Wegovy HSA/FSA Guide · Verified April 16, 2026

Is Wegovy HSA/FSA Eligible? Yes — And Why “Eligible” Isn’t the Whole Answer (2026)

Published: · Last updated:

Is Wegovy HSA/FSA eligible? Yes. When a licensed physician prescribes Wegovy® to treat a diagnosed medical condition — obesity (BMI 30+), overweight (BMI 27+) with a weight-related comorbidity like type 2 diabetes or hypertension, or established cardiovascular disease with obesity/overweight — it’s a qualified medical expense under IRS Publication 502. That’s the legal answer in one sentence. The longer answer — the one that actually keeps your claim from getting denied — is below.

Here’s the trap: you confirm the IRS rule, walk confidently into checkout, and your card declines. Or it clears, and two weeks later your FSA admin emails asking for an itemized receipt and a Letter of Medical Necessity you’ve never heard of. Eligibility is the legal question. Checkout acceptance is the operational one. They break differently at every provider — and the difference can mean paying $221 a month instead of $349.

So we’ll answer both. Below: the IRS rule with the actual citation, a verified matrix of how ten different Wegovy payment paths handle HSA/FSA cards right now, the tax-bracket math on what you’ll actually save, a Letter of Medical Necessity template you can bring to your doctor, and the one move that stacks HSA/FSA savings on top of the Wegovy Savings Card.

The fastest path the verified evidence supports

- Cleanest brand-name direct HSA/FSA path: NovoCare® Pharmacy (manufacturer-direct).

- Best telehealth + direct HSA/FSA card path: SHED.

- Best insurance / prior-authorization path: Ro.

- Best reimbursement-first path: Hims / Hers (sponsored affiliate link, opens in a new tab).

SHED and Ro are affiliate links — full disclosure below. NovoCare is the manufacturer-direct path and is not an affiliate.

What we actually verified for this page (April 16, 2026)

- IRS Publication 502 (2025) — “Weight-Loss Program” section and prescription-medicine rules

- IRS Topic No. 502 and the IRS FAQs on nutrition, wellness, and general health (A8 and A9)

- IRS Publication 969 (2025) — Health Savings Accounts and Other Tax-Favored Health Plans

- Wegovy® Prescribing Information (2026) — current FDA-approved indications for the pen, pill, and HD formulations

- NovoCare® Pharmacy pricing and payment pages — pen, pill, and HD self-pay tiers; FSA/HSA card acceptance

- Wegovy® Savings Offer 2026 terms — “as low as $25/month” language and government-beneficiary exclusions

- CMS Medicare GLP-1 Bridge announcement — July 1, 2026 start date

- Medi-Cal Rx GLP-1 policy document — California weight-management coverage changes and exceptions

- Each provider’s own HSA/FSA policy page in the comparison matrix on the verification date

Methodology: we translate each provider’s stated policy into its practical meaning and flag where the stated language is softer than the hero claim. If you find a discrepancy between what’s here and what you see at a provider’s checkout, trust the provider’s site and let us know. Provider policies and promotional pricing change. We re-verify this page monthly.

Is Wegovy HSA/FSA eligible under IRS rules? Yes — here’s the exact citation

Answer capsule: Wegovy is HSA- and FSA-eligible when a licensed physician prescribes it to treat a specific diagnosed medical condition — obesity, overweight with at least one weight-related comorbidity (such as type 2 diabetes or hypertension), or established cardiovascular disease with obesity/overweight. The authority is IRS Publication 502 and Section 213(d) of the Internal Revenue Code, which treat prescription medications and weight-loss treatment for diagnosed disease as qualified medical expenses.

IRS Publication 502 — the publication that tells you what counts as a medical expense for tax purposes — says you can include amounts paid to lose weight when the weight loss is treatment for a specific disease diagnosed by a physician, naming obesity, hypertension, and heart disease as examples. Prescription medicines get the same qualified-expense treatment. Wegovy is a prescription medicine. Obesity is a physician-diagnosed disease. The two rules line up cleanly.

The IRS reinforced this in its FAQs on medical expenses related to nutrition, wellness, and general health. Question A9 of those FAQs says a weight-loss program counts as a medical expense only when the program treats a specific disease diagnosed by a physician. That language is narrower than it sounds, and it’s why the exact words on your chart matter more than the exact words on your prescription.

What makes Wegovy’s case cleaner than most weight-loss drugs

Three things help:

- Wegovy is FDA-approved for chronic weight management in adults with a BMI of 30+ or a BMI of 27+ with at least one weight-related comorbidity. The FDA-approved indication is itself a medical-necessity signal.

- Wegovy also carries a cardiovascular indication — reducing the risk of major cardiovascular events in adults with established heart disease and either obesity or overweight. If your prescription names the CV indication, your documentation gets even simpler because cardiovascular disease is explicitly named in Publication 502.

- It’s a branded prescription drug dispensed by a licensed pharmacy with an itemized receipt. That’s the paper trail your plan administrator wants to see.

A detail worth knowing: type 2 diabetes and hypertension aren’t standalone Wegovy indications — they’re qualifying comorbidities when paired with overweight (BMI 27+). This matters because your prescriber should document the weight-related diagnosis (like obesity) alongside any comorbidity, not just the comorbidity by itself.

The four scenarios that get Wegovy HSA/FSA claims denied

- A prescription written without a diagnosis in your chart. Some aesthetic or wellness clinics prescribe GLP-1s for “weight management” without documenting an ICD-10-coded diagnosis. The prescription is legal. It will not survive HSA/FSA scrutiny.

- A prescription framed as cosmetic — “for appearance,” “for general health,” “for wellness.” IRS language is explicit: appearance and general health don’t qualify.

- An LPFSA (Limited Purpose FSA). These are typically restricted to dental and vision by plan design.

- Certain HRAs where your employer has carved out weight-loss drugs. HRAs are plan-specific — check your Summary Plan Description.

Source: IRS Publication 502 (2025); IRS Topic No. 502; IRS FAQs on medical expenses related to nutrition, wellness, and general health, questions A8 and A9. Links in the sources section at the bottom.

If you don’t have a Wegovy prescription yet: you need a licensed provider who will document the diagnosis in your chart, not just write the script. The providers in the matrix below show diagnosis-linked prescribing as part of their intake flow.

→ See which providers write diagnosis-coded Wegovy prescriptions

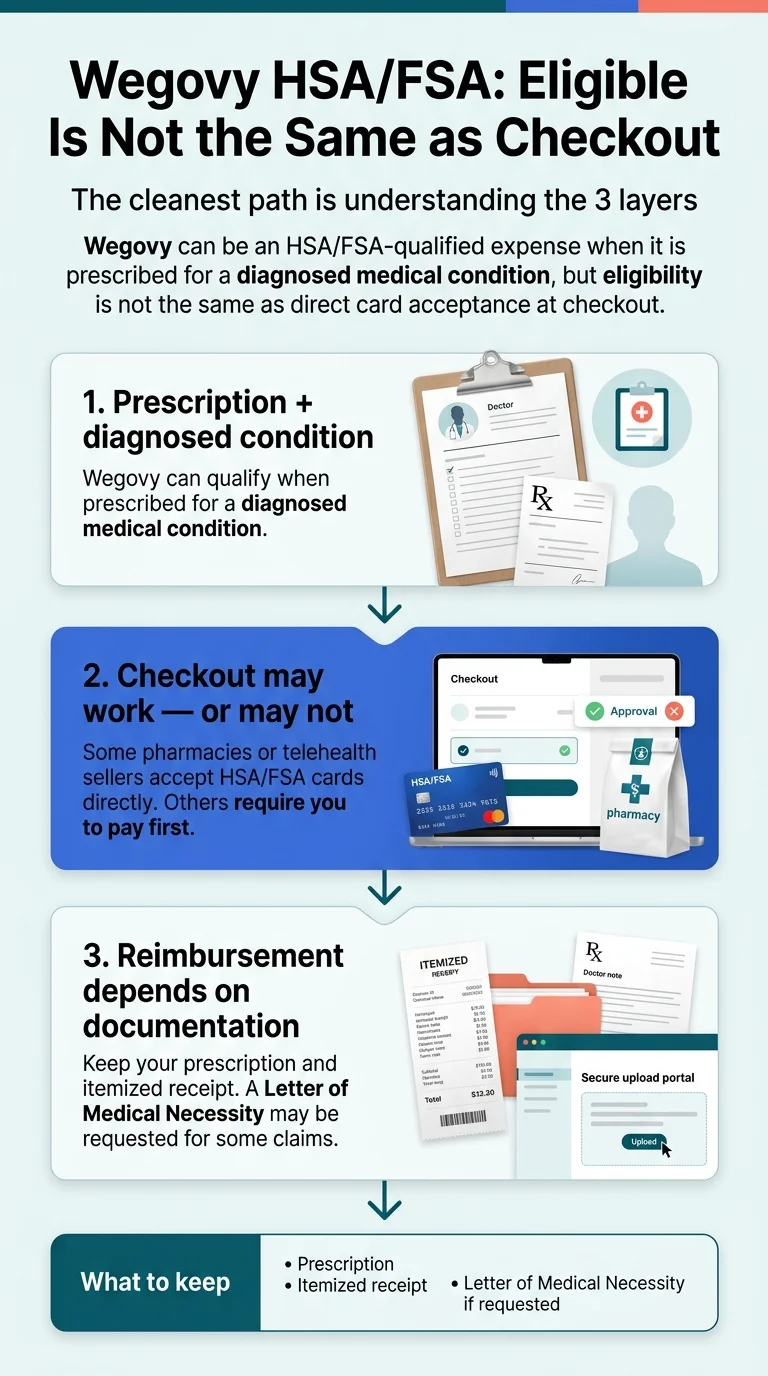

Eligible ≠ your card works: the three-layer reality nobody explains

Answer capsule: There are three separate questions behind “can I use HSA/FSA for Wegovy,” and they have different answers. (1) Is it IRS-eligible? Usually yes, with a proper prescription. (2) Will the provider’s checkout system accept your HSA/FSA card directly? Sometimes — it depends on the seller. (3) Can you pay with a regular card and get reimbursed later? Almost always yes, with documentation. Most Wegovy HSA/FSA confusion lives in the gap between layers 2 and 3.

This is the section that wins the search. Let’s unpack it.

Layer 1 — IRS eligibility. The legal question, covered above. If your prescription treats a diagnosed condition, Wegovy is a qualified medical expense under federal tax rules. This layer doesn’t care where you buy it.

Layer 2 — Card accepted at checkout. The operational question. Not every pharmacy or telehealth site is set up to process HSA/FSA cards the way CVS is. Some mainstream pharmacies and telehealth platforms are. Some explicitly aren’t. Layer 2 is about the merchant — their payment processor, their merchant category code, and whether your card issuer recognizes them as a qualified medical expense vendor.

Layer 3 — Reimbursement with documentation. The fallback. If your card doesn’t work at checkout, you pay with a personal card, keep your receipt and prescription, and submit to your plan administrator. Money gets pulled from your HSA/FSA and returned to you (or paid tax-free from the HSA). Reimbursement almost always works for Wegovy when the underlying expense is eligible. The friction is paperwork, not denial.

Why this matters for your next move

If your top priority is “just swipe and done,” you want a Layer 2 provider — direct card acceptance. That narrows your list fast.

If your top priority is insurance help or the lowest possible monthly cost, you might accept Layer 3 because the provider who does the insurance heavy-lifting often doesn’t accept HSA/FSA cards natively — but they’ll get your net cost lower.

If your priority is a licensed doctor writing a diagnosis-anchored prescription properly, either layer is fine. The documentation is the work product, not the checkout method.

Here’s how those three layers break across the ten most-searched Wegovy pathways in 2026.

The Wegovy HSA/FSA payment path matrix — verified April 2026

Answer capsule: The matrix below shows how ten Wegovy payment paths actually handle HSA/FSA cards as of April 16, 2026 — what each policy says, what that means in plain language, and current published pricing. We assembled this from primary-source pages (manufacturer terms, telehealth policy pages, provider FAQs) on the verification date above. Re-verify at checkout before you pay.

| Path | What their policy says | What that means in practice | Current published price | Best for |

|---|---|---|---|---|

| NovoCare® Pharmacy (manufacturer direct) | NovoCare’s payment page lists FSA/HSA cards among accepted payment methods alongside credit card, Apple Pay, and Google Pay. | Strongest Layer-2 proof in the brand-name world. Card works at checkout; receipt is manufacturer-issued and clean. | Pen: $199/mo new-patient intro on 0.25/0.5mg (through December 31, 2026) → $349/mo standard. Wegovy HD 7.2mg pen: $399/mo. Pill: $149/mo on 1.5mg and 4mg starter (through Aug 31, 2026) → $299/mo on 9mg and 25mg. | Self-pay readers who want manufacturer-direct brand Wegovy with direct HSA/FSA checkout. |

| Wegovy® Savings Card + commercial insurance at a retail pharmacy | Novo’s official savings page says your copay “could be as little as $25/month” with commercial insurance (max $100 savings/mo); HSA/FSA pays the residual at the register. | Best if you have commercial insurance that covers Wegovy. Savings card is not usable with Medicare, Medicaid, TRICARE, or any government plan. | As little as $25/mo after the savings card is applied, subject to savings-cap terms. | Commercially insured patients whose plan covers Wegovy. |

| SHED (telehealth + pharmacy fulfillment) | SHED’s help center says it accepts HSA and FSA cards at checkout for prescription purchases, and provides itemized receipts if you use a personal card. | Strongest Layer-2 telehealth option in our verified set. Direct-card acceptance advertised explicitly. | Per SHED’s current Wegovy product page: starts at $149/mo for the Wegovy pill and $199/mo for the pen, plus a $99/mo SHED membership and provider fee. Verify at checkout. | Readers who want direct HSA/FSA card checkout + telehealth convenience. |

| Embody (compounded semaglutide alternative — not Wegovy) | Embody advertises HSA/FSA eligibility across its programs and provides itemized receipts; confirm with your plan. This is a compounded path, not branded Wegovy. | Cash-pay compounded option for readers who can’t get branded Wegovy. Compounded semaglutide is a different product than Wegovy and is not FDA-approved. Confirm HSA/FSA acceptance at checkout, and check availability in your state during intake. | Compounded semaglutide injection from $99 first month, then $299/mo; needle-free GLP-1 gum from $149 first month, then $349/mo. Compounded tirzepatide options also available. | Cash-pay readers exploring a compounded semaglutide alternative — not readers who need branded Wegovy specifically. |

| Hers / Hims | Reimbursement-first: Hims notes that paying with an FSA/HSA card may require additional steps, and both brands publish clear reimbursement instructions with receipt downloads. | Best reimbursement-first path. Not an absolute “never” for direct card use, but their official positioning is pay-with-a-personal-card, then submit for reimbursement. | Pricing varies by program and medication form; confirm current Wegovy-specific all-in monthly pricing at checkout. | Readers comfortable with reimbursement paperwork. |

| Ro (ro.co) | Per Ro’s FAQ, Ro does not accept HSA/FSA cards at checkout; reimbursement is possible by saving your itemized receipt and submitting to your plan. | Layer-3 only — but the strongest insurance and prior-authorization support of any telehealth Wegovy path. (See damaging-admission pivot below.) | Ro Body program: $39 first month, then $149/month — as low as $74/month with annual plan paid upfront. Medication billed separately via insurance or via the Novo/Lilly savings programs. Ro carries Zepbound® (tirzepatide) and Foundayo™ (orforglipron) among FDA-approved GLP-1 options. | Readers who want help working their insurance or appealing prior authorization. |

| Sesame Care | Sesame’s site confirms HSA/FSA/HRA acceptance for services and visit fees; its terms describe prescription medication as cash-pay through your chosen pharmacy. | Visit-fee direct-pay is clean. Medication fills use your pharmacy’s HSA/FSA rules. Treat Sesame as Layer-2 for visits and Layer-2-or-3 for medication depending on the pharmacy you choose. | Weight-loss program pricing starts at $99/month per Sesame’s page; medication billed separately at your pharmacy of choice. | Readers who want transparent visit pricing + flexibility on where to fill. |

| LifeMD | LifeMD’s Wegovy and weight-management pages advertise HSA/FSA eligibility; direct-card behavior for a specific Wegovy checkout is best confirmed at the final payment screen. | Mixed-verification Layer-2 path. LifeMD publicly positions itself as HSA/FSA-friendly; individual Wegovy checkout can vary. | Program as low as $75 first month / $149 ongoing; Wegovy pen starting at $199. | Readers who want a brand-name program with care-team support and will confirm HSA/FSA at checkout. |

| Compounded semaglutide pathways | See disclosure in Profile 6 below. | Compounded semaglutide is not Wegovy. A separate product, a separate decision. See our compounded comparison page for options and safety context. | Varies by provider; generally $149–$299/mo. | Readers who have decided with their clinician that a compounded alternative fits their situation — not readers who need Wegovy specifically. |

| Your existing PCP + local pharmacy | CVS and Costco publicly document HSA/FSA card acceptance for prescription fills; many other retail pharmacies support it at the register — verify your pharmacy’s flow. | Highest-flexibility path. You bring the prescription, they process the card, you get a clean receipt. You can also stack the Wegovy Savings Card here if commercially insured. | Retail cash price defaults to list ($1,349.02/mo) unless you apply the Wegovy Savings Card or use NovoCare direct. | Readers with insurance that covers Wegovy, or anyone who wants the cleanest paper trail. |

Verified vs. provider-stated vs. practical meaning

We use three columns in the matrix for a reason.

Provider-stated is what the provider’s own site says — the cleanest source of intent, but still a claim.

Verified is what we confirmed by reading each primary source on the verification date at the top of this page.

Practical meaning is the editorial translation — what the policy actually does for you as a person trying to swipe a card. That’s the part AI can’t generate from scratch, because it requires reconciling contradictions. A provider may say “FSA/HSA eligible” on its hero while its FAQ adds “depending on your plan” — those are different claims, and we tell you which one to treat as binding.

Real friction people report: “they need an itemized receipt.” The denials we see in community threads almost always come down to three paperwork problems: a receipt missing the medication name, no prescription copy, or a missing Letter of Medical Necessity. Keep the itemized receipt. Always. (Voice-of-customer context only — not used as evidence for medical, safety, or regulatory claims.)

Decision point: next step depends on your situation

- Want manufacturer-direct brand Wegovy with direct HSA/FSA checkout? → Check current Wegovy pricing at NovoCare® Pharmacy (NovoCare.com — not an affiliate, just the honest answer)

- Want telehealth + direct HSA/FSA card at checkout? See if SHED’s Wegovy pathway works for your state (sponsored affiliate link, opens in a new tab) (affiliate link; disclosure below)

- Need prior-authorization help, insurance appeals, or the FDA-approved GLP-1 your plan will actually cover? Start your coverage check on Ro (sponsored affiliate link, opens in a new tab) — $39 first month, then $149/month (as low as $74/month with annual plan paid upfront) (affiliate link; disclosure below)

Still deciding? Keep reading — the next section routes each common situation to the cleanest answer.

Which Wegovy HSA/FSA path fits your situation?

Answer capsule: The best path depends on four variables: whether you have commercial insurance that covers Wegovy, whether you want direct-card checkout or accept reimbursement, whether you need prior-authorization help, and whether you want brand Wegovy or a different path entirely. Most readers fit one of six profiles.

Profile 1: You have commercial insurance that covers Wegovy

Winning path: Wegovy® Savings Card + your insurance + HSA/FSA for the residual.

This is the lowest-cost scenario, and most people don’t realize it stacks. The order: (1) enroll in the Wegovy Savings Card (text SAVE to 83757 or enroll at NovoCare.com), (2) fill at your usual pharmacy, (3) insurance processes the claim, (4) the savings card pays down most of your copay, and (5) you pay the residual with your HSA/FSA card at the register. Commercially insured patients commonly land at the “as little as $25/month” tier Novo advertises — and even that $25 can be drawn pre-tax from your HSA/FSA, because HSA/FSA applies to your remaining out-of-pocket amount, not the manufacturer-paid portion.

The Wegovy Savings Card is not usable with Medicare, Medicaid, TRICARE, VA, or any government-funded plan. If that’s you, skip to Profile 5.

Next step: Enroll in the Wegovy Savings Card at NovoCare.com (direct link to the manufacturer — not an affiliate, it’s the correct starting point).

Profile 2: You’re self-paying and want the cleanest brand path with direct HSA/FSA checkout

Winning path: NovoCare® Pharmacy direct.

NovoCare sells injectable Wegovy and oral Wegovy pills directly from Novo Nordisk. Per NovoCare’s payment page, accepted methods include FSA/HSA cards. You need a Wegovy prescription from a licensed prescriber (NovoCare is a pharmacy, not a telehealth service — they don’t write scripts), but once you have one, this is the clearest Layer-2 checkout for brand Wegovy at cash-pay tiers.

NovoCare pricing as of April 2026:

- Wegovy pen new-patient intro: $199/mo for 0.25mg and 0.5mg through December 31, 2026

- Wegovy pen standard: $349/mo for most doses after the intro

- Wegovy HD 7.2mg pen: $399/mo

- Wegovy pill starter: $149/mo for 1.5mg and 4mg through August 31, 2026

- Wegovy pill maintenance: $299/mo for 9mg and 25mg doses

With HSA/FSA, that $349/mo pen’s effective cost lands around $221/mo at a 24% federal bracket for payroll-funded contributions. Full math below.

Next step: If you don’t have a prescription yet, your own doctor can send the script to NovoCare. Or use one of the telehealth providers below, most of whom can forward a prescription to NovoCare on your behalf.

Profile 3: You want telehealth convenience + direct HSA/FSA card at checkout

Winning path: SHED.

SHED is our pick for this use case because its help center explicitly says HSA and FSA cards are accepted at checkout for prescription purchases. Among telehealth-first GLP-1 platforms, that’s the strongest Layer-2 language we verified.

Per SHED’s current Wegovy product page, pricing starts at $149/month for the Wegovy pill and $199/month for the pen, plus a $99/month SHED membership and provider fee. You get a licensed provider evaluation, a diagnosis-linked prescription, and direct HSA/FSA card acceptance in one flow.

Decision point

If direct HSA/FSA card checkout is what you came here for, SHED is the answer.

See if SHED’s Wegovy pathway works for your state and plan → (sponsored affiliate link, opens in a new tab)Affiliate link — full disclosure below.

Profile 4: You need help with insurance, prior authorization, or coverage appeals

Winning path: Ro.

Honest read on Ro, stated up front:

Ro does NOT accept HSA/FSA cards at checkout. Their FAQ is explicit. If direct-card checkout is your top priority, Ro is not your path — go back to Profile 2 (NovoCare) or Profile 3 (SHED). We just covered both.

Here’s the pivot: because Ro skips the direct-card-checkout complication, they specialize in the thing most telehealth platforms won’t touch — handling your insurance, writing the prior-authorization appeal, and routing you to whichever FDA-approved GLP-1 your plan will actually pay for. Ro carries Zepbound® (tirzepatide), Foundayo™ (orforglipron), and Wegovy coverage support, and they run a coverage check as part of intake. If your plan covers any of these medications, your real cost can drop to a $0–$50/month copay — dramatically better than any self-pay path — and you can still reimburse that copay from your HSA/FSA by submitting the receipt.

Ro’s pricing: $39 first month, then $149/month — as low as $74/month with annual plan paid upfront. Medication is billed separately via insurance or the manufacturer savings programs.

Decision point

If working the insurance angle is your biggest-dollar opportunity — and for anyone whose plan might cover Wegovy, Zepbound, or Foundayo, it is — Ro is the path.

Start your coverage check on Ro → (sponsored affiliate link, opens in a new tab)Affiliate link — full disclosure below. Or read our prior-authorization providers comparison first.

Profile 5: You’re on Medicare, Medicaid, TRICARE, or another government plan

Winning path: Varies by program — and 2026 changes are material. Read this before you commit.

Medicare (important 2026 update): Per CMS, the Medicare GLP-1 Bridge launches July 1, 2026. Eligible Medicare Part D beneficiaries will be able to access all formulations of Wegovy, Foundayo, and the Zepbound KwikPen through the Bridge at a $50 copay. Wegovy’s existing Part D pathway for the cardiovascular indication continues through normal Part D coverage. If you’re on Medicare and have been paying cash for Wegovy, wait until July 1 to check Bridge eligibility — it may dramatically change your math.

You cannot contribute new money to an HSA while enrolled in Medicare, but existing HSA funds can still pay for Wegovy when it’s prescribed for a qualifying condition. You are not eligible for the Wegovy Savings Card.

Medicaid: State-dependent and shifting fast. California Medi-Cal ended weight-management coverage for Wegovy and Zepbound as of January 1, 2026. Per Medi-Cal Rx documents, Wegovy for MASH may be covered starting April 1, 2026 without prior authorization when the correct diagnosis code is submitted, and Wegovy’s other FDA-approved indications (including the cardiovascular indication) can still be considered with prior authorization. Your state’s Medicaid formulary is the authoritative source. You are not eligible for the Wegovy Savings Card.

TRICARE / VA: TRICARE formulary and VA pharmacy rules apply. The Wegovy Savings Card excludes TRICARE and VA beneficiaries. Work with your military pharmacy benefits coordinator on the coverage pathway.

If your Medicare or Medicaid coverage for Wegovy recently changed, you’re in disruption mode. → See our Wegovy insurance coverage guide for your next move.

Profile 6: You want the cheapest legal path and you’re open to a non-Wegovy alternative

Required context before you read further. Compounded semaglutide is not Wegovy. Compounded semaglutide is not FDA-approved, which means FDA has not verified its safety, effectiveness, or quality before it reaches patients. FDA has issued alerts about dosing errors, adverse events including hospitalizations, and the use of unapproved salt forms in some compounded GLP-1 products. HSA/FSA rules still require a prescription for a diagnosed medical condition. If the brand-name Wegovy indication is what you came here for, this is a different decision and you should make it with your clinician.

For readers who have decided a compounded path is appropriate for their situation, compounded semaglutide from a licensed telehealth provider typically runs $149–$299/month, and many providers advertise HSA/FSA eligibility. The provider you choose matters more here than at any other point on this page — regulatory actions, quality systems, and state licensing differ.

→ See our compounded GLP-1 alternatives guide for a current, verified breakdown of compounded providers with the regulatory context you need before you commit.

If you came here specifically for Wegovy, skip this profile and use Profiles 1–4.

How much HSA/FSA actually saves you on Wegovy (the real math)

Answer capsule: HSA and FSA dollars are generally pre-tax. For most working adults with employer-sponsored plans, that’s roughly 22–37% effective savings on whatever out-of-pocket cost remains. On NovoCare’s $349/month pen, that’s roughly $128/month saved at a 24% federal bracket. On the $1,349/month retail list price, it’s over $480/month saved at the same bracket.

Two things to understand before you lean on the numbers:

First, how the contribution was made matters. FSA contributions and HSA contributions made through employer payroll (cafeteria plan) avoid federal income tax, FICA (7.65%), and most state income taxes. HSA contributions made outside of payroll — on your own, via direct deposit or rollover — avoid federal and state income tax but not FICA, because FICA was already taken out of your paycheck before the money hit your bank. If you’re funding your HSA through payroll, the full savings apply. If you’re funding it yourself, knock about 7.65% off the savings estimate.

Second, HSA/FSA stacks with other programs. You can use the Wegovy Savings Card to reduce a copay and pay the residual with HSA/FSA. You can use NovoCare direct pricing and swipe your HSA card for the $349 or $199. Your pre-tax advantage compounds on top of whichever base price you land on — it applies to what you actually pay out of pocket.

Effective monthly cost after HSA/FSA by tax bracket (payroll-funded, illustrative)

Assumes federal bracket + 7.65% FICA + 5% representative state income tax. Not tax advice — illustrative. Your actual savings depend on your filing status, state of residence, and whether your HSA contribution is payroll-deducted.

| Your Wegovy price | 22% bracket → ~34.65% savings | 24% bracket → ~36.65% savings | 32% bracket → ~44.65% savings |

|---|---|---|---|

| $25/mo (insured + savings card residual) | $16.34 | $15.84 | $13.84 |

| $149/mo (NovoCare Wegovy pill starter) | $97.36 | $94.38 | $82.47 |

| $199/mo (Wegovy pen new-patient intro) | $130.04 | $126.06 | $110.16 |

| $299/mo (Wegovy pill maintenance) | $195.36 | $189.39 | $165.49 |

| $349/mo (Wegovy pen standard) | $228.05 | $221.08 | $193.18 |

| $399/mo (Wegovy HD 7.2mg pen) | $260.72 | $252.78 | $220.87 |

| $1,349/mo (retail list price) | $881.44 | $854.55 | $746.68 |

Why this matters over 12 months

Staying on the standard Wegovy pen at $349/month for a year is $4,188 of spend. At a 24% bracket with payroll-funded HSA/FSA, your effective annual cost drops to roughly $2,653 — a $1,535 real-dollar savings. That’s an emergency fund bump, a family vacation, or the first meaningful dent in credit-card debt.

The long-game HSA move worth knowing

If you have a high-deductible health plan and an HSA, you have a quietly powerful third option: pay for Wegovy out of pocket today, save the receipts, and reimburse yourself from the HSA years later. The IRS does not require you to reimburse in the same year the expense occurred — you can reimburse yourself any time, as long as the expense was incurred after the HSA was established and wasn’t reimbursed or deducted another way, and you keep records to substantiate it. Your HSA keeps growing (invested, if you want), and you pull the tax-free reimbursement out on your own timeline.

This isn’t for everyone — it requires enough non-HSA cash to cover Wegovy month-to-month. But when it fits, it’s the strongest tax-advantaged move available. A tax professional can confirm whether your plan setup supports it.

Decision point after the math

- Insured and just ran the numbers? → Enroll in the Wegovy Savings Card at NovoCare.com and take it to your pharmacy. That’s the lowest-cost path we can point you to.

- Paying cash? NovoCare direct is $199–$349/mo before HSA savings. SHED is $248–$298/mo all-in after its $99 membership/provider fee, before HSA savings. Both accept HSA/FSA at checkout. → See if SHED’s Wegovy pathway works for your state (sponsored affiliate link, opens in a new tab) (affiliate)

- Insurance still in play? → Start your Ro coverage check (sponsored affiliate link, opens in a new tab) — they’ll tell you within intake whether your plan covers Wegovy, Zepbound, or Foundayo. (affiliate)

The Letter of Medical Necessity — when you need it and what goes in it

Answer capsule: A Letter of Medical Necessity (LMN or LOMN) is a short document from your prescriber explaining why Wegovy is medically necessary for a specific diagnosed condition. HSA administrators don’t usually require one at the register, but they may request one in an audit. FSA administrators often require one for reimbursement, especially for weight-management expenses. Ask your prescriber for it at the time the prescription is written — it takes minutes at the visit and saves weeks of back-and-forth later.

When you actually need one for Wegovy

You need an LMN (or should have one on file) in these situations:

- You’re using an FSA and the administrator is flagging the Wegovy claim.

- You’re reimbursing yourself from an HSA and want audit-proof documentation.

- The expense is bundled with a telehealth program fee, coaching, or membership.

- Your prescription doesn’t explicitly state the diagnosis on the face of the script.

- The pharmacy receipt doesn’t link back to a diagnosis code.

The six required elements of a Wegovy LMN

Missing any one of these is the most common reason LMNs get rejected:

- Patient identifiers: full name, date of birth, address.

- Diagnosis + ICD-10 code. Common qualifying codes:

ICD-10 code Diagnosis E66.9 Obesity, unspecified E66.01 Morbid (severe) obesity due to excess calories E11.9 Type 2 diabetes mellitus without complications (as a comorbidity) I10 Essential (primary) hypertension (as a comorbidity) E78.5 Hyperlipidemia (as a comorbidity) G47.33 Obstructive sleep apnea (as a comorbidity) I25.10 Atherosclerotic heart disease (supporting the CV indication) - Statement of medical necessity: a plain sentence saying Wegovy is medically necessary to treat the named condition and is not prescribed for cosmetic or general-wellness purposes.

- Treatment details: prescribed dose, titration schedule, and anticipated duration.

- Prescriber credentials: full name, NPI number, signature, date, and letterhead.

- Contact information so your administrator can follow up.

Which diagnoses clear cleanly vs. which get scrutinized

Clear cleanly: obesity (E66.9 or E66.01); overweight (BMI 27+) with a documented comorbidity — hypertension, type 2 diabetes, hyperlipidemia, sleep apnea, or cardiovascular disease; established cardiovascular disease with obesity/overweight (the CV indication).

Scrutinized but often approved with strong documentation: PCOS with insulin resistance; prediabetes; binge eating disorder.

Likely denied: “cosmetic,” “aesthetic,” “general wellness,” “preventive weight loss,” or any script without a specific coded diagnosis.

Step-by-step: how to actually pay for Wegovy with HSA or FSA

Answer capsule: Five steps between “I want to use HSA/FSA for Wegovy” and “my claim is processed and audit-proof.” (1) Get a diagnosis-linked prescription. (2) Choose a Layer-2 direct-card path or accept Layer-3 reimbursement. (3) Fill the prescription. (4) Save the right receipts. (5) Request or attach a Letter of Medical Necessity if your plan asks. Do all five and the path is smooth.

Step 1: Confirm a diagnosis-linked prescription is in your chart

Before you pay for anything, your prescriber needs to have documented your diagnosis (ICD-10 coded) in your medical chart and written the Wegovy prescription to treat it. If you’re using a telehealth platform, this happens during intake — but confirm that the platform will issue a properly coded prescription.

Step 2: Choose your payment path

Use the profiles above. Direct-card first? NovoCare or SHED. Insurance coverage first? Ro. Fine with reimbursement paperwork? Hims/Hers. On a government plan? Retail pharmacy + your own doctor, and watch the July 2026 Medicare Bridge if you’re on Part D.

Step 3: Fill the prescription

Direct-card checkout: present your HSA/FSA debit card at the pharmacy or at the provider’s online checkout. Reimbursement: pay with a personal card and save everything.

Step 4: Save the audit-proof paper trail

For Wegovy, keep:

- A copy of the prescription showing medication name, dose, and prescriber details.

- The itemized pharmacy receipt — medication name, date, patient name, amount paid. A plain credit card slip is not enough.

- A copy of the Letter of Medical Necessity if you used one.

- The explanation of benefits (EOB) from your insurance if insurance was involved.

- A simple spreadsheet or PDF tying each receipt to the HSA/FSA transaction date.

Most tax professionals recommend keeping these for several years in case of an audit. HSA records in particular should be kept as long as the underlying reimbursement remains open.

Step 5: Submit reimbursement (if Layer-3) — or keep your records and move on (if Layer-2)

Paid with your HSA or FSA card directly? Keep the paperwork for the audit trail. You’re done.

Paid with a personal card? Submit the claim through your administrator’s portal with the receipt and any documentation they require. Processing times vary by administrator.

What to do if your HSA/FSA card declines or your claim gets denied

Answer capsule: A declined card is almost never a signal that Wegovy is ineligible — it’s usually a merchant processing issue or a documentation gap. A denied reimbursement claim is usually fixable with an appeal that includes an itemized receipt, a copy of the prescription, and a Letter of Medical Necessity.

The three reasons Wegovy HSA/FSA claims actually get denied

Reason 1: The receipt isn’t itemized. A credit card slip showing the amount paid isn’t enough. Administrators want to see the medication name, date of service, patient name, and amount. Most pharmacies will print a separate itemized receipt on request, and most allow re-download from the patient portal after the fact.

Reason 2: The prescription isn’t attached or the diagnosis isn’t on the document. Some FSA admins want to see the actual prescription. Some want the LMN. Some want both. Pull the prescription copy from your pharmacy portal and the LMN from your prescriber’s office. Attach both in the appeal.

Reason 3: The plan year ended. FSAs typically require claims within a grace period after the plan year closes — commonly 75 days into the next plan year, but check your plan document. HSAs don’t have this problem; reimbursements aren’t time-boxed.

The three-email appeal template

Email 1 — initial response. Subject: “Appeal for Claim [number] — Wegovy prescription for diagnosed obesity.” Attach: itemized pharmacy receipt, prescription copy, and LMN. Body: one paragraph — “My prescriber has diagnosed me with [condition, ICD-10 code] and prescribed Wegovy as medically necessary treatment. Attached is the itemized receipt, the prescription, and the Letter of Medical Necessity. Please reprocess this claim.”

Email 2 — if they ask for more. Respond within 48 hours. Provide exactly what they asked for, nothing more, nothing less.

Email 3 — escalation. Request supervisor review and reference IRS Publication 502’s language on weight-loss treatment for diagnosed disease.

When to call HR

If your FSA admin is refusing an appeal for a properly documented Wegovy claim, HR or your plan’s ombudsman is your next step. Plan administrators answer to the plan sponsor, which is usually your employer.

Are Wegovy pill, Wegovy pen, and Wegovy HD all HSA/FSA eligible?

Answer capsule: Yes — all three are HSA/FSA eligible under the same IRS rules when prescribed for a qualifying diagnosed condition. A detail worth knowing: the FDA-labeled indications aren’t identical across formulations. The injection label includes metabolic dysfunction–associated steatohepatitis (MASH) under accelerated approval alongside weight management and CV risk reduction; the tablet label covers chronic weight management and cardiovascular risk reduction. The form doesn’t change HSA/FSA eligibility; the diagnosis and the prescription do.

| Form | Dosing | FDA-labeled indications | NovoCare price |

|---|---|---|---|

| Wegovy pen (injectable semaglutide) | Once-weekly injection; 0.25mg – 2.4mg | Chronic weight management, CV risk reduction, MASH (accelerated approval) | $199/mo intro (0.25/0.5mg through Jun 30, 2026) → $349/mo standard |

| Wegovy pill (oral semaglutide) | Once-daily tablet; 1.5mg, 4mg, 9mg, 25mg | Chronic weight management; cardiovascular risk reduction | $149/mo (1.5mg/4mg starter through Aug 31, 2026) → $299/mo (9mg/25mg) |

| Wegovy HD (7.2mg high-dose pen) | Once-weekly injection at 7.2mg dose | For patients who titrate past 2.4mg | $399/mo per NovoCare |

The Wegovy pill is not Rybelsus®, which contains oral semaglutide but is FDA-approved for type 2 diabetes, not weight management.

Which form should you use HSA/FSA for? That’s a clinical question, not a tax one. Your prescriber decides based on your response to titration, GI tolerance, and your goals. All three are HSA/FSA eligible under the same rules.

Can HSA/FSA cover the telehealth visit, membership, labs, shipping, and coaching?

Answer capsule: Yes for the medical components, usually no for the wellness add-ons. The Wegovy medication itself, the telehealth visit fee, and required lab work are almost always HSA/FSA eligible. Bundled membership or program fees that include coaching, lifestyle content, or wellness features can be partially eligible and may require itemization to separate the medical and non-medical portions.

Almost always eligible:

- The Wegovy medication

- The prescribing provider’s consultation fee

- Lab work for safe prescribing (metabolic panel, A1c, etc.)

- Telehealth visit fees tied to medical evaluation and prescription

Partially or conditionally eligible:

- Membership or program fees — IRS Pub 502 covers weight-loss program fees when the program treats a specific physician-diagnosed disease. Ask the provider for an itemization that separates the medical portion (physician oversight, prescription management) from the wellness portion.

- Coaching or behavior-change content — usually not eligible unless directly tied to treating the diagnosed condition.

Shipping fees vary by plan and provider. Some providers (SHED, for example) note that shipping is eligible when properly receipted; some retail pharmacies (CVS among them) say in most cases FSA/HSA cards may not be used for delivery fees. Check your specific provider and plan.

Generally not eligible:

- Gym memberships (unless specifically prescribed for a diagnosed condition per Pub 502)

- Meal replacement products

- Wellness apps without a medical component

- Dietary supplements

- Late fees and program cancellation charges

If the invoice bundles everything into one line, ask for an itemized breakdown.

What real Wegovy HSA/FSA users run into (voice-of-customer friction)

Answer capsule: The three frustrations users post about most often in public forums are denied reimbursement claims due to non-itemized receipts, confusion between insurance and HSA/FSA workflows, and LMN requests that arrive weeks after the initial claim. None of these are dealbreakers — all three are preventable with the paper trail this page walks you through.

The Reddit and community conversation on Wegovy HSA/FSA is consistent: the IRS rules aren’t the problem. Paperwork and merchant processing are. Users who show up with a diagnosis-linked prescription, an itemized receipt, and an LMN on file report smooth approvals. Users who show up with a blank credit card slip report denials and appeals.

One pattern worth naming: people assume that because their FSA card works for ibuprofen at CVS, it will work for Wegovy online. Sometimes it does. Sometimes it doesn’t, because the merchant’s payment processor or the card issuer treats online prescription purchases differently. If direct card acceptance matters to you, use one of the verified Layer-2 paths above.

Voice-of-customer context only — not used as evidence for medical, safety, or regulatory claims.

Frequently Asked Questions

Is Wegovy HSA eligible?

Yes. Wegovy is HSA eligible when a licensed physician prescribes it to treat a diagnosed medical condition such as obesity, overweight with a weight-related comorbidity (like type 2 diabetes or hypertension), or established cardiovascular disease with obesity/overweight. HSAs generally don’t require a Letter of Medical Necessity at the register, but keeping receipts and documentation supports you if the IRS reviews your HSA withdrawals.

Is Wegovy FSA eligible?

Yes, under the same IRS rules. In practice, FSA administrators more frequently request a Letter of Medical Necessity or additional documentation before processing a Wegovy reimbursement. Having the LMN on file before you submit prevents most denials.

Can I use my HSA or FSA card at checkout for Wegovy?

Sometimes. Direct-card checkout is confirmed at NovoCare® Pharmacy (manufacturer direct) and at SHED. Retail pharmacies including CVS and Costco document HSA/FSA card acceptance for prescription fills; other retail chains support it at the register but verify your specific pharmacy’s flow. Some telehealth providers — including Ro — do not accept HSA/FSA cards at checkout and require reimbursement after purchase.

Do I need a Letter of Medical Necessity for Wegovy?

Not always. HSAs typically don’t require an LMN for Wegovy when the prescription is tied to a diagnosed condition. FSAs frequently require an LMN for weight-loss-related reimbursements. If you’ll be reimbursing from an FSA, get the LMN at the time the prescription is written.

Can I reimburse myself later if I paid with a regular credit card?

Yes, and this is the safest approach when direct-card checkout fails or isn’t offered. Pay with a personal card, save the itemized receipt and prescription copy, and submit to your HSA or FSA administrator for reimbursement. The IRS does not require HSA reimbursement in the same year the expense was incurred — you can reimburse yourself later, as long as the expense was incurred after your HSA was established, it wasn’t reimbursed or deducted elsewhere, and you keep records to substantiate it.

Can I use HSA/FSA for Wegovy without insurance?

Yes. HSA/FSA eligibility is based on the medical necessity of the prescription, not your insurance status. Self-pay patients using NovoCare Pharmacy, SHED, or similar direct-pay paths use HSA/FSA cards the same as insured patients.

Can HSA/FSA cover the telehealth visit, labs, and shipping for Wegovy?

Yes for the visit and labs — these are qualified medical expenses when part of diagnosing and treating a medical condition. Shipping eligibility varies by plan and provider. Coaching and wellness content inside bundled memberships may require itemization.

Can I use an LPFSA or DCFSA for Wegovy?

Usually not. LPFSAs (Limited Purpose FSAs) typically cover dental and vision by plan design. DCFSAs (Dependent Care FSAs) cover dependent care, not medical expenses. Wegovy is not eligible under most LPFSAs or any DCFSA.

What receipt do I need for reimbursement?

An itemized pharmacy receipt showing the medication name (“Wegovy”), the dispensing date, the patient name, and the amount paid. A credit card slip without these details is not enough for most administrators.

What should I do if my claim gets denied?

Ask the administrator specifically what’s missing. The fix is almost always (a) an itemized receipt instead of a credit card slip, (b) a copy of the prescription, or (c) a Letter of Medical Necessity. Attach what they asked for in a written appeal.

Can I stack the Wegovy Savings Card with my HSA/FSA?

Yes. If you have commercial insurance, enroll in the Wegovy Savings Card (text SAVE to 83757 or enroll at NovoCare.com). Your insurance adjudicates the claim, the savings card reduces your copay (as low as $25/month per Novo’s current terms, subject to savings caps), and you pay the residual with your HSA or FSA card. The savings card is not available to Medicare, Medicaid, TRICARE, or VA beneficiaries. HSA/FSA funds apply only to your remaining out-of-pocket amount, not to the portion the manufacturer pays.

Is compounded semaglutide HSA/FSA eligible?

Compounded semaglutide is not Wegovy and is not FDA-approved. FDA has issued alerts about dosing errors, adverse events including hospitalizations, and use of unapproved salt forms in some compounded GLP-1 products. HSA/FSA eligibility for compounded GLP-1s depends on whether the prescription is tied to a diagnosed medical condition and whether the medication is dispensed by a licensed pharmacy. Some administrators apply additional scrutiny to compounded prescriptions. If you came here for Wegovy specifically, compounded semaglutide is a different product and a different decision.

Is Wegovy covered by Medicare in 2026?

Medicare generally has not covered Wegovy for weight loss alone, but 2026 changes this. Per CMS, the Medicare GLP-1 Bridge starts July 1, 2026 — eligible Medicare Part D beneficiaries can access all formulations of Wegovy, Foundayo, and the Zepbound KwikPen through the Bridge at a $50 copay. Wegovy’s cardiovascular indication continues through the normal Part D coverage pathway. Medicare beneficiaries cannot use the Wegovy Savings Card and cannot contribute new money to an HSA while enrolled in Medicare, but can still spend existing HSA funds on Wegovy when it’s prescribed for a qualifying condition.

What happened with California Medi-Cal and Wegovy?

Per Medi-Cal Rx documents, California’s Medi-Cal ended weight-management coverage for Wegovy and Zepbound effective January 1, 2026. Wegovy for MASH may be covered starting April 1, 2026 without prior authorization when the correct diagnosis code is submitted. Other FDA-approved Wegovy indications (including cardiovascular risk reduction) can still be considered with prior authorization. Check your state’s Medicaid formulary for your specific situation.

Will my employer see that I’m using HSA/FSA for Wegovy?

Privacy depends on plan structure. Many FSAs are group health plans subject to HIPAA privacy protections, but not every FSA is (HHS notes that an FSA or cafeteria plan is a group health plan unless it has fewer than 50 participants and is self-administered). HSA transactions are between you and your HSA custodian and are generally not reported to your employer at the transaction level.

What we actually verified for this page

We checked every pricing, eligibility, and checkout claim against primary sources on April 16, 2026:

- IRS Publication 502 (2025), Medical and Dental Expenses — “Weight-Loss Program” section. irs.gov/publications/p502

- IRS Topic No. 502. irs.gov/taxtopics/tc502

- IRS FAQs on medical expenses related to nutrition, wellness, and general health (questions A8 and A9). irs.gov

- IRS Publication 969 (2025), Health Savings Accounts and Other Tax-Favored Health Plans. irs.gov/publications/p969

- Wegovy® Prescribing Information (2026) — current FDA-labeled indications for the injection and tablet. accessdata.fda.gov

- FDA compounding alerts — dosing errors and quality concerns with compounded GLP-1s. fda.gov/drugs/human-drug-compounding

- CMS Medicare GLP-1 Bridge announcement (July 1, 2026 start). cms.gov/medicare/coverage/prescription-drug-coverage/medicare-glp-1-bridge

- Medi-Cal Rx GLP-1 policy document — California weight-management changes and exceptions. medi-calrx.dhcs.ca.gov

- NovoCare® Pharmacy pricing and payment pages. novocare.com/pharmacy.html

- Wegovy® Savings Offer 2026 terms. novocare.com/patient/medicines/wegovy/savings-offer.html

- Embody program and pricing pages. joinem.co

- SHED HSA/FSA and Wegovy pages. shedweight.com

- Ro FAQ — cost, pricing, services. ro.co/faq/cost-pricing-services

- Hers FSA/HSA page. forhers.com/weight-loss/fsa-hsa

- Hims weight loss page. hims.com/weight-loss

- Sesame Care. sesamecare.com

- LifeMD Wegovy page. lifemd.com/drugs/w/wegovy

- CVS FSA/HSA information. cvs.com/content/fsa

- Secondary / supporting references: FSAstore and HSAstore eligibility pages.

Provider policies and promotional pricing change. We re-verify this page monthly. If you find a discrepancy between what’s here and what you see at a provider’s checkout today, trust the provider’s own site. Last verified: April 16, 2026. Next scheduled re-verification: May 16, 2026.

Still deciding which GLP-1 program is right for you?

We built a 60-second matching quiz that routes readers based on insurance status, HSA/FSA preference, medication type, and budget. No email gate. Just a personalized result page with the provider path that fits your situation and the exact next step to take.

Takes 60 seconds · Free · No signup

Disclosures & methodology

The RX Index is a pricing intelligence and comparison resource for GLP-1 telehealth providers. We do not provide medical care, legal advice, or tax advice. This page is informational. Your HSA/FSA plan administrator, your prescriber, and your tax professional are the authoritative sources for your specific situation.

Affiliate disclosure: We may receive compensation from some of the providers mentioned on this page if you click through and sign up. Our provider rankings are based on verified evidence and fit for the reader’s search intent — not compensation. For this specific page, the evidence supports NovoCare® Pharmacy (not an affiliate — linked because it’s the right answer) and SHED as the strongest direct-card paths; Ro as the strongest insurance/prior-auth path; Hims/Hers as the strongest reimbursement-first path. The verification sources above are linked so you can form your own view.

Editorial standards: No fabricated testimonials. No “medically reviewed by” labels without a real clinician reviewing the page. No invented credentials. Every material claim is either sourced or flagged for verification. See our full editorial standards.

What this page is not: This is not medical advice. Only a licensed healthcare provider can determine whether Wegovy is appropriate for you. This is not tax advice — your effective HSA/FSA tax savings depend on your specific situation, and a CPA or tax professional is the right source for individualized guidance.

Questions or corrections? The RX Index editorial team maintains this page and re-verifies it monthly. If a provider policy or price shifts, we update it here first.

Last verified: April 16, 2026. Next scheduled re-verification: May 16, 2026.

Your situation changes the answer

Find My GLP-1 Path

The right GLP-1 provider isn't the same for everyone. It depends on your state, your insurance and formulary, whether you want an FDA-approved or compounded medication, your preferred route (injection or oral), and your budget. Because a general answer can't resolve those for you, use The RX Index's Find My GLP-1 Path tool to get a personalized provider match with source-verified pricing before you choose.

- What it asks: your state, insurance situation, medication preference, budget, and support needs

- What you get: a personalized shortlist of GLP-1 providers matched to your situation, with verified pricing and the right questions to ask

- Cost: free · about 2 minutes · no signup