GLP-1 Providers That Take HSA: 7 Verified Picks for 2026

By The RX Index Editorial Team · Last verified: April 2, 2026 · Affiliate disclosure · Editorial standards

Who actually takes your HSA card, who makes you reimburse, and which path saves you the most — with real prices from official provider pages.

Bottom line, verified April 2026:

Most GLP-1 providers are HSA-eligible, but only a handful let you swipe your HSA card directly at checkout. The rest — including two of the biggest names in the space, Ro and Hims — require you to pay with a regular card and reimburse yourself.

Best for paying with your HSA card at checkout: MEDVi — accepts HSA/FSA directly, compounded semaglutide from $179/mo, also offers FDA-approved Wegovy and Zepbound

Best value for HSA users overall: Ro — FDA-approved medications at NovoCare/LillyDirect cash prices (Wegovy pill from $149/mo), insurance concierge, clean receipts built for easy HSA reimbursement

Best direct-card alternative: SkinnyRX — accepts HSA/FSA cards per their FAQ, compounded semaglutide and tirzepatide in multiple formats

No reimbursement steps · HSA card works at checkout

Which GLP-1 Providers Accept HSA? Full Comparison

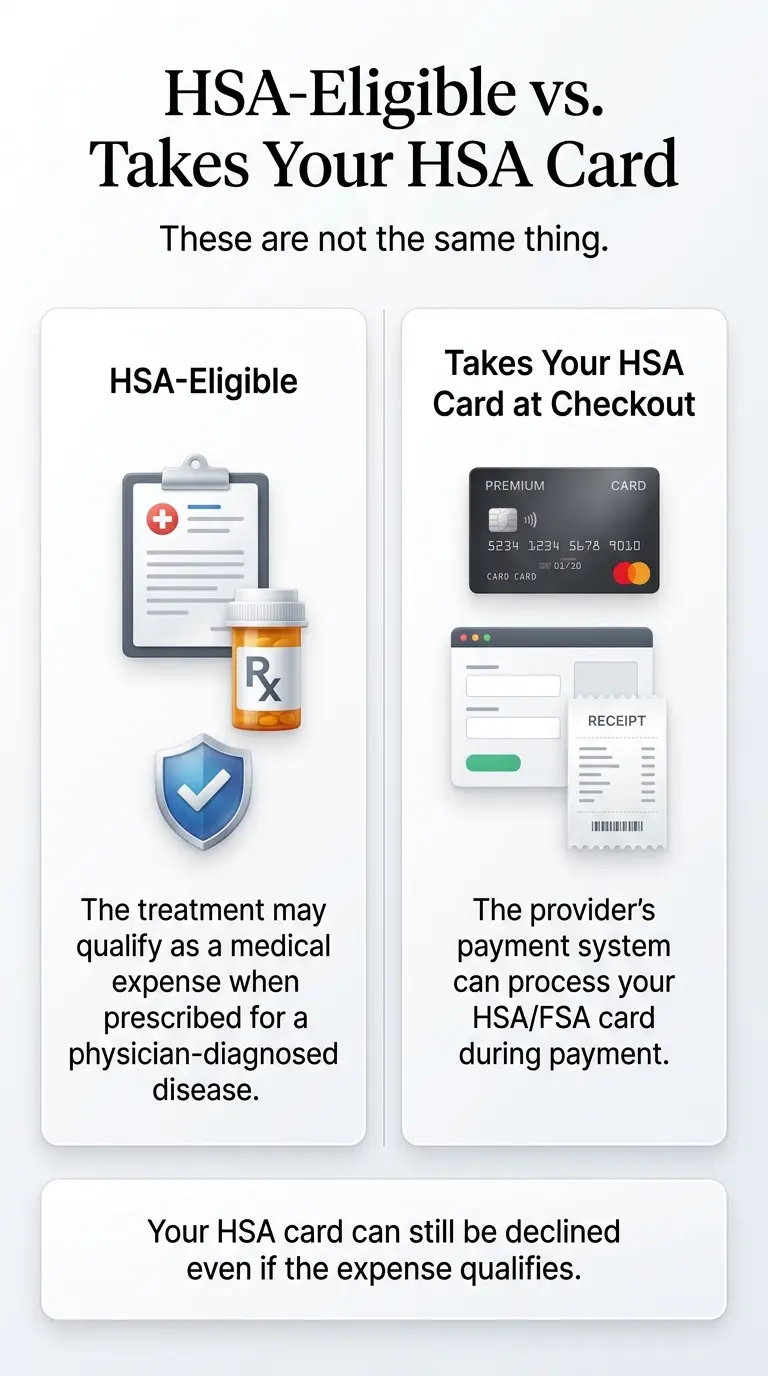

Every provider on this list offers treatment that can qualify as an HSA-eligible medical expense when prescribed to treat a physician-diagnosed condition like obesity or type 2 diabetes (per IRS Publication 502). But “qualifies for HSA” and “takes your HSA card at checkout” are completely different experiences.

| Provider | HSA Card at Checkout? |

|---|---|

| MEDVi | ✅ Direct HSA Card at Checkout |

| SkinnyRX | ✅ Direct HSA Card at Checkout |

| Sesame | ✅ Direct HSA Card at Checkout |

| LifeMD + NovoCare | ✅ Direct HSA Card at Checkout |

| Ro | ❌ Pay First, Reimburse Yourself |

| Hims / Hers | ❌ Pay First, Reimburse Yourself |

| TrimRX | ⚠️ HSA-Eligible — Direct Card Unconfirmed |

Verified from official provider payment pages and FAQs, April 2026. Membership and medication costs are listed separately — your total cost = membership + medication. Always confirm current pricing directly with the provider.

“HSA-Eligible” vs. “Takes My HSA Card” — The Key Distinction

This is the source of almost all the confusion in this category. Two completely separate concepts.

HSA-Eligible

The IRS allows the expense to be paid with HSA funds. Prescription GLP-1 medication prescribed to treat a physician-diagnosed condition generally qualifies under IRS Publication 502. This is a tax rule.

Takes Your HSA Card at Checkout

The provider’s payment system can process your HSA debit card at checkout. This is a payment-processing question. It varies by provider and has nothing to do with IRS rules.

An expense can be fully legitimate under IRS rules and still trigger a card decline if the provider doesn’t support HSA card transactions. That’s why Ro — whose GLP-1 programs clearly qualify as medical expenses — still doesn’t take the card at checkout.

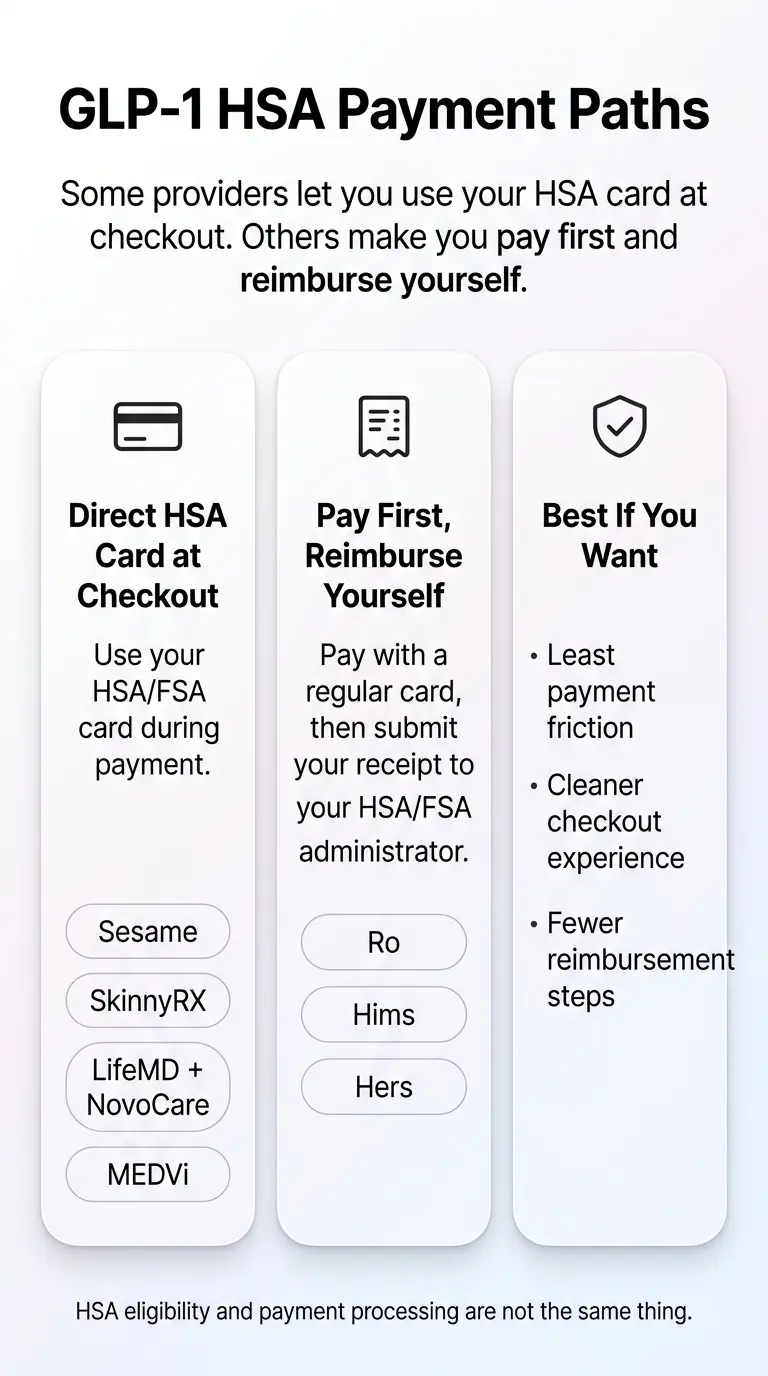

Pick Your HSA Payment Path — Then Choose a Provider

The provider decision gets simple once you know which payment path fits your situation. There are three.

Path 1: Swipe Your HSA Card at Checkout

Who this fits: You want the transaction done in one step. No floating costs on a personal card, no filing reimbursement claims, no waiting for money to come back.

Your options: MEDVi, SkinnyRX, Sesame, and LifeMD (via NovoCare) all accept HSA/FSA cards at checkout. MEDVi is the standout because it offers both compounded AND FDA-approved medication paths with direct HSA card acceptance.

Path 2: Pay First, Reimburse Yourself

Who this fits: You want the strongest FDA-approved options or insurance assistance, and you're fine submitting a receipt to your HSA portal. The tax savings are identical — the only difference is a few minutes of paperwork.

Your options: Ro is the strongest in this path. Their receipts include a detailed receipt and prescription copy designed for clean reimbursement. Their insurance concierge may get your medication partially or fully covered, reducing your HSA spend to just a copay. Hims/Hers also uses this model.

Path 3: FDA-Approved Brand-Name Medication First

Who this fits: You specifically want Wegovy, Zepbound, Ozempic, or another FDA-approved medication — not a compounded alternative.

Your options: Ro (reimbursement, lowest cash prices matching NovoCare and LillyDirect), LifeMD + NovoCare (direct HSA card), Sesame ($89/mo Rx-only subscription + brand-name at your pharmacy), and MEDVi (FDA-approved options available alongside compounded).

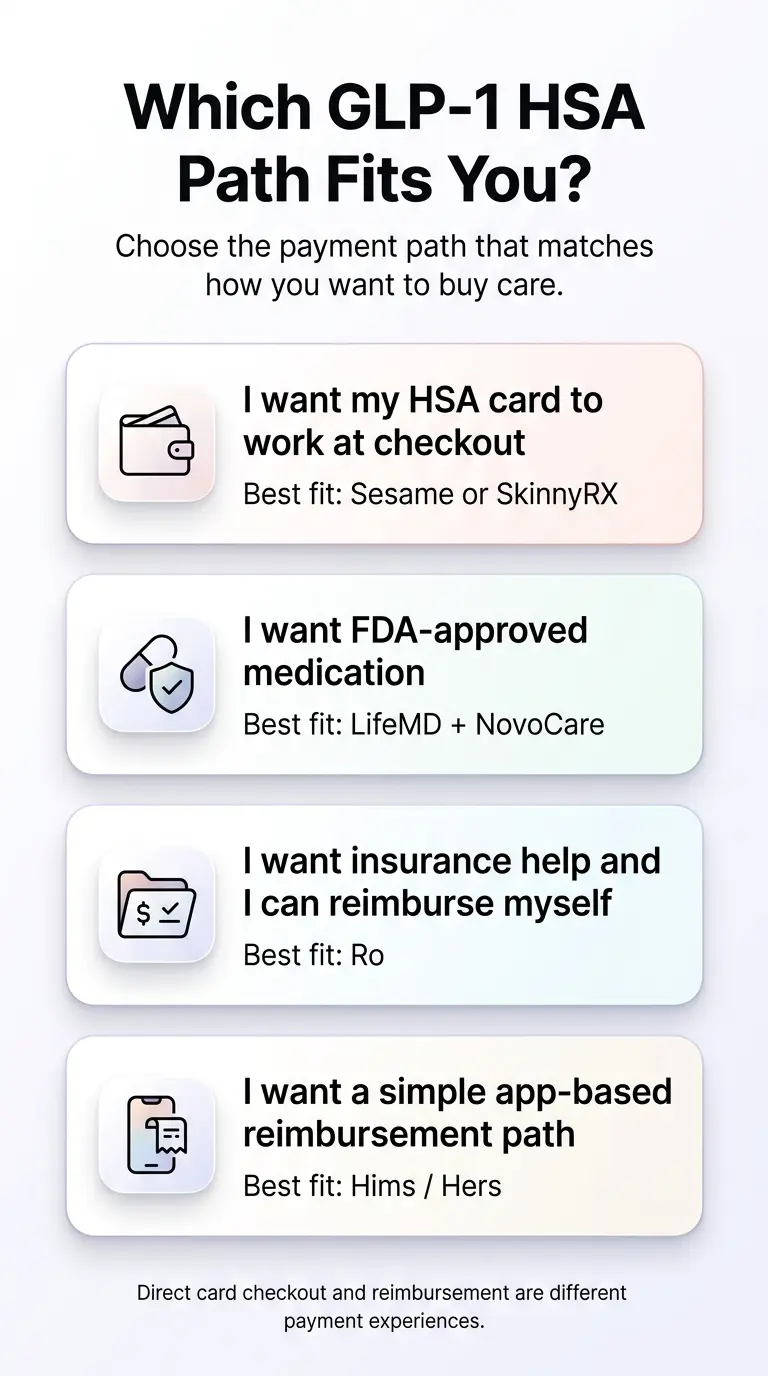

Find Your Situation — Pick Your Provider

“I want my HSA card to work at checkout, no reimbursement.”

→ MEDVi first (widest medication menu with direct card). SkinnyRX second. Sesame if you want provider choice.

“I want FDA-approved Wegovy or Zepbound — not compounded.”

→ Ro if you have insurance or want the lowest cash prices on brand-name (Wegovy pill from $149/mo). LifeMD + NovoCare if you want direct HSA card on FDA-approved.

“I want the lowest total monthly cost using my HSA.”

→ Sesame has the lowest subscription ($59/mo annual) plus cash-pay meds from $149/mo. Ro offers Wegovy pill from $149/mo cash. MEDVi starts at $179/mo all-in for compounded. See the tax savings table below to calculate your real after-tax cost.

“My FSA expires soon — I can't risk reimbursement delays.”

→ MEDVi or SkinnyRX. Direct card at checkout means your FSA funds are spent the moment you complete your purchase. No waiting.

“My HSA card got declined and I don't know what to do.”

→ A declined card does NOT mean you're ineligible. See exactly what to do in the section below.

“I honestly don't know which path fits me.”

→ Take our free 60-second GLP-1 matching quiz. We'll match you to a provider based on your insurance, HSA, and budget.

What Makes Your GLP-1 Expense Qualify for HSA

Under IRS rules, HSA funds can be used for “qualified medical expenses” — costs to diagnose, treat, mitigate, or prevent a disease. For GLP-1 medication, your expense generally qualifies when:

The IRS specifically notes that weight-loss programs qualify only when treating a specific disease diagnosed by a physician. General weight management “for appearance” does not qualify.

This matters because some providers document the medical purpose of your prescription more clearly than others — and that documentation directly affects how smooth your HSA reimbursement goes.

Provider Details

MEDVi

Best for Direct HSA Card Checkout

MEDVi is the most complete direct-card option because it accepts HSA/FSA at checkout AND offers both compounded and FDA-approved medication paths.

Verified (April 2026) — Source: glp.medvi.org

- ✓Accepts HSA and FSA payment for all treatment plans at checkout

- ✓Compounded semaglutide injections: $179/mo first month, $299/mo ongoing

- ✓Compounded semaglutide tablets: $249/mo

- ✓FDA-approved path (Wegovy, Zepbound): $99/mo membership + medication cost

- ✓Compounded daily dissolvable tablets available (needle-averse patients)

- ✓No separate membership fee on the compounded path — all-in pricing

What makes MEDVi strong for HSA users

You enter your HSA card at checkout. No reimbursement forms, no floating costs, no waiting for your money back. The consultation, medication, and shipping are bundled into one price on the compounded path — no separate membership fee.

Here’s the math that matters: MEDVi doesn’t charge a separate membership fee on the compounded path. Compare that to platforms that charge $145/mo for membership plus medication costs. When you factor in the all-in pricing and zero reimbursement friction, MEDVi’s effective cost through HSA is competitive — and the convenience of swiping your card and being done is worth real money.

Check Your Eligibility on MEDVi — HSA/FSA Accepted at Checkout

You’ve already set aside HSA money for your health. MEDVi removes the only remaining obstacle: making the checkout actually take your card.

Check Your Eligibility on MEDVi →Ro

Best Value for HSA Users Who Want FDA-Approved GLP-1

Ro does not take your HSA card at checkout. Their FAQ is clear about this. And for a page about providers that “take HSA,” that might seem like a disqualifier.

It’s not. Here’s why Ro often saves HSA users more money than direct-card providers.

Verified (April 2026) — Source: Ro HSA FAQ & Ro Pricing

- ·HSA at checkout: No — pay with personal card, then submit for HSA reimbursement

- ·Membership: $45 first month, then $145/mo

- ·Wegovy pill: from $149/mo cash

- ·Wegovy pen: from $199/mo cash

- ·Zepbound vials: $299–$449/mo cash

- ·With insurance coverage, medication costs may drop to a copay

- ·Provides detailed receipt and prescription copy with each charge — designed for HSA/FSA reimbursement

- ·Insurance concierge submits prior authorizations and appeals on your behalf

Why Ro often saves HSA users more money than direct-card providers

Ro’s insurance concierge team submits prior authorizations and fights your insurance company for GLP-1 coverage. If they succeed, your HSA only covers the copay — potentially $25–50/mo instead of hundreds. That one service can save you thousands per year.

A real scenario, 22% tax bracket:

Insurance covers Wegovy with a $50/mo copay (after Ro’s concierge handles PA)

HSA expenses: $145/mo membership + $50/mo copay = $195/mo total

Through HSA in the 22% bracket: effectively ~$137/mo after tax savings

vs. $299/mo at a direct-card compounded provider — reimbursement saves ~$1,900/year

SkinnyRX

Direct HSA Card with Format Flexibility

SkinnyRX gives you a second direct-card option with unusually broad medication format choices.

Verified (April 2026) — Source: SkinnyRX FAQ

- ✓Accepts FSA/HSA cards per their FAQ

- ✓Product pages label items as FSA/HSA eligible

- ✓Compounded semaglutide and tirzepatide: injectable, oral, and tablet formats

- ✓Multiple format options if you develop side effects on one delivery method

- ✓Pricing: Verify current rates directly at skinnyrx.com

Sesame

Lowest Subscription Cost + HSA Accepted

Sesame offers one of the most transparent pricing structures in GLP-1 telehealth, with the lowest subscription entry point we’ve seen.

Verified (April 2026) — Source: Success by Sesame

- ✓HSA/FSA accepted at checkout — itemized bill provided for submission

- ✓Subscription: from $59/mo (annual plan) or $99/mo (monthly)

- ✓Cash-pay GLP-1 medication from $149/mo (separate from subscription)

- ✓$89/mo Rx-only option: clinical care + brand-name GLP-1 prescribed to your pharmacy (potentially covered by insurance)

- ✓Live same-day video visits with a provider you choose (unusual in telehealth)

- ✓Compounded semaglutide available at competitive rates

LifeMD + NovoCare

FDA-Approved Wegovy with Direct HSA Card

If you specifically want FDA-approved Wegovy and you want to pay with your HSA card, the LifeMD + NovoCare pathway is one of the cleanest options available.

Verified (April 2026) — Sources: LifeMD Wegovy page & NovoCare Pharmacy

- ✓LifeMD's Wegovy page lists HSA/FSA as eligible

- ✓NovoCare's payment FAQ confirms FSA/HSA card acceptance

- ✓Program & provider fee: $149 (frequently discounted to $75 for new patients)

- ✓Wegovy pill: from $149/mo (medication separate from program fee)

- ✓Wegovy pen: from $199/mo

- ✓NovoCare is Novo Nordisk's own pharmacy — medication direct from manufacturer

External link · Not an affiliate

Hims / Hers

Reimbursement Model — Large Platform, More Steps

“Does Hims accept HSA?” and “Does Hers accept HSA?” are two of the most searched follow-up questions in this category. Here’s the direct answer.

Verified (April 2026) — Sources: Hims HSA page & Hims FAQ

“We recommend using a valid credit or debit card and submitting reimbursement. Payment with an FSA/HSA card may require additional steps from your provider.”

·Membership: $39 first month, then $149/mo

·Compounded injectable GLP-1: from $199/mo (6-mo plan paid upfront)

·Oral medication kits: from $69/mo (10-mo plan paid upfront)

·FDA-approved branded GLP-1s also available

The reimbursement process for Hims/Hers

Pay with a personal card. Go to your “orders” tab in the Hims or Hers app. Download your receipt. Submit it to your HSA administrator. If the receipt isn’t detailed enough (e.g., it just says “subscription”), contact support and request one that includes the medication name and prescribing provider.

When Hims/Hers make sense for HSA users: You already use the platform and you’re comfortable with a reimbursement workflow.

When another provider fits better: If HSA card acceptance matters, or you want the lowest total cost on FDA-approved medication, other providers in this comparison are stronger matches.

TrimRX

Flat-Rate Pricing — HSA Acceptance Unconfirmed

TrimRX uses a flat-rate pricing model — your monthly cost doesn’t increase when your provider titrates you to a higher dose. That’s genuinely unusual and makes HSA budgeting easier.

- ·HSA/FSA acceptance: Unconfirmed — TrimRX discusses eligibility on their blog but we could not confirm a clear direct-card policy from an official payment page

- ·Cost: Flat-rate pricing — verify current rates directly at trimrx.com

- ·Compounded semaglutide and tirzepatide

- ·Contact TrimRX directly to confirm whether your HSA card will work at checkout before committing

How Much You Save Paying Through HSA

Using your HSA isn’t a coupon. It’s the IRS letting you pay for medical treatment with dollars that were never taxed. When your HSA is funded through payroll contributions (the most common setup), those contributions bypass both federal income tax and FICA (7.65%).

| Federal Bracket | Total Savings | $149/mo Effective | $199/mo Effective |

|---|---|---|---|

| 12% | ~20% | $119 | $159 |

| 22% | ~30% | $104 | $139 |

| 24% | ~32% | $101 | $135 |

| 32% | ~40% | $89 | $119 |

Estimates for payroll-funded HSA contributions, which avoid both income tax and FICA. If you fund your HSA with after-tax contributions and deduct on your return, FICA savings don’t apply. State taxes may increase savings further. Always confirm with a tax professional.

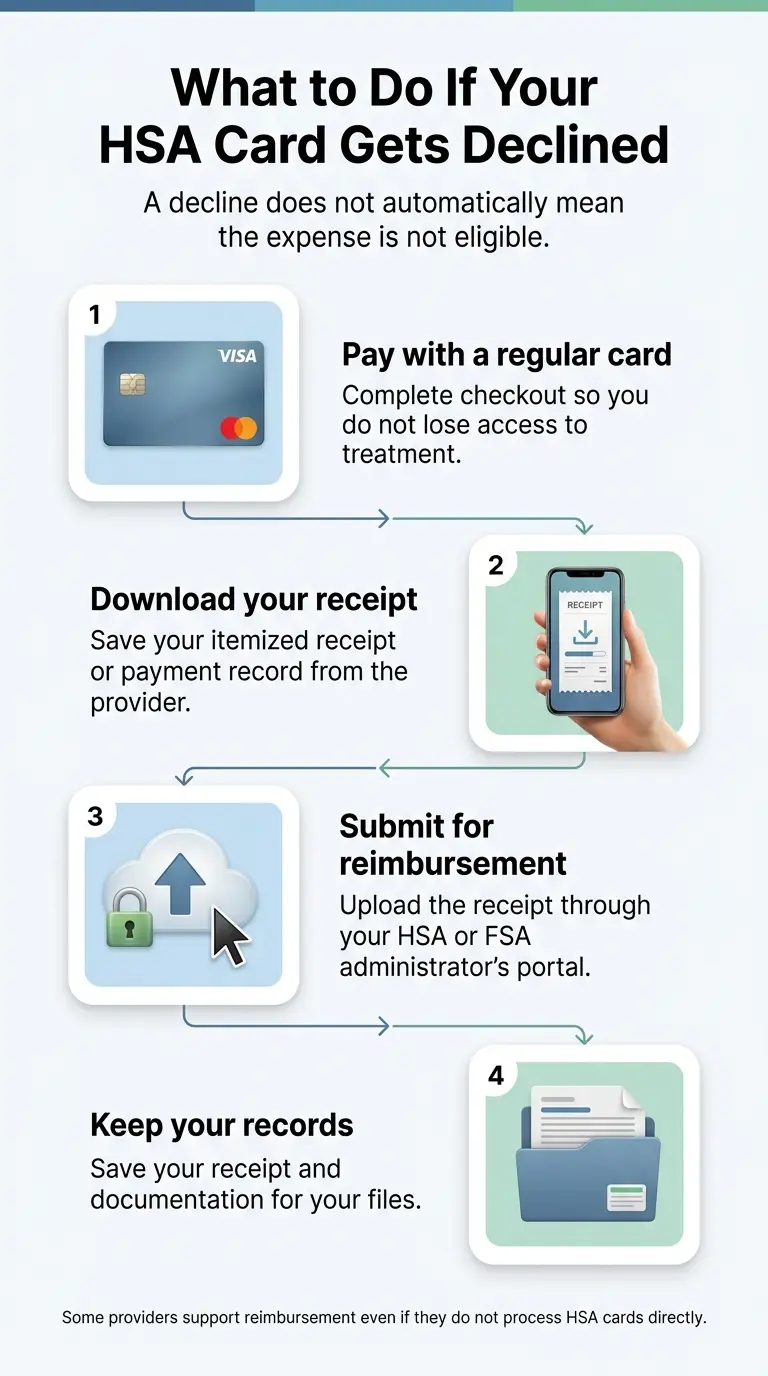

What to Do When Your HSA Card Gets Declined

This happens regularly — especially with telehealth GLP-1 providers. It’s not a stop sign. It’s a 5-minute detour.

Why it happens: The provider’s payment processor isn’t set up to accept HSA/FSA card transactions. Ro, Hims, and Hers are all built this way. It has nothing to do with whether the IRS considers the expense eligible.

Pay with your regular debit or credit card

Complete checkout normally so you don't lose access to treatment.

Download your itemized receipt

A strong receipt includes: medication name, dosage, prescribing provider name, date, and total amount. If yours says something generic, contact support and request a detailed version.

Log into your HSA administrator's portal

Fidelity, Optum, HealthEquity, and most others have a dedicated reimbursement submission section.

Upload the receipt and submit a reimbursement claim

Funds return to your bank account — typically within a few business days.

Get an LMN proactively

A Letter of Medical Necessity from your prescribing provider confirms your diagnosis and the medical purpose. Not every administrator requires one, but having it on file protects you if they ask. Most telehealth providers can generate one through their patient portal.

What Documents to Keep on File

Save these for every month of treatment. They’re your paper trail if your administrator or the IRS asks questions:

Digital copies in a phone folder work fine. Being organized now means a potential review later is a non-event.

FDA-Approved vs. Compounded GLP-1: What HSA Users Need to Know

Both can qualify as HSA-eligible medical expenses when lawfully prescribed and properly documented. The IRS qualified-medical-expense rules apply the same way regardless of whether the medication is FDA-approved or compounded.

FDA-Approved Medications

Wegovy, Zepbound, Ozempic, Mounjaro, Rybelsus, Saxenda

- ·Standardized pharmacy billing

- ·HSA administrators accustomed to these claims

- ·Minimal documentation friction

Best: Ro, LifeMD + NovoCare

Compounded Medications

Compounded semaglutide, compounded tirzepatide

- ·Not FDA-approved finished products

- ·Some administrators may request additional documentation

- ·Get LMN upfront; receipt must name the specific medication

Best: MEDVi, SkinnyRX, Sesame

Practical guidance: Make sure your receipt specifically names the medication (e.g., “compounded semaglutide injection”) rather than something vague. And choose a provider that works with properly licensed 503A or 503B compounding pharmacies.

HSA vs. FSA for GLP-1: Quick Comparison

| Feature | HSA | FSA |

|---|---|---|

| 2026 Contribution Limit | $4,400 individual / $8,750 family | $3,400 employee limit |

| Rollover | Unlimited — funds never expire | Use-it-or-lose-it (up to $680 carryover) |

| HDHP Required | Yes | No |

| Investment Growth | Yes — tax-free growth | No |

| Best for GLP-1 | Long-term treatment planning | Use before year-end if balance available |

If you have both HSA and FSA: Use FSA first (it expires). Preserve your HSA for future years — it rolls over and can be invested.

Does Ro Take HSA?

This is one of the most searched questions in this space, so let’s be direct: No, Ro does not accept HSA or FSA cards at checkout. Their FAQ explicitly states this.

But “doesn’t take your card” is not the same as “can’t use your HSA.” Every penny you spend on Ro’s weight-loss program — membership, medication, consultations — can qualify as an HSA medical expense when prescribed for a diagnosed condition. You just pay with a regular card and reimburse yourself.

Ro provides a detailed receipt and prescription copy with each charge. You download it, submit it through your HSA administrator’s portal, and the funds come back to you. Same tax savings as swiping your card — just with a few minutes of admin.

Why people still choose Ro despite no direct card: Ro offers the same NovoCare and LillyDirect cash prices on FDA-approved Wegovy and Zepbound that you’d get going direct to the manufacturer. But Ro also adds an insurance concierge that fights for coverage on your behalf. If they succeed, your HSA only needs to cover the copay — and the math changes dramatically.

Reimburse yourself via HSA · FDA-approved only · Clean receipts included

Does Hims or Hers Accept HSA?

Hims and Hers officially recommend paying with a regular credit or debit card and submitting for HSA/FSA reimbursement. Their FAQ states that “payment with an FSA/HSA card may require additional steps from your provider.”

The reimbursement process: Pay with a personal card. Go to the “orders” tab in the Hims or Hers app. Download the receipt. Submit to your HSA administrator. If the receipt doesn’t clearly itemize the medication, contact support and request a detailed version before submitting.

If you want direct HSA card checkout, MEDVi and SkinnyRX handle that. If you want the strongest reimbursement documentation for FDA-approved medications, Ro provides cleaner receipts.

Can You Use HSA with GoodRx?

Yes — if you fill a GLP-1 prescription at a retail pharmacy and use a GoodRx discount to lower the price, you can still use HSA funds for what you pay. The GoodRx discount doesn’t change eligibility.

What you can’t do: use HSA to buy a GoodRx Gold membership. The membership itself isn’t a medical expense.

When GoodRx is useful: You have a brand-name prescription being filled at a retail pharmacy rather than through a bundled telehealth program. When it’s not: You’re enrolled in a bundled GLP-1 program where medication is part of the monthly subscription price.

What About Medicare Coverage for GLP-1?

If you’re exploring HSA for GLP-1 and you’re also Medicare-eligible, this matters.

CMS announced the Medicare GLP-1 Bridge, beginning July 2026, where eligible Part D beneficiaries would pay $50/mo for covered GLP-1 medications (Wegovy and Zepbound). If you’re 65+ and potentially eligible, your best financial move might be waiting for that coverage rather than self-paying through HSA.

If you’re under 65 with an HDHP + HSA: This doesn’t affect you. HSA remains your strongest tax-advantaged path.

How We Checked These Providers

For each provider, we reviewed:

What we won’t do:

- ·We don’t label a provider as “accepts HSA” unless the claim is supported by their official page or FAQ

- ·We don’t use star ratings or review schema for providers we haven’t collected first-party review data on

- ·We don’t claim “same active ingredient” for compounded medications

- ·We update this page when provider policies or pricing change

Frequently Asked Questions

Can I use HSA for semaglutide for weight loss?

Semaglutide prescribed to treat a physician-diagnosed condition — such as obesity, type 2 diabetes, or overweight with a weight-related comorbidity — can qualify as a medical expense for HSA purposes under IRS Publication 502. Both brand-name (Wegovy, Ozempic) and compounded semaglutide can qualify when properly prescribed and documented.

Is tirzepatide HSA eligible?

Under the same IRS rules as semaglutide — tirzepatide (Zepbound, Mounjaro, or compounded) prescribed for a medical condition can qualify as an HSA-eligible medical expense. Documentation requirements are the same.

Is Wegovy FSA eligible?

Yes. Wegovy is FDA-approved for weight management. When prescribed, it qualifies as a medical expense for FSA reimbursement. A prescription is typically sufficient documentation.

Is Ozempic eligible for FSA?

Yes. Ozempic is FDA-approved for type 2 diabetes and qualifies for FSA. If prescribed off-label for weight management, a Letter of Medical Necessity strengthens the claim.

Does Ro take HSA?

No — Ro does not accept HSA or FSA cards at checkout. Their FAQ explicitly states this. However, all Ro GLP-1 expenses can qualify as HSA-eligible medical expenses, and Ro provides a detailed receipt and prescription copy designed for HSA reimbursement. You pay with a regular card and reimburse yourself through your HSA administrator.

Does Hims or Hers accept HSA?

Hims and Hers recommend paying with a regular card and submitting for HSA/FSA reimbursement. Their FAQ states that payment with an FSA/HSA card may require additional steps. Receipts are available in the orders tab of the app.

Can you use HSA with GoodRx?

Yes — you can use HSA to pay for a prescription filled with a GoodRx discount. You cannot use HSA for a GoodRx Gold membership itself. The GoodRx discount doesn't change HSA eligibility for the prescription.

Are compounded GLP-1s HSA eligible?

Compounded GLP-1 medications can qualify as HSA-eligible medical expenses when lawfully prescribed to treat a physician-diagnosed condition and properly documented. Some HSA administrators may request additional documentation such as a Letter of Medical Necessity. Compounded drugs are not FDA-approved finished products.

Do I need a Letter of Medical Necessity for HSA to cover GLP-1?

Not always required, but strongly recommended — especially for weight-management prescriptions and compounded medications. Some FSA administrators require an LMN before approving expenses. Having one on file protects you if your plan ever questions the claim.

What if my HSA card is declined at a GLP-1 provider?

A card decline does not mean you're ineligible. It means the provider's payment system doesn't process HSA card transactions. Pay with a regular card, download your itemized receipt, and submit for HSA reimbursement through your administrator. The tax savings are identical either way.

What documents should I save for HSA GLP-1 claims?

Itemized receipt (medication name, dosage, provider, date, amount), prescription record, Letter of Medical Necessity, and visit documentation for telehealth consultations. Digital copies work fine.

Still Not Sure Which GLP-1 Program Is Right for You?

You’ve done more research than most people ever will. You understand the payment paths. You know which providers take your card, which don’t, and what the real costs look like after HSA savings.

The only thing left is matching your specific situation — your insurance, your HSA balance, your medication preference, and your monthly budget — to the right provider.

Take the Free 60-Second GLP-1 Matching Quiz

Answer 5 questions about your insurance, HSA, and budget — and get a personalized recommendation with your HSA savings calculated. No signup. No email gate.

Take the Free GLP-1 Matching Quiz →60 seconds · No signup · No commitment

Related guides

- GLP-1 Providers That Take FSA: 8 Verified Picks (2026)

- Best GLP-1 Providers That Accept Insurance: 6 Verified Picks (2026)

- Best Online Wegovy Provider: 7 Legit Options (2026)

- Best Telehealth for Wegovy: Full Provider Breakdown

- How to Appeal a GLP-1 Insurance Denial (Step-by-Step)

- Cheapest GLP-1 Without Insurance: Full Cash-Pay Comparison

- Does Medicare Cover Wegovy for Weight Loss?

Sources

- IRS Publication 502 — Medical and Dental Expenses

- IRS Publication 969 — HSAs and Other Tax-Favored Health Plans

- IRS FAQ — Medical Expenses Related to Nutrition, Wellness, and Health

- IRS 2026 Inflation Adjustments

- Ro HSA/FSA FAQ

- Ro Weight Loss Pricing

- Hims HSA/FSA Page

- Hims Weight Loss FAQ

- Hims Drug Pricing

- Sesame Weight Loss Program

- LifeMD Wegovy Page

- NovoCare Pharmacy

- MEDVi GLP-1 Program

- SkinnyRX FAQ

- GoodRx HSA Support

- CMS — Medicare GLP-1 Bridge

- FDA — Clarification on Compounded GLP-1s

Affiliate disclosure: We may earn commissions from MEDVi, Ro, SkinnyRX, Sesame, Hims, and TrimRX links on this page. Rankings are based on our verified HSA payment policies and methodology above — not commission rates. Full disclosure →

Tax disclaimer: This content is for informational purposes only and does not constitute tax or financial advice. Consult a tax professional for your specific situation.

Medical disclaimer: GLP-1 medications require a prescription from a licensed healthcare provider.