How to Appeal a Zepbound Denial

7 steps that work — decode the reason, fix the right problem, and hit your deadline.

By The RX Index Editorial Team · Last verified April 3, 2026 · Affiliate disclosure

Your Zepbound denial is not final.

Appeals work — and they work more often than most people realize. In Medicare Advantage alone, over 80% of appealed prior-authorization denials were partially or fully overturned in 2024 (KFF). Insurers count on you not fighting back. Most people don’t. The ones who do, with the right documentation, frequently win.

But a generic appeal letter is often the wrong first move. The fastest path forward depends entirely on why you were denied — and there are five distinct denial types that each require a completely different response.

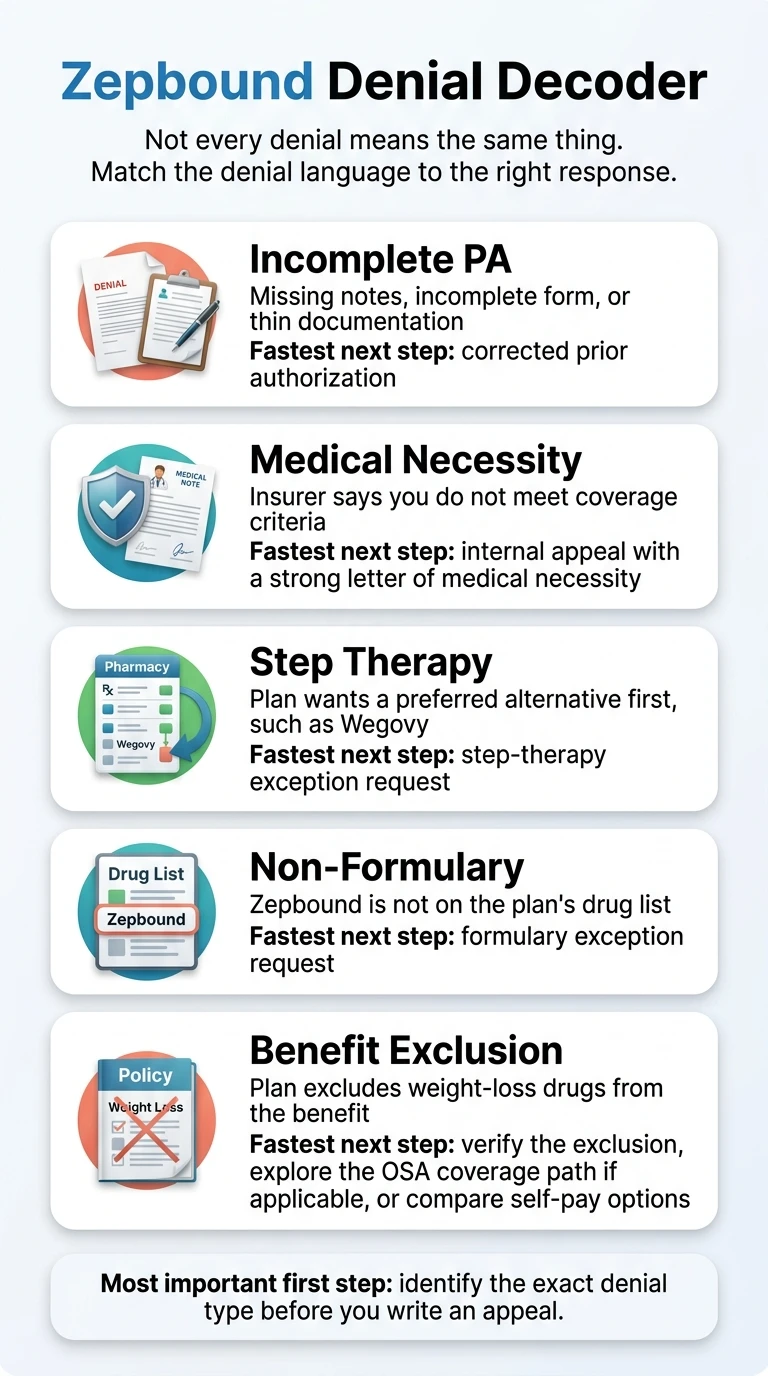

Why Was Your Zepbound Denied? (The 5 Denial Types That Change Everything)

Insurance companies deny Zepbound for five distinct reasons, and each one demands a completely different response. A common mistake is treating every denial the same way — filing a generic appeal when you actually need a corrected PA, or writing a medical-necessity letter when the real problem is a formulary exclusion. Different problem, different fix.

Read the exact wording on your denial letter. The language tells you which bucket you’re in.

| Your denial letter says… | Denial type | Fastest response | Difficulty |

|---|---|---|---|

| "Insufficient documentation," "incomplete," "missing clinical notes" | Incomplete PA | Corrected prior authorization with complete documentation | ★☆☆☆☆ Easiest |

| "Does not meet criteria," "not medically necessary" | Medical Necessity | Internal appeal with Letter of Medical Necessity | ★★★☆☆ Medium |

| "Must try preferred alternative first," "try Wegovy," "step therapy required" | Step Therapy | Step-therapy exception request | ★★★☆☆ Medium |

| "Not on formulary," "non-formulary medication" | Non-Formulary | Formulary exception request | ★★★★☆ Hard |

| "Excluded benefit," "plan does not cover weight-loss medications" | Plan Exclusion | OSA pathway, employer escalation, or alternative access | ★★★★★ Hardest |

What to Do in the First 24 Hours After a Zepbound Denial

The first day is for evidence collection, not emotional letter-writing. The strongest appeals start with the same foundation: the right documents, gathered before the deadline pressure kicks in.

The 7 Documents to Collect Immediately

Your denial letter

Save it. Photograph it. Highlight the exact denial reason and the appeal deadline. This is your roadmap.

The insurer's coverage criteria for Zepbound

Call the number on your denial letter and ask: "What are the specific clinical criteria for Zepbound coverage under my plan?" You have a right to this information.

Your BMI history

At least 6–12 months of documented readings showing BMI ≥30, or BMI ≥27 with weight-related comorbidities.

Comorbidity documentation

Records confirming conditions like type 2 diabetes, hypertension, obstructive sleep apnea, PCOS, NAFLD, cardiovascular disease, or prediabetes.

Prior weight-loss attempt records

Documentation of previous diet programs, exercise regimens, behavioral counseling, and any other medications you've tried.

Recent lab work

A1C, lipid panel, blood pressure readings, liver function tests — whatever's relevant to your comorbidities.

Sleep study results (if you have them)

This can open an entirely different coverage pathway. More on that below.

What to Say When You Call Your Insurance Company

Copy this script exactly:

Script:

“I received a denial for Zepbound, reference number [your reference number]. I’d like to request the following:

- The specific clinical criteria your plan uses to evaluate Zepbound coverage

- Confirmation of whether this is a formulary issue or a benefit exclusion

- The deadline and submission method for filing an internal appeal

- My complete claim file for this denial”

Write down the representative’s name and the date and time of the call. Save everything.

When to Request Expedited Review

Should You Appeal, Resubmit a PA, or Request a Formulary Exception?

A full appeal is not always the right first move. Choosing the wrong path wastes time and can burn one of your limited appeal levels on a problem that had a simpler fix.

Resubmit a corrected prior authorization when:

Your denial says the paperwork was incomplete, missing, or lacked clinical notes. This is the fastest win — many "denials" are really just documentation gaps. Have your doctor resubmit with the full documentation packet, including a proactive Letter of Medical Necessity.

Request a formulary exception when:

Your denial says Zepbound is not on formulary (but doesn't say the benefit is excluded). Your doctor files explaining why Zepbound is medically necessary and why formulary alternatives aren't appropriate. This is a cleaner path than a generic appeal for non-formulary denials.

File an internal appeal when:

Your denial says "not medically necessary," "does not meet criteria," or upholds a previous decision despite complete documentation. This is the formal appeal process with legal protections, mandated timelines, and escalation rights.

Explore alternative paths when:

Your denial is a true benefit exclusion — your plan contract literally does not cover weight-loss medications. A medical-necessity appeal is fighting the wrong battle. Your best options are the FDA-approved OSA indication, employer/HR escalation, or direct self-pay through LillyDirect.

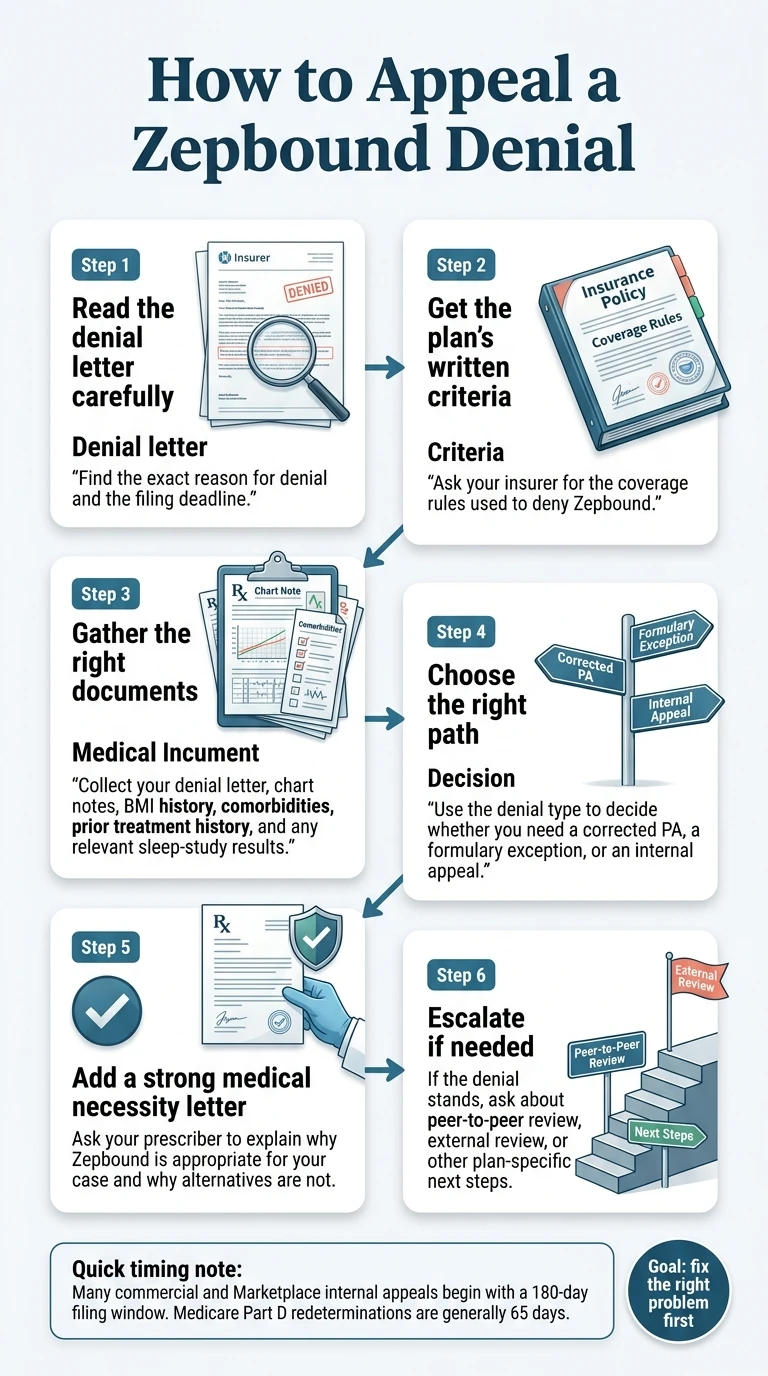

How to Appeal a Zepbound Denial Step by Step

This is the core appeal process for medical necessity and criteria-based denials — the most common and most winnable denial type. If your denial is an incomplete PA or non-formulary issue, use the corrected PA or formulary exception paths described above first.

Read Your Denial Letter Like a Checklist (Day 1)

Your denial letter is required to contain specific information. Look for:

Get the Insurer’s Written Criteria (Day 1–3)

You need to know their exact rules to beat them. Call and request the clinical policy document for Zepbound coverage. Most major insurers require some combination of: BMI ≥30 (or ≥27 with comorbidities), documented prior weight-loss attempts, specific comorbidity documentation, and sometimes a waiting period or lifestyle program requirement.

Once you have their criteria, you’re building your appeal to match it point-by-point. Not a generic letter — a targeted response to their specific rules.

Match Your Medical Facts to Their Criteria (Day 3–7)

Go through the insurer’s criteria line by line. For each requirement, identify where in your medical records the evidence exists. Common gaps and fixes:

BMI not documented recently

Schedule a visit specifically to record current BMI

Comorbidities mentioned but not coded

Ask your doctor to add formal ICD-10 diagnosis codes to your chart

Prior weight-loss attempts not in records

Write a personal statement listing every diet, exercise program, and medication you've tried, with approximate dates

No documented lifestyle modification

Document nutritionist visits, Weight Watchers, gym membership, calorie tracking apps — anything you've done

Get a Letter of Medical Necessity from Your Doctor (Day 3–10)

This letter is often the single most important document in your appeal. A strong Letter of Medical Necessity (LOMN) is not a form letter — it’s a clinical argument for why Zepbound is the right treatment for you specifically.

The 6 elements every winning LOMN includes:

Write Your Patient Statement (Day 5–10)

You can — and often should — file the internal appeal yourself. Under the ACA, you can initiate your own appeal or authorize someone to act for you. Your patient statement should be factual, specific, and brief:

Do not write an emotional plea. Write a factual case.

Submit and Document Everything (Day 7–14)

Your complete appeal packet should include:

Escalate If They Uphold the Denial

A first internal denial isn’t the end. You have more options.

Peer-to-peer review

Your prescribing physician speaks directly with the insurer's medical director. Often more effective than written appeals — physician-to-physician conversation in real time.

Second-level internal appeal

Some plans allow a second round of internal review. Check your denial letter or call to confirm.

External review

Under the ACA, you have the right to an independent review by a third party who doesn't work for your insurer. Their decision is legally binding on the insurer. Generally must be requested within 4 months of the final internal denial.

State insurance department complaint

Creates regulatory pressure and a paper trail. Some states have enacted laws specifically addressing algorithmic or AI-driven denial reviews.

Appeal Timeline at a Glance

| Step | Timeline | Who Does It |

|---|---|---|

| Read denial letter, note deadline | Day 1 | You |

| Request insurer criteria | Day 1–3 | You |

| Gather documentation | Day 1–7 | You + Doctor |

| Get Letter of Medical Necessity | Day 3–10 | Doctor (you provide template) |

| File internal appeal | Day 7–14 | You or Doctor |

| Peer-to-peer review (if needed) | Day 14–30 | Doctor |

| External review (if needed) | Day 30–90 | External reviewer |

Free insurance check · PA handling · Insurance concierge for commercially insured patients

How to Fight the Most Common Zepbound Denial Scenarios

Every denial pattern has a known counter-strategy. Find your scenario below.

"Not Medically Necessary"

Most commonThis is the most common denial — and the one with the strongest track record when appealed with complete documentation. It usually means your records didn't clearly establish that you meet the insurer's published criteria, not that you're truly ineligible. File an internal appeal with a complete documentation packet and a strong LOMN. Match your evidence to their criteria point-by-point. Include every comorbidity, every prior treatment attempt, and every relevant lab result. The insurer's medical reviewer is checking boxes — make sure every box is checked.

"Must Try Wegovy First" (Step Therapy)

Step therapyRequest a step-therapy exception. Your doctor documents why alternatives are not appropriate for your situation. Valid arguments: you previously tried a semaglutide-based medication and it was ineffective or caused intolerable side effects; you have a medical contraindication to semaglutide; your clinical profile specifically indicates Zepbound's dual GIP/GLP-1 mechanism; or you're already on Zepbound and responding well. Zepbound and Wegovy work through different mechanisms — your doctor's LOMN should make this distinction explicit.

"Not on Formulary"

Non-formularyRequest a formulary exception — a specific process, different from a medical necessity appeal, where your doctor explains why you need a non-formulary medication. This is increasingly common after CVS Caremark removed Zepbound from several major commercial formularies effective July 1, 2025. A formulary exception is not a long shot — plans build exception processes into their benefit design because they know the formulary can't cover every clinical situation.

"Incomplete or Missing Documentation"

Easiest fixThe easiest fix. Don't file a formal appeal — resubmit a complete prior authorization with all documentation, including a proactive LOMN. This is faster than the formal appeal process and doesn't use up one of your appeal levels.

"Benefit Exclusion / Plan Does Not Cover Weight-Loss Medications"

HardestThis is the hardest denial to overturn because it's not a clinical decision — it's a contract limitation. A medical necessity appeal usually won't work here. Instead: explore the FDA-approved OSA pathway if you have or suspect sleep apnea; talk to your employer's HR department if you're on a self-funded plan; wait for open enrollment; or access Zepbound directly through LillyDirect starting at $299/month.

"Continuation Denied" (You Were on Zepbound and Coverage Was Pulled)

ContinuationDocument your treatment response. Include baseline vs. current weight, BMI change, improvement in comorbidities (blood pressure, A1C, sleep apnea severity), and your doctor's assessment that ongoing treatment is medically necessary. If the denial is due to a formulary change rather than clinical criteria, follow the formulary exception path above.

What If CVS Caremark Denied Your Zepbound or Wants You to Switch to Wegovy?

What happened

CVS Caremark — one of the largest pharmacy benefit managers in the U.S. — removed Zepbound from several major commercial formularies effective July 1, 2025 and continued to prefer Wegovy on those formularies. Thousands of patients who were successfully using Zepbound received forced-switch letters.

Your provider needs to submit a new PA for Zepbound

You can't appeal the advance notification letter alone. You need an actual denial to appeal from.

Include a Letter of Medical Necessity with the PA submission

Use Eli Lilly's template from zepbound.lilly.com.

Document why Zepbound specifically

Prior semaglutide failure or intolerance, clinical response to Zepbound's dual mechanism, OSA indication, or any reason the switch is clinically inappropriate.

File your appeal even if you also try the preferred alternative

The 180-day clock starts on your denial date. Don't let the clock expire while you're deciding.

The 180-day clock trap

Some patients accept the switch to Wegovy or Mounjaro while “thinking about” their appeal. Meanwhile, the 180-day appeal window is counting down. On day 181, you lose your right to fight for Zepbound coverage. File your appeal and try the alternative if you want to — but don’t let the clock expire.

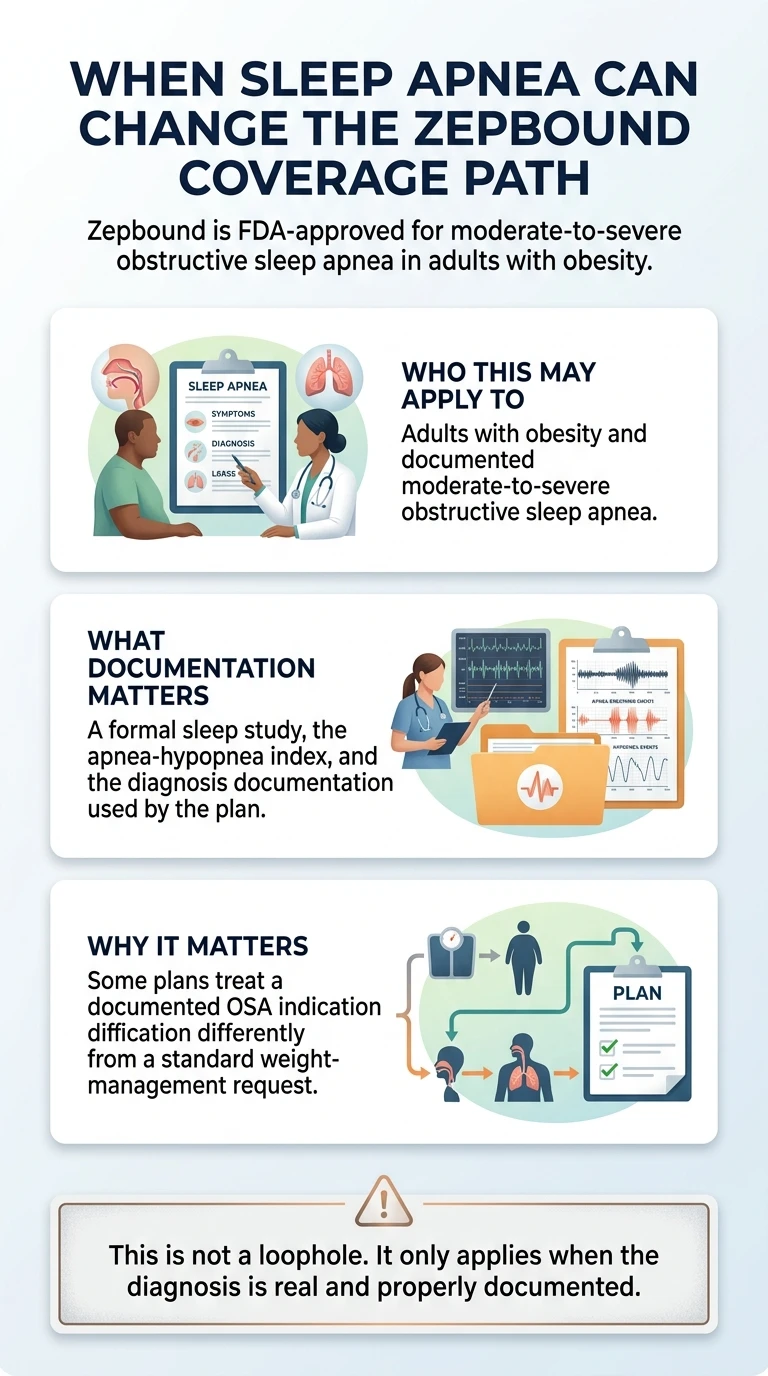

Can Sleep Apnea Change Your Zepbound Coverage Path?

Yes — when the diagnosis is real and properly documented.

Zepbound received FDA approval in late 2024 for the treatment of moderate-to-severe obstructive sleep apnea (OSA) in adults with obesity. This is a separate indication from weight management, and many insurance plans that exclude “weight-loss medications” have distinct coverage criteria for medications prescribed to treat sleep apnea.

Who this pathway works for

- ·Adults with documented moderate-to-severe OSA and obesity (many payer policies commonly use AHI ≥15 and BMI ≥30, but requirements vary)

- ·Patients whose plans exclude weight-loss medications but cover OSA treatments

- ·Medicare Part D enrollees — standard Part D doesn't cover weight-loss drugs but may cover Zepbound when prescribed for OSA

What you need

- ·A formal sleep study (polysomnography or home sleep test) confirming moderate-to-severe OSA

- ·AHI (Apnea-Hypopnea Index) score documentation

- ·Prescription written for the OSA indication specifically

- ·PA submitted under the OSA criteria, not the weight-management criteria

What If Your Doctor Won’t Help With the Appeal?

We hear this more than you’d expect. Some doctors don’t know the appeal process. Some offices are overwhelmed. None of those reasons mean you’re stuck.

You can file the appeal yourself. Under the ACA, you can initiate your own internal appeal or authorize someone to act for you. Your doctor’s documentation still matters — especially the LOMN — but you don’t always need the doctor’s office to handle the submission.

What to ask your doctor (even if they won’t file):

If your doctor’s office is unresponsive or unfamiliar with the process

Consider working with a provider that includes insurance navigation as part of their service. Ro offers FDA-approved GLP-1 medications with a dedicated insurance concierge that handles prior authorizations, appeals paperwork, and coverage coordination for commercially insured patients.

Ro does not coordinate government-plan coverage (Medicare, Medicaid, TRICARE) — if you’re on a government plan, see the Medicare section below.

For commercially insured patients · PA handling · Coverage concierge

“I was thrilled to not have to fight for my coverage.” — Ro member (Members were compensated for their testimonials.)

How Long Do You Have to Appeal? Deadlines by Plan Type

Deadline confusion kills otherwise winnable cases. Miss your window and you forfeit your appeal rights entirely.

| Plan Type | Internal Appeal Deadline | Standard Decision | Expedited |

|---|---|---|---|

| Commercial / Employer | 180 days from denial date | 30 days (pre-service); 60 days (post-service) | 4 business days (internal); 72 hours (external) |

| ACA Marketplace | 180 days from denial date | 30 days (pre-service); 60 days (post-service) | 4 business days (internal); 72 hours (external) |

| Medicare Part D | 65 days for redetermination (CMS) | 7 days standard | 72 hours |

| FEHB (Federal Employee) | Varies by plan — check OPM | 30 days typical | Plan-dependent |

| Medicaid | Varies by state | State-dependent | Available for urgent cases |

Sources: HealthCare.gov · CMS Medicare Part D guidance · Check your specific denial letter — appeal instructions can vary by plan and appeal level.

What to Do While You Wait for the Appeal Decision

Appeals take time. You don’t have to put your health on hold while insurance bureaucracy runs its course.

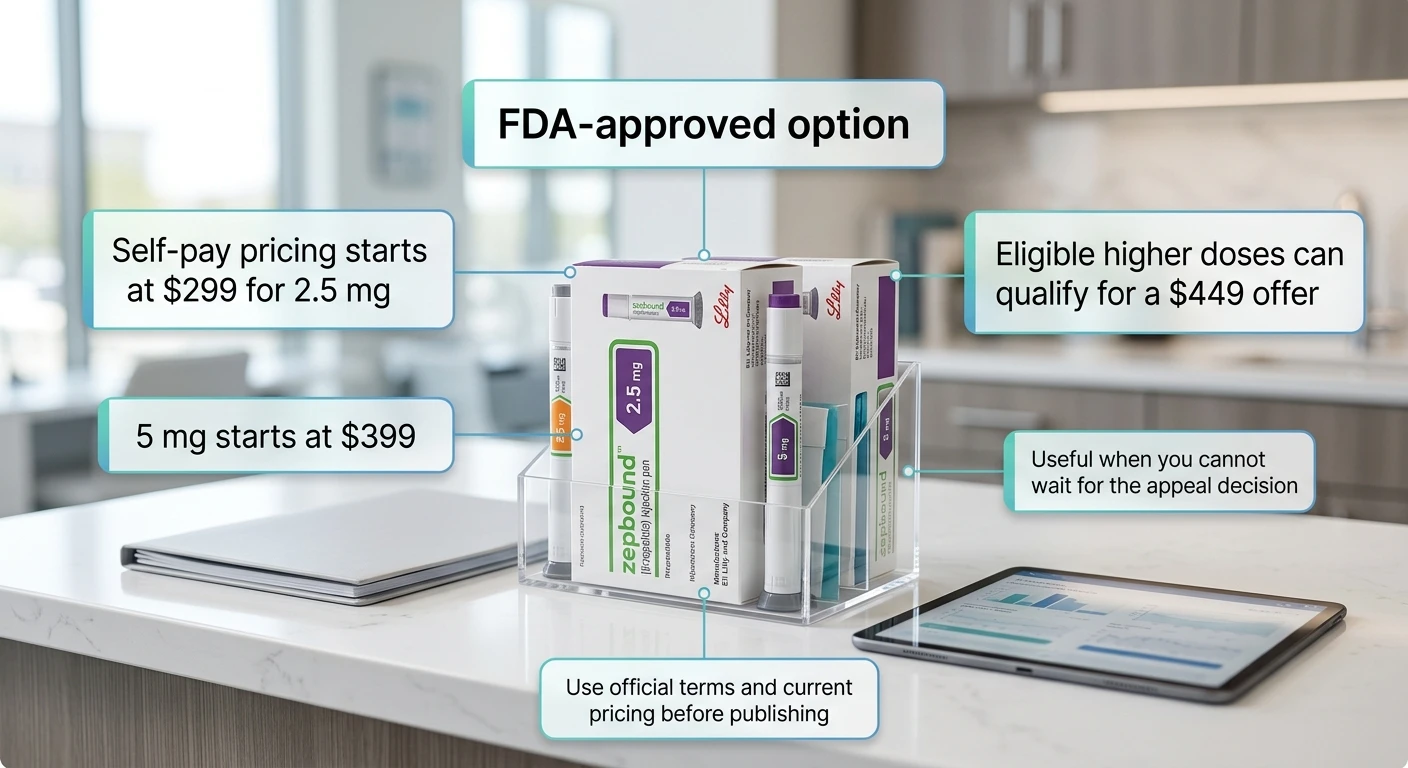

Start FDA-Approved Zepbound Through LillyDirect

Current Zepbound Self-Pay Pricing — Self Pay Journey Program (Verified April 2026)

| Dose | Monthly Cost |

|---|---|

| 2.5 mg (starting dose) | $299/month |

| 5 mg | $399/month |

| 7.5 mg | $449/month* |

| 10 mg | $449/month* |

| 12.5 mg | $449/month* |

| 15 mg | $449/month* |

*The $449 price for 7.5 mg and above requires completing your refill within 45 days of your previous delivery. Set a refill reminder around day 30. Source: zepbound.lilly.com/savings. Terms may change — verify before enrolling.

Available as single-dose vials (free home delivery or free Walmart Pharmacy pickup) or the newer KwikPen for single-patient use (launched February 2026). No insurance or prior authorization required. You may be able to use an HSA or FSA card — check your plan or account terms. FSA-eligible providers →

The Zepbound Savings Card (For Covered Commercial Insurance)

The Math That Matters

Waiting 2–3 months for appeal with no treatment

$0 in drug cost, but potential health regression, weight regain, and worsening comorbidities

LillyDirect for 2–3 months while appealing

$900–$1,350 total at $449/month — then switch to insurance coverage at potentially $25/month if the appeal succeeds

Giving up entirely

The long-term health costs of untreated obesity-related conditions far exceed the cost of a few months of treatment

Want someone to handle the coverage fight for you?

Ro offers FDA-approved GLP-1 medications with a dedicated insurance concierge that checks your coverage, handles PA paperwork, and helps navigate denials — for commercially insured patients. You can start treatment while they work the insurance angle simultaneously.

Free check · PA handling · Self-pay available

MEDVi is another option for patients who want flexibility — offering both FDA-approved and compounded GLP-1 options through licensed prescribers.

FDA-approved and compounded options · Transparent pricing

What If the Appeal Fails?

A failed appeal is not a dead end. It’s a fork in the road with multiple paths forward.

Exhaust Your Appeal Rights First

If You’ve Truly Exhausted All Appeal Levels

Talk to your employer's HR department

On self-funded employer plans, HR can escalate to the plan administrator or even override the PBM's formulary decision. Most employees never try this.

Wait for open enrollment

Choose a plan that covers GLP-1 medications next enrollment period. An estimated 25%+ of large employer plans are expected to offer coverage in 2026, up from 19% in recent years (KFF).

Ask about the Mounjaro pathway

Mounjaro contains the same active ingredient (tirzepatide) as Zepbound but is FDA-approved for type 2 diabetes. If you have type 2 diabetes, your doctor may consider whether Mounjaro is appropriate — some plans cover it more readily.

Go direct with FDA-approved options

LillyDirect starting at $299/month for brand-name Zepbound, or Ro for commercially insured patients who want coverage help alongside treatment.

Direct access options

| Option | What You Get | Monthly Cost |

|---|---|---|

| LillyDirect | FDA-approved Zepbound (vials or KwikPen) | $299–$449/mo |

| Ro | FDA-approved GLP-1 medications + insurance concierge | Varies by plan |

Real People Who Won Their Zepbound Appeals

"I was denied coverage of my Zepbound due to my company changed their requirements. After going over the appeal letter with my doctor (she was incredibly impressed) we submitted and got approved within 48 hours. Worth every penny."

— Zee, via Trustpilot

"My insurance refused prior authorization for Zepbound, but said I could file an appeal. I received my appeal was approved the next day. Thank you for helping me get my life back."

— Patient review, via Trustpilot

Does Medicare Cover Zepbound?

Standard Medicare Part D does not cover Zepbound for weight loss. Federal law currently excludes anti-obesity medications from Part D coverage.

Exception: Obstructive Sleep Apnea

Medicare Part D may cover Zepbound when prescribed for moderate-to-severe OSA in adults with obesity. This requires:

Coverage is not guaranteed even with documentation — individual Part D plans set their own formularies and criteria.

What’s coming for Medicare

Details may change before implementation. Medicare recipients cannot use the Zepbound Savings Card or most manufacturer discount programs.

For the full Medicare Wegovy/GLP-1 coverage breakdown, see: Does Medicare Cover Wegovy for Weight Loss? (2026) →

How We Verified This Guide

Eli Lilly: Zepbound access materials, LOMN template, appeals guide, LillyDirect pricing and terms

zepbound.lilly.com; lilly.com/lillydirect — verified April 3, 2026

HealthCare.gov: Internal appeal rights, external review, and timelines

Federal ACA appeals guidance — verified April 2026

CMS: Medicare Part D appeal procedures, GLP-1 Bridge Program and BALANCE Model announcements

CMS guidance — verified April 2026

KFF: Prior authorization denial and appeal data (Medicare Advantage 2024)

kff.org — 80%+ overturn rate in MA appeals

FDA: Zepbound prescribing information, approved indications (weight management and OSA)

FDA prescribing information — weight management + OSA indication (late 2024)

Payer policy examples reviewed

Aetna, UHC, CVS Caremark published formulary and PA criteria — verified April 2026

Frequently Asked Questions

Can I appeal a Zepbound denial myself?

Yes. Most commercial and Marketplace plans allow patient-initiated internal appeals. You can often file the internal appeal yourself, or authorize someone to act for you. Your doctor's documentation still matters — especially the Letter of Medical Necessity — but you do not always need the doctor's office to submit the appeal packet for you.

How long do I have to appeal a Zepbound denial?

For most commercial and ACA Marketplace plans, you have 180 days from the denial date to file an internal appeal (HealthCare.gov). Medicare Part D redeterminations must generally be filed within 65 days of the notice (CMS). Check your denial letter for your specific deadline and do not wait.

What if Zepbound is not on my insurance formulary?

If Zepbound is not on your plan's formulary, a formulary exception request is usually faster than a traditional appeal. Your doctor submits documentation explaining why Zepbound is medically necessary and why formulary alternatives are not appropriate for your situation. CVS Caremark removed Zepbound from many formularies effective July 2025, making this one of the most common denial scenarios.

What if my insurance says I have to try Wegovy first?

This is a step-therapy denial. You can request a step-therapy exception by documenting why Wegovy or other alternatives are not appropriate — including prior failure, side effects, contraindications, or clinical reasons why Zepbound's dual GIP/GLP-1 mechanism is specifically needed for your condition.

Can sleep apnea help me get Zepbound covered?

It can. Zepbound is FDA-approved for moderate-to-severe obstructive sleep apnea (OSA) in adults with obesity. Some insurance plans that exclude weight-loss medications may still cover Zepbound when prescribed for a documented OSA diagnosis. Many current payer policies use criteria such as AHI of 15 or higher and BMI of 30 or above, but exact requirements vary by plan.

What should be in a Zepbound appeal letter?

A strong Zepbound appeal includes: the exact denial reason quoted from your denial letter, a Letter of Medical Necessity from your prescribing physician, your BMI history and documented comorbidities, records of prior weight-loss attempts and medication trials, recent lab work, and clinical rationale for why Zepbound specifically is the appropriate treatment. Lilly provides a free LOMN template at zepbound.lilly.com.

What if my doctor won't help with the appeal?

You can file a patient-initiated internal appeal on your own. Ask your doctor to at least provide a Letter of Medical Necessity and updated chart notes — even if they don't handle the filing. You can also work with a provider like Ro that includes insurance concierge support for commercially insured patients.

What if my Zepbound appeal was already denied once?

You still have options. Request a peer-to-peer review where your doctor speaks directly with the insurer's medical director. If your internal appeal is denied, you can escalate to an external review — an independent third-party review that your insurer is legally required to accept under the ACA. You can also file a complaint with your state's Department of Insurance.

Is a plan exclusion different from a prior authorization denial?

Yes, and this distinction matters. A PA denial means your plan may cover Zepbound but your specific request didn't meet their criteria — this is often fixable with better documentation. A plan exclusion means your benefit design does not cover weight-loss medications at all, which is much harder to overturn through appeal alone. For plan exclusions, the OSA indication pathway, employer HR escalation, or alternative access through LillyDirect may be more effective.

What should I do while I wait for the appeal result?

You do not have to put your health on hold. LillyDirect — Eli Lilly's patient-access platform — offers FDA-approved Zepbound starting at $299 per month for 2.5 mg, $399 for 5 mg, and $449 for eligible higher doses through its Self Pay Journey Program, with no insurance required.

What if I have Medicare Part D?

Standard Medicare Part D does not cover Zepbound for weight loss, but may cover it for moderate-to-severe obstructive sleep apnea in adults with obesity. CMS has announced a temporary Medicare GLP-1 Bridge Program beginning July 1, 2026 and a broader Medicare Part D BALANCE Model starting January 1, 2027. LillyDirect self-pay is available regardless of Medicare status.

What if I decide to pay cash for Zepbound instead of appealing?

LillyDirect offers FDA-approved Zepbound starting at $299 per month for 2.5 mg, $399 for 5 mg, and eligible higher doses at $449 through the Self Pay Journey Program (refill timing conditions apply). No insurance or prior authorization required. You may be able to use an HSA or FSA card — check your plan or account terms.

Still not sure which GLP-1 program is right for you?

Take our free 60-second matching quiz. We’ll show you a personalized action plan — whether that’s fighting the denial, starting self-pay, or exploring a different path entirely.

Get Your Personalized GLP-1 Action Plan →60 seconds · Free · No signup required

Related guides

- Does Insurance Cover Zepbound for Weight Loss? (April 2026)

- Ozempic vs Zepbound: Which Is Better in 2026? (Real Prices)

- Cheapest Zepbound Without Insurance: Real 2026 Prices

- How to Appeal a Wegovy Denial — 7 Real Steps (2026)

- Best GLP-1 Providers That Accept Insurance (2026)

- Does Medicare Cover Wegovy for Weight Loss? (2026)

- Best Online Wegovy Provider: 7 Legit Options (2026)

- GLP-1 Providers That Take FSA: 8 Verified Picks (2026)

- GLP-1 Providers That Take HSA: 7 Verified Picks (2026)

- Cheapest GLP-1 Without Insurance: All Options Compared

Sources

- Eli Lilly — Zepbound access materials, LOMN template, appeals guide

- LillyDirect — Zepbound Self Pay Journey Program pricing

- HealthCare.gov — Internal appeals

- HealthCare.gov — External review

- CMS — Medicare GLP-1 Bridge Program

- CMS — Medicare Part D BALANCE Model

- KFF — Medicare Advantage prior authorization denial and appeal data (2024)

- FDA — Zepbound prescribing information (weight management and OSA indications)

Affiliate disclosure: Some links on this page go to partner providers including Ro and MEDVi. We earn a commission if you use these services at no extra cost to you. This doesn’t change our analysis or editorial independence. Full disclosure →

This guide is independently researched and not affiliated with any insurance company. All pricing and policy information is verified against official sources and updated monthly.

Last verified: April 3, 2026 · By The RX Index Editorial Team

Free check · PA handling · Self-pay available