Prescribed by a Licensed Provider

You need a prescription from a licensed healthcare provider — your PCP, a specialist, or a licensed telehealth provider. During your consultation, make sure your provider: documents your diagnosis in your medical chart, writes the prescription tied to that diagnosis, and can provide a Letter of Medical Necessity if your plan requires one.

Pay for Your Treatment

Option A: Try your FSA/HSA card at checkout. If it processes, you're done. If it gets flagged, move to Option B. Option B: Pay with a regular credit or debit card. Download your itemized receipt from the provider's portal afterward.

Submit for Reimbursement (if needed)

Log into your FSA/HSA administrator's portal (WEX, HealthEquity, Optum, etc.). Start a new reimbursement claim. Upload your itemized receipt and Letter of Medical Necessity. Submit. Reimbursement timing depends on your administrator — some process in days, others take longer.

Keep Your Records

Save copies of everything for at least 3 years (the IRS audit window): your prescription, Letter of Medical Necessity, all itemized receipts (showing provider name, medication name, date, amount), and reimbursement confirmations.

Your GLP-1 FSA Reimbursement Checklist

Before you pay

After you pay

Which GLP-1 Provider Makes FSA/HSA Payment Easiest?

You know the rules. You know what documents you need. Now — which provider creates the least friction with your benefits account? We reviewed the FSA/HSA payment experience for major online GLP-1 providers based on their official published policies.

| Provider | Direct FSA Card? | Reimbursement Path | Medication Type | Best For |

|---|---|---|---|---|

| Ro | ❌ Pay first, then reimburse | ✅ Detailed itemized receipt | FDA-approved (Wegovy, Zepbound) | Insurance coordination + brand-name meds |

| MEDVi | ✅ Marketed as HSA/FSA approved | ✅ Receipt provided | Compounded + some brand-name | Cash-pay simplicity |

| Hers | ⚠️ Recommends reimbursement | ✅ Receipt in Orders tab | Compounded + oral options | Reimbursement-clear workflow |

| SkinnyRX | ✅ Reimbursement supported | ✅ Documentation provided | Compounded | Budget-friendly |

| TrimRX | ✅ Reimbursement supported | ✅ Documentation provided | Compounded | Affordable compounded |

Prices and payment methods reflect official provider pages as of March 2026. Policies can change — we verify monthly.

Choose the provider path that matches how you want to pay. Source: The RX Index, 2026.

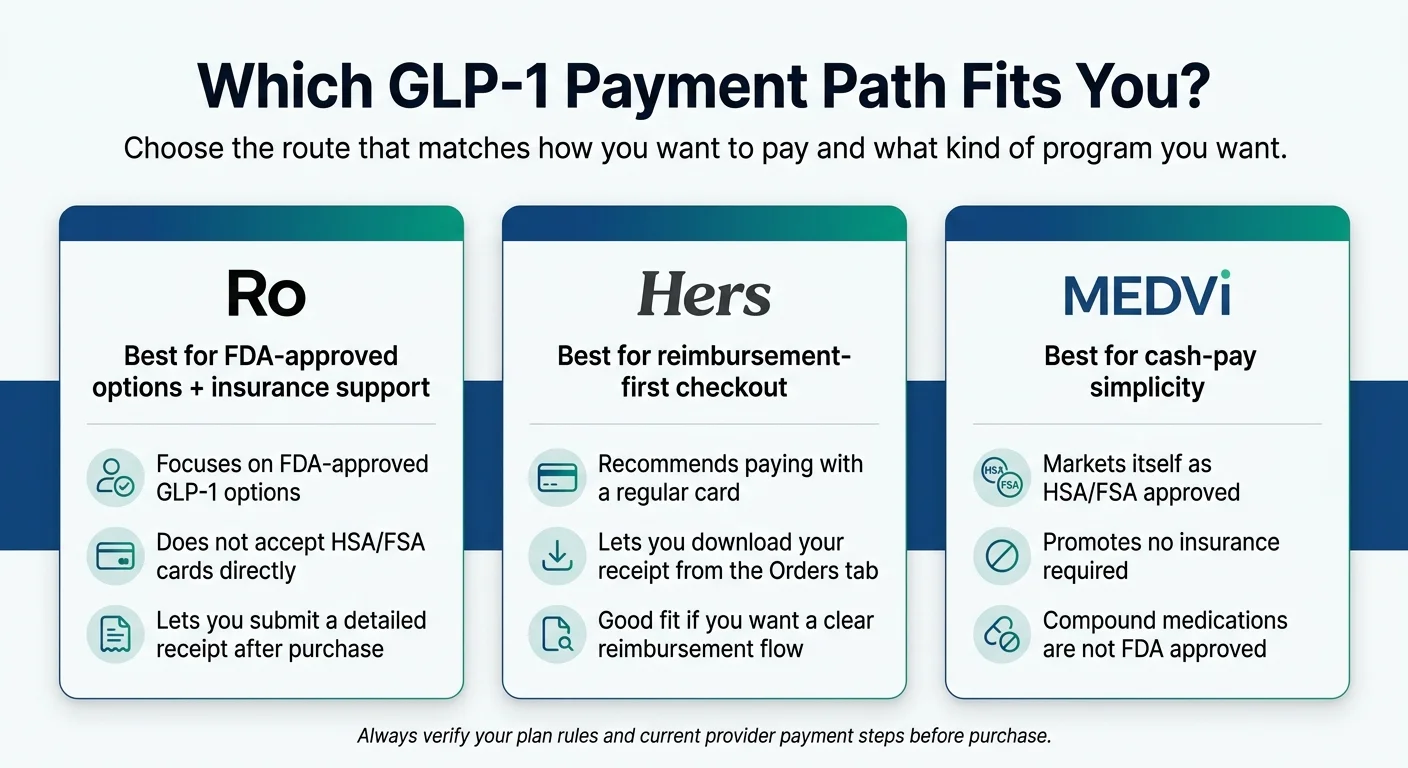

If you have insurance and want FDA-approved medication → Start with Ro

Ro focuses on FDA-approved GLP-1 options like Wegovy and Zepbound. Their insurance concierge handles prior authorization — where most people hit a wall on their own. If your insurance covers GLP-1s, you use FSA/HSA to cover copays and deductibles. If not, Ro offers cash-pay medication starting from $149/month.

Here's the trade-off we want to be transparent about: Ro does not accept FSA/HSA cards directly. You pay with a regular card and submit the receipt for reimbursement. If swiping at checkout with zero follow-up is your non-negotiable, Ro isn't the smoothest for that specific step.

But here's why we still recommend Ro first for most people: FDA-approved medications are the most recognizable category for FSA administrators. Your administrator sees “Wegovy” or “Zepbound” on the receipt and knows exactly what it is — no manual review, no confusion. The checkout requires one extra step. The reimbursement is the cleanest you'll file.

Ro combines insurance navigation with clean itemized receipts built for FSA/HSA reimbursement.

Check Eligibility on Ro →If you're paying cash and want bundled pricing → Look at MEDVi

MEDVi markets some of its compounded offers as HSA/FSA approved with no membership or hidden fees. They also offer some brand-name options. We recommend checking the specific offer you're considering, as the structure varies.

Important: MEDVi's compounded options are not FDA-approved finished drugs. If having FDA-approved, brand-name medication is important to you, Ro is the right path. If you want cash-pay pricing and are comfortable with the compounded route, MEDVi offers a straightforward model with direct FSA/HSA card acceptance.

MEDVi markets direct HSA/FSA card acceptance. Flat pricing for compounded semaglutide with no hidden fees.

See MEDVi Pricing & State Availability →If you want the most affordable option → SkinnyRX or TrimRX

At around $149/month, a full year of treatment costs about $1,788 — well within the 2026 FSA limit of $3,400 with over $1,600 left for other medical expenses. Both offer compounded GLP-1 options and provide documentation for FSA/HSA reimbursement.

If you already have a prescriber and pharmacy access

If your doctor already prescribed a GLP-1 and you're filling it at CVS, Walgreens, or another retail pharmacy, your FSA card very likely works there directly. Retail pharmacies typically have IRS-approved auto-substantiation systems, so the card processes like any other pharmacy purchase — no reimbursement paperwork.

We include this option because being honest about it makes us worth trusting on everything else. If a retail pharmacy fill is the simplest path for you, take it. That said, if your insurance doesn't cover GLP-1s and retail pricing (over $1,000/month for brand-name without savings cards) is out of reach, the online providers above offer dramatically lower price points.

Not sure which route fits your situation?

Take our free 60-second matching quiz. Tell us about your insurance, budget, and goals — we'll show you the best-fit provider and clearest payment path for your specific situation.

Take the 60-Second GLP-1 Quiz →How Much Can You Save Using FSA/HSA for GLP-1?

When you pay with pre-tax FSA or HSA dollars, you avoid federal income tax, state income tax (in most states), and — if contributions come through payroll deductions — FICA taxes. FSAFEDS estimates average savings of about 30%. Your actual savings depend on your specific tax situation.

Illustrative FSA savings examples (payroll-deduction FSA funding):

| Scenario | Monthly Cost | Est. Combined Tax Rate | Annual Savings | Effective Monthly Cost |

|---|---|---|---|---|

| 22% federal, 5% state, 7.65% FICA | $199/mo | ~34.65% | ~$827 | ~$130/mo |

| 24% federal, 5% state, 7.65% FICA | $299/mo | ~36.65% | ~$1,314 | ~$190/mo |

| 22% federal, no state income tax, 7.65% FICA | $149/mo | ~29.65% | ~$530 | ~$105/mo |

Illustrative estimates only. Actual savings vary by state, filing status, and contribution method. Not tax advice.

If you're in a no-income-tax state, paying $149/month for compounded GLP-1, and running it through your FSA — your effective cost is roughly $105/month. About $3.45 a day.

Can Your 2026 FSA or HSA Cover the Full Year?

2026 FSA limit: $3,400 (IRS Revenue Procedure 2025-32) • 2026 HSA limit: $4,400 individual / $8,750 family (+$1,000 catch-up if 55+)

| Monthly Cost | Annual Cost | Covered by FSA ($3,400)? | Covered by HSA ($4,400)? |

|---|---|---|---|

| $149/mo | $1,788 | ✅ Yes, ~$1,612 remaining | ✅ Yes |

| $199/mo | $2,388 | ✅ Yes, ~$1,012 remaining | ✅ Yes |

| $299/mo | $3,588 | ⚠️ Covers ~11 months | ✅ Yes |

The math is clear: if you're going the compounded route at $149–199/month, your FSA covers the entire year with room to spare. If you're on a higher-cost program, HSA has more room — and unlike FSA, unused HSA funds roll over indefinitely.

Is Wegovy FSA Eligible? What About Zepbound, Ozempic, and Mounjaro?

Let's answer each one directly.

Wegovy (semaglutide)

✅ YesFDA-approved specifically for chronic weight management. One of the cleanest GLP-1 options for FSA/HSA purposes because the indication matches. Your administrator may still want an LMN, but the FDA approval makes documentation straightforward.

Zepbound (tirzepatide)

✅ YesFDA-approved for chronic weight management. Same dynamic as Wegovy — clear indication, clean reimbursement path.

Ozempic (semaglutide)

✅ Yes, with a nuanceFDA-approved for type 2 diabetes, not weight loss. Prescribed for diabetes, it sails through FSA/HSA. Prescribed off-label for weight loss, you'll likely need an LMN documenting medical necessity for your diagnosed condition.

Mounjaro (tirzepatide)

✅ Yes, with a nuanceSame as Ozempic — FDA-approved for diabetes, straightforward for that use. Off-label for weight loss requires an LMN.

Rybelsus (oral semaglutide)

✅ YesFDA-approved for type 2 diabetes. Clear for diabetes; LMN recommended for off-label weight-loss use.

Compounded semaglutide or tirzepatide

⚠️ Yes, with more documentationPrescribed medication for a diagnosed condition is a qualified medical expense. But compounded medications aren't FDA-approved, so expect more administrator scrutiny. Have an LMN and clearly itemized receipt ready.

All brand-name GLP-1s follow the same principle: prescribed medication for a diagnosed condition is a qualified medical expense. FDA-approved drugs are the most recognizable to FSA systems and typically process with the least friction.

Can You Use FSA/HSA for Compounded GLP-1s?

This deserves its own section because it's the most common source of confusion.

The IRS answer

IRS rules about qualified medical expenses apply to prescribed medications generally. The IRS does not specifically address compounded vs. brand-name in Publication 502 — the framework is medical necessity, not drug approval status.

The practical answer

Compounded GLP-1 claims may be reimbursable when the medication is lawfully prescribed and properly documented. But expect more scrutiny than with standard pharmacy claims.

Here's why compounded GLP-1 claims get more scrutiny:

- FSA systems are built to recognize NDC (National Drug Code) numbers from FDA-approved drugs. Compounded medications typically don't carry standard NDC codes, so automated verification doesn't work the same way.

- Some administrators are less familiar with compounded prescriptions and may flag them for manual review.

- You'll almost certainly want an LMN, an itemized receipt from the compounding pharmacy, and your prescription on file.

Important safety note

Compounded GLP-1 medications are not FDA-approved finished drugs. The FDA has raised concerns about certain compounded GLP-1 products, particularly around dosing accuracy and misleading marketing. FDA: Concerns about unapproved GLP-1 drugs. If you go the compounded route, verify your provider uses a properly licensed pharmacy.

What this means for you: If you're going the compounded route, plan on the reimbursement path rather than trying to swipe your FSA card. Pay with a regular card, collect your documentation, and submit a clean claim.

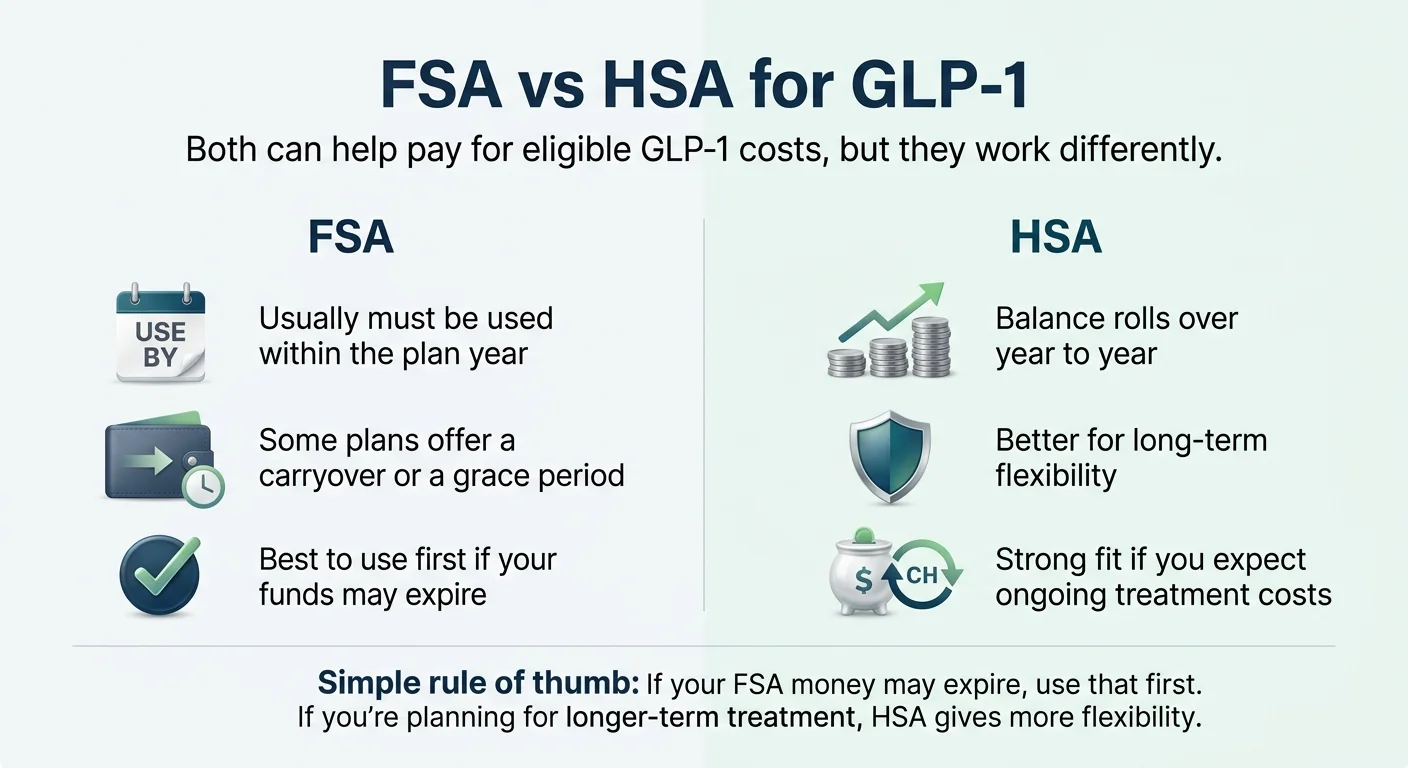

FSA vs. HSA for GLP-1: Which Should You Use First?

Both FSA and HSA can pay for eligible GLP-1 costs, but they work differently. Source: The RX Index, 2026.

| Feature | FSA | HSA |

|---|---|---|

| 2026 Contribution Limit | $3,400/year | $4,400 individual / $8,750 family |

| Funds expire? | Yes (up to $680 carryover or 2.5-mo grace) | No — rolls over indefinitely |

| Requires HDHP? | No | Yes |

| Pre-approval needed for GLP-1? | Some administrators require it | Generally no pre-approval |

| Best for GLP-1? | Planned costs you know in advance | Long-term treatment |

Rule of thumb: If you have FSA money that may expire, use that first — those dollars disappear if you don't. HSA dollars are permanent. Spend the expiring money, save the permanent money.

If GLP-1 treatment is going to be long-term (and for many people, it is), the HSA is the stronger vehicle. Unused balance grows tax-free and carries forward year after year.

Important

You generally cannot contribute to both a general-purpose FSA and an HSA simultaneously. A Limited-Purpose FSA (dental/vision only) can coexist with an HSA, but an LPFSA cannot be used for GLP-1 medications.

For the full HSA guide, see: Can I Use HSA for GLP-1? 2026 IRS Rules →

Your FSA Is About to Expire — Here's What to Do

If you have FSA funds approaching your plan year deadline and you've been considering GLP-1 treatment, both problems solve each other.

Most FSA plans end December 31. Some employers offer a grace period (spending until ~March 15) or a carryover of up to $680. Funds above that? Forfeited.

One critical rule

FSA administrators generally reimburse expenses that are incurred during the coverage period — meaning the service or product must be received before the deadline. FSAFEDS specifically notes that fees paid in advance of services being rendered are not eligible. Do not assume you can prepay several future months and get it all reimbursed.

Here's the timeline to use expiring FSA funds for GLP-1:

Don't lose pre-tax dollars you've already earned. Start your GLP-1 consultation this week.

What to Do If Your FSA Claim Gets Denied

It happens — and it's almost always a documentation issue, not an eligibility issue.

The Most Common Denial Reasons

Missing Letter of Medical Necessity

Your administrator required one for a weight-loss prescription and you didn’t submit it. This is the #1 denial reason.

Non-itemized receipt

A credit card statement isn’t enough. Administrators need a receipt showing provider name, medication name, date of service, and amount. Credit card receipts, canceled checks, and balance-forward statements do not meet FSAFEDS documentation requirements.

Expense coded as "wellness" or "lifestyle"

If the charge description reads "wellness program" instead of "medical consultation" or "prescription medication," it can trigger a denial.

Bundled charges without itemization

If your provider bundles medication + consultation + other services into one line item, administrators can’t verify which components are medical. Itemized charges for actual medical visits, labs, and prescription medication are stronger than access or membership fees.

Compounded medication unfamiliarity

Some administrators don’t recognize compounded medications in their system and default to requesting additional documentation.

How to Get a Denied Claim Approved

Questions to Ask Your Plan Administrator Before You Pay

- →“Do you require an LMN for GLP-1 medication prescribed for weight loss?”

- →“Will you reimburse a telehealth visit that’s part of a treatment plan?”

- →“Can I use my FSA card directly with an online provider, or should I submit a manual claim?”

- →“For compounded medication, what documentation do you require?”

- →“Do bundled program charges need to be itemized?”

Starting with a provider who documents everything properly from day one is the simplest path. Ro builds medical documentation into their onboarding. MEDVi provides itemized receipts designed for FSA/HSA claims.

You're Not Gaming the System

We want to address the unspoken thought a lot of people have: “Is it really okay to use my FSA for weight-loss medication?”

Yes. This is exactly what these accounts are for.

You contribute pre-tax dollars to pay for medical expenses. GLP-1 medication prescribed by a licensed provider for a diagnosed medical condition is a medical expense. The IRS says so in Publication 502. Your plan administrator processes these claims routinely.

Obesity is a disease. Type 2 diabetes is a disease. Treating them with physician-prescribed medications is medical care. Using your medical benefits account to pay for medical care is using your benefits as intended.

You don't need permission from a blog post on the internet. But if it helps to hear it: this is a smart financial decision about a legitimate medical expense.

Planning Ahead: Setting Your 2026 FSA/HSA for GLP-1 Treatment

If you're in open enrollment or planning for next year:

Step 1: Estimate your annual GLP-1 cost (monthly cost × 12, plus initial consultation and any lab work).

Step 2: Add a buffer for other medical expenses — dental, copays, prescriptions, eye exams.

Step 3: Set your contribution (see table below).

| Monthly GLP-1 Cost | Annual Cost | Suggested FSA Contribution | Suggested HSA Contribution |

|---|---|---|---|

| $149/mo | $1,788 | $2,400–$2,800 | $2,500–$3,000 |

| $199/mo | $2,388 | $2,800–$3,200 | $3,000–$3,500 |

| $299/mo | $3,588 | Max out at $3,400 | $4,000–$4,400 |

The HSA advantage for long-term users: If you expect to stay on GLP-1 for a year or more, the HSA is superior. Unused funds roll over, the balance can be invested, and you can reimburse yourself for past expenses at any time. Some people pay out of pocket now, save their receipts, and reimburse themselves later when they may be in a lower tax bracket. That's a legitimate strategy.

How We Verified This Guide

Tax and eligibility sources: IRS Publication 502, IRS Wellness FAQ, IRS Revenue Procedure 2025-32 (2026 contribution limits), FSAFEDS eligible expenses, HealthEquity FSA card documentation.

Provider verification: Ro pricing page, Hers FSA/HSA page, MEDVi site. Payment acceptance reviewed based on official published policies.

Regulatory sources: FDA concerns about unapproved GLP-1 drugs.

Update commitment: We re-verify provider payment methods and pricing monthly. If a provider changes their policy, we update within one week. This guide is not medical advice or tax advice — consult your healthcare provider and tax advisor for your specific situation.

Frequently Asked Questions

Can I use my FSA for GLP-1 weight loss medications?

Usually yes. Prescribed GLP-1 medications are generally FSA-eligible when treating a disease diagnosed by a physician, such as obesity or diabetes. You need a valid prescription, and your plan may require a Letter of Medical Necessity for weight-loss claims. Source: IRS Publication 502.

Are GLP-1 medications HSA eligible too?

Yes, the same IRS rules apply to both FSA and HSA. The key practical difference is mechanics: HSA funds roll over year to year indefinitely, while FSA funds are typically use-it-or-lose-it at plan year-end.

Can I use my FSA card to pay for GLP-1 online?

Sometimes. FSA card purchases work best at merchants with IRS-approved auto-substantiation (like retail pharmacies). Online telehealth providers may not support this system, so the card may be declined even when the expense is eligible. Paying with a regular card and submitting for reimbursement is the more reliable path with most online GLP-1 providers.

Is semaglutide FSA eligible?

Yes — both brand-name semaglutide (Ozempic, Wegovy, Rybelsus) and compounded semaglutide are generally eligible when prescribed for a diagnosed medical condition. Compounded claims may face more administrator scrutiny and require stronger documentation.

Is tirzepatide FSA eligible?

Yes — both brand-name tirzepatide (Mounjaro, Zepbound) and compounded tirzepatide follow the same IRS eligibility rules as other prescribed GLP-1 medications.

Can I use FSA for compounded semaglutide?

Compounded GLP-1 claims may be reimbursable when lawfully prescribed for a diagnosed condition, but they are not FDA-approved finished drugs and often face more documentation requests from administrators. Have a Letter of Medical Necessity and a clearly itemized receipt ready before submitting a claim.

Do I need a Letter of Medical Necessity for Wegovy?

It depends on your plan. Since Wegovy is FDA-approved for weight management, some administrators accept the prescription alone. Others require an LMN for any weight-loss prescription. Get one proactively during your consultation — it eliminates the biggest source of claim denials.

Is a telehealth visit FSA eligible?

Yes. Medical consultations — whether in-person or via telehealth — are qualified medical expenses when part of a treatment plan for a diagnosed condition. This includes GLP-1 consultations through online providers like Ro and MEDVi.

Can I use FSA for the program membership fee?

Do not assume membership or platform fees are automatically eligible. Itemized charges for medical visits, labs, and prescription medication are the strongest FSA claims. Bundled membership or access fees may not qualify, and FSAFEDS specifically notes that fees paid in advance of services being rendered are not eligible. Check with your administrator before submitting.

What if my FSA claim for GLP-1 gets denied?

Read the denial reason carefully — it tells you exactly what is missing. The fix is almost always a Letter of Medical Necessity, a properly itemized receipt with the medication name, or separation of medical charges from bundled non-medical fees. Resubmit with complete documentation. Most denials are paperwork issues, not eligibility issues.

Should I use FSA or HSA first for GLP-1?

If your FSA funds are expiring, use those first — FSA dollars disappear if you don't spend them by your plan year deadline. HSA funds never expire, roll over indefinitely, and can be invested. Save your HSA for longer-term treatment or reimburse yourself later.

Can I get reimbursed for GLP-1 I already paid for?

For HSA: yes, you can reimburse yourself at any time for expenses incurred while the HSA was established, with no time limit. For FSA: you can typically only claim expenses incurred during the current plan year and any applicable grace period. Check your plan rules.

Are weight loss injections FSA eligible?

Yes, when prescribed by a licensed provider for a diagnosed medical condition. Weight loss injections is a colloquial term for GLP-1 receptor agonists — they are prescription medications, and prescribed medications for diagnosed conditions are qualified FSA expenses under IRS Publication 502.

How much of my FSA can I use for GLP-1?

Your entire FSA balance can go toward GLP-1 treatment — there is no separate per-medication cap. The 2026 FSA contribution limit is $3,400. At $149–199/month for compounded GLP-1, your full-year cost falls within that limit, leaving room for other medical expenses.

Still Not Sure Which GLP-1 Program Is Right for You?

Take our free 60-second matching quiz.

Tell us about your insurance, budget, and health goals — then we'll show you the best-fit provider and the clearest payment path for your specific situation.

Take the 60-Second GLP-1 Quiz →Or go direct:

This page is updated monthly. Provider pricing, payment methods, and FSA/HSA policies are verified against official provider pages. Last verified March 2026. The RX Index is an independent research platform. We may earn a commission when you visit a provider through our links — this does not affect our rankings, recommendations, or the accuracy of our information. This content is not medical advice or tax advice. Consult your healthcare provider and tax professional for guidance specific to your situation.

By The RX Index Research Team · Last updated March 28, 2026 · More GLP-1 guides →

Related Guides