GLP-1 Superbill Guide: When It Works, What Insurers Need, and Which Document You Actually Need

Published: · Last updated:

A GLP-1 superbill can recover some of your visit or program fees — but it is not a magic document that makes a non-covered GLP-1 medication suddenly covered. For most people paying cash for a compounded semaglutide or tirzepatide telehealth program, the document you actually need isn’t a superbill at all. This guide covers which document fits your exact situation, exactly what has to be on the bill, which codes insurers expect, and which providers make the paperwork easier or harder.

The RX Index is a pricing intelligence and comparison resource for GLP-1 telehealth providers. This guide is educational and not medical, legal, insurance, or tax advice. We may earn a commission if you click through to a provider; that never changes what we recommend — we lead with the honest answer, including when the honest answer is that a superbill won’t help you.

Bottom Line Up Front

A GLP-1 superbill — a coded, itemized medical bill you submit to your insurance after paying an out-of-network provider — can recover some of your visit or program fees if your plan has out-of-network medical benefits. Here’s the honest version, by situation:

- Brand-name GLP-1 through a retail pharmacy with insurance coverage: skip the superbill conversation. Work your pharmacy benefit and, if denied, appeal via prior authorization — not a superbill. A superbill is for out-of-network medical services, not drugs your pharmacy filled under your pharmacy benefit.

- Out-of-network telehealth visit fees (the consult, the program fee, the provider’s monthly charge): a superbill can help if your plan has out-of-network medical benefits and the bill includes the fields insurers actually require. Reimbursement is based on your plan’s allowed amount, not what you paid.

- The medication itself, bought cash-pay through telehealth: commercial insurance reimbursement is possible but plan-specific and often hard to get. HSA, FSA, and HRA reimbursement is a separate documentation path that works for many people when the expense qualifies as medical care.

- Compounded GLP-1 specifically: most commercial plans make compounded-drug coverage difficult, and the FDA does not approve compounded finished drugs for safety, effectiveness, or quality. For most compounded patients, HSA/FSA — not insurance — is the realistic path.

Best for: insurance-first, brand-name GLP-1

Want someone to check your coverage before you pay anything?

Ro’s free GLP-1 Insurance Checker contacts your plan on your behalf and returns a personalized coverage report — whether Wegovy, Zepbound, Ozempic, or Foundayo is covered, whether prior authorization is required, and your estimated out-of-pocket cost. Ro Body membership starts at $39 for the first month, then as low as $74/month with annual prepay or $149/month month-to-month; medication cost is separate.

Check GLP-1 coverage free on Ro → (sponsored affiliate link, opens in a new tab)Not sure which path fits you?

Take the free 60-second GLP-1 path quiz — five questions about your budget, insurance situation, and reimbursement priorities, and we match you to the provider that fits.

Take the free 60-second GLP-1 path quiz →Trying to Get Reimbursed for What? Jump to Your Situation

| You paid for… | What you usually need | Will a superbill help? |

|---|---|---|

| Telehealth visit, consult, or program fee paid out-of-pocket | Superbill (coded itemized medical bill) | Usually yes — if your plan has out-of-network medical benefits |

| Brand-name GLP-1 filled at a retail pharmacy | Pharmacy claim form or prior authorization — not a superbill | No (wrong document) |

| Brand-name GLP-1 shipped cash-pay from a telehealth provider | Itemized pharmacy-style receipt + sometimes a pharmacy claim form | Sometimes — plan-specific |

| Compounded semaglutide or tirzepatide from a telehealth provider | Itemized receipt + often a Letter of Medical Necessity for HSA/FSA | Rarely (compounded coverage is plan-specific and often difficult) |

| HSA, FSA, or HRA reimbursement for any GLP-1 | Itemized receipt + LMN (often) | Different workflow — simpler than a superbill |

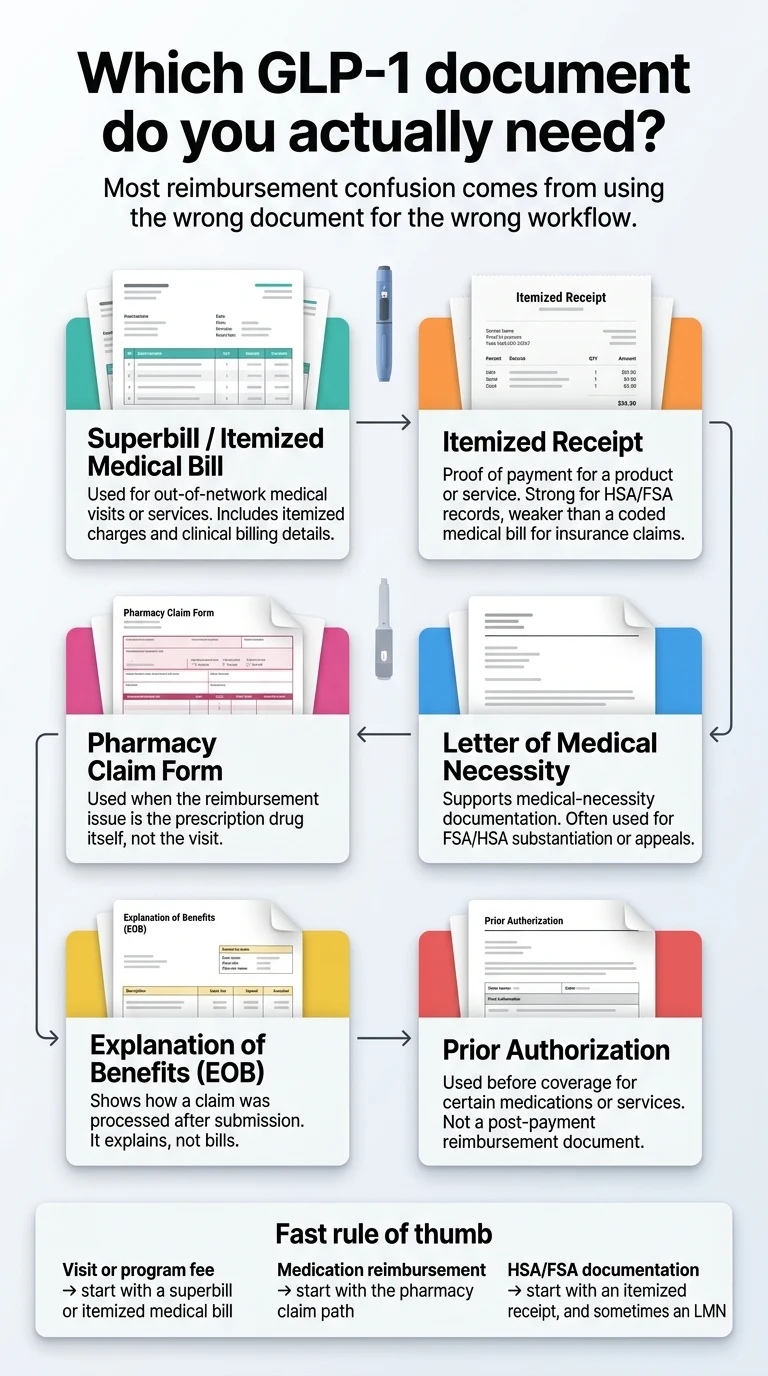

What Is a GLP-1 Superbill, Exactly?

A GLP-1 superbill is a detailed, coded medical invoice from an out-of-network provider containing CPT procedure codes for the visit, ICD-10 diagnosis codes that justified it, the provider’s NPI and Tax ID, itemized charges, and your patient information. You then submit that superbill to your insurance company for out-of-network reimbursement.

Three things matter right away. First, a superbill is specifically for medical services — visits, consults, programs — not for medications dispensed by a pharmacy. Second, it is not the same as a receipt; insurers typically want an itemized bill with codes, not just proof you paid. Cigna’s member medical claim form, for example, spells out the required fields and explicitly says a plain receipt is not a substitute. Third, a superbill reimburses you based on your plan’s allowed amount — which is often significantly less than what you paid.

A Superbill Is Not a Receipt

A plain checkout receipt — the email most GLP-1 telehealth providers send after billing you — shows what you paid and when. It doesn’t show the procedure code for the service or the diagnosis code that made the service medically necessary. Without those, most commercial insurers won’t process an out-of-network medical claim. Cigna’s member claim form requires an itemized bill that includes date of service, procedure or type-of-service code, charge, provider credentials, provider NPI, and Tax ID.

A Superbill Is Not an Explanation of Benefits (EOB)

An EOB arrives after your claim is processed. It explains what the insurer allowed, paid, and denied, and what you owe. It’s not a bill and not a payment request — it’s the insurer’s explanation of the math. Cigna says plainly: an EOB is not a bill. Don’t pay from it.

A Superbill Is Not Prior Authorization

Prior authorization is a pre-coverage workflow: your prescriber asks the insurer to approve a medication or service before you receive it. If you’re trying to get Wegovy or Zepbound covered under your pharmacy benefit, that’s a prior-auth issue — your doctor submits clinical documentation proving medical necessity, and the insurer approves or denies coverage in advance. A superbill, by contrast, is an after-payment reimbursement tool for out-of-network care you’ve already received.

Why GLP-1 Shoppers Keep Confusing These Documents

Because GLP-1 telehealth blurs every line. A single $349/month charge can cover a “visit,” a “program,” and the medication — often without itemization. Invoices that say “Monthly Program — Tirzepatide Subscription, qty 1 for 1 month” with no dose, no service code, no itemization are not superbills. They’re subscription confirmations. And that’s why this guide exists.

The GLP-1 Reimbursement Document Map

This is the single most important table on this page. Most “GLP-1 reimbursement” content online conflates three or four of these documents. They aren’t one thing. They do different jobs, with different insurers, on different forms.

| Document | What it actually does | Works for | Does NOT work for |

|---|---|---|---|

| Superbill / Itemized Medical Bill | Lets your insurer review an out-of-network medical visit or service. Must contain CPT codes, ICD-10 codes, provider NPI and Tax ID, date of service, and itemized charges. | Out-of-network telehealth visits, in-person weight-loss clinic visits, obesity-medicine specialist consults | Medications filled by a pharmacy |

| Itemized Receipt | Proof of payment. Lists what you bought, when, and what you paid. | HSA, FSA, HRA substantiation; tax records; provider support disputes | Commercial out-of-network medical claims (per insurers like Cigna, a receipt alone is insufficient) |

| Pharmacy Claim Form | Submits an out-of-network or direct-member-reimbursement request specifically for a prescription drug. Cigna publishes a separate pharmacy claim form distinct from its medical claim form. | Brand-name GLP-1 bought outside your in-network pharmacy; out-of-network compound prescription claims where allowed | A visit, program, or consult |

| Letter of Medical Necessity (LMN) | A short letter from your prescribing clinician stating your diagnosis (with ICD-10 code) and confirming the medication is medically necessary to treat it — not for general wellness. | HSA/FSA substantiation; appeals after a denial; Section 125 plans; some OON appeals | Replacing a superbill or pharmacy claim (LMN supports these, it doesn’t substitute) |

| Explanation of Benefits (EOB) | The insurer’s after-the-fact summary of how your claim was processed — allowed, paid, denied, and why. | Understanding a denial; triggering an appeal | Paying from (it isn’t a bill) |

| Prior Authorization Packet | Pre-coverage request submitted by your prescriber to the insurer before you get the medication. Contains clinical rationale, BMI, prior therapies tried, comorbidities. | Getting brand-name Wegovy, Zepbound, Ozempic, or Mounjaro covered under your pharmacy benefit | Post-payment reimbursement |

Primary sources: Cigna’s member medical claim form; Cigna’s pharmacy claim form; Cigna’s member guide on claims and EOBs; Cigna’s compounded medications coverage policy; IRS Publication 502; FSAFEDS weight-loss expense guidance. Your plan’s specific language may differ — always pull your own claim forms from your insurer’s member portal before filing.

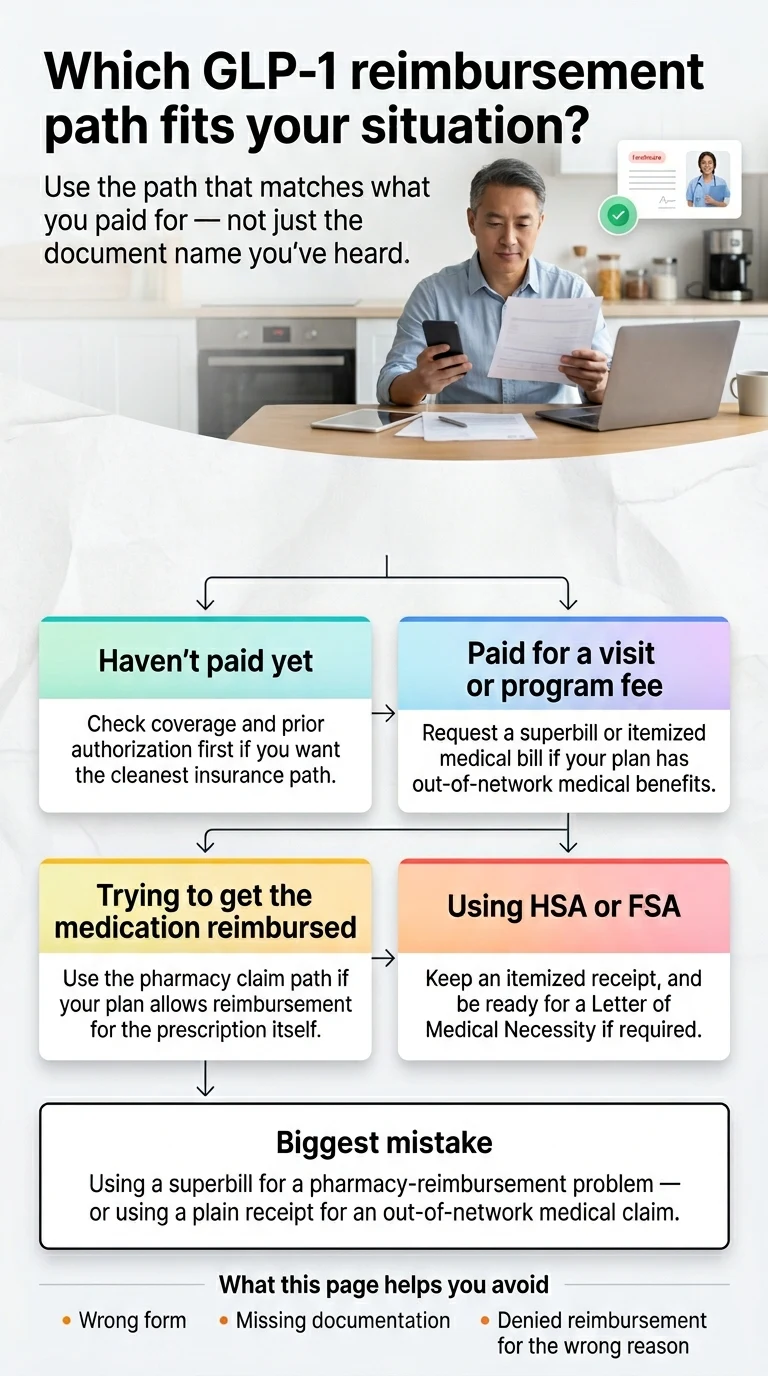

The Three Mix-Ups That Cost People Money

- “I sent them the receipt — why did they deny it?” Because for an out-of-network medical service, most commercial insurers want an itemized bill with CPT and ICD-10 codes, not a payment receipt. Request a coded superbill and resubmit.

- “I sent a superbill for my medication — why did they deny it?” Because a superbill covers medical visits, not pharmacy-dispensed drugs. For medication reimbursement, you typically need your insurer’s pharmacy claim form (sometimes called “direct member reimbursement”) with your pharmacy receipt attached.

- “My doctor won’t write an LMN — now what?” An LMN isn’t a superbill substitute; you often need both. If your prescriber won’t write one, get it from your primary care doctor, or switch to a provider that writes them on request.

Which Path Fits Your Exact GLP-1 Situation?

If You Haven’t Paid Yet and Want the Cleanest Insurer-Facing Path

Verdict: get coverage checked first — before you pay cash for anything.

Ro’s free GLP-1 Insurance Checker calls your insurance plan on your behalf and returns a personalized report showing whether your plan covers Wegovy, Zepbound, Ozempic, or Foundayo, whether prior authorization is required, and what your estimated out-of-pocket cost would be. If coverage is confirmed, Ro’s Body program handles the prior authorization and pharmacy coordination end-to-end. This is the path we recommend if you have commercial insurance and you’d rather not gamble on post-payment reimbursement.

Free · No prescription required to check

Check GLP-1 coverage free on Ro

Check GLP-1 coverage free on Ro → (sponsored affiliate link, opens in a new tab)If You Already Paid an Out-of-Network Telehealth Provider for Visits or Program Fees

Verdict: request a coded itemized medical bill from the provider, then file a medical claim with your insurer.

You’ll need the superbill (with the fields we list below), a copy of your insurance card, and your insurer’s medical claim form (download from your member portal — Cigna, Aetna, UnitedHealthcare, and most BCBS plans publish theirs online). Cigna’s medical claim form requires claims be received within 180 days of the date of service (365 for foreign claims); other insurers and states vary. Confirm your plan’s deadline. See the step-by-step submission guide below, and use the support request template to get the right document from your provider.

If the Money You Want Back Is the Medication Itself

Verdict: verify whether your plan has a direct-member-reimbursement or out-of-network pharmacy benefit, and if so, request a pharmacy claim form — not a superbill.

For compounded GLP-1s specifically, commercial insurance reimbursement is rare in practice, even though some plans do publish a compounded-medications coverage policy with specific medical-necessity criteria. If you’re in the compounded lane, HSA/FSA is usually the faster, cleaner path.

If Your FSA or HSA Is Involved at All

Verdict: you don’t need a superbill — you need an itemized receipt and, for weight-loss expenses, usually a Letter of Medical Necessity.

FSAFEDS, the federal-employee FSA administrator, is explicit that weight-loss programs and medications may require a Letter of Medical Necessity plus a detailed receipt. Commercial FSA administrators follow similar logic. HSAs typically don’t require an LMN at the point of purchase but you should still keep one on file in case of an IRS audit. IRS Publication 502 treats weight-loss treatment as a qualified medical expense when used to treat a diagnosed disease such as obesity, hypertension, heart disease, or type 2 diabetes.

When Will a GLP-1 Superbill Actually Help — and When Won’t It?

A superbill helps when two things are true: your plan has out-of-network benefits for the type of service you received, and the bill is complete enough for the insurer to process a claim. A superbill does not create coverage that doesn’t exist.

It Usually Helps If You Have a PPO, POS, or Indemnity Plan

Preferred Provider Organization (PPO), Point of Service (POS), and traditional indemnity plans typically include out-of-network benefits — meaning your insurer will pay a portion of the cost when you see a provider outside their network. Those plans are the ones where a superbill actually moves money.

It Usually Doesn’t Help If You Have an HMO or EPO Plan

Health Maintenance Organization (HMO) and Exclusive Provider Organization (EPO) plans generally cover out-of-network care only in emergencies. Cigna’s member guide confirms this pattern explicitly for most HMO and EPO products. If you have an HMO or EPO and you paid a cash-pay telehealth GLP-1 provider, a superbill is unlikely to reimburse you — the service wasn’t in the covered network in the first place.

The “Allowed Amount” Problem: Why You Rarely Get 100% Back

Even on a PPO, out-of-network reimbursement is based on your insurer’s allowed amount, not on what you actually paid. Aetna’s own published example walks through the math: an out-of-network doctor bills $825, Aetna’s allowed amount is $400, the member pays a $100 deductible, the plan pays 60% of the remaining $300 ($180), the member pays the other 40% ($120), plus the $425 difference between the provider’s charge and the allowed amount (balance billing). Total member cost: $645 out of $825 billed.

Applied to GLP-1 telehealth, even a successful out-of-network claim often nets you a fraction of what you paid — not the full amount back. That’s still money. But it’s not full recovery. Plan accordingly.

The Honest Admission

A superbill does not force a non-covered GLP-1 to become covered.

If your plan excludes weight-loss drugs, or if compounded-drug coverage requires medical-necessity criteria your case doesn’t meet, no paperwork fixes that. For most cash-pay compounded GLP-1 patients, commercial reimbursement of the drug is a long shot in practice. The realistic reimbursement path is almost always HSA/FSA — and that’s not a downgrade. It’s just the right tool for the job.

If you’re in the HSA/FSA lane and want a provider that makes this as frictionless as possible:

- Embody is a cash-pay program offering compounded semaglutide and tirzepatide — weekly injections or a needle-free GLP-1 gum — advertised as HSA/FSA eligible with no membership fee. Its compounded options are not FDA-approved finished drugs.

- SHED is the strongest fit for Foundayo (orforglipron) and oral Wegovy searches, publicly marketed as FSA eligible with a 100% online visit and checkout.

Cash-pay compounded · HSA/FSA

Compounded semaglutide or tirzepatide — weekly injection or needle-free GLP-1 gum. From $99 first month. No membership fee. Not FDA-approved finished drugs.

See Embody pricing → (sponsored affiliate link, opens in a new tab)Oral & needle-free GLP-1 · FSA eligible

Foundayo (orforglipron), oral Wegovy, and needle-free options. Fully online visit and checkout.

See SHED’s oral GLP-1 options → (sponsored affiliate link, opens in a new tab)What Has to Be on the Bill: The Fields That Make or Break a GLP-1 Claim

If you’re going to submit a superbill for out-of-network medical-visit reimbursement, these are the fields your insurer needs. Miss one and your claim bounces before a human adjuster ever looks at it.

The Required Fields Checklist

- Patient name and insurance member ID — the person who received the service, matched to the policy.

- Date(s) of service — the actual day each service happened, not the date of payment.

- Procedure code (CPT) or type-of-service description — what the provider did, in insurer-recognized code or language form.

- Charge for each service — itemized, not lumped into a “subscription” line.

- Provider name, credentials (MD, DO, NP, PA), National Provider Identifier (NPI), and address — so the insurer can verify licensure.

- Provider Tax ID (TIN/EIN) and diagnosis code (ICD-10) — required for the claim to process through the insurer’s billing system.

Why “Subscription” Invoices Trip People Up

The most common failure mode: cash-pay GLP-1 telehealth invoices that show only a product line (“Monthly Program — $349”) with no CPT code, no ICD-10 diagnosis, no provider NPI. Those invoices work fine for HSA/FSA with most administrators. They won’t work for a commercial out-of-network medical claim.

The Support Request Template — Copy, Paste, Send

Send this through your provider’s support portal or email:

Hi [Provider Support], I'm submitting an out-of-network reimbursement claim to my insurance plan and I need a coded itemized medical bill (superbill) for the services I've already paid for on [dates]. Please include the following on the bill: 1. My full name and your internal patient ID 2. Date(s) of service 3. CPT code or type-of-service description for each billable encounter 4. Itemized charge for each service 5. Rendering provider's name, credentials, and NPI (National Provider Identifier) 6. Your business name, address, and Tax ID (TIN/EIN) 7. ICD-10 diagnosis code associated with the service (for example, E66.01 if treating obesity due to excess calories, or E11.9 if treating type 2 diabetes without complications) If you don't issue coded superbills, please let me know what document you can provide and whether a Letter of Medical Necessity is available on request. Thank you.

If the response is “we only issue an itemized receipt, not a superbill,” that’s your signal: commercial OON reimbursement of the visit isn’t on the table with this provider, and HSA/FSA is your path.

The Codes That Matter for a GLP-1 Superbill

This is the detail most “GLP-1 reimbursement” content skips. It also determines whether your claim can actually enter the insurer’s billing system.

CPT Codes You May See on a GLP-1 Visit

- 99202, 99203, 99204, 99205 — new patient evaluation and management (E/M) visits, office/outpatient

- 99212, 99213, 99214, 99215 — established patient E/M visits

- 99421, 99422, 99423 — online digital E/M services for established patients over a 7-day cumulative period (used by some asynchronous telehealth providers)

- 99401–99404 — preventive medicine counseling, individual

- G0447 — Medicare’s face-to-face obesity behavioral counseling code (15 minutes; Medicare only)

The correct code depends on the service actually performed, the patient’s established-vs-new status, and the time or complexity involved. The coding is the provider’s responsibility — your job is to confirm the superbill you receive has a code on it at all.

ICD-10 Codes Insurers Typically Expect for GLP-1

For weight management:

- E66.811 — obesity, class 1

- E66.812 — obesity, class 2

- E66.813 — obesity, class 3

- E66.01 — morbid (severe) obesity due to excess calories

- E66.9 — obesity, unspecified

- E66.3 — overweight

- Z68.xx — BMI Z-codes, required by most payers alongside the obesity diagnosis to document clinical severity (Z68.25–Z68.45 cover adult BMI ranges)

For type 2 diabetes (on-label for Ozempic, Mounjaro, Rybelsus):

- E11.9 — type 2 diabetes mellitus without complications

- E11.xx — type 2 diabetes with various complications

Supporting codes you may see:

- Z79.899 — long-term (current) use of other medications

- Comorbidities: hypertension (I10), hyperlipidemia (E78.5), obstructive sleep apnea (G47.33), metabolic dysfunction-associated steatohepatitis (K76.81)

The coding mismatch that triggers automatic denials

The most common single failure: a diagnosis code that doesn’t match the drug’s FDA-approved indication, without supporting comorbidities. Ozempic is FDA-approved for type 2 diabetes, not weight loss. If your provider coded an Ozempic claim with E66.01 (obesity) alone and your plan only covers Ozempic for type 2 diabetes (E11.x), the claim gets denied — not because the paperwork is wrong, but because the prescription is off-label. That’s why Wegovy and Zepbound exist as separately FDA-approved weight-loss versions of the same active ingredients.

Can the Medication Itself Be Reimbursed?

Sometimes. Sometimes not. It depends on whether the medication is brand-name or compounded and whether your plan has a direct-member-reimbursement or out-of-network pharmacy benefit.

Brand-Name GLP-1 From a Pharmacy

If your insurance plan covers Wegovy, Zepbound, Ozempic, Mounjaro, or Foundayo — meaning the drug is on your formulary and you meet the prior-authorization criteria — you don’t need a superbill. You need prior authorization, and the pharmacy bills your insurer directly.

If your insurance doesn’t cover the drug but you bought it cash at a retail pharmacy, you can submit a pharmacy reimbursement claim if your plan allows direct member reimbursement. Use the insurer’s pharmacy claim form, not a medical superbill. Success varies by plan.

Note: in 2026, some commercial plans narrowed weight-loss GLP-1 coverage — for example, Mass General Brigham Health Plan publicly announced that starting January 1, 2026, fully insured commercial members would no longer have coverage for GLP-1 medications for weight management, while diabetes coverage continued. Always confirm your specific plan.

Compounded GLP-1 and Why This Is Much Harder

Compounded semaglutide or tirzepatide is prepared by a licensed compounding pharmacy (503A or 503B) under a clinician’s prescription. These are not FDA-approved finished drugs. The FDA does not review compounded GLP-1 products for safety, effectiveness, or quality before they reach you, and has issued warning letters and public advisories about unapproved compounded GLP-1 products with misleading labeling.

Coverage in practice: Cigna’s compounded medications coverage policy says compounded products are typically considered under the pharmacy benefit when specific medical-necessity criteria are met — which is narrower than it sounds. For compounded GLP-1 used for obesity, real-world approval is rare.

The Honest Conclusion for Compounded Patients

We won’t promise you’ll get commercial insurance reimbursement for a compounded GLP-1. You probably won’t, regardless of paperwork. What you can do:

- Use HSA or FSA dollars when the expense qualifies as medical care. IRS Publication 502 treats prescribed medicines and weight-loss treatment for a diagnosed disease as qualified medical expenses; your administrator may still request an LMN for weight-loss purposes.

- Keep receipts for a possible Schedule A medical-expense deduction if you itemize and your total unreimbursed medical spending exceeds 7.5% of adjusted gross income in a tax year.

- Request an LMN from your prescribing provider so your HSA/FSA administrator has it on file.

How to Submit Your GLP-1 Claim, Step by Step

Clean version for an out-of-network medical claim covering visit or program fees. If you’re going the HSA/FSA route, the workflow below is different — jump to the HSA/FSA section.

Step 1 — Confirm Your Plan Has an Out-of-Network Medical Benefit

Call the member services number on the back of your insurance card. Ask three questions:

- “Do I have out-of-network benefits for telehealth or outpatient professional services?”

- “What is my out-of-network deductible, and how much have I met year-to-date?”

- “What is your claim-filing deadline for out-of-network services?”

Write down the rep’s name, the date, and the reference number for the call.

Step 2 — Request the Correct Document From Your Provider

Send the support request template above. Specify that you need a coded itemized medical bill with the required fields. Give the provider 5–10 business days to respond.

Step 3 — Get a Letter of Medical Necessity on File

Even if your insurer doesn’t require one for the initial submission, an LMN helps if the claim is denied and you appeal. Your prescribing provider should be able to produce a short letter (2–5 sentences) naming your diagnosis with its ICD-10 code and confirming the GLP-1 is medically necessary.

Step 4 — Download the Right Claim Form

Log into your insurer’s member portal and search for “member reimbursement claim form” or “out-of-network claim form.” Medical claims and pharmacy claims are separate forms at most major insurers — use the medical form for visit/program fees and the pharmacy form for drug-reimbursement attempts.

Step 5 — Submit and Keep Copies

Submit per your insurer’s instructions (usually upload through the member portal or mail to the address on the form). Keep a PDF of the superbill, the LMN, the claim form, and any confirmation emails or tracking numbers. Typical processing: 2–6 weeks.

Step 6 — Read Your EOB Carefully

When your EOB arrives, look for three numbers: the allowed amount, the plan paid amount, and your member responsibility. If the allowed amount is much lower than what you paid, that’s balance billing territory. If the claim is denied, the denial reason code on the EOB is your starting point for an appeal.

What to Do If Your GLP-1 Claim Is Denied

Denial isn’t one thing. The fix depends on which of four types you’re looking at.

Denial Type 1: Documentation Incomplete

Most common cause: you sent a receipt instead of an itemized bill, or a required field was missing. Request a complete superbill and resubmit within your insurer’s appeal window.

Denial Type 2: Service Not Covered Under Your Plan

Most frustrating and most common for GLP-1 weight-loss services. Your plan excludes the benefit category. Appeal is possible, success rates are low. If the denial language says “obesity treatment not covered” or “weight management services excluded,” realistic options are: (a) a peer-to-peer clinical review between your prescriber and the insurer’s medical director; (b) appealing with evidence of a covered comorbidity; or (c) pivoting to HSA/FSA.

Denial Type 3: Prior Authorization Required

You tried to bypass prior auth by going out-of-network. Most insurers still require prior auth for covered services regardless of network status. If the service genuinely required prior auth, you’d need to submit a retroactive authorization request — possible but often rejected.

Denial Type 4: Coding Issue

CPT or ICD-10 codes don’t align with your plan’s coverage policy. Usually fixable. Contact the provider, explain the denial reason, request a corrected superbill with the appropriate codes, and resubmit.

The Appeal Packet Checklist

If you’re going to formally appeal a denial, include:

- The denial letter or EOB

- The original itemized superbill

- A Letter of Medical Necessity from your prescriber

- A written appeal letter explaining why the denial should be reversed, citing your plan’s specific coverage language

- Any clinical evidence supporting medical necessity (BMI history, comorbidity documentation, prior weight-loss attempts)

- For compounded products, relevant IRS Publication 502 references where medical necessity is the issue

Under the Affordable Care Act, commercial plans must provide at least one internal appeal and, for certain claim types, access to external independent review. Most plans require the internal appeal within 180 days of the denial — confirm your specific plan.

HSA, FSA, and HRA: The Path Most Compounded GLP-1 Patients Should Actually Use

For most people paying cash for a compounded GLP-1 program, HSA, FSA, and HRA reimbursement is a cleaner path than any commercial insurance claim. It’s a different workflow with lighter documentation — and it doesn’t require a superbill.

The IRS Rule You’re Actually Operating Under

IRS Publication 502 defines qualified medical expenses as amounts paid for the diagnosis, cure, mitigation, treatment, or prevention of disease. Prescribed medicines are covered. Weight-loss programs and medications qualify when they treat a specific disease diagnosed by a physician — examples in the publication include obesity, hypertension, and heart disease. General wellness, cosmetic weight loss, and non-prescribed supplements don’t qualify. FSAFEDS adds that weight-loss program expenses may require a Letter of Medical Necessity plus a detailed receipt.

What You Need in Your File

- Valid prescription from a licensed provider, in your name

- Itemized receipt showing the medication name, dose, date, and amount paid (most telehealth provider receipts include this)

- Letter of Medical Necessity — not always required at purchase but recommended, and often required by FSA administrators for weight-loss expenses specifically

The Math Most People Don’t Run

Example: $299/month compounded tirzepatide paid with pre-tax HSA/FSA dollars

$3,588/year program cost. At a combined marginal rate of roughly 37.65% (24% federal + 6% state + 7.65% FICA), paying with pre-tax dollars saves approximately $1,350/year — dropping your effective monthly cost from $299 to roughly $187. That’s real money, recovered without filing a single insurance claim.

Tax brackets and effective rates vary; this is an illustrative calculation. Run your own numbers with your tax situation.

Which Providers Make HSA/FSA Frictionless

Publicly verified HSA/FSA-friendly positioning:

- Embody — cash-pay compounded semaglutide and tirzepatide (injection or needle-free gum), advertised HSA/FSA eligible with no membership fee

- SHED — publicly markets FSA eligibility with a 100% online visit and checkout

- SkinnyRx — publicly markets HSA/FSA acceptance with receipt

- Hims / Hers — receipts available from the orders tab for reimbursement submission; HSA/FSA card payments may require additional provider-side documentation

The Superbill Readiness Matrix: What Each Major GLP-1 Provider Publicly Says

Built from each provider’s public help center, FAQ, and stated policies as of April 16, 2026. Where a provider’s public documentation was unclear on a specific point, we’ve marked it “unclear” rather than guess.

| Provider | Document issued | Insurance handling | HSA/FSA supported | Best reimbursement fit |

|---|---|---|---|---|

| Ro | Detailed receipt; separate free GLP-1 Insurance Checker | Handles insurance for brand-name GLP-1s (Wegovy, Zepbound, Foundayo); manages prior authorization | Ro’s FAQ says HSA/FSA cards aren’t accepted at checkout; submit receipts for reimbursement | Insurance-first, brand-name path |

| Hims / Hers | Itemized receipt from orders tab | Self-pay; March 2026 collaboration with Novo Nordisk added branded Wegovy access | Receipt submission for HSA/FSA reimbursement; card payments may require additional documentation | Mainstream brand + reimbursement submission |

| MEDVi *note below | Itemized receipt | Cash-pay; may reimburse branded options via insurance per MEDVi | Publicly markets “HSA/FSA approved” | Broad self-pay menu with HSA/FSA positioning |

| Embody | Itemized receipt | Cash-pay; no insurance; no membership fee | Advertises HSA/FSA eligibility for compounded semaglutide and tirzepatide (injection or needle-free gum) — confirm with plan | Low-cost cash-pay compounded with HSA/FSA positioning |

| SHED | Itemized receipt | Self-pay; 100% online visit and checkout | Publicly marketed FSA eligible | Foundayo, oral GLP-1, needle-free intent |

| SkinnyRx | Itemized receipt | Self-pay | HSA/FSA accepted with receipt | Aggressive-value compounded |

| Sesame | Booking confirmation/receipt by default; itemized bill available from support on request | Subscription is self-pay; insurance accepted for weight-loss medications | Publicly supports HSA/FSA documentation help | Transparent brand/self-pay hybrid |

| Fridays | Itemized receipt | Cash-pay only for compounded | Publicly accepts HSA/FSA cards for compounded | Compounded cash-pay with HSA/FSA at checkout |

| TrimRx | Itemized receipt | Cash-pay | HSA/FSA typically accepted with receipt | Lean compounded without membership layers |

| Yucca Health | Yucca’s public FAQ says many patients use HSA/FSA funds but that Yucca does not provide itemized receipts or letters of medical necessity. | Cash-pay; async model | Yes for direct payment; documentation limitations noted — confirm current policy before counting on reimbursement | Lowest-friction purchase, higher-friction reimbursement paperwork |

| In-person obesity medicine clinic | True superbill with CPT + ICD-10 + NPI + Tax ID | May file insurance directly or provide superbill for OON | Works for HSA/FSA | Clearest lane for commercial OON superbill workflows |

Material note on MEDVi

On February 20, 2026, the FDA issued a warning letter to MEDVi LLC regarding false or misleading claims about compounded semaglutide and tirzepatide products. MEDVi remains a large cash-pay telehealth platform with published HSA/FSA positioning; if the FDA warning is a deal-breaker for you, Embody, SHED, and Fridays (sponsored affiliate link, opens in a new tab) cover similar use cases with different regulatory histories. Check the current status on FDA’s warning-letter database and MEDVi’s own response before deciding.

How to Read This Matrix

- If you need a true superbill (coded itemized bill for commercial OON reimbursement of visit fees), the honest answer is that most cash-pay compounded GLP-1 telehealth providers don’t issue one in the format insurers need — they issue itemized receipts without CPT codes. The lanes where a superbill-style workflow is most likely to work: visit-based platforms like Sesame (sponsored affiliate link, opens in a new tab) (with an itemized bill requested from support), insurance-coordinating platforms like Ro, and in-person clinics.

- If you need HSA/FSA documentation, almost every provider on this matrix works — itemized receipt plus an LMN on file is sufficient for nearly all administrators. The outlier is Yucca Health, which publicly says it doesn’t provide itemized receipts or LMNs.

- If you need insurance coverage of a brand-name GLP-1, Ro is the clearest path because of its free Insurance Checker and prior-auth coordination. Hims and Hers added branded Wegovy access through the March 2026 Novo Nordisk collaboration.

Picking a GLP-1 Provider Whose Paperwork Matches Your Reimbursement Plan

If you haven’t chosen a provider yet and reimbursement is a major factor, your provider choice matters almost as much as your plan’s benefits.

If You Want Commercial Insurance Coverage for a Brand-Name GLP-1

Pick Ro. Ro’s free GLP-1 Insurance Checker does the coverage lookup for you — calls your plan, confirms whether Wegovy, Zepbound, Ozempic, or Foundayo is covered, identifies prior-auth requirements, and returns a personalized report. If coverage is confirmed, Ro’s Body program manages prior authorization and pharmacy coordination end-to-end. Ro carries Zepbound (tirzepatide) and Foundayo (orforglipron).

Note: Ro does not accept HSA/FSA cards directly at checkout. If that’s your priority, Fridays (sponsored affiliate link, opens in a new tab) or Embody fits better. But because Ro skips the HSA/FSA checkout integration, their team’s attention goes into the actual insurance work — which is exactly what you want if coverage is your real goal.

Insurance-first path · Ro Body

Ro Body membership starts at $39 for the first month, then as low as $74/month with annual prepay or $149/month month-to-month. Medication cost is separate.

Check GLP-1 coverage free on Ro → (sponsored affiliate link, opens in a new tab)If You Want a Low-Cost Cash-Pay Compounded Path With HSA/FSA Positioning

Consider Embody. Embody is a cash-pay program that ships compounded semaglutide and tirzepatide — as weekly injections or a needle-free GLP-1 gum — and advertises HSA/FSA eligibility (confirm it works with your plan). Pricing starts at $99 for your first month of compounded semaglutide injection, then $299/month for refills; other forms run $349–$449/month. There is no separate membership fee. Embody does not sell brand-name Wegovy, Zepbound, Ozempic, or Mounjaro, and its compounded options are not FDA-approved finished drugs. Check availability in your state during intake.

Cash-pay compounded · injection or gum · HSA/FSA

Embody: compounded semaglutide or tirzepatide. Weekly injection or needle-free GLP-1 gum. From $99 first month. No membership fee. HSA/FSA eligible — confirm with your plan.

See Embody pricing → (sponsored affiliate link, opens in a new tab)Embody’s shipped compounded GLP-1 options are not FDA-approved finished drugs. A licensed provider determines whether treatment is medically appropriate. Prices, pharmacy availability, shipping timelines, and state eligibility can change and should be confirmed during intake. Last verified June 11, 2026.

If You Want Foundayo or Oral GLP-1 Access Specifically

Pick SHED. SHED leads on Foundayo (orforglipron), oral Wegovy, and needle-free GLP-1 intent. Publicly marketed FSA eligible with a fully online visit and checkout flow. If your search intent is “I want the pill, not the shot,” SHED is the specialist.

Oral GLP-1 · needle-free · FSA eligible

See SHED’s oral GLP-1 options → (sponsored affiliate link, opens in a new tab)If You’re Not Sure Which Lane Fits You

Take the quiz. We built a 60-second matching tool that asks five questions about your budget, insurance situation, medication format, and reimbursement priorities, then routes you to the provider that fits. Free, no email required to see your result.

Free · 60 seconds · No email required

Five questions about your budget, insurance situation, and medication preference — and we match you to the provider that fits.

Take the free 60-second GLP-1 path quiz →Risks, Limitations, and Tradeoffs Before You Pay Cash

No Superbill Guarantees Reimbursement

A perfectly executed superbill is necessary, not sufficient. If your plan excludes the service, coverage doesn’t exist. Confirm your out-of-network benefits before you pay cash, not after.

Balance Billing Is Real

Reimbursement is based on your insurer’s allowed amount, not what you paid. The gap between the provider’s charge and the allowed amount is your balance bill — and on out-of-network claims, that gap is often substantial. Aetna’s own example shows a member paying $645 out of $825 billed even after the plan pays its share.

Timing Matters

Reimbursement processing typically takes 2–6 weeks once your claim is complete. That doesn’t help cash flow now. If cash flow is tight, a lower-priced provider ($149–$199/month) is often a better move than a higher-priced provider with reimbursement on the back end.

Compounded GLP-1 Carries Regulatory Considerations

Compounded semaglutide and tirzepatide are not FDA-approved finished drugs. The FDA does not review compounded products for safety, effectiveness, or quality before they reach patients. FDA has publicly flagged concerns about unapproved compounded GLP-1 products, including products with misleading labeling, and has issued warning letters to specific companies. Legitimate, LegitScript-certified providers using state-licensed 503A or 503B compounding pharmacies are a different category than unlicensed sellers — but the regulatory category is not the same as an FDA-approved brand-name drug, and your reimbursement options are narrower as a result.

Privacy of Diagnosis Codes

Your superbill includes your ICD-10 diagnosis code. If you share insurance with someone else (a spouse’s plan, a parent’s plan), they may see this information on shared EOBs. Factor that into your filing decisions.

When Paying Cash Is Still the Right Call

For millions of people, cash-pay GLP-1 through a legitimate telehealth provider at $150–$350/month is the fastest, cleanest path to treatment — with HSA/FSA reducing the effective cost meaningfully, and without the months of prior-auth battles that insured paths sometimes require. Reimbursement math should inform your choice. It shouldn’t paralyze it.

Frequently Asked Questions

What is a GLP-1 superbill?

A GLP-1 superbill is a coded, itemized medical bill from an out-of-network provider containing CPT procedure codes, ICD-10 diagnosis codes, provider credentials and Tax ID, and itemized charges — the data your insurance needs to process an out-of-network reimbursement claim for a medical visit or service. It is for medical services, not for medications dispensed by a pharmacy.

Does a GLP-1 superbill help with the medication or just the visit?

Primarily the visit. A superbill covers out-of-network medical services — the consult, the program fee, the provider visit. For the medication itself, you generally need a pharmacy claim form or prior authorization, not a superbill. Brand-name GLP-1s filled at a pharmacy go through your pharmacy benefit. Compounded GLP-1s are rarely reimbursed by commercial insurance in practice, though HSA/FSA covers many of them when the expense qualifies as medical care.

Does a receipt count as a superbill?

No. A receipt shows what you paid; a superbill shows what clinical service was provided (with CPT codes) and for what diagnosis (with ICD-10 codes). Most commercial insurers explicitly require an itemized bill, not a receipt, for an out-of-network medical claim. A receipt is usually sufficient for HSA/FSA reimbursement but not for commercial insurance claims.

What has to be on a GLP-1 superbill?

Patient name and member ID; date(s) of service; CPT procedure code or type-of-service description; itemized charges; provider name, credentials, NPI, and address; provider Tax ID; and ICD-10 diagnosis code. Missing any one of these usually causes an automatic return before a human adjuster reviews the claim.

Can I get reimbursed for semaglutide or tirzepatide after paying cash?

Brand-name semaglutide (Ozempic, Wegovy) or tirzepatide (Mounjaro, Zepbound) purchased cash at a pharmacy may qualify for pharmacy reimbursement if your plan allows direct member reimbursement — file with your insurer's pharmacy claim form. Compounded semaglutide or tirzepatide from a telehealth provider is rarely reimbursed by commercial insurance in practice. HSA/FSA reimbursement is a separate documentation path that works for many patients when the expense qualifies as medical care.

Do I need a pharmacy claim form instead of a superbill?

Yes, if the money you want back is for the medication itself rather than a medical visit. Medical claims and pharmacy claims are separate workflows at most insurers (Cigna publishes separate medical and pharmacy claim forms, for example). Using the wrong form delays or kills the claim.

Do I need a Letter of Medical Necessity for GLP-1 reimbursement?

Often, yes — particularly for HSA/FSA reimbursement of weight-loss medications and for insurance appeals after a denial. An LMN is a short letter from your prescribing provider naming your diagnosis with its ICD-10 code and confirming the medication is medically necessary. It's not always required at purchase but is recommended to have on file.

Can I use HSA or FSA for a GLP-1 instead of insurance reimbursement?

Often, yes — when the expense qualifies as medical care. IRS Publication 502 treats prescribed medicines and weight-loss treatment as qualified medical expenses when used to treat a diagnosed disease such as obesity, hypertension, heart disease, or type 2 diabetes. Administrator documentation rules still apply — FSAFEDS and many commercial FSA administrators require a Letter of Medical Necessity plus a detailed receipt for weight-loss expenses.

Why did my GLP-1 claim get denied?

Four common reasons: (1) documentation incomplete — receipt instead of itemized bill, or a required field was missing; (2) the service or drug isn't covered by your plan — weight-loss exclusion or compounded-drug limitation; (3) prior authorization was required but not obtained; (4) coding mismatch — diagnosis code doesn't support the drug's FDA-approved indication. The fix depends on which bucket you're in.

What's the cheapest GLP-1 path if reimbursement is what I care about?

The cheapest net-cost path for most cash-pay patients is a lower-priced compounded provider ($149–$199/month) paid with HSA or FSA dollars — the pre-tax benefit effectively reduces your cost by 20–37% depending on your marginal tax rate. Trying to reimburse a more expensive provider through commercial insurance rarely beats picking a cheaper provider upfront. If you have a covered comorbidity and solid PPO coverage, an insurance-first brand-name path through Ro can beat cash-pay math — but confirm coverage before paying.

How long do insurance companies take to reimburse a superbill?

Typically 2–6 weeks for a clean claim. Missing documentation or coding issues can extend that to 2–3 months. Filing deadlines vary — Cigna uses 180 days for most claims on its member claim form (365 for foreign claims); your plan's deadline may differ.

Can Medicare reimburse a GLP-1 superbill?

Traditional Medicare does not cover GLP-1 medications for weight loss under federal statute. Medicare does cover GLP-1s for type 2 diabetes under Part D. The Medicare GLP-1 Bridge runs July 1, 2026 through December 31, 2027 (18 months) as a coverage pathway for eligible Part D beneficiaries at $50/month — covering Wegovy, Zepbound KwikPen, and Foundayo. BALANCE will not launch for Medicare Part D in 2027. Medicare Advantage (Part C) plan policies may differ.

Can I claim GLP-1 costs on my tax return?

Potentially. Qualified unreimbursed medical expenses above 7.5% of adjusted gross income are deductible on Schedule A if you itemize. That's a deduction, not a reimbursement — it reduces taxable income, not your cash outlay. For most taxpayers who take the standard deduction, this doesn't move the needle; for those who itemize with high medical costs, it can.

What do I do if my telehealth provider won't give me a superbill?

Two options. One: accept that this provider is in the HSA/FSA lane and use that pathway — often the better deal anyway for compounded. Two: switch to a visit-based provider (Sesame with an itemized bill requested from support) or an insurance-coordinating provider (Ro, Hims for branded Wegovy) whose documentation model supports what you need.

Still not sure which GLP-1 program is right for you?

Take the free 60-second matching quiz. Five questions about your budget, insurance situation, medication preference, and reimbursement priorities — and we match you to the provider that actually fits. No email required to see your result.

Take the free 60-second matching quiz →What We Actually Verified

Primary-source documents we consulted for this guide:

- Cigna member medical claim form — itemized bill required, not receipt; required fields; 180-day filing (365 for foreign claims)

- Cigna pharmacy claim form — separate from medical claims; handles out-of-network and compound prescription pathways

- Cigna member guide on claims and EOBs — EOB is not a bill; HMO/EPO out-of-network limits

- Cigna compounded medications coverage policy — medical-necessity criteria for compounded products under pharmacy benefit

- Aetna’s out-of-network cost example — allowed-amount and balance-billing mechanics ($825 / $400 / $180 / $645 example)

- IRS Publication 502 — qualified medical expense rules; weight-loss treatment for a diagnosed disease

- FSAFEDS weight-loss expense guidance — Letter of Medical Necessity and detailed receipt requirements

- FDA public guidance on compounded GLP-1 products — regulatory status and safety communications

- FDA warning letter to MEDVi LLC (February 20, 2026) — false or misleading claims regarding compounded semaglutide and tirzepatide

- CMS Medicare GLP-1 Bridge FAQ — July 1, 2026 – December 31, 2027 (18-month program); BALANCE not launching Medicare Part D 2027

- Mass General Brigham Health Plan 2026 coverage update — example of a specific 2026 commercial plan narrowing GLP-1 weight-loss coverage

- Novo Nordisk Wegovy ICD-10 coding resource — commonly used codes for Wegovy billing

- ICD-10-CM obesity coding — E66.811 / E66.812 / E66.813 class codes, E66.01, E66.9, E66.3, Z68.xx BMI codes

Re-verified quarterly; policies change, and we update this page when they do. Last verified: .