GLP-1 Providers That Take FSA: 8 Options Compared for 2026

By The RX Index Editorial Team · Last updated: April 2, 2026 · Affiliate disclosure · Editorial standards

Which GLP-1 providers actually accept your FSA card at checkout — and which ones make you pay first and file a claim later.

Bottom line, April 2026

We compared 8 major GLP-1 providers to find out which ones actually accept FSA. MEDVi and Shed both accept FSA/HSA cards at checkout and are both listed on FSA Store — the largest dedicated marketplace for FSA-eligible products. Ro is the strongest pick for FDA-approved GLP-1 with insurance support, but Ro does not accept FSA cards at checkout — they provide clean itemized receipts for reimbursement.

Best FSA card at checkout: MEDVi — FSA Store listed, accepts FSA/HSA directly, compounded semaglutide from $179/mo

Best FDA-approved + insurance: Ro — no FSA card accepted, but clean receipts for reimbursement and full insurance concierge

Best direct-card alternative: Shed — FSA Store listed, accepts HSA/FSA cards, $100 off first month

Listed on FSA Store · No reimbursement paperwork · Month-to-month

Which GLP-1 Providers Accept FSA? Quick Comparison

Every provider below offers GLP-1 treatment that can qualify as an FSA-eligible medical expense when prescribed to treat a diagnosed condition. But “eligible” and “accepted at checkout” are two completely different things.

| Provider | FSA Card at Checkout? | Starting Price | Medication Type |

|---|---|---|---|

| MEDVi | ✅ Yes — FSA Store listed | $179/mo | Compounded + FDA-approved |

| Ro | ❌ No — reimbursement only | Varies (insurance) | FDA-approved only |

| Shed | ✅ Yes — FSA Store listed | $199+/mo | Compounded + brand |

| LifeMD | ✅ HSA/FSA-friendly | Varies | FDA-approved + compounded |

| Hers | ⚠️ Reimbursement-first | $199+/mo | Compounded + brand |

| SkinnyRX | ✅ Accepts FSA/HSA cards | $199+/mo | Compounded |

| Fridays | ⚠️ Mixed signals — verify | $199+/mo | Compounded |

| Eden | ⚠️ Eligible, reimbursement-focused | $129–$229/mo | Compounded + brand |

Policies checked April 2026. ✅ = consistent public evidence of FSA card acceptance across provider pages or FSA Store listing. ⚠️ = contradictory language or reimbursement-first model. ❌ = provider FAQ explicitly states FSA/HSA cards not accepted. Confirm directly before purchasing.

What “Takes FSA” Actually Means — and Why Most Provider Pages Are Misleading

Prescribed GLP-1 treatment generally qualifies as an FSA-eligible medical expense when used to treat a diagnosed disease like obesity or type 2 diabetes. But “eligible” and “accepted at checkout” are two completely different things. This is the single biggest source of confusion in this space — and it’s the reason your FSA card might decline even when the medication itself qualifies.

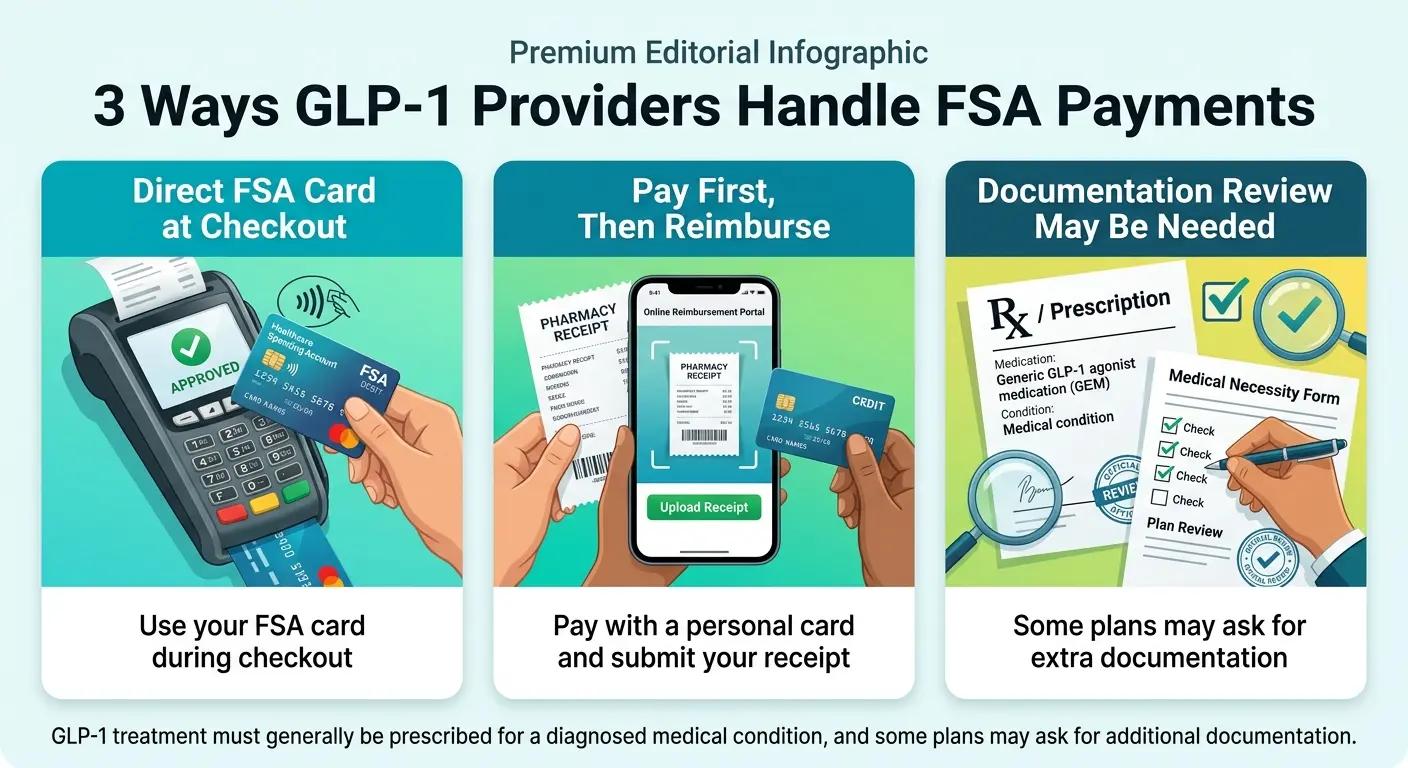

Direct FSA card at checkout (the easiest path)

You enter your FSA debit card number during checkout, just like a regular debit card. The charge processes immediately. No reimbursement paperwork, no claim submission, no waiting. Providers in this category: MEDVi, Shed, and SkinnyRX.

Reimbursement-first (works, but requires a step)

You pay with a personal credit or debit card, then log into your FSA portal, upload your itemized receipt, and submit a claim. Your FSA administrator reimburses you — typically within a few business days. Providers in this category: Ro and Hers.

"Eligible" but documentation-heavy (verify before you pay)

The provider says "FSA/HSA eligible" on their marketing page, but the actual payment flow may require a Letter of Medical Necessity, may trigger a documentation review, or may not process your FSA card at all. Providers: Eden and Fridays (Fridays says you can use FSA cards on one page, but describes a cash-pay reimbursement model on another).

A practical way to think about it: “FSA-eligible” is like saying a restaurant accepts credit cards. Of course it does. But does this specific restaurant’s card reader actually work with your card? That’s the question — and that’s what our comparison above answers.

Direct card checkout · No reimbursement steps

Best GLP-1 Provider for FSA: Pick by Situation

Not everyone reading this page is solving the same problem. Ask yourself two questions first:

Do you have insurance that might cover GLP-1?

If yes → Check Ro first. Insurance + FSA reimbursement is usually the cheapest total path. If no (or you're not sure) → Go cash-pay with a direct FSA checkout provider.

Is direct FSA card checkout important, or is reimbursement fine?

If direct card is important → MEDVi, Shed, or SkinnyRX. If reimbursement is fine → Your options open up significantly (Ro, Hers, Eden, and more).

Listed on FSA Store, accepts FSA cards at checkout. Compounded semaglutide starts at $179/mo, plus FDA-approved Wegovy and Zepbound.

Ro doesn't accept FSA cards, but their itemized receipts are designed for clean reimbursement. If your insurance covers Wegovy or Zepbound, Ro handles the prior authorization — and your out-of-pocket cost could be significantly lower than cash-pay.

LifeMD's site labels its weight-management program "HSA/FSA Eligible" and its telehealth consent says qualified medical expenses may be paid with HSA/FSA cards. Also FSA Store listed.

Their receipt download flow is simple and built into the app. One of the most polished consumer experiences in the space.

SkinnyRX at $199+/mo with direct FSA card, or Eden starting at $129/mo (promotional, reimbursement-focused).

“I’m not sure which path fits me.”

Take our free 60-second GLP-1 matching quiz and we’ll factor in your FSA status, budget, insurance, and medication preference.

Provider Breakdowns

MEDVi

Best Overall for FSA Card Checkout

MEDVi is our top pick for FSA users because it directly addresses the problem you searched for: you can use your FSA debit card at checkout without filing reimbursement paperwork. Starting at $179/mo for compounded semaglutide injections, MEDVi is one of the most accessible GLP-1 providers for cash-pay patients — and FSA makes it even more affordable.

Verified (April 2026) — Sources: MEDVi official site; Health-E Commerce press release, October 21, 2025

- ✓Site says "HSA/FSA Approved" and accepts FSA/HSA debit cards at checkout for eligible medical expenses

- ✓Listed on FSA Store and HSA Store (Health-E Commerce partner) — stronger evidence than any marketing tagline

- ✓Compounded semaglutide injection: $179 first month, $299/mo ongoing

- ✓Compounded tirzepatide injection: $349/mo

- ✓Compounded semaglutide tablet: $249/mo | Compounded tirzepatide tablet: $279/mo

- ✓FDA-approved Wegovy / Zepbound: $99 membership + medication cost

- ✓Month-to-month, no long-term contracts

| Medication | Month 1 | Ongoing | Format |

|---|---|---|---|

| Compounded semaglutide injection | $179 | $299/mo | Injectable |

| Compounded tirzepatide injection | $349 | $349/mo | Injectable |

| Compounded semaglutide tablet | $249 | $249/mo | Oral |

| Compounded tirzepatide tablet | $279 | $279/mo | Oral |

| FDA-approved Wegovy / Zepbound | $99 membership + med | Varies by dose | Injectable / oral |

What the process looks like

You complete a health assessment online. A licensed provider reviews it (typically within 24 hours). If approved, you confirm your treatment plan, enter your FSA debit card at checkout, and your medication ships in temperature-controlled packaging. Month-to-month. Done.

Your effective cost with FSA tax savings: If you’re in a combined 27% tax bracket, that $299/mo ongoing cost effectively becomes $218/mo after FSA tax savings. At a 38% combined rate, it drops to $185/mo.

Check Your Eligibility on MEDVi — FSA Store Listed, Accepts FSA at Checkout

FSA card accepted. No reimbursement forms. Month-to-month.

Check Your Eligibility on MEDVi →Ro

Best for FDA-Approved GLP-1 With Insurance Support

Ro is the strongest GLP-1 provider for readers who want FDA-approved medication, insurance navigation, and the clinical credibility that comes with brand-name prescriptions. The caveat for this page: Ro’s own FAQ explicitly states they do not accept HSA/FSA cards at this time.

But they provide clean, itemized receipts designed for easy reimbursement. And if your insurance covers Wegovy or Zepbound, Ro handles the prior authorization. Your out-of-pocket cost is what you’d reimburse from your FSA — and in many cases, this ends up lower than the cash-pay price at direct-checkout providers.

Verified: Ro FAQ — April 2026

Ro does not accept HSA/FSA cards at checkout. Ro provides itemized receipts for HSA/FSA reimbursement.

How FSA reimbursement works with Ro (step by step)

Complete Ro's intake and get prescribed

Ro checks your insurance coverage and handles prior authorization

Pay your copay/coinsurance with a personal credit or debit card

Download your itemized receipt from your Ro account

Log into your FSA portal, submit the receipt, and get reimbursed

The hidden advantage of Ro + FSA:

If your insurance covers Wegovy at a $50 copay, you’re paying $50/mo out of pocket for FDA-approved, brand-name GLP-1 medication. Reimburse that $50 from your FSA and your effective after-tax cost drops to roughly $33/mo. That’s less than many gym memberships — for physician-supervised weight management with serious clinical evidence behind it.

See if Wegovy or Zepbound is covered before you pay cash anywhere

Shed

Strong Direct-Checkout Alternative — FSA Store Partner

Shed is an FSA Store partner with some of the clearest public FSA language we found. Shed’s help page explicitly says it accepts HSA and FSA cards for prescription purchases, and they’re listed on FSA Store as a weight-loss partner.

Verified (April 2026) — Source: Shed help center FSA/HSA page; Health-E Commerce partnership announcement, October 2025

- ✓Listed alongside MEDVi and LifeMD on FSA Store as a telehealth GLP-1 offering

- ✓Help center explicitly states acceptance of HSA/FSA cards for prescription purchases

- ✓$100 off the first month of any GLP-1 program for new users

- ✓Unlimited provider access — month-to-month

- ✓Compounded and brand-name options available

Who Shed is best for: FSA holders who want a direct-checkout experience backed by explicit FSA card acceptance language and FSA Store validation. A solid middle ground between MEDVi’s aggressive pricing and Ro’s insurance-focused approach.

LifeMD

Best Branded Telehealth With FSA Support

LifeMD is one of the more established telehealth brands offering GLP-1 programs, and their FSA/HSA positioning is consistent across their site. Their weight-management page is labeled “HSA/FSA Eligible,” their telehealth consent says qualified medical expenses may be paid with HSA/FSA cards, and they’re listed on FSA Store alongside Shed and MEDVi.

Sources: LifeMD weight management page; LifeMD telehealth consent page; FSA Store listings

- ✓Weight-management page labeled "HSA/FSA Eligible"

- ✓Telehealth consent says qualified medical expenses may be paid with HSA/FSA cards

- ✓Listed on FSA Store — independently validated

- ✓FDA-approved and compounded pathways available

- ✓Insurance support available

Who LifeMD is best for: Readers who want a recognizable, mainstream telehealth brand with FDA-approved medication options and insurance support — and the added confidence of FSA Store listing.

External link · Not an affiliate

Hers

Best When Reimbursement Is Fine

Hers is not the cleanest direct-FSA-card path, but it’s a strong option if you’re comfortable paying first and reimbursing yourself. Their official FSA/HSA page explicitly describes the reimbursement flow: pay with your regular card, download your receipt from the “orders” tab, and submit it to your FSA administrator.

Source: Hers official FSA/HSA page

FSA/HSA card payments may require additional steps from your provider. Hers recommends using a standard card and submitting receipts afterward.

- ·Compounded + brand-name GLP-1 options available

- ·Compounded injectable from $199+/mo

- ·Receipt download built into the app — simple reimbursement flow

Who should look elsewhere: If you specifically want to swipe your FSA card and be done — no reimbursement step at all — MEDVi, Shed, or SkinnyRX is a better fit.

SkinnyRX

Budget Compounded With FSA Card Support

SkinnyRX’s FAQ states they accept HSA/FSA cards, and their product pages display “FSA/HSA eligible” badges. At $199+/mo for compounded semaglutide, they’re one of the more affordable options with direct-card support.

Sources: SkinnyRX FAQ; SkinnyRX semaglutide product page

- ✓FAQ confirms FSA/HSA card acceptance at checkout

- ✓Product pages display "FSA/HSA eligible" badges

- ✓Detailed published guide on HSA/FSA eligibility for GLP-1

- ✓Cash-pay telehealth model — no insurance processing

- ✓Compounded semaglutide and tirzepatide available

Who SkinnyRX is best for: FSA holders who want a lower compounded price point and want to use their FSA card directly rather than dealing with reimbursement.

Fridays

Mixed Signals — Verify Before You Commit

Fridays earns a spot because of their competitive pricing ($199+/mo for compounded semaglutide), but we’re flagging an inconsistency in their FSA messaging. One official Fridays page states that users can use their HSA/FSA card to pay for compounded GLP-1 medications. But their FAQ describes the service as cash-pay and says some members can use HSA/FSA funds for reimbursement. Those two statements don’t fully align.

Sources: Fridays FAQ; Fridays compounded medications page; Fridays pricing page

Who Fridays is best for: FSA holders interested in Fridays’ program who are willing to confirm the FSA card experience before committing.

Eden

Good for Budget-Conscious, Paperwork-Tolerant Readers

Eden advertises FSA/HSA eligibility and offers some of the most aggressive first-month pricing in the space. On a 3-month plan, compounded semaglutide starts at $129 the first month, then $209/mo ongoing. Monthly plans start at $149 first month, then $229/mo. They also offer flat-rate pricing across all dosages.

Sources: Eden GLP-1 treatments page; Eden weight-loss page

- ·Says "FSA/HSA eligible" on weight-loss page

- ·Separate content describes reimbursement steps and LMN documentation

- ·Eden is in the "eligible but documentation-heavy" category — works, but expect paperwork rather than a clean card swipe

- ·Flat-rate pricing: same price regardless of dose level (unusual and useful for budgeting)

- ·3-month plan: from $129 first month, $209/mo ongoing · Monthly: from $149 first month, $229/mo

Who Eden is best for: Readers who are comfortable with reimbursement and possible LMN documentation, want competitive pricing for compounded GLP-1, and value the flat-rate dosing model.

How Much You’ll Actually Save Using FSA for GLP-1

Using FSA to pay for GLP-1 medication effectively gives you a 20–37% discount because you’re paying with pre-tax dollars. That’s not a promotional discount that expires — it’s a structural tax advantage that applies every single month.

| Combined Tax Bracket | Monthly GLP-1 Cost | Annual Tax Savings | Effective Monthly Cost |

|---|---|---|---|

| 22% + 5% = 27% | $179/mo (MEDVi) | $580 | $131/mo |

| 24% + 5% = 29% | $299/mo (MEDVi ongoing) | $1,040 | $212/mo |

| 32% + 6% = 38% | $299/mo (MEDVi ongoing) | $1,363 | $186/mo |

| 24% + 5% = 29% | $50/mo (Ro copay w/ insurance) | $174 | $36/mo |

FSA contributions also avoid FICA taxes (7.65%), which many calculators miss. When included, total tax savings reach 35–40% for most earners. Over a year of GLP-1 treatment, that’s $700–$1,400 back compared to paying with after-tax cash.

Direct FSA card checkout · FSA Store listed

What Documents You Need to Use FSA for GLP-1 (Without Getting Denied)

The most common reason FSA claims get denied isn’t eligibility — it’s paperwork. The medication qualifies. Your account has funds. But your plan administrator flags the charge because the receipt is missing a detail or the expense category doesn’t match.

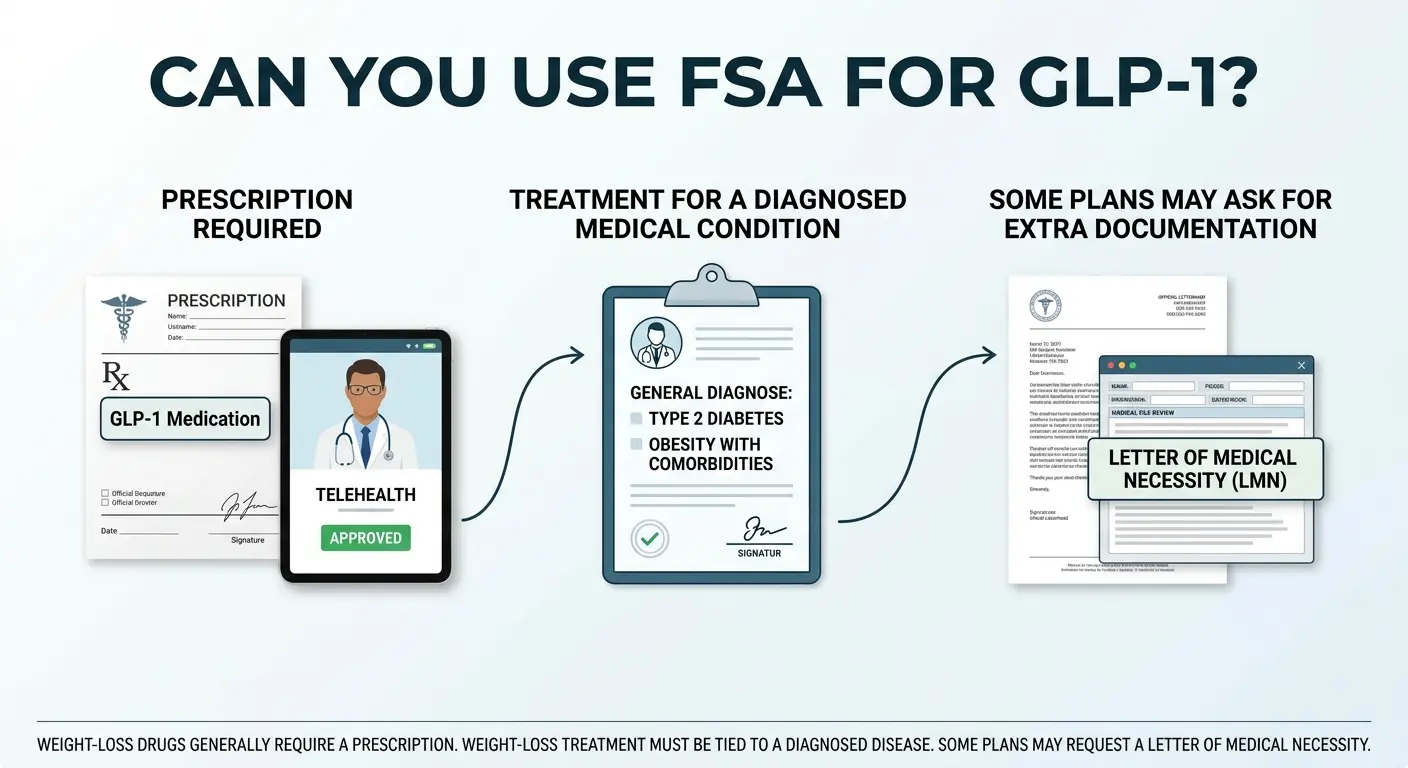

1. Your prescription

A valid prescription from a licensed healthcare provider for a diagnosed medical condition — obesity (BMI 30+), overweight with comorbidities (BMI 27+), type 2 diabetes, or metabolic syndrome. IRS guidance ties weight-loss expense eligibility to treatment of a specific disease diagnosed by a physician. Every telehealth GLP-1 provider on our list generates a prescription during intake.

Source: IRS medical expense FAQ

2. An itemized receipt with these five elements

Your receipt must include: (1) provider or pharmacy name, (2) date of service or purchase, (3) description of the service or medication, (4) patient name, and (5) amount paid. Missing any one of these is the most common denial trigger. Most providers generate compliant receipts automatically — but check before you submit.

3. Letter of Medical Necessity (LMN)

A short letter from your prescribing provider confirming that the GLP-1 medication is treating a diagnosed medical condition. Not every FSA administrator requires one, but weight-management prescriptions are more likely to trigger a request. FSA Store's own eligibility guidance notes that weight-loss programs may require an LMN.

Source: FSA Store eligibility list

4. Any diagnosis documentation

Documentation of your diagnosis (e.g., ICD-10 code E66.01 for obesity) from your provider. Keep digital copies of everything — if you're ever audited, you'll need them.

What to request from your provider’s support team (before you pay)

Copy this message:

“Can you confirm that your receipts include itemized medical expense details suitable for FSA reimbursement? Can you also provide a Letter of Medical Necessity if my plan administrator requests one?”

This single step eliminates most downstream friction.

Is the membership fee FSA eligible?

This is a gray area. Some GLP-1 programs bundle a platform or membership fee with the medical consultation and medication. The IRS considers medical consultations and prescription medications as qualified expenses. Platform fees not directly tied to a specific medical service may not qualify. The workaround: ask your provider to issue a receipt that itemizes the medical components separately from any non-medical charges.

FSA card accepted at checkout with compliant receipts

Can You Use FSA for GLP-1? (IRS Rules Explained)

Under IRS rules, FSA funds can pay for “qualified medical expenses” — costs to diagnose, treat, mitigate, or prevent a disease. For GLP-1 medication, your expense generally qualifies when:

Is Semaglutide FSA Eligible?

Prescription semaglutide is generally FSA-eligible when prescribed to treat a diagnosed disease such as obesity or type 2 diabetes. This applies to brand-name FDA-approved forms and compounded semaglutide from licensed pharmacies.

| Semaglutide Form | FDA-Approved? | Generally FSA Eligible? |

|---|---|---|

| Wegovy (injection) | ✅ Yes | ✅ Yes |

| Wegovy (oral tablet) | ✅ Yes | ✅ Yes |

| Ozempic | ✅ Yes | ✅ Yes |

| Rybelsus | ✅ Yes | ✅ Yes |

| Compounded semaglutide | ❌ Not FDA-approved | ✅ Generally yes |

Is Tirzepatide FSA Eligible?

Prescription tirzepatide is generally FSA-eligible when prescribed to treat a diagnosed disease. Same principle as semaglutide — the key factor is medical necessity, not the specific medication form.

| Tirzepatide Form | FDA-Approved? | Generally FSA Eligible? |

|---|---|---|

| Zepbound | ✅ Yes | ✅ Yes |

| Mounjaro | ✅ Yes | ✅ Yes |

| Compounded tirzepatide | ❌ Not FDA-approved | ✅ Generally yes |

Can You Use FSA for Compounded GLP-1 Medications?

Generally, yes. Compounded GLP-1 medications prescribed for a diagnosed medical condition can qualify as FSA-eligible expenses. IRS Publication 502 covers amounts paid for prescribed drugs as qualified medical expenses when they’re used to treat a specific disease diagnosed by a physician.

FSA plan administrators vary

Some process compounded medication claims automatically. Others may request a Letter of Medical Necessity. Having your LMN ready eliminates this friction.

Compounded GLP-1 medications are not FDA-approved

The FDA has stated that compounded drugs are not FDA-approved and are not reviewed for safety, effectiveness, or quality before marketing. This does not automatically disqualify them from FSA eligibility, but it does mean they carry different risk and regulatory considerations than brand-name products like Wegovy or Zepbound.

The practical difference for your FSA

Whether you choose compounded semaglutide at $179/mo or FDA-approved Wegovy through insurance, both are prescribed medications for a medical condition. The difference is clinical pathway and cost — not the underlying FSA eligibility principle. Always confirm with your specific plan administrator.

What If Your FSA Card Gets Declined or Your Claim Is Denied?

A declined FSA card does not mean you’re ineligible. It almost always means one of three things: the provider’s payment system isn’t configured for FSA card processing (merchant category code issue), your FSA balance is insufficient, or the IIAS system flagged the purchase for manual review.

If your card declines at checkout:

Don't panic. Pay with a personal credit or debit card instead.

Download your itemized receipt immediately.

Log into your FSA portal and submit a manual reimbursement claim with your receipt.

If your plan requires one, attach your Letter of Medical Necessity.

You get the same tax benefit through reimbursement — it just takes an extra step.

If your reimbursement claim is denied:

Most common reasons: Missing receipt details (check all five required elements), the expense was categorized as “wellness” or “general health” instead of “prescription medication,” or the plan administrator wants an LMN you didn’t include.

Fix it: Get your LMN from your provider. Make sure your receipt clearly describes the charge as a prescription medication for a diagnosed condition. Resubmit. If denied again, call your plan administrator directly — a short phone call often resolves what a web portal cannot.

Script to use if your plan administrator pushes back:

“I’m submitting a reimbursement claim for a prescribed GLP-1 medication. My licensed healthcare provider prescribed this for treatment of [obesity / type 2 diabetes / metabolic syndrome]. I have an itemized receipt from the provider and a Letter of Medical Necessity if needed. Under IRS Publication 502, prescribed medications for diagnosed medical conditions are qualified medical expenses. Can you help me understand what specific documentation you need to process this claim?”

This frames the expense in IRS language, references the specific publication, and asks them what they need rather than arguing.

MEDVi — FSA card accepted at checkout

FSA vs. HSA for GLP-1: Which Should You Use First?

If you have access to both accounts, use your FSA first. FSA funds are use-it-or-lose-it — most plans require you to spend them by the end of the plan year or you lose the balance. HSA funds roll over indefinitely and can be invested for growth.

| Feature | FSA | HSA |

|---|---|---|

| Funds roll over? | ❌ Most expire (up to $680 carryover in 2026) | ✅ Roll over indefinitely |

| 2026 contribution limit | $3,400 per employer | $4,400 individual / $8,750 family |

| Requires high-deductible plan? | No | Yes |

| Tax advantage | Federal + state income tax + FICA | Federal + state income tax + FICA |

| Best GLP-1 strategy | Use for current-year treatment costs | Preserve for long-term or future costs |

2026 limits per IRS inflation adjustments.

Important compatibility note: A general-purpose health FSA usually makes you ineligible to contribute to an HSA in the same year, unless your FSA is a limited-purpose FSA (dental/vision only). Check with your benefits administrator. Source: IRS Publication 969

The optimal play: Max out your FSA for this year’s GLP-1 costs. If your annual GLP-1 expense exceeds your FSA balance, use HSA for the overflow.

FSA Deadline Approaching? Here’s How to Use Expiring Funds for GLP-1

If your FSA plan year is ending soon, GLP-1 medication is one of the highest-value ways to spend those dollars before they disappear. A single month of treatment can use $179–$349 of FSA money that would otherwise go back to your employer.

The math is simple: If you have $500 sitting in your FSA with no other planned medical expenses, that money evaporates at your deadline. Two months of GLP-1 treatment at $179/mo uses $358 of those funds for physician-supervised weight management — funds you’d otherwise lose entirely.

MEDVi operates month-to-month with no long-term contracts. Start with one month using your expiring FSA funds, see how you respond, and decide from there. That’s the lowest-risk way to convert FSA dollars into a real health outcome.

$179/mo · Month-to-month · No contracts

Is FSA, HSA, or Insurance the Best Way to Pay for GLP-1?

Use insurance first when:

Your plan covers Wegovy or Zepbound with a reasonable copay. Check through Ro, which handles prior authorization. Then reimburse your copay from FSA/HSA for the additional tax savings.

Use FSA when:

Your insurance doesn't cover GLP-1, you're paying cash anyway, and you have FSA funds available (especially if they're expiring). Swipe your FSA card at a direct-checkout provider like MEDVi or Shed.

Use HSA when:

You don't have FSA, or your FSA funds are already spoken for. HSA works identically for tax purposes but rolls over indefinitely — no deadline pressure.

Go straight cash-pay when:

You don't have FSA/HSA access and your insurance doesn't cover GLP-1. Compare cash-pay prices across providers — see our cheapest GLP-1 providers guide.

How We Verified Every Provider on This List

We don’t repeat marketing claims. We also don’t label a provider “FSA-confirmed” just because their sales page says so. Here’s what we reviewed:

Official payment policy pages

The FAQ or pricing page where the provider states what payment methods are accepted. If the provider says "we do not accept HSA/FSA cards" (like Ro), we report that exactly. If they say "FSA eligible" on one page but describe reimbursement on another (like Fridays), we flag the inconsistency.

FSA Store / HSA Store marketplace listings

Whether the provider is listed on FSA Store or HSA Store, operated by Health-E Commerce. Being listed means Health-E Commerce has included the provider in their FSA/HSA-eligible marketplace — stronger evidence than any self-reported marketing claim.

Provider help centers and support documentation

Help pages, support articles, and published guides that describe the FSA/HSA payment flow in detail.

IRS source material

Publication 502 (medical and dental expenses), Publication 969 (HSA rules), IRS FAQ on medical expenses related to nutrition and general health, and 2026 contribution limits.

Our labeling system:

✅ Direct card / FSA Store listed — consistent public evidence across provider pages or FSA Store/HSA Store listings.

⚠️ Mixed signals / verify — contradictory language or evidence points more toward reimbursement than direct card acceptance.

❌ Not accepted — provider’s own official FAQ explicitly states they don’t accept FSA/HSA cards.

We re-check provider payment policies monthly. If a provider changes their FSA acceptance status, this page is updated within the same cycle.

Frequently Asked Questions

Can I use my FSA card to pay for GLP-1 online?

Yes — GLP-1 medications prescribed for a diagnosed medical condition generally qualify as FSA-eligible medical expenses under IRS Publication 502. Some providers accept FSA debit cards directly at checkout (MEDVi, Shed, SkinnyRX), while others require you to pay with a personal card and submit receipts for reimbursement (Ro, Hers). Check your specific provider's payment page before purchasing.

Is semaglutide FSA eligible?

Prescription semaglutide is generally FSA-eligible when prescribed to treat a diagnosed disease such as obesity or type 2 diabetes. This applies to Wegovy, Ozempic, Rybelsus, and compounded semaglutide. Some FSA plan administrators may request a Letter of Medical Necessity for weight-management prescriptions.

Is tirzepatide FSA eligible?

Prescription tirzepatide is generally FSA-eligible when prescribed to treat a diagnosed disease. This includes Zepbound, Mounjaro, and compounded tirzepatide. Your plan administrator may request supporting documentation for weight-management use.

Is Wegovy FSA eligible?

Yes. Wegovy is FDA-approved for chronic weight management and is generally FSA-eligible when prescribed. Both the injection and the newer oral tablet form qualify as prescription medication expenses.

Is Ozempic FSA eligible?

Yes. Ozempic is FDA-approved for type 2 diabetes and generally qualifies as an FSA-eligible prescription. If prescribed off-label for weight management, your FSA administrator may request a Letter of Medical Necessity.

Is Zepbound FSA eligible?

Yes. Zepbound is FDA-approved for chronic weight management and generally qualifies as an FSA-eligible medical expense when prescribed.

Can I use FSA for compounded semaglutide?

Compounded semaglutide prescribed for a diagnosed medical condition generally qualifies as an FSA-eligible expense. However, compounded medications are not FDA-approved and some FSA plan administrators may request additional documentation such as a Letter of Medical Necessity. Having an LMN ready before you pay is the safest approach.

Do I need a Letter of Medical Necessity for GLP-1 FSA?

It depends on your FSA plan administrator. Many FSA purchases go through without one, but weight-management prescriptions are more likely to trigger documentation requests than diabetes prescriptions. Having an LMN on file before you pay is the safest approach. Most telehealth GLP-1 providers will write one if you ask.

Are GLP-1 membership fees FSA eligible?

Generally, only the medical portions of a GLP-1 program qualify — the consultation, prescription, and medication itself. Platform or membership fees not tied to a specific medical service may not qualify. Ask your provider to itemize the receipt so medical expenses are separated from non-medical charges.

Which GLP-1 providers also take HSA?

Most providers that accept FSA also accept HSA, since both cards process through similar payment networks. MEDVi, Shed, SkinnyRX, and LifeMD accept HSA/FSA. Ro does not accept either card directly but provides receipts for HSA/FSA reimbursement.

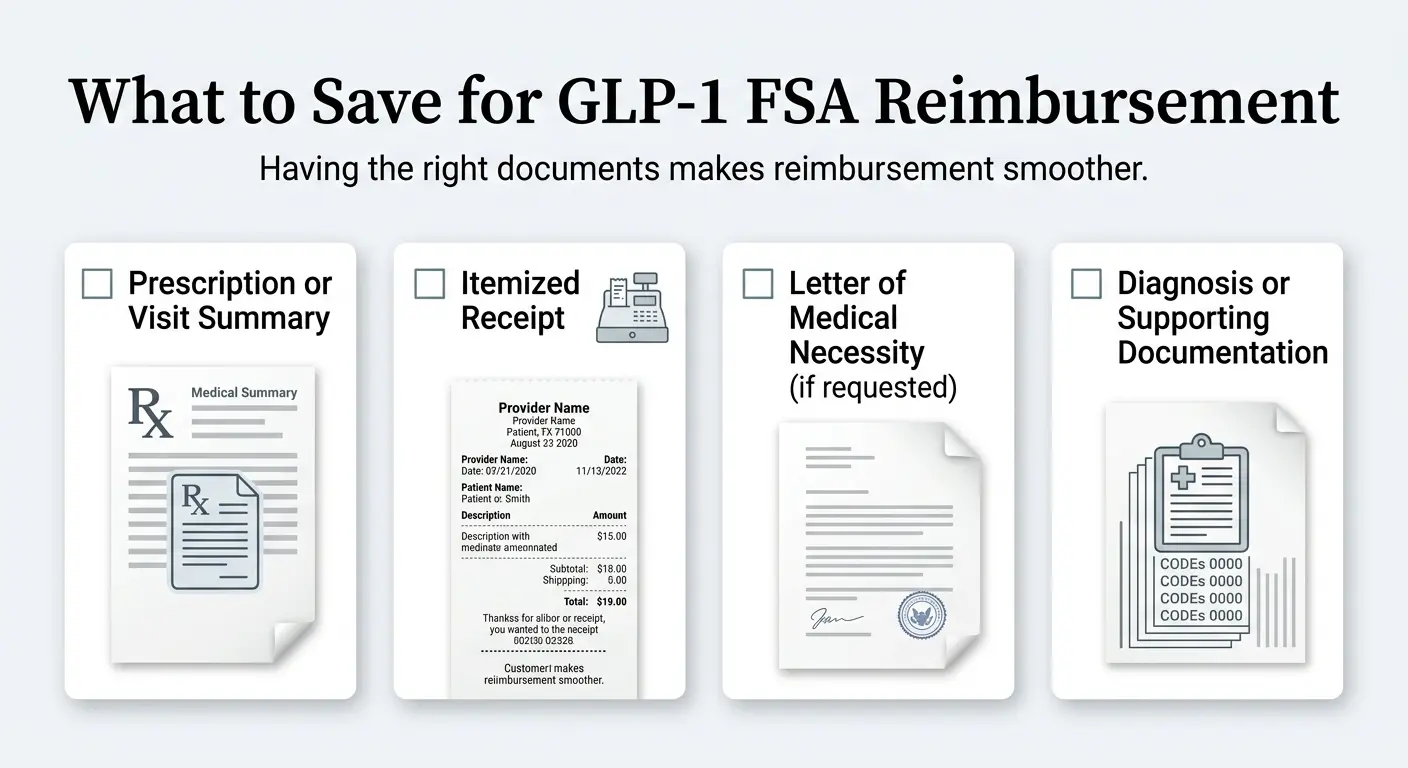

What should I save for FSA GLP-1 reimbursement?

Save four things: your prescription or provider visit summary, an itemized receipt showing provider name, date, service description, patient name, and amount paid, a Letter of Medical Necessity if your plan administrator requires one, and any diagnosis documentation from your provider. Keep digital copies of everything.

What happens if my FSA plan denies the GLP-1 claim?

Most denials are documentation problems, not eligibility problems. Check for missing receipt information, add a Letter of Medical Necessity if you did not include one, make sure the receipt describes the expense as a prescription medication for a medical condition, and resubmit. If denied again, call your plan administrator directly.

Still Not Sure Which GLP-1 Program Is Right for You?

We’ll ask about your budget, FSA/HSA access, insurance coverage, medication preference, and your state — then match you to the provider that fits your specific situation. No email required. No sales pitch.

Take the Free 60-Second GLP-1 Matching Quiz

Answer 5 questions about your insurance, FSA/HSA, and budget — get a personalized recommendation with your pre-tax savings calculated.

Get My Personalized GLP-1 Match →60 seconds · No email required · No sales pitch

Related guides

- GLP-1 Providers That Take HSA: 7 Verified Picks (2026)

- Best GLP-1 Providers That Accept Insurance: 6 Verified Picks (2026)

- Best Online Wegovy Provider: 7 Legit Options (2026)

- Cheapest GLP-1 Without Insurance: Full Cash-Pay Comparison

- Best Telehealth for Wegovy: Full Provider Breakdown

- How to Appeal a GLP-1 Insurance Denial (Step-by-Step)

Sources

- IRS Publication 502 — Medical and Dental Expenses

- IRS Publication 969 — HSAs and Other Tax-Favored Health Plans

- IRS FAQ — Medical Expenses Related to Nutrition, Wellness, and Health

- IRS 2026 Tax Inflation Adjustments

- Ro HSA/FSA FAQ

- Hers Official FSA/HSA Page

- MEDVi Official Site

- SkinnyRX FAQ

- FSA Store — Official FSA-Eligible Product Marketplace

- Health-E Commerce Press Release — October 21, 2025

- FDA — Compounded GLP-1 Medications

Affiliate disclosure: We may earn commissions from MEDVi, Ro, Shed, Hers, SkinnyRX, Fridays, and Eden links on this page. Rankings are based on our verified FSA payment policy methodology — not commission rates. Full disclosure →

Medical disclaimer: This content is for informational purposes only and does not constitute medical advice. GLP-1 medications require a prescription. Compounded medications are not FDA-approved. FSA/HSA eligibility depends on your specific plan administrator — confirm before purchasing.

Tax disclaimer: This content is informational and does not constitute tax or financial advice. Consult a tax professional for your specific situation.

Last updated: April 2, 2026 · Written by The RX Index Editorial Team