How to Get Insurance to Cover GLP‑1: 7 Approval Paths (2026)

Disclosure: Some links on this page are affiliate links. If you purchase through these links, we may earn a commission at no extra cost to you.

Updated March 2026 · Prices last verified March 2026 · Sources: FDA prescribing information, CMS, KFF, insurer criteria documents, manufacturer coverage tools

How to Get Insurance to Cover GLP-1: The Bottom Line

Here's how to get insurance to cover GLP-1 without wasting weeks on dead-end requests: match the right drug to the right FDA-approved use, document the insurer's exact criteria before your doctor submits the prior authorization, and know your backup plan before you need it.

Most people get stuck because they ask for the wrong drug, use the wrong diagnosis code, or skip paperwork their insurer quietly requires. We've mapped out 7 legitimate coverage paths based on your diagnosis and insurance type — and for each one, we'll tell you exactly what to submit, what gets denied, and what to do if it doesn't work.

The quick version of what we found:

- Commercial insurance coverage is much stronger for FDA-approved type 2 diabetes uses than for weight loss, though restrictions are common even for diabetes. Among firms with 200+ workers, 19% cover GLP-1s primarily for weight loss; among firms with 5,000+ workers, the figure is 43% (KFF, 2025 Employer Health Benefits Survey). Prior authorization is nearly always required, and the rules got stricter in 2026.

- Medicare is finally entering the picture. The new Medicare GLP-1 Bridge launches July 2026 with a $50/month copay for eligible beneficiaries. This is a genuine game-changer for millions of people who've been shut out.

- Medicaid varies wildly by state. Only 13 states cover GLP-1s for obesity as of January 2026 — down from 16 after budget cuts hit California, Pennsylvania, and others.

- If insurance fails entirely, FDA-approved GLP-1s now start at $149/month through manufacturer direct pricing for eligible patients. That's not a typo. The Wegovy pill launched in late 2025 and dropped the floor on pricing. (Note: many manufacturer cash-pay offers exclude government insurance beneficiaries — check program terms.)

Below, we'll walk through every path, every common denial, every appeal tactic, and every cost-reduction trick we know. If your insurance can cover this, we'll help you get it approved. If it can't, we'll show you the fastest affordable alternative.

Tell us your insurance, goals, and budget. We match you to the right program.

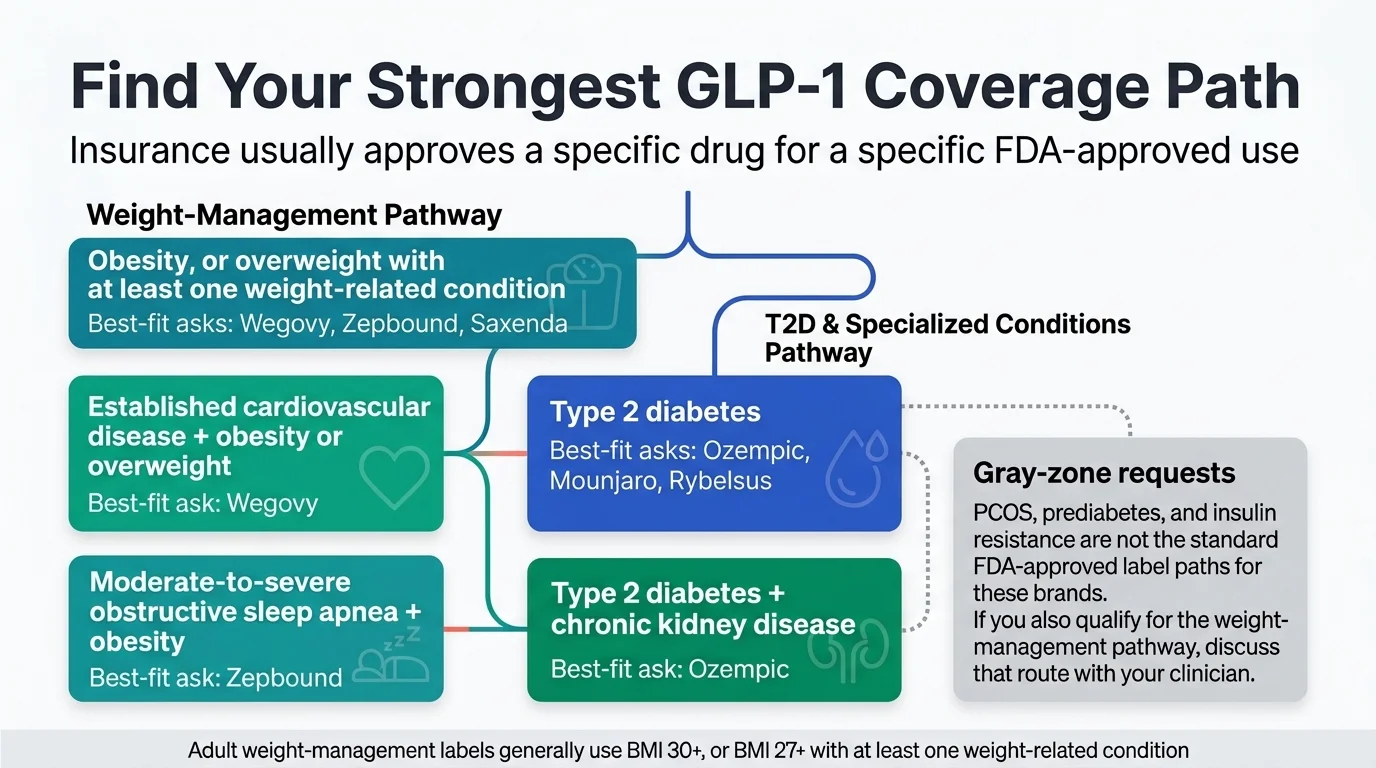

Which GLP-1 Coverage Path Gives You the Best Odds?

This is the part most guides get wrong. They tell you to “check your formulary” and “talk to your doctor” — generic advice that doesn't account for the fact that which drug you ask for, and which diagnosis it's tied to, changes everything about whether insurance says yes.

Insurance companies don't approve or deny “GLP-1s.” They approve or deny a specific drug for a specific FDA-approved use. Ozempic for diabetes? Almost always covered. Ozempic for weight loss? Usually denied — because that's off-label.

We built this table to show you the 7 real paths that actually get approvals. Find the row that fits your situation.

The 7 Real Approval Paths

| Coverage Path | Best For | Drug(s) to Ask About | Why This Works | What Your Doctor Needs to Prove | Biggest Denial Risk | Best Next Step |

|---|---|---|---|---|---|---|

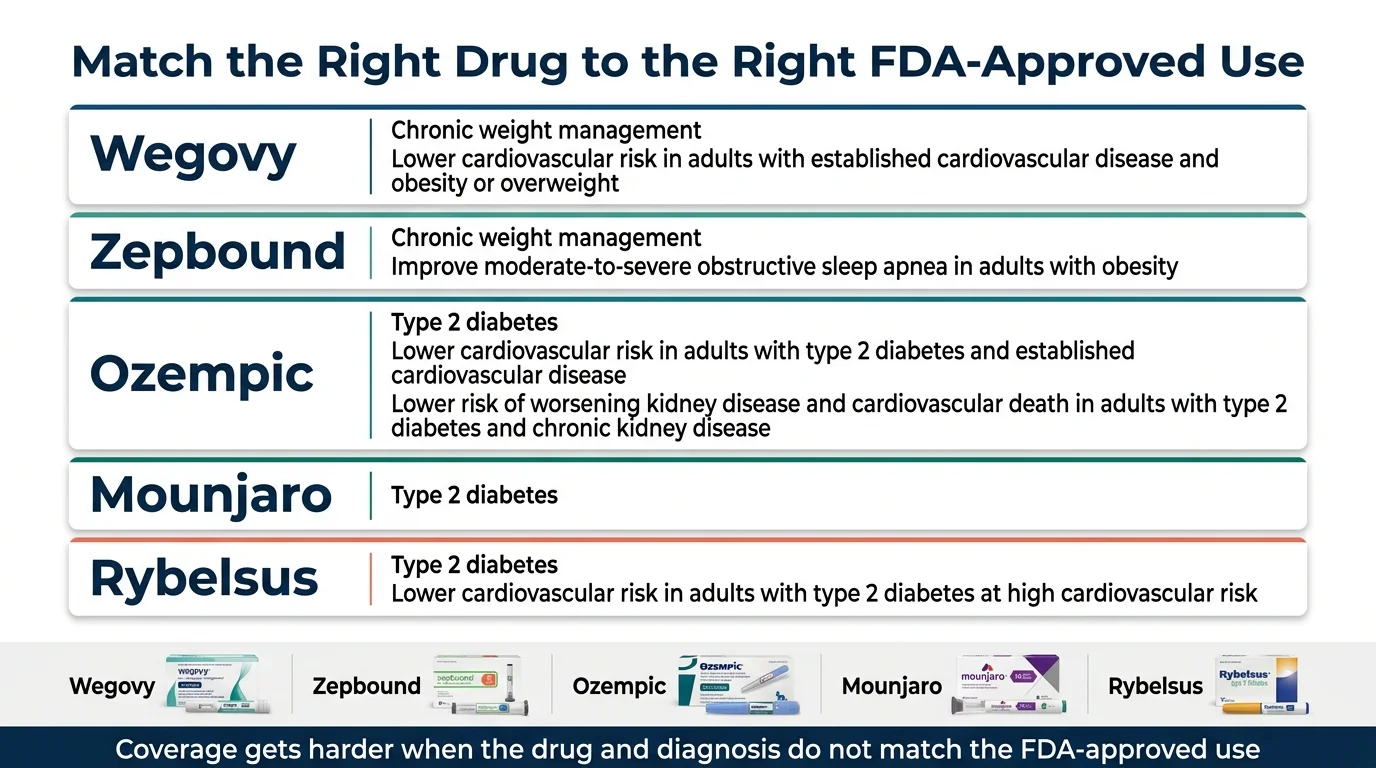

| 1. Type 2 Diabetes | Anyone with a T2D diagnosis | Ozempic, Mounjaro, Rybelsus, Trulicity | Strongest coverage path — almost all plans cover this | A1C levels, diabetes diagnosis, prior treatment history | Step therapy (insurer wants metformin first) | Ask doctor to document diabetes management rationale |

| 2. Obesity/Overweight + Comorbidity | BMI ≥30 or BMI ≥27 with a weight-related condition | Wegovy, Zepbound, Saxenda | FDA-approved for chronic weight management | BMI, documented comorbidity (hypertension, T2D, dyslipidemia, sleep apnea), prior weight-loss attempts | Plan excludes weight-loss drugs entirely; BMI threshold not met | Check if weight loss is a covered benefit BEFORE submitting PA |

| 3. Cardiovascular Disease | Adults with established CVD + obesity/overweight | Wegovy (approved March 2024 for CV risk reduction) | Separate FDA indication — often covered even when “weight loss” isn't | Documented CVD history (prior heart attack, stroke, or coronary artery disease), BMI criteria | Doctor codes it as weight loss instead of CV risk reduction | Specifically request Wegovy for cardiovascular risk reduction |

| 4. Obstructive Sleep Apnea | Adults with moderate-to-severe OSA + obesity | Zepbound (FDA-approved for OSA) | Newer indication that many plans haven't restricted yet | Sleep study results, OSA diagnosis, BMI | Plan hasn't updated formulary to include this indication yet | Bring the FDA approval documentation to your doctor |

| 5. Chronic Kidney Disease | T2D patients with CKD risk | Ozempic (kidney risk reduction indication) | Expanded label strengthens medical necessity argument | CKD staging, eGFR levels, diabetes diagnosis | Insurer doesn't recognize the newer indication | Reference the updated FDA label in the PA submission |

| 6. MASH (Liver Disease) | Adults with MASH + liver fibrosis | Wegovy (accelerated approval for MASH) | Very new — most competitors haven't written about this yet | Liver biopsy or imaging showing fibrosis, MASH diagnosis | Accelerated approval means some plans are still deciding on coverage | Present the FDA approval letter with the PA request |

| 7. Medicare GLP-1 Bridge | Medicare Part D enrollees who meet BMI criteria | Wegovy (injection + pill), Zepbound | First-ever Medicare coverage for weight-loss GLP-1s, starting July 2026 | BMI ≥35 alone; or BMI ≥30 with HFpEF, uncontrolled hypertension, or CKD stage 3a+; or BMI ≥27 with prediabetes, prior MI, prior stroke, or symptomatic PAD | Bridge ends Dec 2026; transition to BALANCE model uncertain | Confirm Part D enrollment now; watch for Spring 2026 CMS guidance |

Understanding the Gray Zones: PCOS, Prediabetes, and Off-Label Requests

If your primary concern is PCOS, prediabetes, or insulin resistance, you're in trickier territory. None of these are standalone FDA-approved indications for GLP-1 medications.

PCOS: There's growing clinical interest in GLP-1s for PCOS, and some doctors prescribe them off-label. But insurers rarely approve off-label requests without a fight. The better path: most people with PCOS also have a qualifying BMI or comorbidity (like insulin resistance or hypertension) that opens the obesity/overweight pathway. Lead with that. For a full breakdown of GLP-1 options for PCOS — including semaglutide vs tirzepatide and how to access them affordably — see our guide: Best GLP-1 for PCOS: 3 Options Compared.

Prediabetes: Ozempic and Mounjaro are approved for type 2 diabetes, not prediabetes. Insurers draw a hard line here. If your A1C is in the prediabetes range (5.7–6.4%), you likely won't get coverage through the diabetes pathway. Focus on the weight-management pathway instead if your BMI qualifies.

Why Ozempic and Mounjaro often get denied for weight loss: This is the single most common mistake we see. Ozempic is FDA-approved for type 2 diabetes. Mounjaro is FDA-approved for type 2 diabetes. Neither is approved for weight loss. If your doctor prescribes Ozempic “for weight loss” to someone without diabetes, the insurer will almost certainly deny it — because that's off-label use. The fix is usually straightforward: use Wegovy or Zepbound instead, which ARE approved for weight management. Same active ingredients in their respective drug families, but different dosing, different FDA labels — and a completely different coverage conversation.

Work with your doctor to find the strongest legitimate pathway. Don't force a weak one — it wastes time and can make future requests harder.

We factor in your insurance type, goals, and budget to find the right fit.

What Insurance Are You Dealing With? Your Next Move Depends on the Plan.

The same drug, same diagnosis, same patient can get approved under one plan and denied under another. Here's what matters for each type.

Employer or Private Commercial Insurance

This is where most people start, and it's where the most variation exists.

The uncomfortable truth: Only about 19% of firms with 200+ workers cover GLP-1s primarily for weight loss, according to KFF's 2025 employer benefits survey. And only 1% of non-covering firms said they're “very likely” to add it in the next 12 months. That means roughly 4 out of 5 large employer plans don't cover this. If your employer plan explicitly excludes anti-obesity medications as a benefit category, no amount of prior authorization paperwork will override that exclusion. That's not a denial you can appeal — it's a benefit design decision.

But here's the important nuance: An employer plan that excludes “weight loss drugs” may still cover Wegovy for cardiovascular risk reduction, or Ozempic for diabetes. The exclusion is usually tied to the indication, not the molecule. This is why the coverage-path table above matters so much — the same drug can be covered or denied depending on what it's being prescribed for.

Here's something else worth knowing: Research from the University of Pennsylvania shows that patients are facing new barriers to GLP-1 coverage in 2026 even when their plans technically cover these drugs. Prior authorization requirements have increased dramatically — going from around 5% of Medicare beneficiaries requiring PA before 2024 to nearly 100% in 2025 (Penn LDI). Commercial plans are following the same trend. Even if your plan covers GLP-1s, expect paperwork.

What to do:

- Check your plan's formulary for the specific drug you want

- Call the number on your insurance card and explicitly ask: “Does my plan cover anti-obesity medications as a pharmacy benefit?”

- If the answer is no, ask: “Which GLP-1 medications ARE covered, and for which conditions?”

- If the entire drug class is covered but your specific drug isn't, ask about a formulary exception

- If weight loss is excluded but you have diabetes, CVD, OSA, or another qualifying condition — that changes the conversation entirely

If your employer excludes weight-loss drugs: You're not without options. You can request that HR add coverage at the next plan renewal — Novo Nordisk even offers a sample letter on their website you can give to your benefits department. You can explore whether a different covered indication applies to you. You can use HSA/FSA funds toward cash-pay costs. And you can access FDA-approved GLP-1 medication through telehealth programs starting at $149/month — often less than you'd pay through insurance with a high deductible anyway.

If your coverage changed or got dropped in 2026: You're not imagining it. Multiple major PBMs and employer plans adjusted their GLP-1 formularies for 2026. CVS announced it would exclude Zepbound from certain formularies starting mid-2025. Some employers raised BMI thresholds. Others added engagement requirements — like mandatory participation in a wellness program before coverage kicks in. If you were covered last year and aren't now, check exactly what changed and whether you qualify under the new criteria. Sometimes the drug switched tiers or the insurer now prefers a different brand. Your doctor can request a formulary exception if there's a clinical reason you need the specific drug that was dropped.

ACA Marketplace Plans

Marketplace plans vary as much as employer plans. HealthCare.gov recommends checking the insurer's website formulary, reviewing the Summary of Benefits and Coverage document, and calling the insurer directly (HealthCare.gov). Do all three — sometimes the website is outdated.

The key question is the same: is the drug on the formulary, and is the weight-loss indication covered? Marketplace plans are more likely to cover GLP-1s for diabetes than for weight loss.

Medicare

This section matters more than anything else on this page right now, because the landscape is shifting fast.

Where things stand today (before July 2026): Federal law has prohibited Medicare from covering drugs prescribed “solely for weight loss” since 2003. That's not your plan being difficult — it's a statute. GLP-1s for type 2 diabetes, cardiovascular risk reduction, and obstructive sleep apnea can be coverable under standard Part D, subject to your plan's formulary and utilization-management rules (CMS). So if you're on Medicare and have one of those conditions, your path is through the traditional Part D benefit, not the Bridge.

What's changing — the Medicare GLP-1 Bridge (July 1 – December 31, 2026):

CMS announced this program in December 2025 and released detailed FAQs in March 2026. Here's what we know:

- Eligible drugs: Wegovy (injection and pill) and Zepbound

- Eligible indication: Weight loss/weight management

- Copay: $50/month — flat, regardless of which Part D benefit phase you're in

- Eligibility: Must be enrolled in a Part D plan (PDP or MA-PD) for 2026. BMI ≥35 alone; or BMI ≥30 with HFpEF, uncontrolled hypertension, or CKD stage 3a+; or BMI ≥27 with prediabetes, prior MI, prior stroke, or symptomatic PAD (CMS, Medicare GLP-1 Bridge FAQs)

- How it works: Your doctor submits a prior authorization to CMS's central processor — NOT your Part D plan. If approved, you fill at your pharmacy and pay $50.

- Important catches:

- The $50 copay does NOT count toward your Part D deductible or $2,100 out-of-pocket cap

- Low-Income Subsidy (Extra Help) does NOT apply — you still pay $50 even if you normally pay little for prescriptions

- This is temporary — it runs July through December 2026 only

After the Bridge: Coverage is supposed to shift to the BALANCE Model starting January 2027, but your Part D plan must voluntarily opt in. If your plan doesn't participate, you'd need to switch plans during 2027 open enrollment. KFF has flagged this transition as one of the program's biggest risks (KFF).

What to do right now if you're on Medicare:

- If you have diabetes, CVD, or OSA — talk to your doctor about getting a GLP-1 covered under your current Part D benefit. Don't wait for the Bridge.

- Confirm you're enrolled in Part D for 2026 (required for Bridge eligibility)

- Watch for CMS updates in Spring 2026 on final Bridge eligibility criteria

- Some cash-pay options may still be available in the meantime, but eligibility varies by program — many manufacturer offers exclude government beneficiaries. Check program terms carefully before assuming you qualify.

Medicaid

Medicaid is where things get frustrating, because every state makes its own rules.

Federal law does NOT require states to cover weight-loss drugs under Medicaid. Coverage for diabetes-indicated GLP-1s is required, but obesity drugs are optional. As of January 2026, only 13 state Medicaid programs cover GLP-1s for obesity under fee-for-service (KFF, Medicaid Coverage of and Spending on GLP-1s) — and that number dropped from 16 after California, Pennsylvania, New Hampshire, and South Carolina cut coverage due to budget pressure.

States with some Medicaid weight-loss coverage include Massachusetts, Minnesota, Mississippi, New York, North Carolina (reinstated December 2025), and Wisconsin. Michigan restricted coverage to morbid obesity only.

The BALANCE Model may improve this — state Medicaid programs can opt in starting May 2026 — but participation is voluntary and state budgets are tightening.

What to do if your state doesn't cover weight-loss GLP-1s on Medicaid:

- Check if you qualify under a diabetes, CVD, or OSA indication — coverage for these uses is generally required under Medicaid, though utilization-management rules still apply

- Children under 21 may qualify under federal EPSDT requirements even when adults don't

- Cash-pay options may be available, but eligibility varies by program — many manufacturer offers exclude Medicaid beneficiaries. Check specific program terms.

VA, TRICARE, and Federal Employees

- VA: Veterans may access GLP-1s through the MOVE! Weight Management Program. Availability varies by facility — contact your local MOVE! coordinator.

- TRICARE: Covers some GLP-1s for diabetes; weight-loss coverage varies. Check your formulary.

- Federal Employees (FEHB): Good news — FEHB is treated as commercial insurance for savings-card purposes. You can use manufacturer copay cards. Coverage varies by plan.

60 seconds. No email required. Clear recommendation based on your situation.

How to Check If Your Plan Covers Wegovy, Zepbound, Ozempic, or Mounjaro

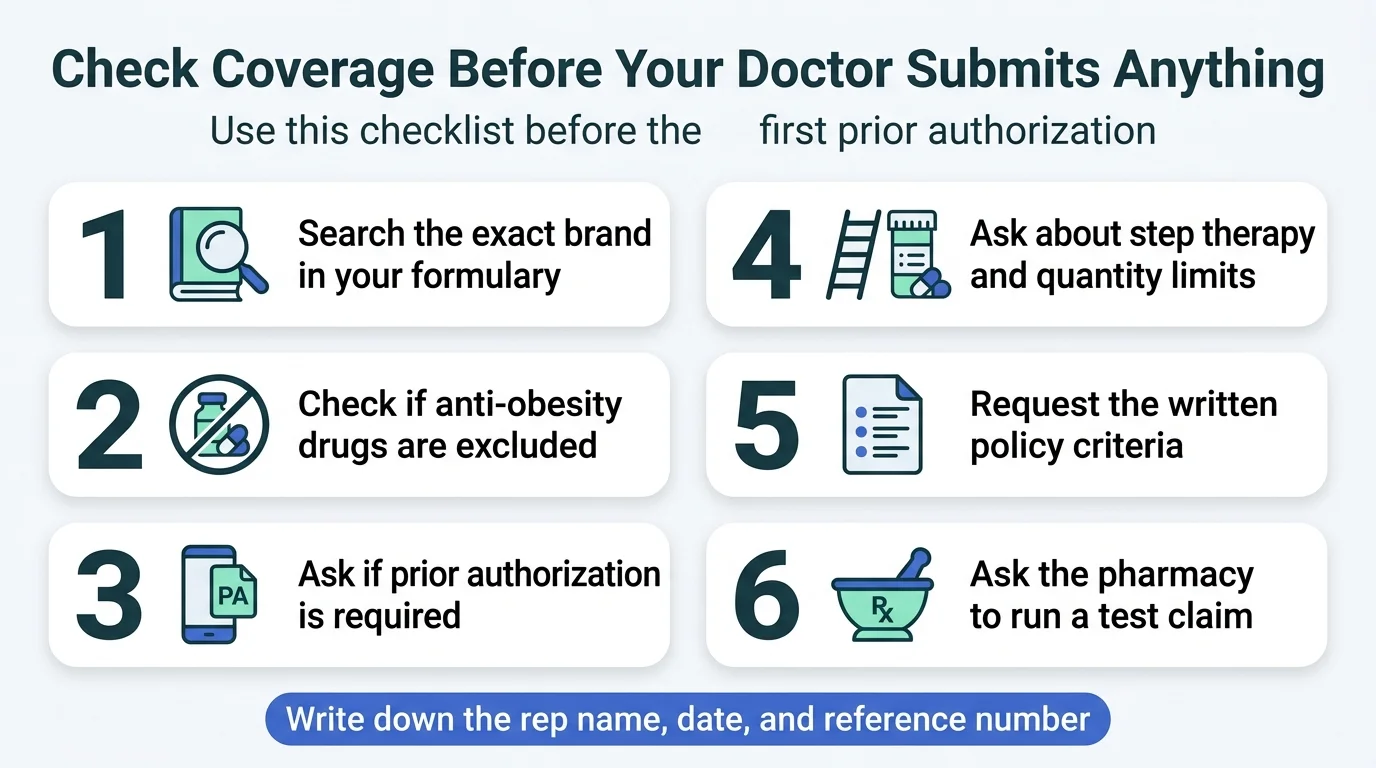

Before your doctor spends time on prior authorization paperwork, do this homework first. It takes 20 minutes and prevents the most common waste of time: submitting a PA for a drug your plan doesn't cover at all.

Your 7-step coverage check:

- Log into your insurer's portal. Search for the exact brand name in the formulary (drug list). Note which tier it's on.

- Look for restrictions. Is prior authorization required? Step therapy? Quantity limits?

- Check for exclusions. Search specifically for whether “anti-obesity medications” or “weight loss drugs” are excluded as a benefit category. This is different from a drug not being on the formulary — an exclusion means the entire category is blocked.

- Call the number on your card. Ask the questions in the call script below. The website doesn't always tell the full story.

- Ask the pharmacy to run a test claim. A pharmacist can submit a test claim before filling the prescription. This shows you real-time coverage status and out-of-pocket cost.

- Use manufacturer coverage checkers. Wegovy has a coverage tool at NovoCare.com. Zepbound has one through Lilly. These are free and give you a quick read on your specific plan.

- Ro offers a free GLP-1 Insurance Coverage Checker that contacts your insurer by phone on your behalf and sends you a personalized coverage report. According to Ro's published data, 43% of users who checked had coverage for a GLP-1 for weight loss, and half of those with coverage had copays of $50/month or less. It's free and takes a few minutes to submit your info.

Record everything. The tier, the PA requirements, the exclusions, the phone rep's name, the date, the reference number. You'll need this if you appeal later.

What to Say When You Call Your Insurance Company

Most people dread this call. Having a script makes it painless. Here's exactly what to ask — and what to write down.

Opening: “Hi, I'm calling to check coverage for a specific prescription medication. My member ID is [number].”

The critical questions:

- “Is [drug name] on my plan's formulary for [your diagnosis]?”

- “Is anti-obesity medication covered as a pharmacy benefit under my plan, or is it excluded?”

- “What are the exact prior authorization criteria for this drug?”

- “Does my plan require step therapy — meaning I'd need to try other medications first?”

- “What specific documents does my prescriber need to submit with the PA request?”

- “If the PA is denied, what is the appeal process and what are the deadlines?”

- “Can you send me the written policy or criteria document for this drug?”

What to record:

- Representative's name and ID number

- Date and time of the call

- Reference or confirmation number

- Exact language used in any denial or restriction

- The appeal deadline they mention

Getting the insurer's actual criteria document is gold. It tells your doctor exactly what boxes to check in the PA submission — no guessing.

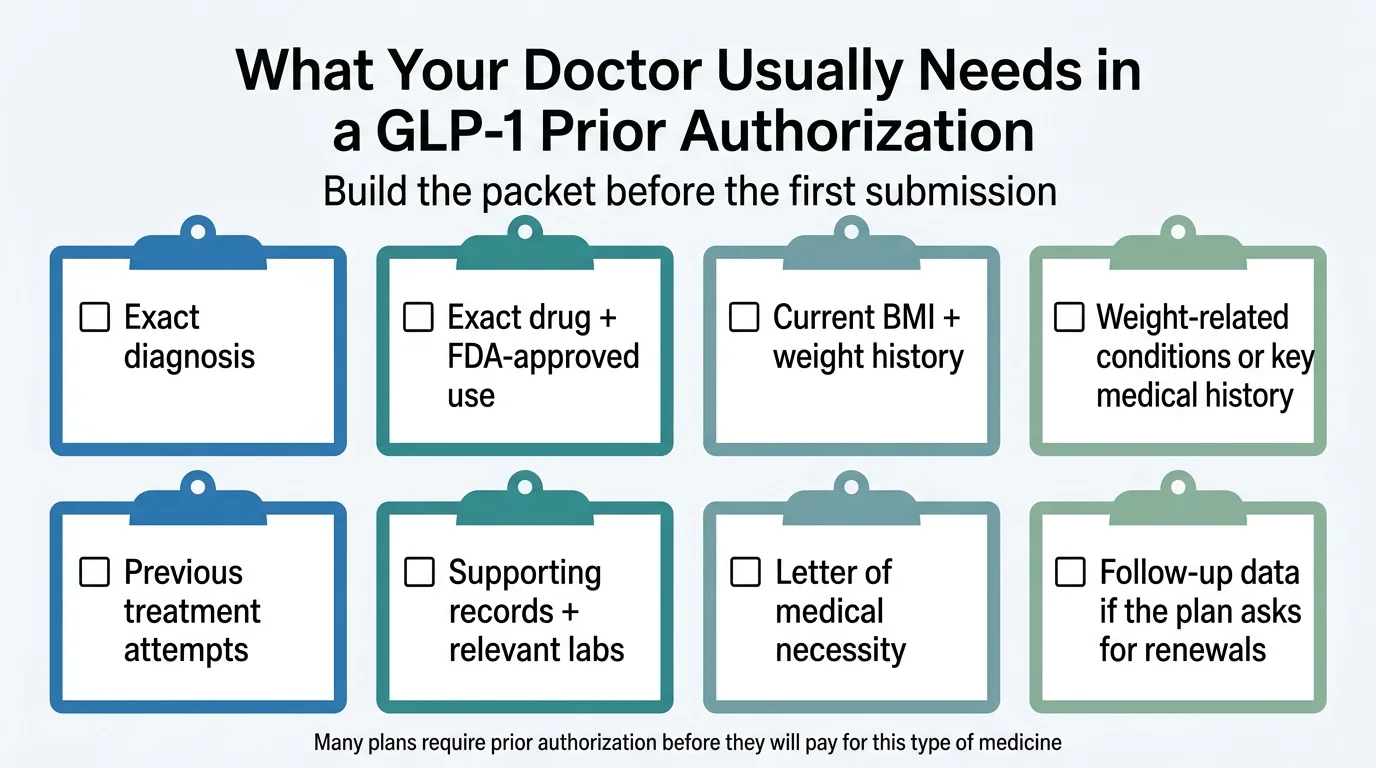

What Your Doctor Needs to Include in the Prior Authorization

This is where most GLP-1 requests succeed or fail. A strong PA submission isn't just paperwork — it's a targeted argument that maps your medical situation to the insurer's specific approval criteria.

If your doctor's office handles prior authorizations regularly, they likely know this. But many patients have told us their PA was denied because of missing documentation that could have been included from the start. Share this section with your prescriber — seriously.

The diagnosis must match the drug's approved use

This sounds obvious, but it's the #1 fixable reason for denials. If you're requesting Wegovy for chronic weight management, the PA needs to clearly state the weight-management indication with supporting BMI and comorbidity data. If the request is vague or coded incorrectly, the insurer's system may auto-deny it.

If you have a qualifying condition like cardiovascular disease or OSA, make sure the PA specifically references that indication — not just “weight loss.” The exact framing can determine whether the claim is approved or routed to the wrong review pathway.

Baseline BMI, weight history, and comorbidities

The PA should include:

- Current BMI (measured in-office, not self-reported)

- Weight history over the past 1–2 years

- All weight-related comorbidities: type 2 diabetes, hypertension, dyslipidemia, sleep apnea, cardiovascular disease, MASH, chronic kidney disease

- Relevant lab work: A1C, lipid panel, fasting glucose, liver enzymes, eGFR — depending on which pathway you're using

Don't leave comorbidities out. Many plans require BMI ≥ 30 alone OR BMI ≥ 27 with a comorbidity. If you're at BMI 28 with hypertension, the hypertension is what makes you eligible.

Previous weight-loss attempts

Many plans require documented prior weight-management efforts or participation in a structured program, and some specify time-based requirements (e.g., 3–6 months). Plans may also require trial-and-failure of older or cheaper medications (step therapy).

If you've done Weight Watchers, worked with a nutritionist, used an app-based program, or tried other medications — document it. Even informal efforts count if they're in your medical records.

A letter of medical necessity

This is where your doctor makes the case. A strong letter ties your specific situation to the insurer's criteria language and explains why this particular GLP-1 is the most appropriate option. It should reference the FDA-approved indication, your qualifying metrics, previous treatment failures, and why alternatives aren't suitable.

Renewal documentation

Getting approved the first time is only half the battle. Many plans require proof of ongoing benefit — typically at least 5% body weight loss — to continue coverage. CVS Caremark, for example, includes maintenance-dose and weight-loss continuation language in their Wegovy criteria (CVS Caremark PA criteria). Know the renewal requirements from day one so you're tracking the right data.

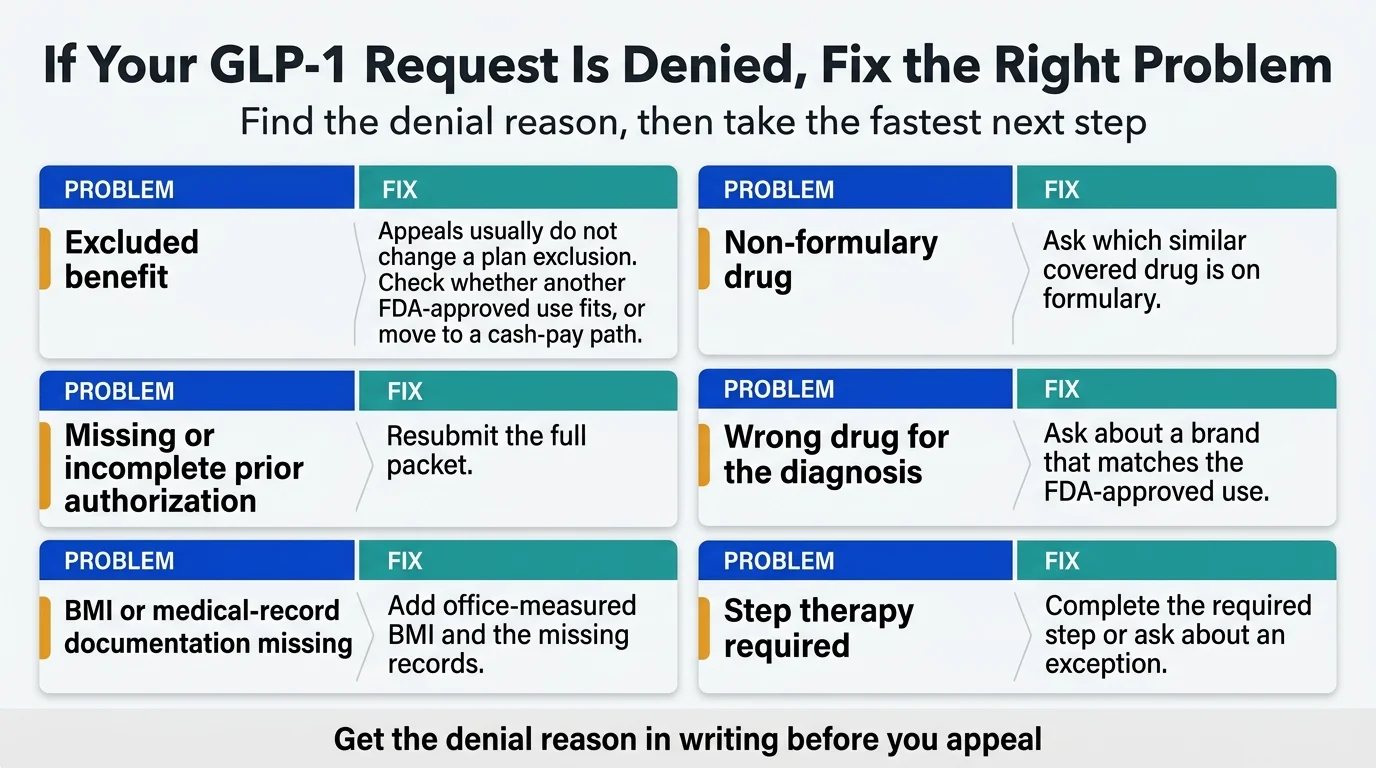

Why GLP-1 Requests Get Denied (And Whether Yours Is Fixable)

Not every denial is the end of the road. Some are easily fixable. Others mean you need a different strategy entirely. Here's how to tell the difference.

| Denial Reason | What It Means | Fixable? | Fastest Fix |

|---|---|---|---|

| Excluded benefit | Your plan doesn't cover weight-loss drugs as a category | Usually no (by appeal). Yes by switching paths. | Check if another covered indication applies; explore cash-pay options |

| Wrong drug for the diagnosis | The drug doesn't match its FDA-approved use for your coded diagnosis | Yes | Have your doctor resubmit with the correct drug/indication pairing |

| Missing prior auth paperwork | PA wasn't submitted, was incomplete, or went to the wrong department | Yes | Resubmit with complete documentation |

| BMI or comorbidity threshold not met | Your documented BMI or conditions don't meet the plan's criteria | Sometimes | Get an in-office BMI measurement; document all comorbidities |

| Step therapy not completed | Insurer requires you to try cheaper alternatives first | Yes (with time) or request exception | Try the required medication, OR request a step-therapy exception |

| “Not medically necessary” | Insurer's reviewer didn't find sufficient justification | Yes | Appeal with stronger letter of medical necessity and additional documentation |

| Non-formulary drug | The drug isn't on your plan's approved list | Sometimes | Request a formulary exception, or ask which similar drug IS on formulary |

| Renewal data missing | You didn't demonstrate enough weight loss for continued coverage | Yes | Submit updated weight records and clinical notes |

The most important distinction: An excluded benefit is fundamentally different from a denied prior authorization. If weight-loss drugs are excluded from your plan, appealing won't help — the benefit simply doesn't exist. But if the benefit exists and your PA was denied, an appeal with better documentation has a real chance of success.

How to Appeal a GLP-1 Denial

If your prior authorization was denied (not excluded — denied), here's the step-by-step appeal process.

Step 1: Get the denial reason in writing

Your insurer is required to send you a written explanation. Read it carefully. The specific reason matters — “not medically necessary” requires a completely different response than “step therapy not completed.”

Step 2: Figure out if this is a paperwork problem or a path problem

If the denial says your documentation was incomplete, this is a paperwork fix. If it says the drug isn't covered for your diagnosis, you may need to change the drug or the indicated use — not just resubmit the same request.

Step 3: Fix the request before you appeal

The most common mistake is appealing with the same paperwork that got denied. Gather new or additional documentation that directly addresses the denial reason. If the insurer said your BMI didn't meet threshold, get a fresh in-office measurement. If they said prior weight-loss efforts weren't documented, gather those records now.

Step 4: File an internal appeal

Under the ACA, you have the right to an internal appeal within 180 days of the denial for most commercial plans. Your doctor should submit a stronger letter of medical necessity that specifically addresses the denial reason, includes any new documentation, and references the FDA-approved indication and current clinical guidelines. For a full walkthrough with a letter template and evidence checklist, see our guide: How to Appeal a GLP-1 Denial →

What makes a strong appeal letter:

- Opens with the specific denial reason and directly refutes it

- Cites the FDA-approved indication for the specific drug being requested

- References current medical guidelines (American Diabetes Association Standards of Care, Endocrine Society guidelines, etc.)

- Includes any new documentation: updated BMI, new lab results, additional comorbidity diagnoses

- Explains why alternatives aren't appropriate for this specific patient (this counters “not medically necessary” denials)

- Requests a specific action — approval of the specific drug at the specific dose

The difference between a form letter and a targeted appeal can be the difference between approval and another denial. If your doctor's office doesn't have experience with GLP-1 appeals specifically, this is another area where Ro's insurance concierge can add real value — they do this daily.

Step 5: Request an external review

If your internal appeal is denied, you can request an independent external review within 4 months of the final internal denial. An outside reviewer — not employed by your insurer — evaluates your case. This is your right under federal law for most plans. Standard external reviews must be completed within 45 days; expedited external reviews within 72 hours (HealthCare.gov).

Key timelines to know: Insurers generally must respond to a standard prior-authorization request within 15 days, and within 72 hours for urgent/expedited requests. For internal appeals, the insurer typically has 30 days (non-urgent) or 72 hours (urgent) to issue a decision (HealthCare.gov).

Step 6: Know when to stop appealing and switch paths

If you've been through internal appeal and external review and the answer is still no, it's time to pivot. Continuing to appeal the same denial rarely produces a different result. At this point, your best options are:

- A different drug/indication that might get approved

- Manufacturer savings cards or cash-pay pricing

- A telehealth program that handles insurance navigation for you

Speaking of which: Ro's insurance concierge provides coverage checks and prior-authorization support as part of their program. If fighting with insurance companies isn't your idea of a good time (and it's nobody's), having a dedicated team help manage the process can save weeks of frustration. More on this below.

“Covered” Doesn't Always Mean Cheap: What You'll Actually Pay

This catches a lot of people off guard. You do the work, get the PA approved, walk into the pharmacy — and the bill is still $300. What happened?

Insurance “coverage” just means the plan participates in the cost. It doesn't mean it's free. What you'll actually pay depends on:

- Your plan's tier structure. GLP-1s are often placed on specialty tiers (Tier 4 or 5), which can carry 25–40% coinsurance instead of a flat copay.

- Your deductible. If you haven't met your annual deductible, you may pay full cost until you do — and for a drug that lists at $1,000+/month, that adds up fast.

- Coinsurance vs. copay. A $50 copay is predictable. 30% coinsurance on a $1,000 drug is $300. Know which your plan uses.

- Out-of-pocket maximum. Once you hit this, the plan covers everything. But getting there can be painful.

This is exactly why manufacturer savings cards matter so much. With the Wegovy Savings Card on a commercial plan that covers the drug, eligible patients may pay as little as $25/month, subject to program terms and savings limits (NovoCare). That can dramatically reduce what you'd otherwise owe under your plan's coinsurance structure.

And here's the uncomfortable math that some people need to run: if your plan charges $400/month in coinsurance for a GLP-1 because of a high deductible, and cash-pay through Ro or NovoCare is $149–$349/month — you might be better off skipping insurance entirely and paying cash. Run the numbers before assuming insurance saves you money.

How to Cut Your GLP-1 Cost — Even With Insurance

Getting approved is one thing. The bill is another. “Covered” doesn't always mean “affordable.” Here's how to minimize what you actually pay.

Manufacturer Savings Cards

These are the single biggest cost-reduction tool for people with commercial insurance. They're free, and the savings are substantial.

Wegovy Savings Card (Novo Nordisk):

- With commercial insurance that covers Wegovy: Eligible patients may pay as little as $25, subject to program terms and maximum savings limits (NovoCare savings terms)

- Without commercial coverage (self-pay): $349/month for injection, $149–$299/month for the pill through NovoCare Pharmacy

- New patient intro offer: $199/month for first 2 months of 0.25 mg and 0.5 mg doses through NovoCare (through March 31, 2026)

- NOT available for Medicare, Medicaid, VA, or TRICARE beneficiaries

Zepbound Savings Card (Eli Lilly):

- With commercial insurance: Eligible patients may pay as low as $25/month, subject to program terms

- Cash-pay vials through LillyDirect: Starts at $299/month for 2.5 mg, $399/month for 5 mg, $449/month for higher doses under current terms

- NOT available for government insurance

Ozempic and Mounjaro Savings Cards: Both offer commercial-insured patients copays as low as $25/month for their diabetes indications.

What to watch out for: Some employer plans use “copay accumulator” or “copay maximizer” programs that prevent savings-card payments from counting toward your deductible. Ask your insurer directly whether your plan has one of these programs before assuming the savings card solves everything.

HSA and FSA

GLP-1 copays, deductibles, and even some cash-pay costs are generally eligible expenses for Health Savings Accounts and Flexible Spending Accounts. If you have either, use them.

When cash-pay is actually cheaper than insurance

This surprises people, but it's true in more situations than you'd expect. If your insurance has a high deductible and your GLP-1 is on a specialty tier with 30–40% coinsurance, you might be paying $400–$600/month until you hit your deductible — while the cash-pay price through the manufacturer is $149–$349/month.

Run the numbers before assuming insurance is always the cheaper path.

Ro compares insurance vs. cash-pay so you know your cheapest path. Free to check.

When Insurance Won't Work: Your Plan B (And Why It's Better Than You Think)

Let's be direct. If you've checked your coverage, submitted a PA, appealed a denial, and the answer is still no — or if your plan flat-out excludes weight-loss drugs — you are not stuck. Not even close.

Here's the reality most people don't know yet: the GLP-1 pricing landscape completely changed in 2025 and 2026. Manufacturers started competing on price. The Wegovy pill launched. Direct-to-consumer pharmacy channels opened up. FDA-approved GLP-1s are now available at prices that would have been unthinkable two years ago.

You don't have to choose between a $1,000+/month branded drug and giving up. That's a false binary, and it's the thing that keeps the most people stuck.

Why cash-pay sometimes makes more sense than insurance

This isn't just a backup plan. For some people, paying cash through a telehealth program is genuinely the better path — even when insurance is an option.

Think about it: if your plan has a $3,000 deductible and your GLP-1 sits on a specialty tier with 30–40% coinsurance, you might spend $400–$600/month for the first half of the year before your deductible kicks in. Meanwhile, the cash-pay price through the manufacturer's own pharmacy is $149–$349/month from day one. No prior authorization wait. No step therapy hoops. No surprise bills.

Cash-pay also means you can start treatment in days instead of weeks. No waiting 3–10 business days for a PA decision. No appeal process. No letters of medical necessity. You complete an online visit, a provider evaluates you, and if eligible, your medication ships or is ready for pickup.

The most complete option: Ro Body Program

We recommend Ro as the starting point for most commercially insured people navigating GLP-1 treatment. Here's why: Ro combines insurance coverage support with affordable FDA-approved cash-pay backup options in a single program — so you don't hit a dead end regardless of what your insurer decides.

Here's how the program actually works:

- You complete a quick online health assessment. Ro charges $45 upfront for the first-month evaluation.

- A licensed provider reviews your information and, if you're eligible, prescribes a personalized treatment plan. If you're eligible for treatment, ongoing membership is $145/month; medication cost is separate and varies based on your treatment and insurance situation.

- Ro's dedicated insurance concierge gets to work — they check your commercial insurance coverage, submit prior authorizations, and can help you explore alternatives if a drug isn't covered. This is the part that saves you hours on hold and weeks of back-and-forth.

- If your insurance covers the medication, you fill at your pharmacy and pay your copay

- If insurance doesn't cover it, your provider recommends FDA-approved cash-pay options at competitive prices through manufacturer channels

What you'll actually pay for medication through Ro (cash-pay pricing, per Ro's published terms as of March 2026):

- Wegovy pill: From $149/month for lower doses (Ro pricing page)

- Wegovy injection: $199/month intro for 0.25 mg and 0.5 mg doses (limited-time offer through March 31, 2026), $349/month for maintenance doses

- Zepbound vials: From $299/month for 2.5 mg, $399/month for 5 mg, $449/month for higher doses

These are manufacturer-direct prices available through Ro's integration with NovoCare Pharmacy and LillyDirect.

What the clinical data shows: Clinical trials of branded semaglutide and tirzepatide medications show 14–20% average body weight loss in the first year for non-diabetic adults with obesity, combined with diet and exercise (FDA prescribing information for Wegovy). Ro reports that members taking GLP-1 medication see results consistent with this clinical data (provider-stated).

A Ro member named Hannah said she was “thrilled to not have to fight for my coverage” after the concierge team helped with her prior authorization process. (Ro members were compensated for their testimonials.)

Who Ro is NOT ideal for: Ro's insurance concierge currently can't coordinate coverage for government insurance plans (Medicare, Medicaid, VA) — with the exception of FEHB (Ro). If you're on government insurance, you may still be able to join for certain cash-pay medication options, but the insurance navigation benefit won't apply. For commercially insured people, this is where we'd start.

You've spent the last several minutes learning exactly how GLP-1 coverage works — the paths, the pitfalls, the paperwork. If you'd rather have a team handle that process for you while you focus on actually losing the weight, that's what Ro's program is built for.

Insurance concierge + cash-pay backup. FDA-approved medications only.

Another solid option: Hims & Hers

Hims and Hers offer FDA-approved branded GLP-1 access without requiring insurance. The process is straightforward: online consultation, provider review, and medication access. Insurance is not required. If you want the simplest possible path from “I want a GLP-1” to “I have a GLP-1” without a lot of bells and whistles, this is a clean option.

NovoCare Pharmacy and LillyDirect

If you already have a prescription from your own doctor, you can fill directly through the manufacturers' pharmacies at cash-pay prices. NovoCare (Novo Nordisk) handles Wegovy and Ozempic. LillyDirect (Eli Lilly) handles Zepbound and Mounjaro. These aren't telehealth programs — they're pharmacy fulfillment channels. Useful if you have a doctor you already trust and just need a cheaper way to fill your script.

What's Changing in 2026 and Beyond

The GLP-1 coverage landscape is moving faster than most content on the internet can keep up with. Here are the policy shifts that matter most right now.

Medicare GLP-1 Bridge (July–December 2026): The first-ever Medicare coverage for weight-loss GLP-1s. Wegovy and Zepbound at $50/month for eligible Part D beneficiaries. This is a temporary 6-month demonstration, not permanent coverage.

BALANCE Model (2027+): The longer-term successor to the Bridge. State Medicaid programs can opt in starting May 2026, Medicare Part D plans in January 2027. Participation is voluntary for everyone — manufacturers, states, and plans. Not a guarantee of coverage for any individual.

TrumpRx: A separate government-negotiated out-of-pocket pricing platform. TrumpRx currently lists Wegovy Pill starting at $149 and Wegovy Pen starting at $199 (TrumpRx). Note: the CMS $245 figure referenced in Medicare GLP-1 Bridge documents is the net manufacturer price under the Bridge, not the TrumpRx consumer price — these are separate programs.

Wegovy Pill (Oral Semaglutide for Weight Loss): FDA approved December 2025. Cash prices starting at $149/month for the lowest dose through NovoCare. This is a genuine inflection point for affordability.

Orforglipron (Eli Lilly): An oral GLP-1 being developed for weight loss and diabetes. If approved (expected to seek approval in 2026), Eli Lilly has indicated a starting cash price of $149 for the lowest dose.

Medicaid coverage trending down: Four states eliminated or restricted weight-loss GLP-1 coverage in January 2026 due to budget constraints. The BALANCE Model could reverse this, but it depends on state participation and federal funding dynamics.

Employer coverage plateauing: After years of growth, the percentage of large employers covering weight-loss GLP-1s may be leveling off or declining. Rising drug costs are pushing some employers to restrict or eliminate coverage.

We update this section as policies change. Bookmark this page — the next 12 months will bring more shifts than the last 5 years combined.

Frequently Asked Questions

What BMI do I need for insurance to cover a GLP-1?

Most plans follow the FDA label: BMI ≥ 30, or BMI ≥ 27 with at least one weight-related health condition (hypertension, type 2 diabetes, or dyslipidemia). However, some plans set their own higher thresholds — BMI 32 or even 35 — so always check your plan's specific criteria before assuming you qualify.

Does insurance cover Ozempic for weight loss?

Ozempic is FDA-approved only for type 2 diabetes (and more recently for CV and kidney risk reduction). If your doctor prescribes it off-label for weight loss, most insurers will deny coverage because it's not the approved indication. Wegovy contains the same ingredient at a different dose and IS approved for weight loss — making it a stronger coverage candidate if weight management is your primary goal.

Will insurance cover GLP-1 for PCOS?

PCOS is not a standalone FDA-approved indication for any GLP-1 medication. However, many people with PCOS also have a BMI that qualifies under the obesity/overweight pathway, or have insulin resistance, prediabetes, or other comorbidities that open another coverage door. Work with your doctor to identify the strongest qualifying pathway based on your full clinical picture.

Does Medicare cover Wegovy now?

Not yet under standard Part D for weight loss — but starting July 2026, the Medicare GLP-1 Bridge will cover Wegovy and Zepbound for weight loss at $50/month for eligible Part D beneficiaries. If you have established cardiovascular disease, Wegovy may already be coverable under Part D for the CV risk reduction indication.

Does Medicaid cover GLP-1?

For diabetes: yes, in all states. For weight loss: only in about 13 states as of January 2026. Coverage varies dramatically by state, and several states recently cut or restricted coverage. Check with your state Medicaid program directly.

How long does GLP-1 prior authorization take?

Typically 3–10 business days for a standard request. Urgent or expedited requests may be processed in 24–72 hours if your doctor indicates clinical urgency. Don't wait until you're out of medication to submit.

Can I use a savings card with Medicare or Medicaid?

No. Federal law prohibits manufacturer savings cards for government insurance beneficiaries. The Medicare GLP-1 Bridge (starting July 2026) is the first real cost-reduction pathway for Medicare patients seeking GLP-1s for weight loss.

What if my employer plan excludes weight-loss drugs entirely?

An exclusion is different from a denial. You can't appeal an exclusion — it's a plan design decision. Your options: ask HR about adding coverage at the next plan renewal, check if a different covered indication applies to your situation (CVD, OSA, diabetes), use an HSA/FSA toward cash-pay costs, or explore telehealth programs with manufacturer-direct pricing starting at $149/month.

What is step therapy, and how do I get past it?

Step therapy means your insurer requires you to try cheaper medications before approving the one your doctor prescribed. For GLP-1s, this might mean trying metformin or orlistat first. You can either complete the required trial, or your doctor can request a step-therapy exception with a clinical justification for why those alternatives aren't appropriate for you.

Can a telehealth company help with prior authorization?

Yes. Programs like Ro include an insurance concierge that checks your coverage, submits prior authorizations, and can help you explore alternatives if coverage isn't available. This can save weeks compared to navigating the process yourself or waiting for an overloaded doctor's office to follow up.

Is Zepbound easier to get covered than Wegovy?

It depends on your plan's formulary. Some plans prefer Wegovy, others prefer Zepbound, and some cover both. Zepbound's OSA indication gives it a unique coverage pathway that Wegovy doesn't have, which can be an advantage if you have sleep apnea. Check your specific plan — there's no universal answer.

What is the cheapest legitimate GLP-1 option right now?

For commercially insured patients with coverage: as low as $25/month with the Wegovy Savings Card, subject to program terms. For cash-pay patients: the Wegovy pill from $149/month for the lowest dose through NovoCare or Ro. For Medicare patients starting July 2026: $50/month through the GLP-1 Bridge for eligible beneficiaries.

How much does a GLP-1 cost with insurance?

It depends heavily on your plan's tier structure and your deductible status. With commercial insurance and a manufacturer savings card, eligible patients may pay as little as $25/month. Without a savings card, copays for specialty-tier drugs can run $100–$500/month depending on your plan. The only way to know your exact cost is to check your specific plan — or have your pharmacy run a test claim.

Can I switch from Ozempic to Wegovy to get insurance coverage for weight loss?

Potentially. If your doctor prescribed Ozempic off-label for weight loss and your insurer denied it, switching to Wegovy (which IS FDA-approved for weight loss) with a proper prior authorization may succeed. They're both semaglutide, but Wegovy has the weight-management indication that opens the coverage door. Your doctor would need to submit a new PA under the weight-management indication.

What happens if I start a GLP-1 and then my insurance coverage changes?

This is happening more often in 2026. If your plan drops coverage mid-year, you typically have options: ask your doctor to submit a continuity-of-care exception (most plans must allow this for a transition period), switch to a covered alternative on your new formulary, or pivot to cash-pay pricing. Don't abruptly stop your medication without talking to your doctor — GLP-1 discontinuation can lead to weight regain.

How We Built and Verify This Guide

We're The RX Index Research Team — an independent editorial group focused on GLP-1 medication access, pricing, and insurance navigation. We are not doctors, pharmacists, or insurance advisors. What we do is research coverage pathways, verify pricing against primary sources, and synthesize it into something you can actually use. Learn more about our team and editorial standards →

Our methodology:

Every claim in this guide is sourced from one of five tiers, in order of priority:

- FDA prescribing information and approval letters — for drug indications, approved uses, and safety information

- CMS announcements, HealthCare.gov, and KFF reports — for Medicare, Medicaid, and policy data

- Insurer criteria documents and formularies — for specific plan rules and PA requirements (e.g., CVS Caremark published criteria)

- Manufacturer coverage tools and published pricing — NovoCare, LillyDirect, TrumpRx, verified against official terms pages

- Provider-published data — clearly labeled as “provider-stated” whenever used (e.g., Ro membership costs, program features)

How we handle pricing claims: Every price in this guide reflects currently published manufacturer or insurer terms as of the date at the top of this page. We verify pricing against primary source pages quarterly and after major policy announcements. When a price is provider-stated, we label it as such and link to the source.

Medical disclaimer: This guide is for informational purposes only and does not constitute medical advice. Always consult with a licensed healthcare provider before starting any medication. GLP-1 medications require a prescription and have risks and side effects that should be discussed with your doctor.

Your Next Step

You now know more about GLP-1 insurance coverage than 95% of people who search for this topic — and probably more than some of the people answering phones at insurance companies.

Here's the honest picture: navigating GLP-1 coverage takes effort. The system wasn't designed with patients in mind. Prior authorization requirements are increasing. Some employers are dropping coverage. Medicaid states are cutting back. It's a frustrating landscape.

But the other side of that picture is this: there are more paths to affordable GLP-1 treatment right now than at any point in history. Medicare coverage is coming for the first time ever. Manufacturer pricing has dropped to levels that put treatment within reach for millions more people. Telehealth programs have turned a months-long insurance battle into a days-long process. The Wegovy pill changed the cost equation overnight.

Whatever your situation — commercially insured, on Medicare, on Medicaid, uninsured, denied, confused, or just getting started — there is a viable path forward. We just walked through all of them.

Your Quick-Reference Checklist

Before you close this tab, here's the condensed action plan:

- Identify your strongest coverage path from the 7-path table above. Match your insurance type + diagnosis to the right drug.

- Check your formulary and confirm whether weight-loss drugs are covered or excluded as a category.

- Call your insurer using the script in this guide. Get the PA criteria in writing.

- Prepare the PA packet with your doctor — BMI, comorbidities, prior treatment attempts, letter of medical necessity.

- If denied, decode the reason using our denial table. Fix the request before you appeal.

- Stack savings. Manufacturer savings cards can significantly reduce your out-of-pocket cost on commercial plans — eligible patients may pay as little as $25/month.

- If insurance is a dead end, don't stop here. Cash-pay GLP-1s start at $149/month for eligible patients. Programs like Ro combine insurance navigation with affordable backup options.

The Bottom Line

People who get on GLP-1 treatment and stay consistent see real, measurable results. Clinical trials of branded semaglutide and tirzepatide show 14–20% average body weight loss in the first year when combined with diet and exercise (FDA prescribing information). These are among the most effective medical weight-loss tools ever studied, backed by large-scale randomized controlled trials and multiple FDA approvals.

The only wrong move is doing nothing because the insurance system feels too complicated. You now have the roadmap. Pick your path.

Personalized recommendation based on your insurance, goals, and timeline.

Related Guides

© 2026 The RX Index. All rights reserved. This page is reviewed and updated regularly as coverage policies change. Last comprehensive review: March 2026. Pricing and coverage details verified against manufacturer and CMS sources.