HSA & FSA Eligibility Guide ·

By The RX Index Editorial Team · · Pricing verified against NovoCare.com · IRS rules verified against Publication 502 (2025)

Can You Use HSA or FSA for Ozempic?

Published:

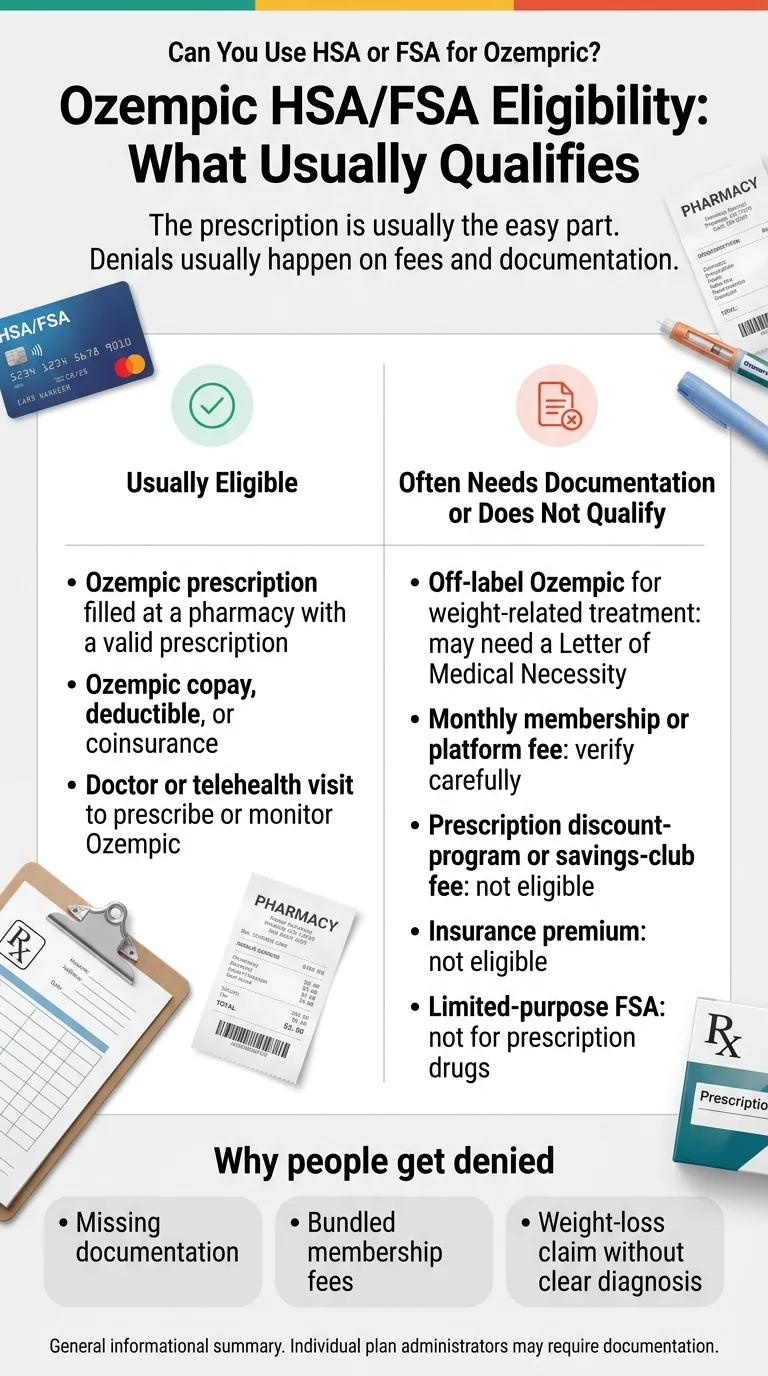

Can you use HSA or FSA for Ozempic? Yes — you can generally use your HSA or FSA to pay for Ozempic if you have a valid prescription for a diagnosed medical condition. But here’s what the other pages on this topic don’t tell you: the Ozempic pen itself is usually the straightforward part. The denials and surprises happen on the surrounding charges — membership fees, platform fees, discount-program enrollment fees — and on off-label weight-loss prescriptions that lack proper documentation.

Three separate sets of rules govern what you can actually do with your pre-tax dollars for Ozempic, and every article we reviewed blurs all three together. We’re going to separate them clearly so you know exactly what qualifies, what doesn’t, and what paperwork to have ready before you swipe.

The RX Index Ozempic HSA/FSA Eligibility Matrix

| Ozempic-related expense | HSA eligible? | FSA eligible? | What trips people up | What to save |

|---|---|---|---|---|

| Ozempic prescription filled at a pharmacy (valid Rx for a diagnosed condition) | ✅ Yes | ✅ Yes | The drug itself is usually the straightforward part; documentation requirements vary by administrator | Itemized pharmacy receipt + Rx details |

| Ozempic prescribed off-label for obesity or weight-related disease | ⚠️ Yes, but documentation-sensitive | ⚠️ Yes, but documentation-sensitive | Ozempic's label is for type 2 diabetes — administrators may ask for proof the prescription treats a diagnosed disease, not general wellness | Itemized receipt + Rx + LMN |

| Insurance copay, deductible, or coinsurance for Ozempic | ✅ Yes | ✅ Yes | Insurance coverage and HSA/FSA eligibility are separate questions — one can deny while the other approves | EOB + pharmacy receipt |

| Doctor or telehealth visit to obtain or monitor Ozempic | ✅ Yes | ✅ Yes | The medical consultation qualifies; a bundled platform or access fee may not | Itemized visit receipt |

| Monthly membership or access fee tied to a telehealth GLP-1 program | ⚠️ Verify with administrator | ⚠️ Verify with administrator | Flat retainer-style membership fees are generally not reimbursable unless actual medical services are billed separately; see the 2026 DPC nuance | Itemized bill showing medical services |

| Prescription discount-program or savings-club enrollment fee | ❌ No | ❌ No | These are not medical expenses under IRS rules — they provide access to a discount, not treatment of a disease | Don't use HSA/FSA for this line item |

| Insurance premium | ❌ No (limited HSA exceptions exist) | ❌ No | HSA has narrow statutory exceptions (COBRA, certain unemployment situations, long-term care within IRS limits); FSA cannot cover premiums | N/A |

| Limited-purpose FSA (LPFSA) | N/A | ❌ Not for Rx drugs | LPFSAs are generally restricted to dental, vision, and preventive care | Check plan document |

Sources: IRS Publication 502, “Medical and Dental Expenses” (2025 edition); IRS Publication 969; IRS Tax Topic 502; HealthCare.gov FSA guidance; FSAFEDS eligible expense list.

What we actually verified for this page

- ✅ IRS Publication 502 (2025): prescribed-drug eligibility, weight-loss expense rule, exclusions

- ✅ IRS Publication 969: HSA rules, premium limitations, distribution rules, 2026 DPC provision

- ✅ Official Ozempic prescribing information and all three FDA-approved indications

- ✅ NovoCare Pharmacy: self-pay pricing, FSA/HSA acceptance, copay-card policy, FDA-indication requirement

- ✅ Novo Nordisk Savings Card: terms, eligibility, savings limits

- ✅ 2026 HSA contribution limit: $4,400 individual / $8,750 family (IRS Rev. Proc. 2025-19)

- ✅ 2026 FSA contribution limit: $3,400 (IRS tax year 2026 inflation adjustments)

The IRS Rule That Governs Everything

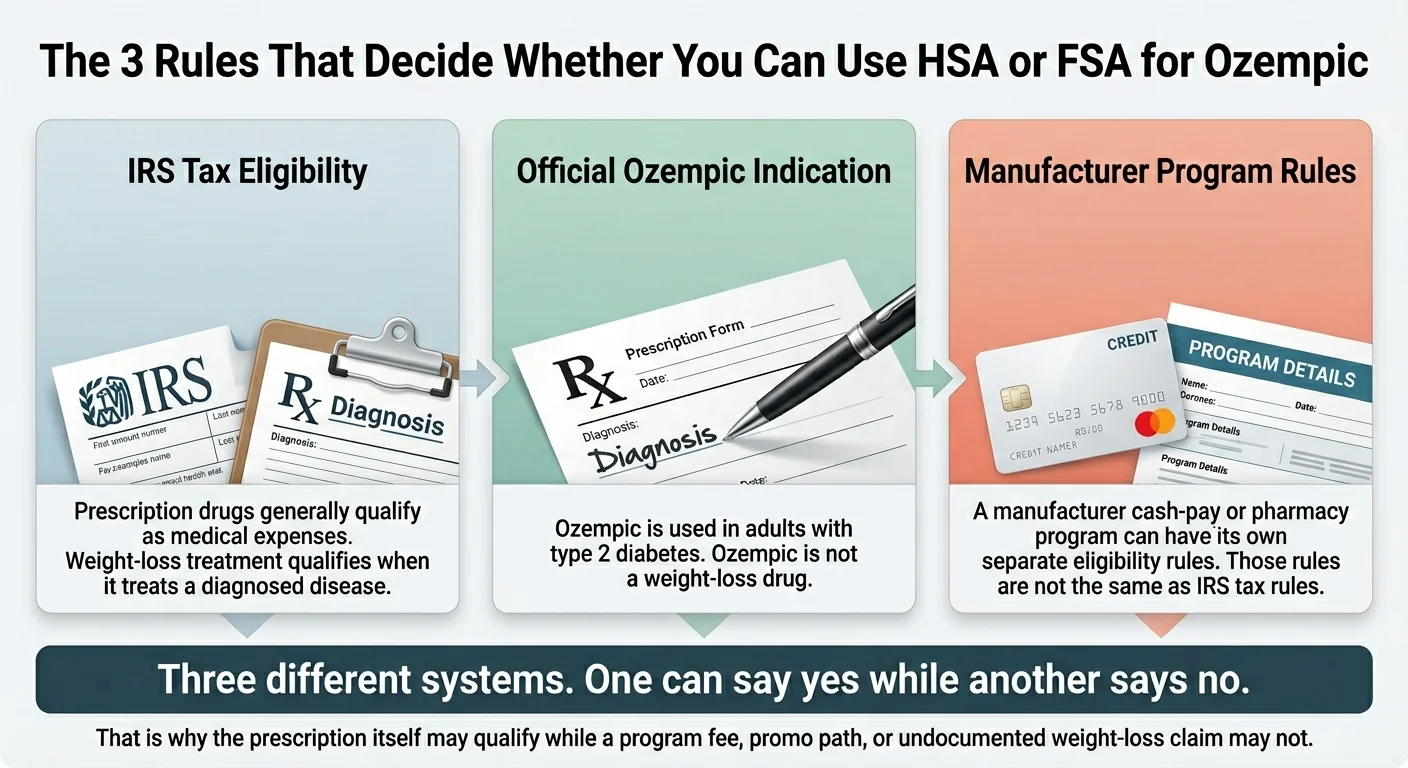

Under IRS Publication 502, HSA and FSA funds can be used for “the diagnosis, cure, mitigation, treatment, or prevention of disease.” Prescription medications prescribed by a licensed provider to treat a diagnosed medical condition qualify as medical expenses under Section 213(d) of the Internal Revenue Code. This is the foundational rule that makes Ozempic generally eligible.

But here’s where most articles stop — and where the real confusion starts. Three separate eligibility systems apply to Ozempic, and they don’t always agree:

| IRS tax eligibility Can your HSA/FSA pay? | FDA-approved indication What is Ozempic officially for? | NovoCare self-pay program Can you access $349/$499 pricing? | |

|---|---|---|---|

| Governed by | IRS Publication 502 / IRC Section 213(d) | FDA-approved labeling | Novo Nordisk program terms |

| Key test | Is it a prescribed drug treating a diagnosed disease? | Is it used for an FDA-approved indication? | Is the prescription for an FDA-approved indication? Government beneficiaries excluded. |

| Ozempic for type 2 diabetes | ✅ Qualifies | ✅ On-label | ✅ Eligible |

| Ozempic off-label for diagnosed obesity | ✅ Generally qualifies (IRS allows weight-loss treatment for a "specific disease diagnosed by a physician, such as obesity, hypertension, or heart disease" — Pub 502) | ❌ Not an FDA-approved Ozempic indication | ❌ NovoCare terms require FDA-approved indication |

| Ozempic for cosmetic / general wellness weight loss | ❌ Does not qualify | ❌ Not on-label | ❌ Not eligible |

The key insight most articles miss

An Ozempic expense can be a qualified medical expense for your HSA or FSA even when it doesn’t qualify for the manufacturer’s self-pay program. And your insurance can deny Ozempic while your HSA or FSA still covers it. These are genuinely different questions with different answers.

Sources: IRS Publication 502, sections on “Medicines and Drugs” and “Weight-Loss Program”; IRS FAQ on medical expenses related to nutrition, wellness, and general health; Ozempic prescribing information; NovoCare Pharmacy terms (novocare.com).

Can You Use HSA or FSA for Ozempic When It’s Prescribed for Weight Loss?

It depends on what your doctor documented — and the answer involves a nuance that most pages on this topic get wrong.

Ozempic is FDA-approved for three type 2 diabetes-related indications: improving glycemic control in adults with type 2 diabetes, reducing the risk of major cardiovascular events in adults with type 2 diabetes and established cardiovascular disease, and reducing the risk of worsening kidney disease and cardiovascular death in adults with type 2 diabetes and chronic kidney disease. Ozempic’s own labeling states that it is not indicated for weight loss.

But the IRS doesn’t follow FDA labeling for eligibility purposes. Under Publication 502, weight-loss treatment qualifies as a medical expense when it treats a specific disease diagnosed by a physician — the examples given are obesity, hypertension, and heart disease. So if your doctor prescribes Ozempic off-label for weight management and documents that it’s treating diagnosed obesity (generally BMI ≥30) or a weight-related disease like hypertension, the IRS rule generally supports eligibility.

Off-label weight-loss prescriptions attract more scrutiny

When Ozempic is prescribed for type 2 diabetes, the medical purpose is apparent and transactions tend to process without additional documentation requests. When it’s prescribed for weight management — even with a legitimate diagnosis — administrators are more likely to flag the transaction and request supporting documentation.

Do You Need a Letter of Medical Necessity for Ozempic?

Not always. Here’s the real framework — not the oversimplified “always get one” or “just need a prescription” that other pages give you.

When a prescription alone is typically sufficient

Your Ozempic is prescribed for type 2 diabetes. The diagnosis directly matches the FDA-approved indication, and the medical purpose is clear from the prescription itself.

When an LMN is the smart move

Your Ozempic is prescribed off-label for weight management — even with a legitimate diagnosis like obesity or hypertension. An LMN from your prescribing provider establishes the clinical justification before your administrator asks for it, rather than after a denial.

When an LMN is essential

Your first claim was denied or your card was declined. Your administrator flagged the purchase. You’re paying through a telehealth provider where the merchant category code doesn’t clearly indicate “pharmacy” or “medical.”

On forums focused on GLP-1 reimbursement, users report claims initially denied for lack of an LMN, and FSA administrators requiring proof of medical need before processing GLP-1 reimbursement requests. (These are anecdotal user experiences illustrating administrator behavior — not eligibility rules.)

What your LMN should include

- •Your name and date of the letter

- •The specific diagnosed medical condition (with ICD-10 code if your provider is willing)

- •A clear statement that Ozempic is medically necessary to treat that condition

- •A statement that the prescription is not for cosmetic or general wellness purposes

- •The provider's signature, credentials, and contact information

Our recommendation: get the LMN before your first fill. Having it on file prevents a denial from becoming a delay.

What Does Ozempic Actually Cost in 2026 — and How Much Does HSA/FSA Save You?

Ozempic’s official list price is $1,027.51 per pen (28-day supply), per Novo Nordisk. But most people don’t pay that number. The actual cost depends on which payment path you take.

Verified Ozempic Pricing Paths (April 2026)

| Payment path | What you pay | HSA/FSA accepted? | Key details and limitations |

|---|---|---|---|

| Commercially insured + Novo Nordisk Savings Card | As little as $25 per Rx (max savings $100/month, up to 48 months) | ✅ Yes — pay your out-of-pocket portion with HSA/FSA | Requires commercial insurance with Ozempic coverage. Government-plan beneficiaries excluded. |

| NovoCare Pharmacy — new patient intro | $199 per fill for 0.25mg or 0.5mg (limit: 2 monthly fills, 11/17/2025–6/30/2026) | ✅ Yes — NovoCare confirms FSA/HSA cards accepted at checkout | Must be prescribed for an FDA-approved indication. Payments do not count toward insurance deductible or OOP max. NovoCare does not accept copay cards. |

| NovoCare Pharmacy — ongoing | $349/month (0.25mg–1mg) · $499/month (2mg) | ✅ Yes — FSA/HSA cards accepted | Same FDA-indication requirement. Government beneficiaries excluded. Free home delivery. |

| Regular pharmacy — no insurance | $1,027.51 list price; third-party discount cards may reduce to ~$825–$1,100 | ✅ Yes — with valid Rx for diagnosed condition | Discount-card enrollment fees are not HSA/FSA eligible, but the discounted prescription price is. |

| Telehealth provider (brand-name Ozempic) | Varies. Ro lists approximately $900–$1,100/month without insurance; membership from $39 first month, then as low as $74/month annual | ⚠️ Medication and medical visits: yes. Membership fee: verify with your administrator. | Medical consultations and prescription costs generally qualify. Flat membership/access fees may not. |

Sources: Ozempic.com/savings-and-resources (verified April 2026); NovoCare Pharmacy terms (novocare.com); Ro pricing page (ro.co). Third-party pharmacy pricing approximate — verify before filling.

| Provider claim | What we verified | Source | Verified |

|---|---|---|---|

| NovoCare: "We accept payment from FSA/HSA accounts" | Confirmed on official NovoCare FAQ and HCP pharmacy page | novocare.com/pharmacy.html | |

| NovoCare self-pay pricing as shown above | Confirmed via NovoCare terms and conditions | novocare.com/eligibility/pharmacy.html | |

| NovoCare: does not accept copay cards | Confirmed on official NovoCare FAQ | novocare.com/hcp/pharmacy.html | |

| Novo Nordisk Savings Card: as little as $25 per Rx | Confirmed; subject to $100/month max savings, 48-month limit, commercial insurance required | ozempic.com/savings-and-resources | |

| Ro: membership $39 first month, then $149/month or $74/month annual | Stated on Ro pricing page; not independently verified beyond published pricing | ro.co |

How Much Does Paying With HSA or FSA Actually Save You?

When you pay for Ozempic with pre-tax HSA or FSA dollars, you effectively get a discount equal to your combined marginal tax rate. For most employed people contributing through payroll, the effective savings rate is 25%–40%+.

| What you pay for Ozempic | After-tax cost at ~30% rate | After-tax cost at ~35% rate | Annual savings vs. after-tax |

|---|---|---|---|

| $25/mo (insured + savings card) | ~$17.50 | ~$16.25 | ~$90–$105/yr |

| $199/mo (NovoCare intro) | ~$139 | ~$129 | ~$720–$840/yr |

| $349/mo (NovoCare ongoing) | ~$244 | ~$227 | ~$1,260–$1,464/yr |

| $499/mo (NovoCare 2mg) | ~$349 | ~$324 | ~$1,800–$2,100/yr |

These figures are illustrative. Your actual tax benefit depends on your federal bracket, state tax rate, whether contributions are made through payroll, and your overall tax situation. Consult a tax professional for personalized guidance.

Paying $349/month through your HSA at a 30% combined rate saves you roughly $105/month. That’s over $1,200/year — a meaningful number on an ongoing medication.

NovoCare Pharmacy: The Clearest HSA/FSA Path for Self-Pay Ozempic

NovoCare Pharmacy accepts FSA/HSA cards at checkout, ships free, and charges $349/month for most doses ($199/month intro for new patients on starter doses through ). Requires an FDA-approved indication. Does not accept copay cards. Payments do not count toward your deductible.

See current NovoCare Ozempic pricing and terms →Which Ozempic-Related Charges Do NOT Qualify?

Every other page about Ozempic and HSA/FSA focuses on what qualifies. We’re going to be equally specific about what doesn’t — because that’s where the real financial mistakes happen.

Insurance premiums — No

You cannot use HSA or FSA to pay health insurance premiums, with limited HSA exceptions (COBRA continuation coverage, premiums while receiving unemployment compensation, and long-term care premiums within IRS age-based limits per Publication 969). Your monthly insurance premium does not become HSA/FSA eligible just because you’re using the insurance to access Ozempic.

Prescription discount-program or savings-club enrollment fees — No

If you pay an enrollment or membership fee to access a discount drug card or coupon service, that fee is not a medical expense under IRS rules. You can use HSA/FSA to pay for the prescription itself once the discount is applied — just not the access fee.

Flat monthly membership or platform fees — Verify carefully

Many telehealth GLP-1 programs charge a monthly membership that bundles access, messaging, provider availability, and sometimes medication. FSA administrators have historically distinguished between charges for actual medical services and flat retainer-style access fees. If the provider can bill medical services separately from the membership, the medical services portion is typically eligible. The blanket membership fee, on its own, may not be.

2026 HSA nuance that made headlines but has narrow application

The One Big Beautiful Bill introduced a provision allowing certain direct primary care (DPC) arrangement fees to be paid from HSAs starting in 2026. However, IRS guidance on this provision excludes fixed-fee arrangements that include prescription drugs or services beyond primary care. That means most GLP-1 telehealth membership fees should not be assumed HSA-eligible under the new DPC rule, even though “HSA + membership fees” made news. Verify your specific program with your administrator before assuming eligibility. (Verify current status of IRS Notice 2026-05.)

Late fees — No

Administrative charges, not medical expenses.

Bundled invoice tip

If a telehealth program sends you one bundled invoice that combines medication + consultation + membership, ask for an itemized breakdown. The medication and consultation portions are generally eligible. The membership fee may not be. Getting that line-item separation before you submit for reimbursement can be the difference between an approved claim and a denial.

What If Your HSA/FSA Card Gets Declined — or Your Claim Is Denied?

A declined card doesn’t automatically mean the expense is ineligible. Here’s what actually happens and how to recover.

Common reasons for card declines

- • The merchant category code (MCC) at the telehealth provider isn’t recognized as “medical” or “pharmacy”

- • Your administrator auto-flagged the purchase for review

- • The transaction exceeds your available balance

- • The provider processed the charge under a general category that doesn’t auto-approve

Recovery steps

Don't delay your prescription. Pay with a regular credit or debit card.

Get an itemized receipt that includes: your name, medication name and dose, date of service, amount paid, and pharmacy or provider name and address.

Log into your HSA or FSA administrator's portal and submit a manual reimbursement claim with the receipt.

If your administrator asks for more, submit your prescription details and/or LMN.

If the claim is denied, read the denial reason:

Missing documentation — easily fixable. Submit the receipt and LMN.

Ineligible expense type — resubmit with an itemized receipt clearly showing the medical nature of the charge.

Weight-loss exclusion — submit an LMN from your prescriber explicitly stating the diagnosed condition.

Keep all reimbursement documentation with your tax records. The IRS can audit HSA distributions.

FSA use-it-or-lose-it: don’t miss the deadline

FSA plans are generally use-it-or-lose-it — unused funds may be forfeited at the end of the plan year. Your employer’s plan may offer a carryover (up to $680 for 2026) or a grace period of up to 2.5 months — but not both. Check your plan’s specific deadlines. The 2026 FSA contribution limit is $3,400. That covers 9+ months of treatment at many provider price points.

HSA: no deadline, rolls over forever

HSA funds roll over indefinitely. You own the account even if you change jobs. There is no deadline for HSA reimbursement — you can pay out of pocket today and reimburse yourself from your HSA later, as long as the expense occurred after your HSA was established and you keep the receipt. 2026 HSA limits: $4,400 individual, $8,750 family (IRS Rev. Proc. 2025-19).

What’s the Right Path for Your Situation?

If you already have an Ozempic prescription for type 2 diabetes

You’re in the clearest position. The FDA indication matches, the IRS eligibility is established by the prescription, and NovoCare’s self-pay program is available if you’re uninsured or self-paying. Save your pharmacy receipt. Pay with your HSA/FSA card at the pharmacy or through NovoCare (they accept FSA/HSA). If you have commercial insurance, activate the Novo Nordisk Savings Card first to bring your copay as low as $25, then pay that copay with HSA/FSA for an additional tax benefit.

If you’re using Ozempic off-label for obesity or a weight-related disease

Get the Letter of Medical Necessity before your first fill. Have your provider document the diagnosed condition clearly. Your HSA/FSA eligibility is governed by the IRS rule on disease-based weight-loss treatment, not the FDA label. But be aware: NovoCare’s self-pay pricing is not available for off-label use, so you’ll fill at a regular pharmacy or through a telehealth provider.

Cost check: if you’re paying $998+/month at retail for off-label Ozempic when semaglutide is also available through Wegovy (FDA-approved for weight management, at $349/month through NovoCare) — the Wegovy path may give you both better HSA/FSA documentation standing and better pricing. Your doctor can help determine which medication is the right clinical fit.

If you need brand-name Ozempic and want help checking insurance coverage

Ro checks coverage for free, carries FDA-approved GLP-1 options including Zepbound® (tirzepatide) and Foundayo™ (orforglipron), and starts at $39 for the first month, then as low as $74/month with an annual plan paid upfront. Medication is priced separately.

Check your coverage and see current Ro pricing → (sponsored affiliate link, opens in a new tab)If your FSA funds are about to expire

With the 2026 FSA contribution limit at $3,400 and the use-it-or-lose-it deadline approaching, expiring FSA funds are a legitimate reason to start a GLP-1 program now rather than waiting — assuming you have a qualifying diagnosis. That $3,400 covers 9+ months of treatment at many provider price points. Make sure you have the prescription and documentation in place first.

Not sure which path fits?

Take our free 60-second quiz — we’ll ask about your insurance, diagnosis, and budget, then show you the options that work for your situation, including which accept HSA/FSA at checkout.

Take the free 60-second GLP-1 matching quiz →Frequently Asked Questions

Is Ozempic HSA eligible?

Yes, when prescribed for a diagnosed medical condition such as type 2 diabetes, obesity, hypertension, or heart disease. The prescription establishes medical necessity. Off-label weight-loss use may require a Letter of Medical Necessity to satisfy your administrator's documentation requirements.

Is Ozempic FSA eligible?

Yes, under the same IRS rules as HSA. The expense must be for a prescribed medication treating a diagnosed disease. FSA administrators may require additional documentation for weight-management claims, and FSA funds generally must be used within the plan year (check your plan for carryover or grace-period provisions).

Can I use HSA/FSA for Ozempic if it's for weight loss, not diabetes?

It depends on your documented diagnosis. If your provider has diagnosed obesity, hypertension, heart disease, or another qualifying condition and prescribed Ozempic to treat it, that generally qualifies under IRS Publication 502's weight-loss treatment rule. If the prescription is for cosmetic or general-wellness weight loss without a disease diagnosis, it does not qualify.

Does NovoCare Pharmacy accept HSA/FSA cards?

Yes. NovoCare's official FAQ confirms they accept FSA/HSA card payments at checkout. NovoCare does not accept copay cards. NovoCare payments are processed outside insurance and do not count toward your deductible or out-of-pocket maximum.

Does NovoCare's Ozempic self-pay price count toward my insurance deductible?

No. NovoCare Pharmacy operates as a cash-pay program, processed outside insurance. Payments do not count toward any deductible or out-of-pocket maximum.

Can I use HSA/FSA for my Ozempic copay?

Yes. Copays, deductibles, and coinsurance for medical care are qualified medical expenses under IRS rules.

Can I stack the Novo Nordisk Savings Card with HSA/FSA?

Yes, in a specific way. If you're commercially insured and the savings card reduces your out-of-pocket cost, you can pay the remaining copay with HSA/FSA funds. You cannot apply HSA/FSA and the savings card to the same dollar — no double-dipping.

Can I use HSA/FSA for a telehealth visit to get an Ozempic prescription?

Generally yes. Medical consultations are qualified medical expenses. If the telehealth provider charges a separate membership or platform fee beyond the consultation, that fee may not qualify — see the section on non-eligible charges above.

Does my telehealth GLP-1 membership fee qualify for HSA/FSA?

It depends on how the fee is structured and how your administrator classifies it. Flat access or retainer fees that are not tied to specific medical services are often not reimbursable. The 2026 HSA DPC provision has narrow IRS exclusions that likely exclude most GLP-1 program memberships. Ask for an itemized bill and verify with your administrator.

What happens if I use HSA funds for a non-eligible Ozempic expense?

You'll owe regular federal income tax on the amount, plus a 20% additional tax if you're under age 65. After 65, the 20% penalty goes away but income tax still applies. For FSA, your employer may require repayment of the ineligible amount.

Can I reimburse myself from my HSA for an Ozempic expense I paid out of pocket?

Yes. HSA reimbursement has no deadline — you can pay out of pocket today and reimburse yourself later, as long as the expense occurred after your HSA was established and you keep the receipt.

How We Verified This Page

What we verified

- ✅ IRS Publication 502 (2025 edition): prescribed-drug eligibility rule, weight-loss expense rule, transportation rule, and exclusions

- ✅ IRS Publication 969: HSA recordkeeping, premium limitations, distribution rules, and the 2026 DPC provision

- ✅ IRS FAQ on medical expenses related to nutrition, wellness, and general health (irs.gov)

- ✅ Official Ozempic prescribing information and all three FDA-approved indications (ozempic.com)

- ✅ NovoCare Pharmacy: self-pay pricing, FSA/HSA acceptance, copay-card policy, FDA-indication requirement

- ✅ Novo Nordisk Savings Card: terms, eligibility, and savings limits

- ✅ 2026 HSA limits: $4,400 individual / $8,750 family (IRS Rev. Proc. 2025-19)

- ✅ 2026 FSA limit: $3,400 (IRS tax year 2026 inflation adjustments)

- ✅ Ro pricing: published pricing page (ro.co)

What we did not assume

- • We did not assume all telehealth membership fees are HSA/FSA eligible

- • We did not assume NovoCare pricing applies to off-label prescriptions (their terms explicitly require FDA-approved indications)

- • We did not assume every administrator treats weight-loss claims identically — requirements vary by plan

What may vary

Individual HSA and FSA plan administrators may interpret eligibility differently, particularly for weight-management prescriptions. Your employer’s FSA plan may have specific documentation requirements, deadlines, or runout periods. Always confirm with your administrator if you’re unsure about a specific expense.

Still not sure which GLP-1 program is right for you?

Take our free 60-second matching quiz. We’ll ask about your insurance, diagnosis, and budget — then show you the providers that fit, including which ones accept HSA/FSA at checkout.

Take the Free GLP-1 Matching Quiz →Check Ro eligibility — free, 2 minutes → (sponsored affiliate link, opens in a new tab)Related guides

- GLP-1 copay assistance programs 2026 — every savings card, PAP, and Medicare Bridge option

- Cheapest GLP-1 options without insurance — full pricing breakdown

- Best GLP-1 telehealth providers compared for 2026

- Orforglipron vs Ozempic — side-by-side comparison

- Does TRICARE cover GLP-1? 2026 guide

- Best Wegovy providers that accept insurance in 2026

Pricing verified against NovoCare.com and official Ozempic savings terms. IRS rules verified against Publication 502 (2025) and IRS FAQ on medical expenses. This page is not tax advice. Individual HSA and FSA plan administrators may interpret eligibility differently — always confirm with your administrator before assuming a specific expense qualifies. Published by The RX Index, a pricing intelligence and comparison resource for GLP-1 telehealth providers.

Your situation changes the answer

Find My GLP-1 Path

The right GLP-1 provider isn't the same for everyone. It depends on your state, your insurance and formulary, whether you want an FDA-approved or compounded medication, your preferred route (injection or oral), and your budget. Because a general answer can't resolve those for you, use The RX Index's Find My GLP-1 Path tool to get a personalized provider match with source-verified pricing before you choose.

- What it asks: your state, insurance situation, medication preference, budget, and support needs

- What you get: a personalized shortlist of GLP-1 providers matched to your situation, with verified pricing and the right questions to ask

- Cost: free · about 2 minutes · no signup