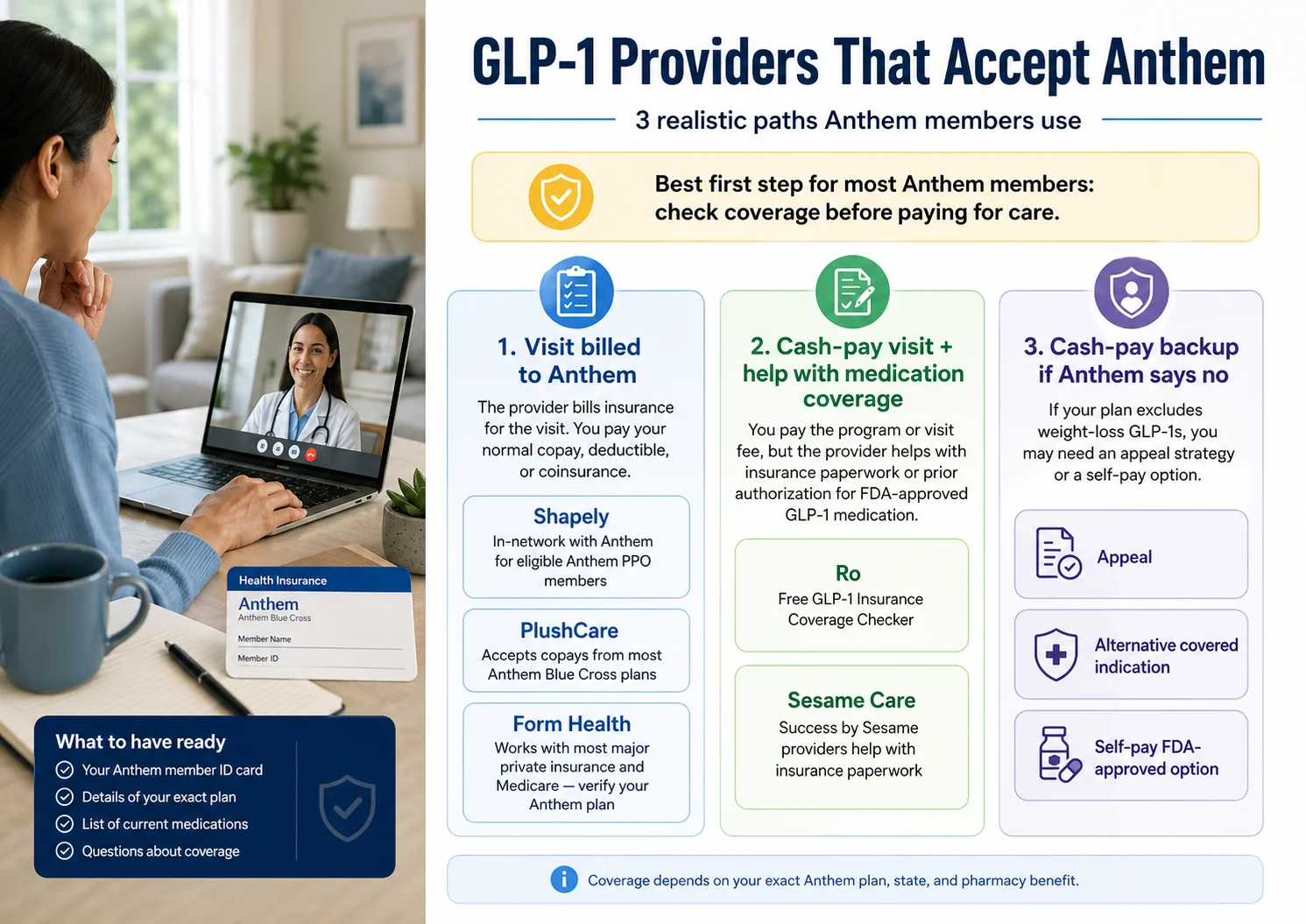

What “GLP-1 providers that accept Anthem” actually means

The short version: “Accepts Anthem” is doing three different jobs in different telehealth marketing copy. It can mean the provider bills Anthem for the office visit (true in-network billing). It can mean the provider is cash-pay but their team submits prior authorization on the medication. It can mean the provider doesn't touch insurance at all and offers a cash-pay backup if Anthem denies you. Pick the lane that matches what you actually want — visits covered, medication covered, or both.

Lane 1: The provider bills Anthem for visits (true in-network)

This is the most literal reading of “accepts Anthem.” The telehealth medical practice has contracted with Anthem (or an Anthem-affiliated Blue Cross Blue Shield plan in your state) and bills Anthem for the office or video visit. You pay your normal Anthem copay, deductible, and coinsurance — exactly like you would at an in-person primary care doctor.

Who fits this lane: Shapely (in CA, FL, NY, TX for Anthem PPO members), PlushCare (most Anthem Blue Cross plans), Form Health (most major private insurance and Medicare; verify Anthem-specific participation at intake).

The catch: Most national-name GLP-1 telehealth brands (Ro, Hims, Sesame, MEDVi, Embody) do not bill Anthem for visits. Their membership is cash-pay. That's not a flaw — it's a different model — but it's important to know upfront.

Lane 2: The provider has an insurance concierge for the medication

This is where most national-name FDA-approved GLP-1 telehealth lives. The membership itself is cash-pay (not billed to Anthem), but a dedicated team verifies your benefits, files prior authorization on the medication side, fights denials, and gets your prescription routed to your insurance pharmacy where you pay your normal Anthem copay on Wegovy, Zepbound, or Ozempic.

The leader here is Ro. Ro publishes one of the clearest medication-side insurance workflows in this category — a centralized concierge team plus a free GLP-1 Insurance Coverage Checker that anyone can use to check Anthem coverage before signing up. See also our guide to GLP-1 providers that help with prior authorization.

Lane 3: The provider offers cash-pay backup when Anthem won't cover the medication

This isn't really “accepting Anthem” in the insurance sense. It's a backup path for the (sadly common) scenario where Anthem denies coverage or your plan excludes weight-loss GLP-1s outright. The provider doesn't bill Anthem and doesn't file prior authorization. You pay cash for both the membership and the medication. This lane includes Ro's NovoCare and LillyDirect cash-pay integrations, Sesame's branded self-pay pricing, and the broader cash-pay GLP-1 options.

Reader translation

- If you want Anthem to pay for the visit, you want Lane 1. The honest list is short: Shapely, PlushCare, Form Health.

- If you want Anthem to pay for the medication but you're willing to pay cash for the membership, you want Lane 2. Ro is the strongest pick. Sesame Care is a solid second.

- If your Anthem plan won't cover GLP-1s at all, Lane 3 is your reality — and within that lane, the FDA-approved cash-pay paths through Ro at LillyDirect and NovoCare pricing are usually cheaper than retail by hundreds of dollars per month.

The mistake we see Anthem members make over and over: they pay for a Lane 2 membership before they know whether their plan actually covers the medication. That's why we lead with Ro's free Coverage Checker — it answers the most expensive question for free, before you commit to anything.

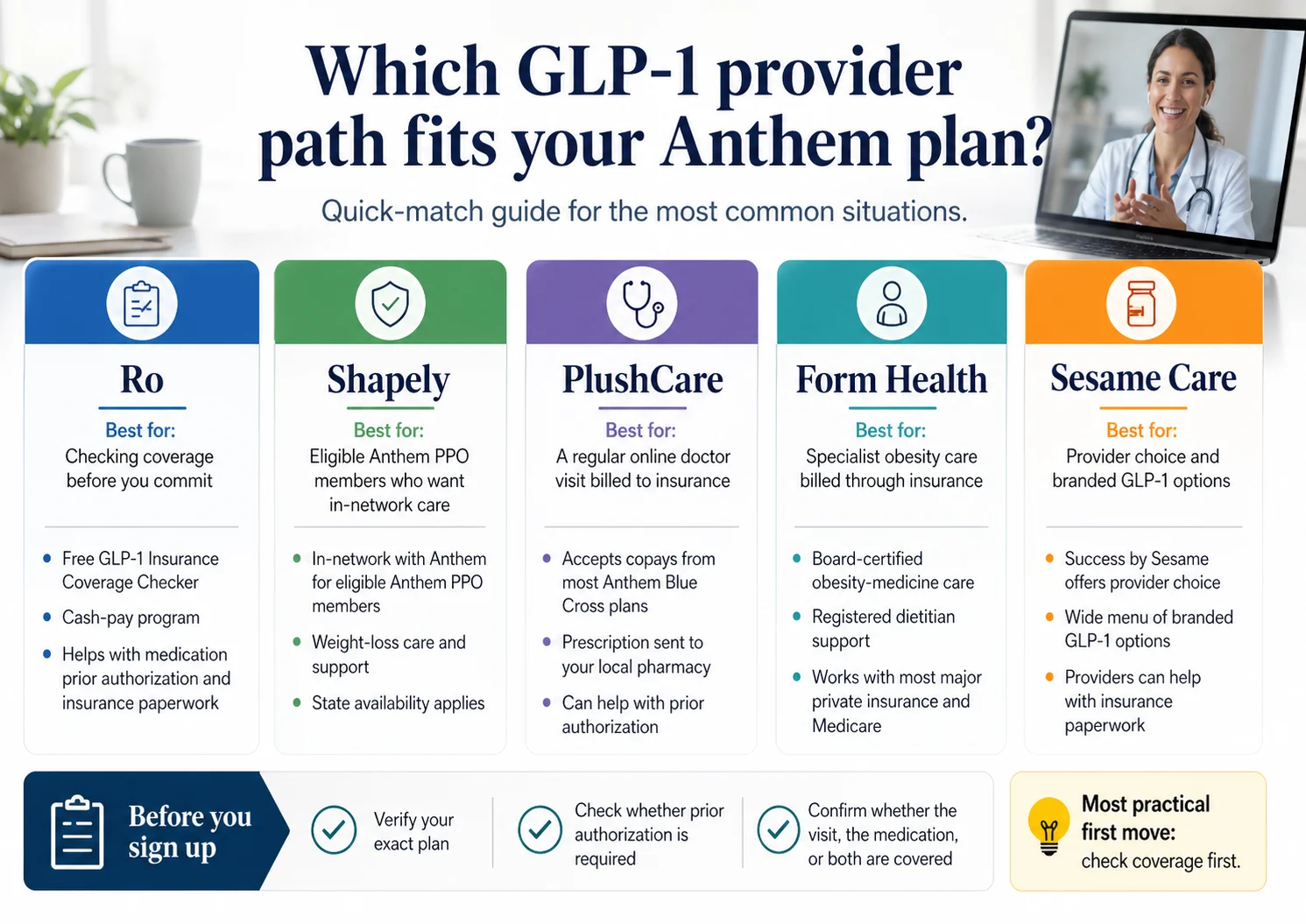

The 5 real paths: Anthem GLP-1 provider compatibility matrix

The short version: Five providers cover the realistic Anthem GLP-1 landscape. Each one fits a different reader — based on whether you need visit billing, medication coverage help, or both, plus your state and plan type.

| Provider | Bills Anthem for visits? | PA support on medication | Free coverage checker | Cost (program/membership) | Best for |

|---|---|---|---|---|---|

| Ro (Ro Body) | No — cash-pay membership | Yes — centralized insurance concierge | Yes | $39 first month; $149/mo monthly, or as low as $74/mo with annual prepay | Anthem members unsure if their plan covers the medication; FDA-approved focus |

| Shapely | Yes — in-network with Anthem PPO in CA, FL, NY, TX | Yes — concierge support locating in-stock pharmacies | No | $49/mo program fee + Anthem visit cost-sharing | Eligible Anthem PPO members in those four states |

| PlushCare | Yes — accepts copays from most Anthem Blue Cross plans | Yes — care team can submit PA | No | Membership fee plus your Anthem visit copay (verify at booking) | Anthem members who want a regular online doctor visit |

| Form Health | Yes for most major private insurance and Medicare; verify Anthem at intake | Yes — board-certified obesity-medicine physicians file PA | No | Insurance copay/deductible if covered; $299/mo if self-pay | Anthem members who want specialist obesity care with dietitian support |

| Sesame Care | No — cash-pay subscription | Yes — Success by Sesame providers assist with insurance paperwork | No | Starts at $59/mo with annual subscription | Anthem members who want a wide brand-name menu and provider choice |

Editorial conclusion (our judgment)

For most Anthem members trying to lower their GLP-1 medication cost, Ro is the best first move — a centralized insurance concierge plus a free Coverage Checker tool that answers the most expensive question before you pay for ongoing care. Shapely, PlushCare, and Form Health are the right answer specifically when “accept Anthem” to you means “I want my plan to pay for the visit, not just the medication.” Sesame Care is the strongest second when you want to choose your own provider and access a wide brand-name formulary.

Best for most Anthem members: Ro

The short version: Ro is the strongest fit for most Anthem members because three things stack — a centralized insurance concierge (not just a single prescriber filing paperwork), a broad FDA-approved formulary at the lowest cash-pay prices available, and a free Coverage Checker that lets you verify before you commit. In Ro's published 2025 Coverage Checker Report (a Ro-overall dataset, not Anthem-only), 43% of users had GLP-1 weight-loss coverage and half of covered patients had copays at or below $50/month.

What Ro's insurance concierge actually does

When you sign up for Ro Body, the insurance concierge isn't a chatbot. It's a specialized team. Here's the workflow Ro publishes:

- Benefits verification. They check whether your GLP-1 costs can be covered without prior authorization (sometimes they can).

- Prior authorization submission. If PA is required, the concierge files the paperwork on your behalf.

- Denial handling. If Anthem denies the first request, the concierge can resubmit with stronger documentation or pivot to a clinically appropriate alternative (Wegovy if Zepbound was denied, for example) and re-file.

- Pharmacy coordination. Once approved, your prescription is sent to your preferred pharmacy. You pick it up like any other prescription — only now you're paying your Anthem copay instead of $1,300 cash.

The whole process typically takes about 2–3 weeks from sign-up to first fill, per Ro.

Ro's FDA-approved GLP-1 formulary in 2026

- Foundayo (orforglipron) — Eli Lilly's new oral GLP-1 tablet, FDA-approved April 1, 2026

- Wegovy pill (oral semaglutide) — the first oral GLP-1 specifically approved for weight management

- Wegovy pen (injectable semaglutide)

- Zepbound pen and Zepbound KwikPen (injectable tirzepatide)

- Zepbound vials (the lower-cost vial-and-syringe format via LillyDirect)

- Ozempic — FDA-approved for type 2 diabetes; sometimes prescribed off-label for weight loss when clinically appropriate

Ro states that its cash-pay prices on these medications match LillyDirect, NovoCare, and TrumpRx pricing. If your Anthem plan denies coverage, you're not stuck at retail — you're at manufacturer pricing through Ro's integrations.

What Ro Body costs

- $39 for the first month as an intro offer

- $149 a month on the standard monthly plan

- As low as $74 a month when you prepay for an annual plan

The Ro Body membership is separate from medication cost. Current cash-pay medication pricing on Ro:

- Wegovy pill — starts at $149/month for lower starting doses

- Wegovy pen — $199/month introductory, then $199–$349/month depending on dose and eligibility

- Zepbound KwikPen — $299 for 2.5 mg, $399 for 5 mg, $449 for 7.5 mg through 15 mg via LillyDirect's discounted manufacturer offer (45-day refill window applies)

- Foundayo — starts at $149/month for the starting dose; higher doses priced higher

If your Anthem plan covers the medication, you pay your Anthem copay plus the Ro Body fee instead.

The honest part about Ro

Ro Body's membership itself is cash-pay. Ro does not bill Anthem for the visit. If your only goal is “I want a provider that bills Anthem for the visit the way my regular doctor does,” Ro isn't your answer — Shapely, PlushCare, or Form Health are.

The reason Ro still wins for most Anthem members is that what makes GLP-1 access expensive isn't the visit, it's the medication. Retail Wegovy is around $1,349 a month. Retail Zepbound is around $1,086. The visit is a rounding error. Ro's insurance concierge is structured around the medication side, and the membership fee is what buys you that team — plus access to the lowest cash-pay prices if Anthem says no.

One more thing: Ro states it cannot coordinate GLP-1 medication coverage for government insurance plans, with Federal Employee Health Benefits Program (FEHB) as an exception. If you're on Anthem Medicare Advantage or Anthem-administered Medicaid and you specifically want help getting GLP-1 coverage through your government plan, Ro isn't the right path right now.

Real member experience

In Ro's published 2025 Insurance Coverage Checker Report, one member described initially delaying her GLP-1 journey by months because she thought she'd have to pay around $1,000 a month for medication, then discovered through Ro that her actual cost was a fraction of that after coverage was checked and PA was approved. Another member described having Ro handle a Wegovy-to-Zepbound switch with prior authorizations resubmitted within about a week. (Source: Ro 2025 Coverage Checker Report. Ro labels member stories as paid partner content. Individual experiences are not typical results.)

Check what Ro can actually do for your Anthem plan

Run your specific Anthem plan through Ro's free GLP-1 Insurance Coverage Checker. You'll get a personalized benefits report with copay details and PA requirements. The check itself is free — you'll provide your name and insurance card so Ro can do the lookup.

Start My Free Anthem Coverage Check → (sponsored affiliate link, opens in a new tab)When Shapely is the better Anthem choice

The short version: Shapely is the strongest fit when you specifically want Anthem PPO visits billed in-network and you live in California, Florida, New York, or Texas. Shapely's published Anthem page states they're in-network with Anthem for weight-loss care. The trade-off is state availability — outside those four states, Shapely isn't an option right now.

What Shapely says about Anthem

Shapely's published Anthem insurance page states the practice is in-network with Anthem and that eligible Anthem PPO members can access medical treatment, lifestyle support, and weight-loss care covered by insurance. For commercial insurance members where the medication is covered, Shapely says copays are typically around $25 a month — though the exact amount depends on your specific plan.

That's a meaningfully different value proposition than Ro. With Shapely, the visit itself is being billed to Anthem the way your regular doctor would bill it. You pay your normal copay, deductible, and coinsurance — not a separate cash-pay membership for the visit.

Where Shapely fits — and where it doesn't

Shapely's primary fit:

- Anthem PPO members specifically (verify your plan type at intake)

- Living in California, Florida, New York, or Texas

- Want medical visit + lifestyle support + weight-loss care as a coordinated program billed through insurance

Shapely's program fee is $49 a month for app access, chat with the care team, education content, tracking tools, and concierge support locating in-stock pharmacies. That's separate from your Anthem visit cost-sharing.

The honest limitation

Shapely is excellent if you fit. The two filters are real, though: you need a qualifying Anthem PPO plan and you need to be in one of the four supported states. If you're outside CA/FL/NY/TX, no amount of paperwork will fix that — Shapely is a state-licensed practice.

If Shapely doesn't fit your state, the next-best in-network alternative for an Anthem-billed visit is PlushCare (broader national coverage, more general-doctor model) or Form Health (specialist obesity care, also billed through insurance — verify Anthem participation).

See if Shapely works with your Anthem PPO plan in CA, FL, NY, or TX

Shapely's intake will verify your specific plan and state in a few clicks. Best fit if you specifically want Anthem PPO visits billed in-network alongside ongoing weight-loss support.

Check Shapely Anthem Eligibility →When PlushCare fits: Anthem copay-style telehealth visits

The short version: PlushCare is the right pick when you want a regular online doctor visit billed to Anthem on a copay basis — not a GLP-1-membership-first program. PlushCare states it accepts copays from most Anthem Blue Cross plans, and the care team can submit prior authorization for branded weight-loss medications when clinically appropriate.

What makes PlushCare different from Ro and Sesame

PlushCare isn't a GLP-1 specialist platform. It's a national virtual primary care practice. You book a video visit with a licensed doctor, you pay your normal Anthem copay (because PlushCare bills your insurance for the visit), and if the doctor determines a GLP-1 is clinically appropriate, they write the prescription and the care team can help with prior authorization on the medication side.

That structure works well for Anthem members who:

- Don't want to pay a separate $39–$149/month membership on top of their insurance

- Want a doctor relationship more than a coaching program

- Have an Anthem Blue Cross plan with a standard PCP copay

- Are willing to pay the prescription cost separately at their pharmacy

What PlushCare says about prior authorization

PlushCare warns clearly that not every Anthem plan covers branded weight-loss medications and that most branded weight-loss prescriptions require prior authorization. Their care team can reach out to Anthem on the patient's behalf, but coverage is plan-specific — PlushCare can submit the PA, but they can't override formulary exclusions.

PlushCare's published advice for new GLP-1 patients: bring documentation of your prior medication history, lab results, and any earlier diet/exercise program records to your first visit. That documentation is what makes a clean first PA submission instead of an automated denial. For more, see our guide to getting insurance to cover GLP-1.

Where PlushCare doesn't fit

PlushCare doesn't ship medications to your door — your prescription goes to your local pharmacy. There's no app-based progress tracking on the same level as Ro or Shapely. There's no included dietitian or weekly coaching. If you want a coordinated program with coaching, labs, and an integrated app experience, this isn't that. PlushCare is a doctor visit billed to Anthem. That's the value, and it's a real one — but it's narrower than a comprehensive weight-loss membership.

Check PlushCare visit cost with your Anthem plan

Best fit when you want a normal online doctor visit billed to your Anthem Blue Cross plan, not a GLP-1 membership. PlushCare's booking flow shows you the visit cost before you confirm.

Book a PlushCare Anthem Visit →When Form Health fits: insurance-billed specialist obesity care

The short version: Form Health is built around board-certified obesity-medicine physicians and registered dietitians, and the program is billed through most major private insurance plans and Medicare. It's the strongest fit when you want specialist clinical care — not just a general doctor — billed through your Anthem plan, after Form verifies your specific plan at intake.

Form Health's insurance-native model

Form Health's structure is closer to an in-network medical practice than a consumer telehealth brand. Visits, lab tests, and FDA-approved medications are billed through insurance. You pay your copay or deductible based on your specific Anthem plan. If your plan doesn't cover Form Health's program, the self-pay rate is $299 a month — on the higher end, but reflects the specialist credentialing and dietitian support.

What you get when insurance covers it:

- Monthly video visits with a board-certified clinician

- Visits with a registered dietitian

- Lab testing through the program

- FDA-approved GLP-1 medications when clinically appropriate, with prior authorization handled by the clinical team

- App-based messaging and progress tracking

Form Health states it only prescribes FDA-approved medications — they're not in the compounded GLP-1 lane. That's a meaningful trust signal for Anthem members who want their care to look like specialist medicine, not direct-to-consumer telehealth.

Eligibility and the Anthem-specific verification step

Form Health requires you to be 18+ with a BMI of 30 or above, or 27 or above with a weight-related risk factor (the standard FDA-aligned criteria for GLP-1 eligibility). They also require you to have an existing primary care physician with a visit in the last 12 months — they're a specialist add-on, not a replacement for primary care.

The one verification step we'd encourage before signing up: confirm Anthem-specific in-network participation for your specific plan. Form Health says it works with most major private insurance and Medicare, but Anthem has many flavors (Anthem Blue Cross, Anthem Blue Cross Blue Shield, Anthem HealthKeepers, Anthem Medicare Advantage). Run your card number through Form Health's intake — they'll verify specifically for your plan.

Verify whether Form Health can bill your specific Anthem plan

Best fit when you want specialist obesity-medicine care with a registered dietitian and labs, billed through Anthem instead of paying a cash membership.

Check Form Health Coverage →When Sesame Care beats Ro: provider choice and a wide brand-name formulary

The short version: Sesame's Success by Sesame program is the strongest second when you want to choose your own provider from a marketplace and want access to a wide brand-name GLP-1 formulary in telehealth. Their providers facilitate Anthem prior authorization paperwork on FDA-approved medications, and patients who get coverage approved and stack a manufacturer savings card can pay as little as $25 a month for branded GLP-1s.

Why Sesame is structured differently

Most GLP-1 telehealth platforms randomly assign you a provider. Sesame's marketplace lets you browse provider profiles, read patient reviews, check credentials, and pick the person you want managing your care. That's a real differentiator if patient–provider fit matters to you.

The Success by Sesame weight-loss program starts at $59/month on an annual subscription (verify current flexible-plan pricing in checkout). The subscription includes ongoing video visits, dedicated provider care, lab testing through Quest, and unlimited messaging. Medication is billed separately based on insurance status and the specific medication.

Sesame's medication menu

- Wegovy injection and Wegovy pill (oral semaglutide)

- Zepbound KwikPen and Zepbound vial

- Ozempic and Mounjaro

- Foundayo (orforglipron) — FDA-approved April 1, 2026

- Saxenda and Rybelsus

- Plus non-GLP-1 alternatives like Contrave and metformin when appropriate

Self-pay pricing on Sesame's program page (verify at signup, since promotional pricing shifts):

- Wegovy pill starts at $149/month for the lower starting doses

- Wegovy injection at $199/month introductory, then $349/month standard self-pay

- Zepbound vials at LillyDirect pricing starting $299/month

- Zepbound KwikPen at $1,086/month self-pay (most members route this through insurance with PA)

For Anthem members who get coverage approved and use a manufacturer savings card, brand-name GLP-1s through Sesame can drop to as little as $25/month with insurance, depending on the medication and plan.

Two honest limitations

First, Sesame's billing cadence runs on a 28-day cycle (verify in checkout), which on a flexible plan can mean billing more often than once a month. It's not a hidden fee, but it's worth knowing if you're comparing monthly numbers head-to-head with Ro.

Second, Sesame says Success by Sesame providers assist with insurance paperwork and prior authorization. If your goal is centralized concierge support with a dedicated team handling submissions and resubmissions, Ro's model is more centralized. If your goal is provider choice and a broad menu, Sesame is the right call.

Browse Success by Sesame providers and current GLP-1 pricing

Best fit when you want to pick your own clinician and access a wide brand-name menu in telehealth.

See Sesame's GLP-1 Plans → (sponsored affiliate link, opens in a new tab)Does Anthem actually cover GLP-1s for weight loss in 2026?

The short version: Sometimes. Anthem has no single national policy. Coverage depends on your plan type, your state, your employer, and whether the prescription is for weight management or another FDA-approved indication. California Medi-Cal Rx (which includes Anthem-administered Medi-Cal managed care) ended weight-loss coverage of Wegovy, Zepbound, and Saxenda effective January 1, 2026. Anthem covers about 14 states under Blue Cross or Blue Cross Blue Shield branding; outside those states, you may be on a different Blue Cross licensee with different rules.

What Anthem is — and what it isn't

Anthem (a subsidiary of Elevance Health) operates Blue Cross or Blue Cross Blue Shield plans in roughly 14 states, including California, Colorado, Connecticut, Georgia, Indiana, Kentucky, Maine, Missouri, Nevada, New Hampshire, New York, Ohio, Virginia, and Wisconsin. Pharmacy benefits are typically administered through CarelonRx, Anthem's pharmacy benefit manager, with formularies that vary by plan. Member tools live at anthem.com or through the Sydney Health mobile app.

If you're in Massachusetts, Michigan, Florida (most plans), Texas (most plans), or many other states, your “Blue Cross” plan is a different Blue Cross licensee — not Anthem. Coverage policies on those plans don't transfer to Anthem and vice versa.

The 2026 Anthem coverage reality

| Plan / source | 2026 GLP-1 weight-loss status | Source type |

|---|---|---|

| California Medi-Cal Rx (Anthem-administered Medi-Cal managed care) | Coverage ended January 1, 2026 for Wegovy, Zepbound, Saxenda for weight-loss indications. PA still possible for non-weight-loss indications (CVD, OSA, MASH) | Anthem CA provider portal fact sheet |

| Anthem commercial plans across all 14 states | Highly variable by plan type and employer; Anthem warns formulary inclusion does not by itself guarantee benefit coverage | Anthem pharmacy pages / drug list tools |

| Anthem Medicare Advantage | Weight-loss-only coverage excluded historically; Medicare GLP-1 Bridge launches July 1, 2026 for eligible Part D beneficiaries at $50/month flat copay | CMS BALANCE Model FAQ |

| Anthem-administered Medicaid (other states) | Varies by state Medicaid policy; only 13 state Medicaid fee-for-service programs covered GLP-1s for obesity as of January 2026 | KFF Medicaid Coverage of GLP-1s, January 2026 |

What's typically still covered

Even when Anthem won't pay for a GLP-1 for weight loss specifically, the same medications may still be covered for other FDA-approved indications:

- Ozempic — for type 2 diabetes management (its primary FDA approval)

- Mounjaro — for type 2 diabetes

- Wegovy — for cardiovascular risk reduction in adults with established cardiovascular disease and obesity, or for adults with obesity and metabolic dysfunction-associated steatohepatitis (MASH)

- Zepbound — for moderate-to-severe obstructive sleep apnea in adults with obesity (FDA-approved this indication December 20, 2024)

If you have a covered comorbidity, your prescriber can document the qualifying indication — often the cleanest path to approval. See also our guide to GLP-1 providers that accept insurance and our guide to getting insurance to cover GLP-1.

Why two Anthem members on the same street can have different coverage

It comes down to whether the employer plan is fully insured (Anthem makes the coverage decisions) or self-funded (the employer makes coverage decisions and uses Anthem to administer claims). Two Anthem members in the same state with the same brand on their card can have completely different formularies if one works for an employer that included GLP-1 coverage and the other doesn't.

How to check Anthem's drug list (or use Sydney Health) for GLP-1 coverage

The short version: Anthem provides drug list tools at anthem.com and inside the Sydney Health mobile app. You can search Wegovy, Zepbound, Foundayo, Ozempic, or Mounjaro by name and see your specific plan's formulary tier, prior authorization requirements, step therapy flags, and exclusion language. This takes about five minutes once you're logged in.

The step-by-step lookup

- Log in at anthem.com or open the Sydney Health app on your phone (you'll use the same credentials).

- Navigate to “Pharmacy” from the main menu.

- Select “Find a Drug” or your plan's drug list / formulary.

- Search for each medication by both brand name and generic name: Wegovy (semaglutide), Wegovy pill (oral semaglutide), Zepbound (tirzepatide), Foundayo (orforglipron), Saxenda (liraglutide), Ozempic, Mounjaro, Rybelsus.

- Note the tier and any flags. The Notes column shows whether prior authorization (PA) or step therapy (ST) applies. Look for words like “PA Required,” “Step Therapy,” or “Excluded” / “Not Covered.”

- Screenshot what you find. This becomes your reference when you're talking to a provider, comparing telehealth options, or appealing a denial.

What to do if the medication shows as “excluded”

If your drug list shows the medication as excluded for your plan — that's different from “covered with prior authorization.” A true exclusion means Anthem doesn't cover that medication category for your plan, regardless of medical necessity. No PA can override an exclusion.

What to do if you can't find the answer in the drug list

Some employer-sponsored plans have custom formularies that aren't fully exposed in the public drug list tool. If you're not getting a clear answer, two paths:

- Call Anthem member services using the number on the back of your card and use the script in the next section.

- Run your card through Ro's free Coverage Checker — they'll do the call for you and email you the answer.

Skip the 30-minute hold time on Anthem

Ro contacts Anthem on your behalf and emails you a benefits report showing what your plan covers and what PA will require. The check is free.

Run My Anthem Plan Through Ro's Free Coverage Checker → (sponsored affiliate link, opens in a new tab)The Anthem call script (if you want to verify yourself)

The short version: If you'd rather call Anthem directly than use Ro's Coverage Checker, the script below gets you a clean answer in one call. Take notes. Get the rep's name and a reference number. Total time: usually 15–30 minutes.

Call the member services number on the back of your insurance card and ask these questions in order:

- “Is Wegovy on my drug list, and what tier?” (Repeat for Zepbound, Foundayo, Saxenda, and — if relevant — Ozempic, Mounjaro, Rybelsus.)

- “Is the medication covered for my diagnosis, or is there a benefit exclusion for weight loss?” — Exclusion and prior authorization mean very different things.

- “If it's not excluded, is prior authorization required? What about step therapy?”

- “What clinical criteria does my plan require for approval?” (BMI threshold, comorbidity documentation, prior weight-loss attempts, etc.)

- “Do I need to be enrolled in a supervised weight-loss program before or during treatment?”

- “What's the renewal criteria after the initial approval period?”

- “Which PBM administers my pharmacy benefits — CarelonRx or another?”

- “Can a telehealth provider submit the prior authorization, or does it need to come from an in-person doctor?”

- “What's my expected copay or coinsurance after deductible, by tier?”

- “Does my employer plan have a GLP-1 rider or exclusion?” (For commercial plans only.)

- “Are there separate criteria for FDA-approved indications other than weight loss — OSA, cardiovascular disease, MASH, type 2 diabetes?”

- “What are the timelines for standard PA, expedited PA, step therapy exceptions, and appeals on my plan?”

Write this down before you hang up

| Item | What the rep said |

|---|---|

| Medication asked about | Record your answer here |

| Formulary tier | Record your answer here |

| PA required? | Record your answer here |

| Step therapy required? | Record your answer here |

| Excluded for weight loss? | Record your answer here |

| Required BMI / comorbidity | Record your answer here |

| Estimated copay | Record your answer here |

| PBM | Record your answer here |

| Rep name | Record your answer here |

| Reference number | Record your answer here |

| Next step | Record your answer here |

Documents to gather before any GLP-1 visit

Whether you're going to Ro, Shapely, PlushCare, Form Health, Sesame, or your in-person PCP, bring this:

- Insurance card (front and back)

- Current height and weight (BMI)

- Weight history over the last 12+ months

- Documentation of prior diet and exercise efforts (apps, programs, gym memberships, food logs)

- Prior weight-loss medication history (what you tried, what happened)

- Recent labs (last 6 months if available)

- Any documented comorbidities (hypertension, type 2 diabetes, dyslipidemia, OSA, CVD)

- Prior denial letters and case numbers, if applicable

What if Anthem denies your GLP-1?

The short version: A denial isn't the end. The first move is identifying the denial type — because prior authorization denial and benefit exclusion require completely different responses. See our full guide to GLP-1 prior authorization for a deep-dive.

Denial type decision tree

| Denial reason | What it usually means | Best next step |

|---|---|---|

| Missing BMI / weight records | Documentation gap | Ask your provider to resubmit with baseline + current weight |

| No documented lifestyle effort | Criteria gap | Submit program receipts, app data, dietitian notes, or clinician documentation |

| Step therapy required | Plan wants you to try cheaper meds first | Ask which alternatives, document any prior intolerance, or request a step therapy exception |

| Not medically necessary | Criteria mismatch | Request the plan's full criteria in writing; get a clinical letter of medical necessity |

| Not on formulary | Drug-list problem | Request a formulary exception or ask which alternative GLP-1 is on your formulary (often Wegovy if Zepbound is excluded) |

| Benefit exclusion / plan exclusion | Your plan doesn't cover this category | Appeals are unlikely to succeed; pivot to alternate indication, employer route, or cash-pay |

| Renewal denial after initial approval | Failed to meet ongoing criteria (e.g., documented weight loss) | Document weight maintenance arguments; appeal with weight history |

What appeals can and can't do

If your denial is a prior authorization denial (the plan covers GLP-1s but says you don't qualify), appeals can succeed when the plan covers the category and the denial is documentation-based. A clinician's letter of medical necessity citing your specific clinical rationale and comorbidities is worth requesting.

If your denial is a benefit exclusion (your plan doesn't cover weight-loss GLP-1s as a category), appeals rarely win. In that case, your real options become:

- Switch to an alternate covered indication. If you have a comorbidity (CVD, MASH, OSA, type 2 diabetes), your prescriber can document the qualifying indication.

- Employer route. Self-funded employer plans can add GLP-1 coverage at renewal. If your HR team is responsive, this is worth raising.

- FDA-approved cash-pay through manufacturer programs. Ro's NovoCare and LillyDirect integrations — Wegovy pill from $149/mo at lower doses, Wegovy pen at $199–$349/mo, Zepbound KwikPen $299–$449/mo depending on dose.

- Manufacturer savings cards. Wegovy and Zepbound both offer copay savings programs that can stack with cash-pay or commercial coverage. Eligibility excludes federal/state program enrollees.

When Ro can still help after a denial

Ro's insurance concierge keeps working after a first denial. Per Ro's published process: if the first medication is denied, the affiliated provider considers a clinically appropriate alternative (Wegovy if Zepbound was denied, for example) and the concierge resubmits. If all coverage attempts fail, you can pivot to Ro's cash-pay options at NovoCare/LillyDirect/TrumpRx pricing — the lowest cash-pay prices available — without losing your Ro Body membership.

Denied by Anthem? Find your right next step in 60 seconds

Take our free matching quiz to identify whether you're facing a PA denial (often appealable), a benefit exclusion (different strategy), or an unaffordable copay (where cash-pay or savings stacking might beat your insurance path).

Find My GLP-1 Path →Anthem Medicare Advantage and Anthem Medicaid in 2026

The short version: Government insurance is a different track. Anthem Medicare Advantage historically excluded GLP-1s prescribed solely for weight loss, but the Medicare GLP-1 Bridge launches July 1, 2026 and runs through December 31, 2027 — providing eligible Part D beneficiaries access to Foundayo, Wegovy, and Zepbound KwikPen at a $50/month flat copay for qualifying weight management. Anthem-administered Medicaid coverage varies by state — only 13 state Medicaid fee-for-service programs covered GLP-1s for obesity as of January 2026.

The Medicare GLP-1 Bridge — what it actually is

CMS announced the BALANCE Model and the Medicare GLP-1 Bridge demonstration on December 23, 2025. The Bridge runs from July 1, 2026 through December 31, 2027 (18 months) — covering Wegovy, Zepbound KwikPen, and Foundayo at $50/month. BALANCE did not launch for Medicare Part D in 2027 — CMS extended the Bridge. Watch for BALANCE 2028 announcements during fall 2027 open enrollment.

What the Bridge covers:

- Foundayo — all formulations (FDA-approved April 1, 2026; added to the Bridge April 6, 2026)

- Wegovy — both injection and tablet formulations

- Zepbound — KwikPen formulation only. Single-dose Zepbound vials and single-dose pens are not available through the Bridge.

Eligibility (per CMS guidance): age 18+, lifestyle modification, and one of the following:

- BMI ≥35

- BMI ≥30 with HFpEF (heart failure with preserved ejection fraction), uncontrolled hypertension despite two or more antihypertensive medications, or chronic kidney disease stage 3a or later

- BMI ≥27 with prediabetes, prior myocardial infarction, prior stroke, or symptomatic peripheral artery disease

Cost: $50/month flat copay for eligible Part D beneficiaries. The Bridge operates outside the normal Part D coverage and payment flow — pharmacies collect the $50 copay through a central processor (Humana administers it using LI NET infrastructure), and CMS states the copay does not count toward your True Out-of-Pocket (TrOOP) costs or gross covered prescription drug costs.

Important nuance on indications: the Bridge is for qualifying weight-management use. If your prescriber is using the medication for a basic Part D-coverable indication (Zepbound for OSA, or Wegovy for cardiovascular risk reduction in adults with established CV disease), the prior authorization goes through your standard Part D plan instead.

The catch for Anthem Medicare Advantage members

The Bridge is administered through Humana as the central processor, not through your Medicare Advantage plan directly. That means your prescriber submits the PA through the Bridge process, not through Anthem's standard pharmacy benefit. This is good news — you don't have to fight Anthem MA's standard formulary — but it's a separate workflow.

CMS will publish full details on the prior authorization process in Spring 2026. If you're an Anthem Medicare Advantage member who thinks you might qualify, get your eligibility documentation organized now — BMI, comorbidity diagnosis, and any cardiovascular event history — so your prescriber can submit immediately when the Bridge opens July 1, 2026. See our guide to GLP-1 providers that accept insurance for Medicare-specific options.

Anthem Medicaid by state

Medicaid coverage for weight-loss GLP-1s is decided state-by-state. As of January 2026, KFF reports that 13 state Medicaid fee-for-service programs covered GLP-1s for obesity. Several states cut coverage in late 2025 and early 2026:

- California Medi-Cal Rx: Weight-loss coverage ended January 1, 2026 (covers Anthem-administered Medi-Cal managed care). PA still possible for non-weight-loss indications.

- Pennsylvania Medicaid: Eliminated obesity-treatment GLP-1 coverage effective January 1, 2026.

- New Hampshire and South Carolina also eliminated GLP-1 obesity-drug coverage.

- North Carolina eliminated then reinstated coverage.

Which telehealth providers can actually help on government insurance

Honestly? Few. Most national-name FDA-approved GLP-1 telehealth platforms — Ro included — say they cannot coordinate GLP-1 medication coverage for government insurance plans. Ro's exception is FEHB (Federal Employee Health Benefits Program), which can use Ro Body's insurance concierge.

For Anthem Medicare members specifically, Form Health's published policy states it works with most major private insurance and Medicare. Verify your specific Anthem Medicare Advantage plan with their intake before signing up.

How we verified this

What we actually verified — April 30, 2026 (click to expand)

Verified directly from each provider's published policy or pricing page:

- Ro Body pricing ($39 first month, $149/mo monthly, as low as $74/mo with annual prepay) — ro.co/weight-loss/pricing

- Ro's free GLP-1 Insurance Coverage Checker (free; requires user to enter name and insurance card information) — ro.co/weight-loss/glp1-insurance-checker

- Ro Coverage Checker dataset (43% of users had GLP-1 weight-loss coverage; half of covered patients had ≤$50/month copay; data collected August 2024 through April 2025; Ro-overall, not Anthem-specific) — Ro 2025 Coverage Checker Report

- Ro's FDA-approved GLP-1 formulary (Foundayo, Wegovy pill, Wegovy pen, Zepbound pen, Zepbound KwikPen, Zepbound vials via LillyDirect, Ozempic) — ro.co/weight-loss

- Ro's government insurance limitation (cannot coordinate GLP-1 coverage for government insurance plans; FEHB is the exception) — ro.co/weight-loss/insurance

- Shapely's Anthem PPO in-network status, $49/mo membership, and CA/FL/NY/TX state availability — getshapely.com/weightloss/insurance/anthem

- PlushCare's Anthem Blue Cross copay acceptance and PA support — plushcare.com

- Form Health insurance-billed model (most major private insurance and Medicare; $299/mo self-pay; BMI 30+ or 27+ with risk factor; PCP visit within 12 months required) — formhealth.co/faqs

- Sesame Care subscription pricing ($59/mo annual) and medication menu — sesamecare.com/service/online-weight-loss-program

- California Medi-Cal Rx January 1, 2026 GLP-1 weight-loss coverage end — providers.anthem.com (CA provider portal fact sheet)

- CMS Medicare GLP-1 Bridge eligibility, drug list, $50/month copay, Humana administration — cms.gov/medicare/coverage/prescription-drug-coverage/medicare-glp-1-bridge

- FDA Foundayo (orforglipron) approval — April 1, 2026 — fda.gov press announcement

- FDA proposed exclusion of semaglutide, tirzepatide, liraglutide from 503B bulks list — April 30, 2026 — fda.gov press announcement

- KFF Medicaid GLP-1 obesity coverage figures (13 states as of January 2026) — KFF Medicaid Coverage of and Spending on GLP-1s, January 2026

What we couldn't verify directly and labeled accordingly:

- State-by-state Anthem commercial plan formulary detail beyond what's in primary Anthem documents. Two Anthem members in the same state can have different coverage based on employer plan design. Always verify your specific plan via Sydney Health, anthem.com, or by calling the number on your card.

- Form Health Anthem-specific in-network participation — Form's published policy supports “most major private insurance and Medicare” but does not name Anthem specifically. Confirm at intake.

- Sesame Anthem-specific visit billing — Sesame's subscription is cash-pay; medication-side PA support is provider-driven. Specific Anthem visit-billing questions should be confirmed with Sesame support.

- PlushCare exact membership fee tier — PlushCare's Anthem Blue Cross copay acceptance is published; current visit fee structure should be confirmed in the booking flow.

Update cadence: Pricing rows refreshed monthly. Anthem state-level signals refreshed quarterly. FDA and CMS regulatory items refreshed on news triggers.

Frequently Asked Questions

Do online GLP-1 providers actually accept Anthem?

Some do — but 'accept Anthem' means three different things. Some bill Anthem for visits (Shapely, PlushCare, Form Health). Some are cash-pay membership but help fight for medication coverage (Ro, Sesame Care). Some don't touch insurance at all. Match the lane to your goal: visit billing, medication coverage, or cash-pay backup.

Does Ro accept Anthem insurance?

Ro does not bill Anthem for the Ro Body membership — Ro's membership is cash-pay. However, Ro's insurance concierge contacts your Anthem plan to check medication coverage, files prior authorization on the medication, and handles denials. Ro's free GLP-1 Insurance Coverage Checker contacts your Anthem plan and emails you a benefits report at no cost (you'll provide insurance card details so Ro can run the lookup).

Does Shapely accept Anthem?

Yes. Shapely's published Anthem page states they're in-network with Anthem, with eligible Anthem PPO members able to access medical treatment, lifestyle support, and weight-loss care covered by insurance. Shapely currently serves adults in California, Florida, New York, and Texas.

Does PlushCare accept Anthem?

Yes — PlushCare states it accepts copays from most Anthem Blue Cross plans for visits. Their care team can submit prior authorization on branded weight-loss medications, but coverage is plan-specific.

Does Form Health accept Anthem?

Form Health states it works with most major private insurance and Medicare, with visits, labs, and medications billed through insurance. Anthem-specific participation should be verified through Form Health's intake for your specific plan.

Does Sesame Care accept Anthem?

Sesame's subscription is cash-pay (not billed to Anthem), but Success by Sesame providers assist with insurance paperwork and prior authorization on FDA-approved GLP-1s. Patients who get Anthem to cover the medication and stack a manufacturer savings card can pay as little as $25/month for branded GLP-1s through Sesame, depending on the medication and plan.

Does Anthem cover Wegovy for weight loss?

It depends on your specific plan. Many Anthem commercial plans cover Wegovy for weight loss with prior authorization. California Medi-Cal Rx (covering Anthem-administered Medi-Cal managed care) ended weight-loss coverage January 1, 2026. Always verify your specific plan's formulary at anthem.com or in Sydney Health.

Does Anthem cover Zepbound for weight loss?

Varies by plan. Many Anthem plans cover Zepbound for weight loss with PA. Some plans removed Zepbound while keeping Wegovy on formulary in 2025–2026. Zepbound is also FDA-approved for moderate-to-severe obstructive sleep apnea (December 2024) and may be covered for that indication when weight-loss coverage isn't available.

Does Anthem cover Foundayo?

Foundayo (orforglipron) was FDA-approved April 1, 2026 for chronic weight management. Coverage depends on individual Anthem plan formulary additions — newly approved drugs typically take time to appear on formularies. Anthem Medicare Advantage members may access Foundayo through the Medicare GLP-1 Bridge starting July 1, 2026 at a $50/month flat copay if eligible.

Does Anthem cover Ozempic for weight loss?

Ozempic is FDA-approved for type 2 diabetes — most Anthem plans cover Ozempic for diabetes with PA. Coverage for off-label weight-loss use is rare; most plans require diabetes documentation.

What is the difference between prior authorization and plan exclusion?

Prior authorization means your plan covers the medication if you meet specific clinical criteria (BMI, comorbidity, prior treatment attempts) and your provider documents them. Plan exclusion means your plan doesn't cover that medication category — no PA can override an exclusion. The two require completely different responses, which is why identifying the denial type is the critical first step.

What should I do if Anthem denies my GLP-1?

Identify the denial type first. If it's a documentation-based PA denial, appeal with stronger clinical records — these can succeed when the plan covers the category. If it's a benefit exclusion, appeals rarely work; pivot to an alternate FDA-approved indication you qualify for (CVD, OSA, type 2 diabetes, MASH), explore manufacturer cash-pay programs at NovoCare/LillyDirect prices, or consider the Medicare GLP-1 Bridge if you're Medicare-eligible.

Can I use HSA or FSA funds if Anthem doesn't cover my GLP-1?

Prescription GLP-1 costs and weight-loss program fees may be HSA/FSA-eligible when used to treat a specific physician-diagnosed disease such as obesity, diabetes, hypertension, or heart disease. General weight loss or appearance-based weight loss is not an eligible expense. Verify with your specific HSA/FSA administrator.

Can I use Anthem with a compounded GLP-1?

Generally no. Compounded GLP-1 medications are not FDA-approved and are typically not covered by Anthem (or any commercial insurer). Compounded GLP-1 telehealth is cash-pay only. If your Anthem plan covers FDA-approved GLP-1s with PA, the FDA-approved path almost always beats compounded on cost when stacked with manufacturer savings.

How long does Anthem prior authorization take?

Timelines vary by plan and medication. Industry-standard ranges: standard PA is typically days to a few weeks; expedited PA when medical urgency is documented is faster; step therapy exceptions and appeals add additional time. Total timeline from sign-up to first prescription, for a covered Anthem plan with concierge support, is typically 2–3 weeks per Ro's published process.

Still not sure which path fits your situation?

You've got Anthem, you want a GLP-1, and you now have the full landscape. Run your state, plan type, and coverage goal through our 60-second matching quiz — we'll route you to the right action: a free coverage check, an in-network provider for visit billing, or a cash-pay alternative if your plan excludes weight-loss GLP-1s.

Find My GLP-1 Path →Free. No signup required to see your result.

This page was researched and written by The RX Index Editorial Team. The RX Index is a pricing intelligence and comparison resource for GLP-1 telehealth providers. We may receive compensation when readers sign up with some of the providers covered on this page. Our editorial recommendations are based on verified provider behavior, current pricing, and reader fit — not on commission rate alone. Where a provider we don't earn commission on is the better fit for a specific reader, we say so.

Medical disclaimer: This page is informational and not medical advice. GLP-1 medications carry serious considerations including contraindications for personal or family history of medullary thyroid carcinoma (MTC) or Multiple Endocrine Neoplasia syndrome type 2 (MEN 2), and other warnings. Always consult a licensed healthcare provider before starting any prescription medication. Coverage decisions, pricing, and policies change frequently — verify directly with your specific Anthem plan and any provider before committing.