HSA & FSA FOR GLP-1 — 2026 COMPLETE GUIDE

Can I Use HSA for GLP-1? Yes — But Most People Get One Part Wrong

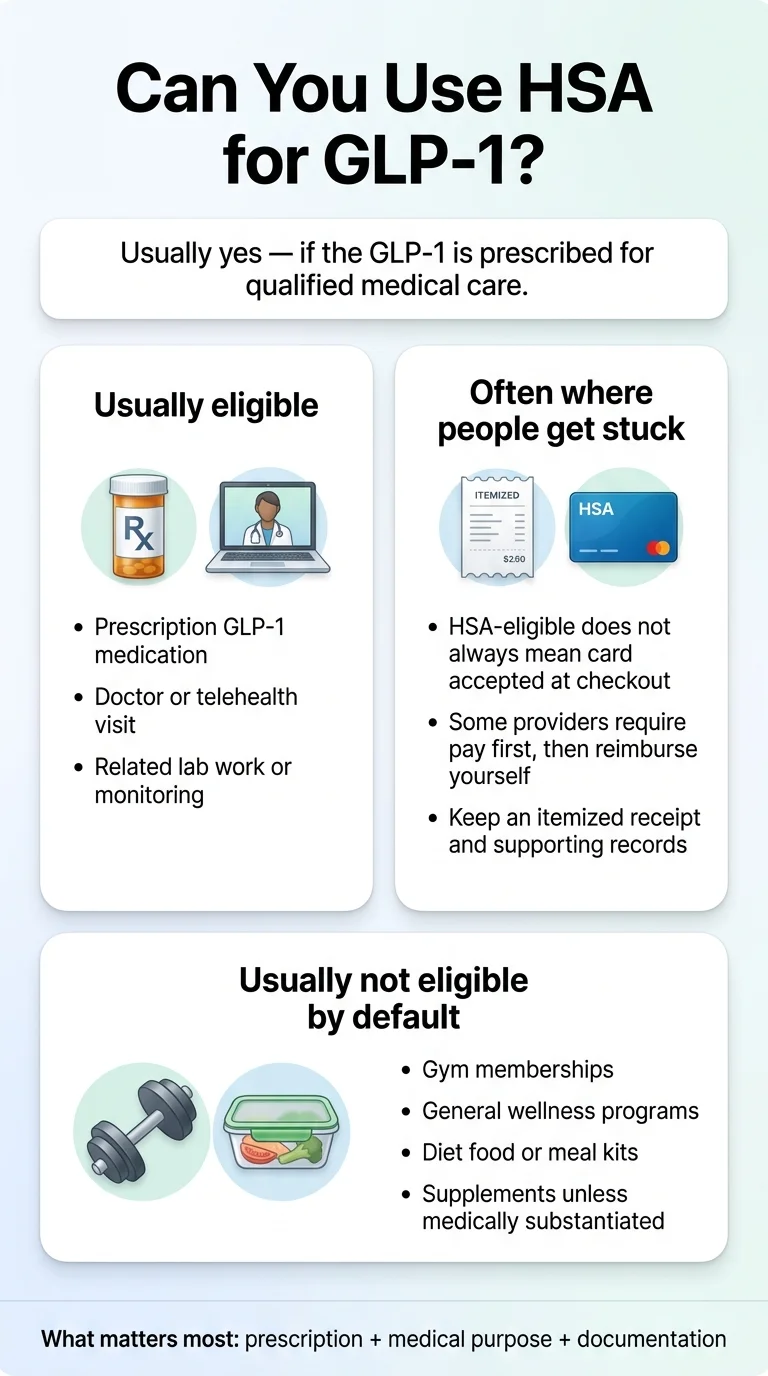

Yes — GLP-1 medications are generally HSA/FSA eligible when prescribed for a medical condition like obesity, type 2 diabetes, or overweight with comorbidities. The IRS considers them qualified medical expenses under Publication 502 and Publication 969. The part most guides miss: HSA-eligible does not always mean your HSA card will work at checkout.

Some of the most popular online GLP-1 providers — including Ro and Hims/Hers — don't accept HSA/FSA cards directly at checkout. You pay first, then reimburse yourself. This causes real confusion: cards get declined, people assume they're not eligible, and they give up or switch providers needlessly.

That gap between eligible and accepted at checkout is where people panic, waste hours on hold, or leave hundreds in tax savings on the table. This guide closes that gap completely.

We'll cover the actual IRS rules, which conditions qualify, how to pay (card vs. reimbursement), which providers have the smoothest HSA/FSA workflows, how much you can save in your tax bracket, what documentation protects you if audited — and exactly what to do if your claim gets denied.

Sources: IRS Publication 502 (2025), IRS Publication 969 (2025), IRS Notice 2026-05, Revenue Procedure 2025-19. Last verified March 28, 2026.

Disclosure: Some links on this page are affiliate links. If you purchase through these links, we may earn a commission at no extra cost to you.

What you need to use HSA for GLP-1:

- A valid prescription from a licensed clinician

- An itemized receipt showing the medical expense

- Documentation of medical purpose (diagnosis on file with your provider)

- A Letter of Medical Necessity when your administrator asks — get it proactively regardless; it takes minutes

What matters most: prescription + medical purpose + documentation. Source: The RX Index, 2026.

At a Glance: What's HSA/FSA Eligible for GLP-1 — and What's Not

| Expense | Usually HSA-Eligible? | What to Keep on File | Common Friction Point |

|---|---|---|---|

| Prescription GLP-1 (Wegovy, Zepbound, Ozempic, Mounjaro, Rybelsus, Saxenda) | ✅ Yes | Rx + itemized receipt | Vague receipt or missing diagnosis documentation |

| Compounded semaglutide or tirzepatide | ⚠️ Yes with docs | Rx + receipt + LMN strongly recommended | FSA administrators may request extra proof of medical necessity |

| Telehealth consultation (for GLP-1 prescription) | ✅ Yes | Visit documentation + receipt | Card-processing or documentation mismatch at checkout |

| Lab work ordered by prescriber | ✅ Yes | Lab receipt + ordering provider info | Missing order or itemized receipt |

| Medically supervised weight-loss program | ⚠️ Only if treating diagnosed disease | LMN + diagnosis + program itemization | Classified as “general wellness” instead of medical treatment |

| Coaching/app fee bundled with medication | ⚠️ Depends on billing | Itemized receipt separating medical from non-medical | Billed as “wellness” or “lifestyle” rather than medical care |

| Gym membership | ❌ Usually no | N/A | IRS allows only when treating a specific diagnosed condition |

| Supplements, special foods, meal replacements | ❌ Usually no | N/A | IRS allows only when recommended as treatment for a specific condition |

Sources: IRS Publication 502, IRS Publication 969, IRS FAQ on nutrition/wellness expenses

If your GLP-1 is prescribed and your diagnosis is documented, you're on solid ground. The rest of this guide is about making sure the process actually works — because the rules and the payment systems don't always cooperate.

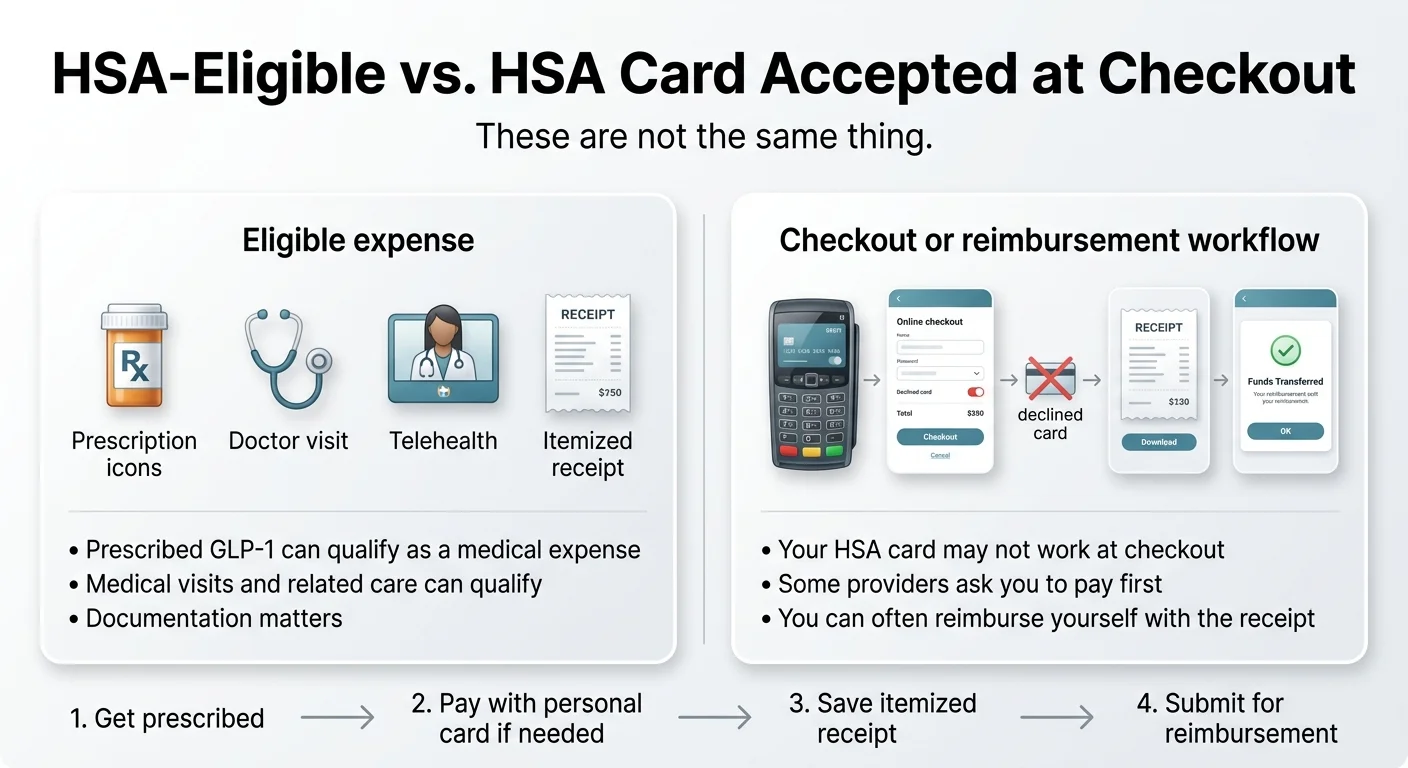

The #1 Mistake: Confusing “HSA-Eligible” With “My HSA Card Will Work”

A GLP-1 expense can be 100% legitimate under IRS rules and still fail when you swipe your HSA card. It happens regularly — and it doesn't mean you're doing anything wrong. It means the provider's payment system isn't set up to process HSA/FSA transactions at checkout.

Here's what actually happens at major providers:

Ro

Does not accept HSA/FSA cards directly at checkout. Their FAQ directs users to pay with a personal card first, then download an itemized receipt and submit for reimbursement. Their documentation is clean and administrator-friendly.

Hims and Hers

Recommends the same pay-then-reimburse workflow. Their support pages say to use a regular credit or debit card, then submit for reimbursement. If you try an HSA card, your provider may request additional documentation before processing.

MEDVi

States they accept HSA and FSA payments directly at checkout. For cash-pay compounded options, direct card acceptance can eliminate reimbursement paperwork entirely.

The takeaway: Many popular online GLP-1 providers use a pay-then-reimburse model. If your HSA card gets declined, it's almost certainly a payment-system issue — not an eligibility issue. Don't panic. Pay with your regular card, keep the receipt, and reimburse yourself. The tax savings are identical either way.

This distinction matters because forums are full of people who gave up or switched providers after a card decline, thinking they weren't eligible. One Reddit user described setting aside $2,500 in HSA funds specifically for GLP-1 treatment, only to discover at checkout that the provider wouldn't take the card. They were eligible the whole time — the payment system just didn't support it.

HSA-eligible and HSA card accepted at checkout are not the same thing. Source: The RX Index, 2026.

If direct HSA card swipe is your top priority, your options are narrower. If you're comfortable paying first and reimbursing yourself (which takes 3–10 business days with most HSA administrators), your choices open up significantly.

If you know you want GLP-1, you have HSA funds, and you need a provider with clean documentation and insurance support:

Ro offers FDA-approved GLP-1 medications with clean itemized receipts designed for easy HSA/FSA reimbursement. Their insurance concierge also helps fight for coverage, which can reduce your out-of-pocket HSA spend.

Check Your Eligibility on Ro →What the IRS Actually Says About Using HSA for GLP-1

The IRS doesn't mention “GLP-1” by name — it doesn't need to. The rules are broader.

Under IRS Publication 969, HSA funds can be used for “qualified medical expenses” as defined by Section 213(d) of the Internal Revenue Code. Publication 502 defines those expenses as costs for the “diagnosis, cure, mitigation, treatment, or prevention of disease.”

Prescription medications treating a diagnosed medical condition fall squarely into that definition. Here's what that means for GLP-1:

GLP-1 prescribed for type 2 diabetes

Qualified medical expense. The prescription itself is typically sufficient documentation.

GLP-1 prescribed for obesity (BMI 30+)

Qualified medical expense. A Letter of Medical Necessity strengthens your documentation.

GLP-1 prescribed for overweight (BMI 27+) with a comorbidity

Qualified medical expense when the diagnosis is documented. Comorbidities include hypertension, sleep apnea, high cholesterol, PCOS, cardiovascular disease, or prediabetes.

GLP-1 prescribed "for weight loss" without a documented condition

This is where it gets risky. Some wellness clinics don’t put a medical diagnosis code in your chart. The prescription is legal — but the weak documentation makes reimbursement harder and audit defense weaker.

The IRS also explicitly addresses weight-loss programs: they qualify only when used to treat a specific disease diagnosed by a physician. General weight loss for appearance or wellness does not qualify.

The rule of thumb: Prescription + medical diagnosis + documentation = you're good. Vague “wellness” billing without a diagnosis code = you're exposed.

What about the 20% penalty?

This is what scares people away from using HSA for GLP-1 — and the fear is usually unfounded if you do the basics right.

If you withdraw HSA money for something that turns out not to be a qualified medical expense, you'll owe income tax on the amount plus an additional 20% tax penalty (before age 65). A $299 non-qualified withdrawal could cost you $60+ in penalties on top of regular taxes.

But here's the reassuring part: GLP-1 medications clearly qualify when prescribed for a medical condition. The penalty only becomes a risk when someone skips the basics — no prescription, no diagnosis, no records. Do those three things and you have nothing to worry about.

Which Medical Conditions Make Your GLP-1 HSA/FSA Eligible?

Not all prescriptions are created equal in the eyes of your HSA administrator.

✅ Green light — prescription alone is usually sufficient

- Type 2 diabetes

- Cardiovascular disease risk reduction (when prescribed for this indication)

✅ Green light with documentation recommended (get an LMN)

- Obesity (BMI 30+)

- Overweight (BMI 27+) with hypertension

- Overweight with high cholesterol or dyslipidemia

- Overweight with obstructive sleep apnea

- Overweight with cardiovascular disease

- Overweight with type 2 diabetes

- Insulin resistance

- Metabolic syndrome

- Prediabetes

⚠️ May qualify with strong documentation

- PCOS (polycystic ovary syndrome) — off-label but increasingly documented

- Binge eating disorder

- Non-alcoholic fatty liver disease (NAFLD)

❌ Does not qualify

- Cosmetic weight loss without a medical diagnosis

- “Body optimization” or “metabolic reset” programs without medical codes

- Prescriptions from clinics that don't document conditions in your medical chart

The important nuance: The IRS doesn't focus on what a medication is FDA-approved for — it focuses on what you're actually treating. If your provider documents a real diagnosis and prescribes GLP-1 to treat it, the medical purpose is established regardless of whether it's on-label or off-label.

Ask your prescribing provider: “Is there a diagnosis code (ICD-10) in my chart for the condition you're treating?” If the answer is yes, you're in strong position. If they hesitate, that's a red flag for HSA purposes.

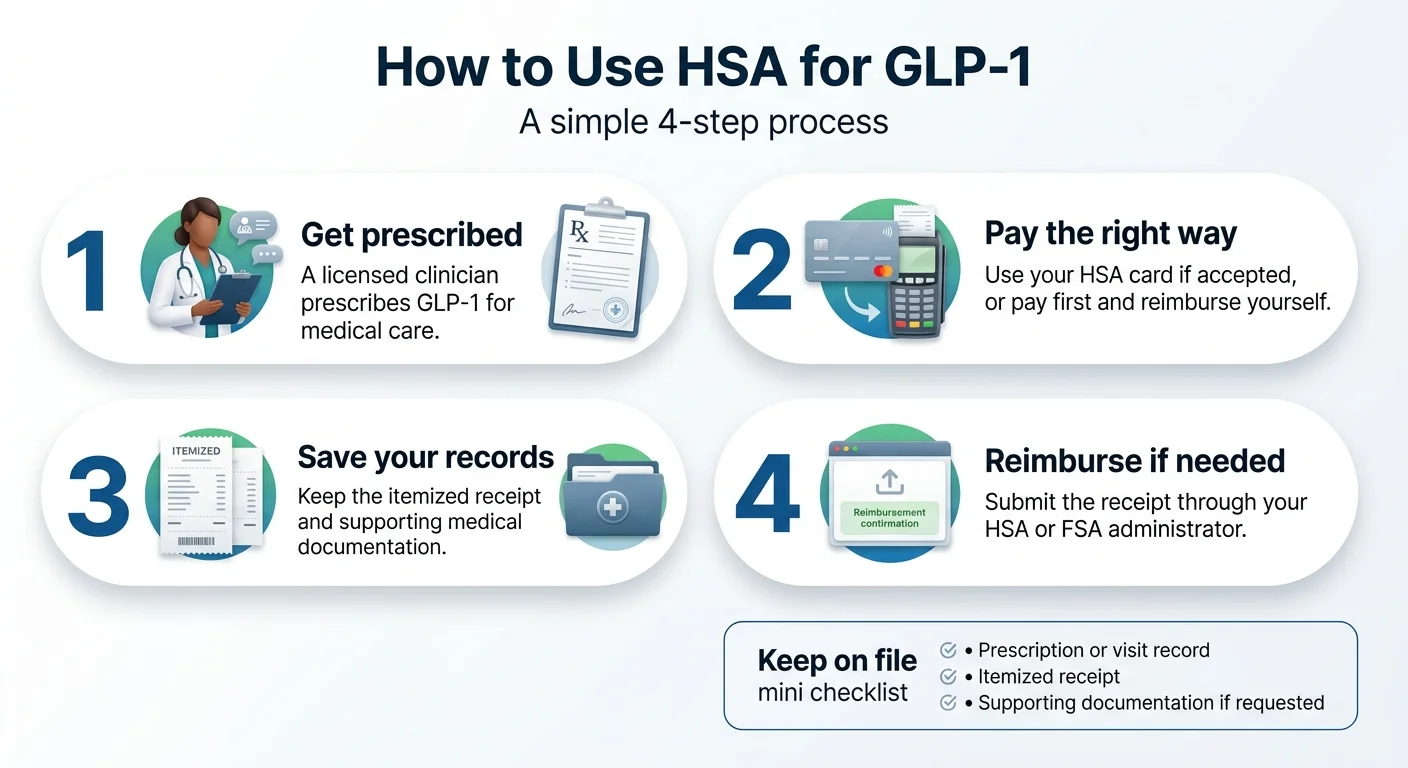

How to Actually Pay for GLP-1 With Your HSA or FSA: 4 Steps

Whether you're swiping a card or reimbursing yourself, this is the process.

The 4-step process for using HSA funds for GLP-1 medication. Source: The RX Index, 2026.

Get a prescription tied to a medical diagnosis

Make sure your prescribing provider — whether in-person or telehealth — documents a qualifying medical condition in your chart. Not "patient wants to lose weight" but "patient diagnosed with obesity (E66.01) and prescribed semaglutide for treatment." Reputable providers do this automatically. If yours doesn't document a diagnosis, find a different provider.

Pay for your medication (card or personal payment)

Option A — Direct HSA/FSA card: If the provider accepts it, swipe your card. Done. Option B — Pay and reimburse (more common for online GLP-1): Pay with your personal credit or debit card. You'll reimburse yourself in Step 4. The tax savings are identical either way.

Save your documentation (non-negotiable)

- ☐Itemized receipt showing medication name, dosage, cost, and date

- ☐Prescription documentation from your provider

- ☐Letter of Medical Necessity (LMN) — request this when your provider writes the prescription. It takes minutes.

- ☐Visit documentation for any telehealth or in-person consultations

- ☐Lab results if labs were ordered as part of your treatment

Submit for reimbursement (if you paid with personal card)

Log into your HSA/FSA administrator's portal (HealthEquity, Fidelity, Optum, etc.). Submit a reimbursement claim with your itemized receipt, LMN (if requested), and prescription documentation. Most administrators process in 3–10 business days. Important: You cannot double-dip. An expense reimbursed from HSA/FSA cannot also be claimed as an itemized medical deduction.

Pro tip: Get your LMN at the same appointment where your provider writes the prescription. It takes them 2–3 minutes, costs you nothing, and protects you whether your administrator asks for it now or the IRS asks later. If you're using an online provider, message their clinical team through the patient portal.

Do You Need a Letter of Medical Necessity (LMN)?

The honest answer: it depends on your account type and your administrator.

For HSA users

You typically don't need one to make a purchase or submit a reimbursement. HSAs are “self-certified” — no gatekeeper approves each transaction. However, if the IRS audits your HSA distributions, you'll need to prove the expense was qualified. An LMN is your strongest proof.

For FSA users

More likely to be required upfront. FSA administrators actively review expenses and often request documentation before processing. Weight-management prescriptions are more likely to trigger a “please upload supporting documentation” request than diabetes prescriptions.

Our recommendation regardless of account type: Get one proactively. It takes minutes. It eliminates risk. Think of it as insurance for your insurance.

What a good LMN includes:

- Your name and date of birth

- Your diagnosed medical condition (with ICD-10 code if possible)

- The prescribed medication and why it's medically necessary

- Expected duration of treatment

- Your clinician's signature, credentials, and date

When you especially want one:

- Compounded GLP-1 medications (higher administrator scrutiny)

- Receipts that say “weight management program” instead of specific medication

- FSA plans with aggressive review processes

- Bundled programs where medication and coaching are billed together

- First-time reimbursement through a new administrator

How Pre-Tax Dollars Can Lower Your GLP-1 Cost

Here's where the math gets compelling.

When you pay for GLP-1 through your HSA or FSA, you're using pre-tax dollars. Most people with employer-sponsored HSAs or FSAs contribute through payroll, which means the full savings apply — both federal income tax and FICA (Social Security + Medicare at 7.65%).

Estimated savings at $299/month (typical compounded GLP-1 cost), payroll-funded HSA or FSA:

| Federal Tax Bracket | Est. Combined Rate | Monthly Savings | Annual Savings | Effective Monthly Cost |

|---|---|---|---|---|

| 12% | ~20% | ~$60 | ~$715 | ~$239 |

| 22% | ~30% | ~$89 | ~$1,064 | ~$210 |

| 24% | ~32% | ~$95 | ~$1,137 | ~$204 |

| 32% | ~40% | ~$119 | ~$1,425 | ~$180 |

Estimates assume payroll-funded HSA or FSA contributions. Actual savings vary by state taxes, filing status, and contribution method. This is not tax advice — consult your tax professional for your specific situation.

In the 22% bracket — which covers a wide range of American households — paying $299/month through HSA instead of after-tax dollars saves you over $1,000 per year. Same medication, same treatment, different wallet impact.

And HSAs have no time limit on reimbursement — if you've been paying for GLP-1 out-of-pocket, you may be able to reimburse yourself for past expenses as long as the expense occurred after your HSA was established.

At $299/month for compounded semaglutide through MEDVi — which accepts HSA/FSA cards directly — your effective cost can drop below $210/month after tax savings. No insurance required, no reimbursement paperwork.

See Current Pricing on MEDVi →HSA vs. FSA: What Actually Changes for GLP-1?

If you're not sure which account you have — or if the difference matters — here's the practical breakdown.

Health Savings Account (HSA)

- Requires High Deductible Health Plan (HDHP)

- 2026 limits: $4,400 individual / $8,750 family (+$1,000 catch-up if 55+)

- Funds roll over indefinitely — no expiration

- You own it even if you change jobs

- Self-certified — no pre-approval for purchases

- Triple tax advantage

- No time limit on reimbursement

Flexible Spending Account (FSA)

- Available through employer regardless of plan type

- 2026 limit: $3,400 (up to $680 carryover if employer allows)

- Use it or lose it at plan year-end

- Administrator actively reviews expenses

- May flag GLP-1 and request documentation

- No time-limit flexibility — plan your contributions carefully

| Feature | HSA | FSA |

|---|---|---|

| Funds expire? | Never | End of plan year |

| Pre-approval needed? | No | Often yes for weight-loss meds |

| 2026 individual limit | $4,400 | $3,400 |

| Rolls over? | Yes, fully | Limited ($680 max) |

| Requires HDHP? | Yes | No |

| Best for GLP-1? | ✅ Easier process | ⚠️ Works, more friction |

HSA wins on flexibility. If you're planning to use GLP-1 long-term, HSA is the better vehicle. If you have an FSA with money about to expire, GLP-1 medication is one of the best ways to use those funds before you lose them.

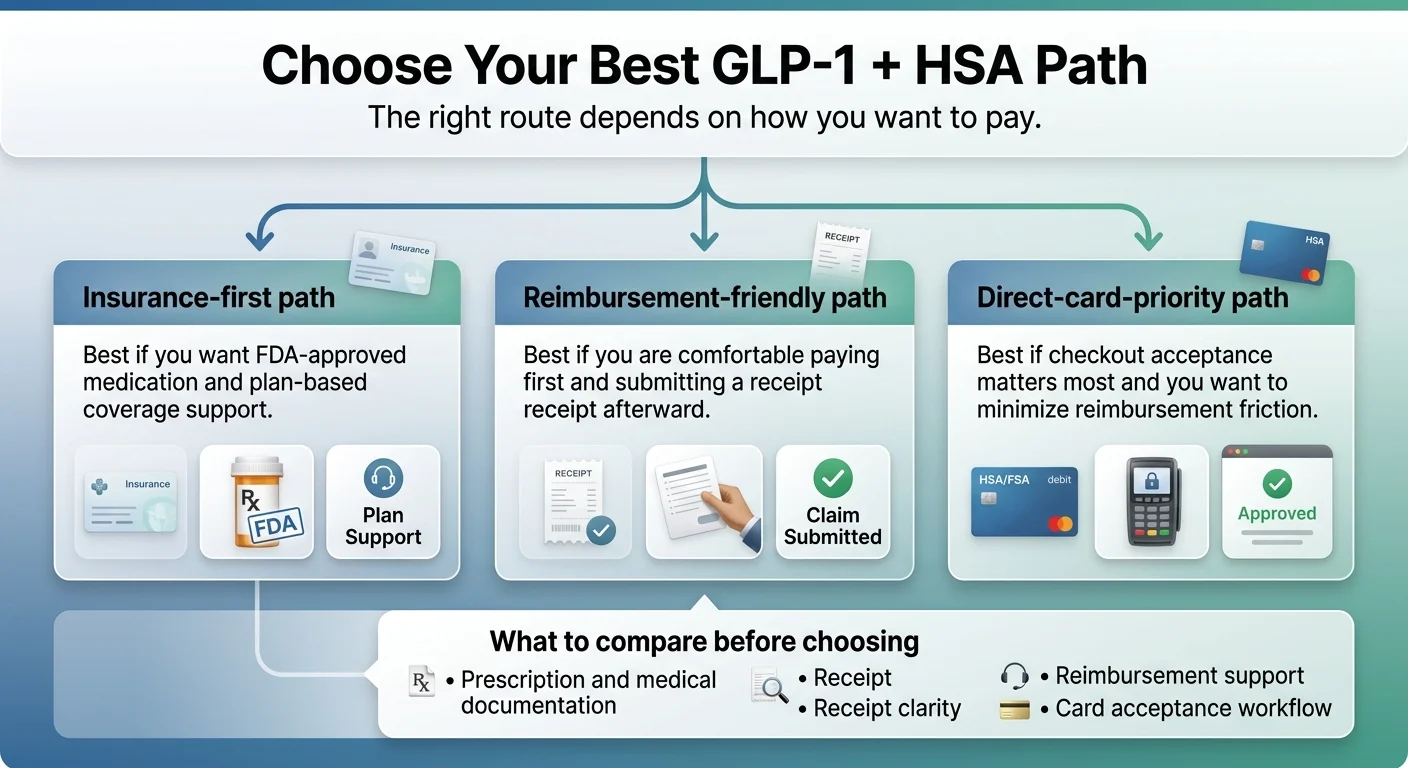

Which GLP-1 Providers Work Best With HSA/FSA?

Here's what we verified from each provider's payment policies and support documentation, as of March 2026.

| Provider | Direct HSA Card? | Reimbursement? | Medication Type | Best For |

|---|---|---|---|---|

| Ro | ❌ Pay first | ✅ Clean itemized receipt | FDA-approved only | Insurance path, cleanest docs |

| MEDVi | ✅ Accepts HSA/FSA | ✅ Yes | Compounded semaglutide & tirzepatide | Cash-pay, direct card, flat pricing |

| Hims/Hers | ⚠️ May need extra steps | ✅ Recommended path | FDA-approved + compounded | Broad medication selection |

| SkinnyRX | ✅ Accepts HSA/FSA | ✅ Yes | Compounded | Budget-conscious, straightforward |

Policies verified March 2026. Payment acceptance can change — confirm with your chosen provider before purchasing.

Three GLP-1 + HSA paths depending on insurance, budget, and checkout preference. Source: The RX Index, 2026.

If you have insurance and want the cleanest HSA path → Ro

Ro's Body Program works with your insurance to get brand-name, FDA-approved medications like Wegovy or Zepbound. If your insurance covers GLP-1s (even partially), you pay the copay — and that copay is an HSA-eligible expense. If you have a high-deductible plan, those costs count toward your deductible and are HSA-eligible. You're building toward your out-of-pocket maximum with pre-tax dollars.

Ro doesn't accept HSA cards at checkout — you pay first and get reimbursed. But their receipt documentation is clear and itemized, which is exactly what HSA administrators need to process a claim without pushback. Their insurance concierge also handles prior authorizations at no extra charge.

Best for: Someone with an HDHP + HSA who wants FDA-approved GLP-1 medications, insurance coordination, and the most defensible documentation trail for tax purposes.

Ro combines insurance navigation with clean receipt documentation built for HSA/FSA reimbursement. If you have insurance, this is the most efficient way to use pre-tax dollars for GLP-1 treatment.

Check Insurance Eligibility on Ro →If you're paying cash and want direct HSA card acceptance → MEDVi

MEDVi operates on a flat cash-pay model and accepts HSA/FSA payments directly. No insurance needed, no reimbursement paperwork. Their pricing: $299/month for compounded semaglutide, $399/month for tirzepatide, with first-month discounts.

Important context: Compounded GLP-1 medications are not FDA-approved — they're prescription medications prepared by compounding pharmacies. This doesn't change HSA/FSA eligibility (the IRS cares about the prescription and diagnosis, not FDA approval status), but some FSA administrators may request more documentation. Keep your LMN handy.

Best for: Cash-pay buyers with HSA/FSA who want direct card acceptance, predictable pricing, and no insurance complexity.

MEDVi accepts HSA/FSA cards directly at checkout — no reimbursement forms, no waiting. Flat $299/month for compounded semaglutide, all-in.

See If You Qualify on MEDVi →Not sure which path fits your situation?

The right choice depends on your insurance, budget, and what matters most. If you're still weighing FDA-approved vs. compounded, insurance vs. cash-pay, or you're just not sure where to start:

Take our free 60-second GLP-1 matching quiz. Tell us about your insurance, budget, and goals — we'll show you the provider path that fits.

Find My GLP-1 Path →Can You Use HSA for Ozempic, Wegovy, Mounjaro, Zepbound, and Others?

This comes up constantly, so let's answer each one directly.

Can you use HSA for Wegovy?

Yes. Wegovy (semaglutide) is FDA-approved for chronic weight management. When prescribed for obesity or overweight with comorbidities, it's a qualified medical expense. An LMN strengthens your documentation.

Can you use HSA for Zepbound?

Yes. Zepbound (tirzepatide) is FDA-approved for chronic weight management and sleep apnea. Same rules as Wegovy — prescription plus documented diagnosis makes it HSA/FSA eligible.

Can you use HSA for Ozempic?

Yes. Ozempic (semaglutide) is FDA-approved for type 2 diabetes. If prescribed for diabetes, your prescription alone is typically sufficient. If prescribed off-label for weight management, an LMN is recommended.

Can you use HSA for Mounjaro?

Yes. Mounjaro (tirzepatide) is FDA-approved for type 2 diabetes. Straightforward for diabetes; LMN recommended for off-label weight-management use.

Can you use HSA for Rybelsus or Saxenda?

Yes. Both are FDA-approved (Rybelsus for type 2 diabetes, Saxenda for weight management) and HSA/FSA eligible with a prescription for a qualifying condition.

Can you use HSA for compounded semaglutide or tirzepatide?

Compounded GLP-1 can qualify when lawfully prescribed. Because compounded drugs are not FDA-approved, expect more administrator scrutiny — especially from FSAs. An LMN is strongly recommended. See the compounded section below.

The bottom line: The IRS doesn't play medication favorites. What matters is the prescription, the diagnosis, and the documentation — not the brand name.

What about platform fees and membership costs?

The medication itself is the strongest HSA/FSA claim. Many providers bundle medication with platform fees, coaching, or membership costs. If the fee covers medical services (consultations, prescription management, clinical monitoring), it's generally eligible. If it covers coaching or wellness content, it's murkier. The safest approach: choose providers that itemize their receipts, and claim only the clearly medical portion.

Can You Use HSA for GLP-1 Prescribed Online or Through Telehealth?

Yes. A telehealth visit that is medical care — meaning a licensed provider diagnoses, treats, or prescribes for a medical condition — is a qualified medical expense.

Federal law now permanently allows HDHPs to cover telehealth services before the deductible is met without making you ineligible to contribute to an HSA. This became permanent for plan years beginning on or after January 1, 2025.

- Online consultations with providers like Ro and MEDVi are HSA-eligible medical expenses

- The prescription written during a telehealth visit carries the same weight as an in-person prescription for HSA purposes

- Follow-up visits, dose adjustments, and clinical check-ins are all qualified expenses

- Your HDHP can cover these telehealth visits before your deductible without jeopardizing HSA eligibility

You don't need to see a doctor in-person to use HSA funds for GLP-1.

Can You Use HSA for Compounded GLP-1 Medications?

Short answer: Compounded GLP-1 medications can qualify for HSA/FSA when lawfully prescribed to treat a medical condition. The IRS eligibility rules are the same as for brand-name medications.

The practical reality: While IRS eligibility is straightforward, the process has more friction than brand-name medications:

FSA administrators may apply more scrutiny

Brand-name medications have clear NDC codes and established billing. Compounded medications may trigger additional review or documentation requests.

Receipt quality matters more

A receipt that says "weight loss medication — $299" might get flagged. A receipt that identifies "compounded semaglutide injection, prescribed by [Provider Name] for treatment of obesity" is much cleaner.

Compounded medications are not FDA-approved

This doesn't change IRS eligibility, but it means choosing a reputable provider with properly licensed pharmacy partnerships matters — both for safety and for the quality of your documentation.

An LMN is practically essential

For brand-name medications, the prescription often speaks for itself. For compounded, always have an LMN on file.

Want the cleanest FDA-approved path with insurance support?

Check Ro's Current Options →Prefer the cash-pay route with direct HSA card acceptance?

See MEDVi Pricing →New for 2026: The OBBBA Expanded HSA Eligibility

If you were previously told you couldn't open an HSA because your health plan didn't qualify — check again.

The One, Big, Beautiful Bill Act (OBBBA, signed July 4, 2025) expanded HSA eligibility in several important ways starting in 2026:

Bronze and catastrophic ACA Marketplace plans are now HSA-compatible

Even if they don't meet traditional HDHP deductible requirements. The IRS clarified in Notice 2026-05 that this applies whether or not the plan was purchased through an Exchange.

Telehealth before deductible is permanent

Your HDHP can cover telehealth visits (including GLP-1 consultations) before you meet your deductible without disqualifying your HSA eligibility. Permanent for plan years starting on or after January 1, 2025.

Direct Primary Care arrangements are now HSA-compatible

You can use HSA funds to pay periodic DPC fees without jeopardizing your eligibility.

What this means for GLP-1: If you have a bronze or catastrophic plan through healthcare.gov and didn't think you could use an HSA, you now can. Open an HSA, contribute pre-tax dollars (up to $4,400 individual / $8,750 family in 2026), and use them for GLP-1 medications and related medical expenses.

Sources: IRS Notice 2026-05, Revenue Procedure 2025-19

What to Do If Your HSA or FSA Claim Gets Denied

It happens. And it's almost always fixable. Here's the playbook.

Check whether the receipt is too vague

The most common denial reason. "Wellness program — $299" gets flagged. "Compounded semaglutide injection, prescribed by Dr. Smith for treatment of obesity — $299" is much harder to deny. Contact your provider and request an itemized receipt with the medication name, dosage, and prescribing provider.

Add an LMN if you haven't already

If your administrator asks for additional documentation, an LMN is usually what they need. Contact your prescribing provider and request one. Most telehealth providers can generate this through their patient portal.

Separate medical from non-medical charges

If your provider bills medication, consultation, and coaching under a single line item, ask them to break it out. The medication and medical consultation are the strongest HSA/FSA claims. Bundled "program" billing creates ambiguity.

Switch from card to reimbursement

If your HSA card keeps getting declined at a specific merchant, stop fighting the payment system. Pay with your personal card and submit for reimbursement through your administrator's portal. Same tax-free result, less checkout frustration.

Ask the administrator exactly what's missing

Don't guess. Call your HSA/FSA administrator and ask: "What specific document or information do you need to approve this claim?" They're required to tell you. Once you know the gap, fill it.

If all else fails

Pay out-of-pocket and claim the expense as a medical deduction on Schedule A (medical expenses exceeding 7.5% of your AGI are deductible if you itemize). Less tax-efficient than HSA/FSA but still recovers some cost. Remember: an expense reimbursed from HSA/FSA cannot also be claimed as an itemized deduction.

Tired of reimbursement friction? MEDVi and SkinnyRX accept HSA/FSA cards directly at checkout — no reimbursement forms needed.

7 Mistakes That Waste Your HSA Money on GLP-1

Using a clinic that doesn’t document a diagnosis

Some online clinics prescribe GLP-1s for “weight loss” without putting a medical diagnosis code in your chart. The prescription is legal — but the weak documentation makes reimbursement harder and audit defense weaker.

Not getting an LMN

It takes your provider minutes. It protects you for up to a year. There’s no good reason not to have one.

Forgetting about payroll tax savings

If your HSA or FSA is funded through payroll, you save your federal tax rate plus 7.65% FICA on every dollar. In the 22% bracket, that’s roughly 30% total savings — not 22%.

Trying to use a Limited-Purpose FSA (LPFSA) for GLP-1

If you have an HSA + LPFSA combo, the LPFSA covers dental and vision only. Use your HSA for GLP-1, not the LPFSA. Getting this wrong means penalties.

Over-contributing to FSA

FSAs are use-it-or-lose-it. If you contribute $3,400 expecting to use GLP-1 all year and stop treatment in June, you could forfeit over $1,000. HSAs don’t have this problem since funds roll over.

Not keeping receipts

Even if the transaction goes through cleanly, the IRS can audit your HSA distributions. Keep prescription + receipt + LMN with your tax records through your normal tax-record retention period.

Assuming a card decline means you’re not eligible

Card decline = payment-system issue. It does not mean the expense isn’t qualified. Pay with your personal card and reimburse yourself.

Common Friction Points From Real Users

Based on what we see in Reddit threads, support forums, and HSA administrator communities, these are the most frequent pain points — and they're all solvable:

“My HSA card was declined at checkout.”

Payment-processing issue, not an eligibility issue. The merchant category code may not match what your HSA administrator expects. Pay with a personal card and submit for reimbursement — same tax result.

“My FSA administrator is asking for extra documentation.”

FSA administrators are more hands-on than HSA administrators. Having your LMN ready turns a multi-week back-and-forth into a same-day resolution.

“The receipt just says ‘weight loss program’ and my administrator rejected it.”

Ask your provider for an itemized receipt that specifically names the medication. Most providers can regenerate receipts with more detail if you ask.

“I didn’t realize I could reimburse myself later.”

If you have an HSA and have been paying for GLP-1 out-of-pocket, you can submit those past receipts for reimbursement anytime. There’s no deadline as long as the expense occurred after your HSA was established.

“I’m not sure if my compounded GLP-1 will get flagged.”

It might get an extra look, especially from FSA administrators. But with a clear prescription, diagnosis documentation, and an LMN, compounded medications are a defensible HSA expense. The IRS focuses on medical purpose, not FDA approval status.

Frequently Asked Questions

Can I use my HSA for GLP-1 medication?

Yes, when prescribed to treat a diagnosed medical condition like obesity, type 2 diabetes, or overweight with related health issues. The IRS considers prescription GLP-1s a qualified medical expense under Publication 502 and Publication 969. Keep your prescription, itemized receipt, and ideally a Letter of Medical Necessity.

Can I use my HSA card for GLP-1 at checkout?

It depends on the provider. Some providers accept HSA/FSA cards directly (MEDVi, SkinnyRX). Others recommend paying with a personal card and submitting for reimbursement (Ro, Hims/Hers). A card decline at checkout does not mean the expense isn't HSA-eligible — it means the payment system doesn't support it. Pay with a personal card and reimburse yourself for the same tax-free result.

Are GLP-1s HSA eligible?

Prescription GLP-1 medications are generally qualified medical expenses when prescribed for medical care — obesity, type 2 diabetes, cardiovascular disease risk reduction, or overweight with comorbidities. Compounded GLP-1 products qualify under the same IRS rules but may involve more administrator scrutiny and require stronger documentation.

Are GLP-1s FSA eligible?

Yes, under the same IRS rules as HSA. FSA administrators may require more upfront documentation, including a Letter of Medical Necessity, particularly for weight-management prescriptions. Keep your prescription, itemized receipt, and LMN ready.

Is Wegovy HSA eligible?

Yes. Wegovy (semaglutide) is FDA-approved for chronic weight management. When prescribed for obesity or overweight with comorbidities, it is a qualified medical expense. A Letter of Medical Necessity strengthens your documentation since it is a weight-management medication.

Is Zepbound HSA eligible?

Yes. Zepbound (tirzepatide) is FDA-approved for chronic weight management and obstructive sleep apnea. Same rules as Wegovy — prescription plus documented diagnosis makes it HSA/FSA eligible.

Is Ozempic HSA eligible?

Yes. Ozempic (semaglutide) is FDA-approved for type 2 diabetes. If prescribed for diabetes, your prescription alone is typically sufficient documentation. If prescribed off-label for weight management, a Letter of Medical Necessity is recommended.

Is Mounjaro HSA eligible?

Yes. Mounjaro (tirzepatide) is FDA-approved for type 2 diabetes. Straightforward for diabetes; LMN recommended for off-label weight-management use.

Can I use HSA for compounded semaglutide or tirzepatide?

Compounded GLP-1 medications can qualify for HSA/FSA when lawfully prescribed to treat a medical condition. The IRS eligibility rules are the same as for brand-name medications. However, because compounded drugs are not FDA-approved, some plan administrators apply more scrutiny. A Letter of Medical Necessity is strongly recommended, and your receipt should clearly identify the medication by name.

Do I need a Letter of Medical Necessity for GLP-1 HSA claims?

Not always required upfront, especially for HSAs (which are self-certified). But we recommend getting one proactively. FSA administrators are more likely to request one. It takes minutes to get from your provider and eliminates the biggest source of claim denials. For compounded GLP-1, it is practically essential.

Can I reimburse myself from my HSA for GLP-1?

Yes. There is no time limit on HSA reimbursements. You can reimburse yourself months or years after paying, as long as the expense occurred after your HSA was established, was for a qualified medical expense, and was not reimbursed from another source or claimed as a tax deduction.

What if my HSA or FSA claim for GLP-1 gets denied?

Most denials are fixable. Check if your receipt is too vague — request an itemized receipt from your provider that names the medication specifically. Add a Letter of Medical Necessity if you don't have one. Separate medical charges from non-medical bundled fees. Call your administrator and ask exactly what documentation they need to approve the claim.

What are the 2026 HSA contribution limits?

$4,400 for individual HDHP coverage, $8,750 for family coverage, plus an additional $1,000 catch-up contribution for those 55 and older. Source: IRS Revenue Procedure 2025-19.

Does telehealth count for HSA with GLP-1?

Yes. Telehealth medical visits are qualified medical expenses. Additionally, federal law now permanently allows HDHPs to cover telehealth before the deductible without disqualifying your HSA eligibility. Online GLP-1 prescriptions from providers like Ro and MEDVi carry the same weight as in-person prescriptions for HSA purposes.

How We Verified This Page

- IRS guidance: Publication 502, Publication 969, IRS FAQ on medical expenses related to nutrition/wellness/general health, Notice 2026-05 (OBBBA guidance), Revenue Procedure 2025-19 (2026 HSA/HDHP limits), Form 8889 instructions

- Provider payment policies: Verified HSA/FSA acceptance, reimbursement workflows, and receipt availability for Ro, MEDVi, Hims/Hers, and SkinnyRX as of March 2026

- Legislative changes: OBBBA provisions affecting HSA eligibility, telehealth safe harbor

- User experience patterns: Reviewed Reddit threads and support forums about HSA card declines, reimbursement friction, and LMN requirements at GLP-1 providers

Provider policies and HSA/FSA rules change. We update this page whenever card acceptance, reimbursement flow, contribution limits, or IRS guidance changes. If you spot something outdated, contact our editorial team.

Your GLP-1 + HSA Action Plan

What if you don't have an HSA or FSA?

Check whether your plan qualifies for an HSA — especially with the 2026 OBBBA expansion. Bronze and catastrophic plans purchased through the Marketplace are now HSA-compatible. If your plan qualifies, you can open an HSA and start contributing pre-tax dollars this year.

If HSA/FSA isn't an option, you can still claim GLP-1 costs as a medical deduction on Schedule A (medical expenses exceeding 7.5% of your AGI are deductible if you itemize). Just remember: an expense claimed as a deduction can't also be reimbursed from an HSA/FSA.

For a full breakdown of every way to reduce your GLP-1 costs, see our complete guide to GLP-1 pricing without insurance.

Still not sure which GLP-1 program is right for you?

Take our free 60-second matching quiz. Tell us about your insurance, budget, and goals — we'll show you the provider path that fits. The money is already in your account. The medication is available. The IRS allows it.

The RX Index provides independent research and comparisons for GLP-1 weight loss medications. We may earn a commission when you use links on this page — this does not affect our editorial recommendations or the price you pay. We are not doctors, tax advisors, or financial professionals. This content is for informational purposes only and is not tax, medical, or financial advice. Consult your healthcare provider for medical decisions and your tax professional for guidance specific to your situation. All IRS rules referenced are current as of March 2026 — verify with IRS.gov for the most current guidance.

Written by The RX Index Editorial Team · Last verified March 28, 2026 · More GLP-1 guides →