Insurance · April 22, 2026

Employer GLP-1 Coverage for Weight Loss Drugs: What Your Job-Based Plan Can Actually Cover

By The RX Index Research Team — Last verified: April 22, 2026. Next scheduled refresh: May 22, 2026.

Bottom line: Most employer GLP-1 denials fall into one of three buckets: a true plan exclusion (a dead end without an exception path), a prior-authorization failure (fixable with better paperwork), or a formulary issue (fixable by switching brands or requesting an exception). Which bucket you’re in determines whether the next step is an appeal, an exception path, or a pivot to cash-pay. The rest of this page walks you through each one.

Quick-diagnose your denial

The exact phrase in your denial letter usually tells you what kind of problem you’re actually solving — and which documents will fix it. Find yours in the table below.

Your denial letter phrase usually tells you what kind of problem you’re solving. Coverage depends on your specific plan.

| What your letter says | What it usually means | What to do next |

|---|---|---|

| “Not a covered benefit” / “Excluded from coverage” | Plan-design issue. Your employer excluded anti-obesity drugs entirely. A perfect prior auth won’t override a benefit exclusion. | Confirm the exclusion in your SPD. Check the FDA-approved exception paths below. If none fit, pivot to cash-pay. |

| “Prior authorization required” / “Criteria not met” | Process issue. The plan may cover it — you didn’t meet a specific threshold (BMI, documentation, step therapy). | Get the exact PA criteria in writing, correct the gap, and resubmit. Many denials in this bucket reverse on appeal. |

| “Not medically necessary” | Evidence issue. The paperwork didn’t prove the plan’s medical-necessity requirements. | Request a Letter of Medical Necessity from your prescriber citing BMI, comorbidities, and prior weight-loss attempts. Appeal. |

| “Drug not covered — try preferred alternative” | Formulary issue, not benefit exclusion. The plan covers GLP-1s but prefers a different brand. | Ask whether the preferred drug fits your situation. If not, request a formulary exception — a separate process from a standard appeal. |

| “Coverage ended at renewal” / “PBM switched preferred brand” | Plan or formulary change. This hit roughly 12 million Zepbound enrollees and 12 million Wegovy enrollees in 2025–2026. | Check the new formulary — you may still qualify for a different GLP-1. If the whole category was dropped, appeal-then-pivot. |

Not sure which path fits your situation?

Take the free 60-second GLP-1 matching quiz →Covers insurance, medication preference, coaching needs, and budget. No sign-up required.

The bottom line: dead end, fixable, or exception path?

If your plan excludes the weight-loss benefit itself, a perfect prior authorization usually won’t save you. If the plan covers the drug class or your diagnosis but the request failed on criteria, documentation, or preferred-product rules, you probably still have a real path.

Most coverage pages treat every denial the same. That’s why people waste weeks on appeals that were never going to work, and why others give up on appeals that would have succeeded in one round. Three buckets. Know yours before you spend energy.

Dead end

The plan document explicitly excludes “anti-obesity medications,” “weight-loss drugs,” or “drugs for weight management.” This is a plan-design decision made by your employer. You can’t appeal your way around a benefit exclusion the same way you appeal a clinical denial. You can sometimes find an exception path, and you can always pivot to cash-pay. What you can’t do is out-paperwork a contract.

Fixable

The plan covers anti-obesity drugs as a category, or covers your drug under a different indication, but your specific request didn’t meet utilization-management rules. BMI below the threshold? Step therapy not documented? Comorbidity note missing? Wrong diagnosis code? These are process problems, and process problems get solved with better paperwork. The fix is usually faster than you think.

Exception path

Your plan excludes weight-loss coverage, but the medication you’re prescribed has another FDA-approved indication your plan does cover. Wegovy was FDA-approved in March 2024 to reduce cardiovascular event risk in adults with established cardiovascular disease and overweight or obesity. Zepbound was FDA-approved for moderate-to-severe obstructive sleep apnea in adults with obesity. Ozempic and Mounjaro cover type 2 diabetes. If any of those diagnoses apply to you, the exception paths section is where to start.

Does your employer have to cover GLP-1s for weight loss?

No. There is no federal law requiring employer-sponsored health plans to cover GLP-1 medications for weight loss. Self-funded plans — which cover 67% of workers with employer-sponsored health coverage per KFF 2025 — are governed by ERISA and are generally not bound by state insurance mandates.

This is the fact most people don’t know when they get denied, and it changes everything about how you respond. Three things matter:

1. ERISA preemption means most state mandates stop at the employer’s door.

If your plan is self-funded — and 67% of covered workers are in one — state insurance laws, including any new state mandates, generally do not bind it. A California employee at a large self-funded employer does not automatically get GLP-1 coverage even if California passes expanded anti-obesity legislation.

2. North Dakota’s mandate is real but narrower than the headlines suggest.

Effective January 1, 2025, North Dakota added GLP-1 and GIP drugs to its ACA Essential Health Benefit benchmark for prevention of diabetes or treatment of insulin resistance, metabolic syndrome, or morbid obesity. It applies to qualifying individual and small-group ACA plans in North Dakota — not grandfathered plans, not self-funded large-group employer plans.

3. ADA/disability protections exist but are fact-specific.

EEOC guidance distinguishes between typical weight variation (not an impairment) and severe or morbid obesity, which can qualify as a disability in some situations — especially when tied to an underlying physiological condition. Courts continue to split on whether obesity alone is an ADA-protected disability. If you’re considering a discrimination angle, talk to an employment attorney before filing anything.

What this means for you: if your denial is a true plan exclusion, the most productive paths are (a) check for an FDA-approved exception indication, (b) pursue cash-pay at manufacturer self-pay prices, or (c) plan for a different employer or plan at next open enrollment. We cover each below.

How common is employer GLP-1 coverage for weight loss in 2026?

Coverage exists but is still a minority position among employers. Among firms with 5,000+ workers, only 43% covered GLP-1s primarily for weight loss in 2025 — and millions of enrollees lost coverage they already had between 2025 and 2026.

The 2025 KFF snapshot (most recent employer-coverage data)

| Employer size | % covering GLP-1s primarily for weight loss (2025) |

|---|---|

| 200–999 workers | 16% |

| 1,000–4,999 workers | 30% |

| 5,000+ workers | 43% |

Source: KFF 2025 Employer Health Benefits Survey. Firms with fewer than 200 workers are not included in these figures.

What’s shaping 2026

Three signals are pulling in opposite directions at the same time:

More of the biggest employers are covering. KFF reports coverage among firms with 5,000+ workers rose from 28% in 2024 to 43% in 2025.

Enrollees are losing access anyway. GoodRx research reported by NPR on April 22, 2026 documented roughly 12 million people losing Zepbound coverage and 12 million losing Wegovy coverage between 2025 and 2026 — the largest single-year contraction in modern anti-obesity drug history, driven largely by PBM formulary decisions including CVS Caremark’s mid-2025 move.

Covering employers are adding restrictions. Brown & Brown’s 2026 employer survey found 63% of employers covering GLP-1s have some form of restriction, and 49% have restrictions beyond standard prior authorization — clinical criteria stricter than the FDA label. Among covering employers, 34% now require enrollees to meet with a dietitian, case manager, or therapist (up from 10% the year before).

Why employers are pulling back: In one Minnesota school district, GLP-1s represent 2% of prescriptions but account for 56% of total drug spending. One benefits director told Peterson-KFF researchers that GLP-1s went from the #32 line item in pharmacy spend to #1 in a single year. When a drug category rewrites the pharmacy budget, employers either scale back coverage, tighten utilization, or shift to alternate payment models.

You’re not being singled out. You’re caught in a national cost correction with employers, PBMs, and insurers all pulling different levers at once.

Why the insurer logo on your card doesn’t tell you enough

The logo on your insurance card (UnitedHealthcare, Aetna, Cigna, BCBS) is usually not the entity that decided whether your GLP-1 is covered. Your employer designed the plan. The insurer processes claims. A pharmacy benefit manager manages the formulary. If your plan is self-funded, your employer pays the claims directly, and state mandates generally don’t apply. This is why two coworkers at the “same” insurer can get opposite answers.

The fastest way to find out: email HR and ask “Is our health plan self-funded or fully insured?” They are required to tell you. That answer determines which rules apply when you appeal.

| Plan type | Who bears financial risk | State mandates apply? | Share of workers (KFF 2025) |

|---|---|---|---|

| Self-funded (ERISA) | Your employer; insurer just administers | Generally no | 67% |

| Fully insured | The insurer; governed by state insurance law | Yes | ~33% |

| Non-ERISA self-funded (government, school, church) | Employer-funded; exempt from ERISA | Often yes (state law applies) | Varies |

An appeal that tries to invoke state protections on a self-funded ERISA plan goes nowhere. An appeal that misses ERISA’s filing window gets dismissed regardless of how strong the clinical argument is. Know which bucket you’re in first.

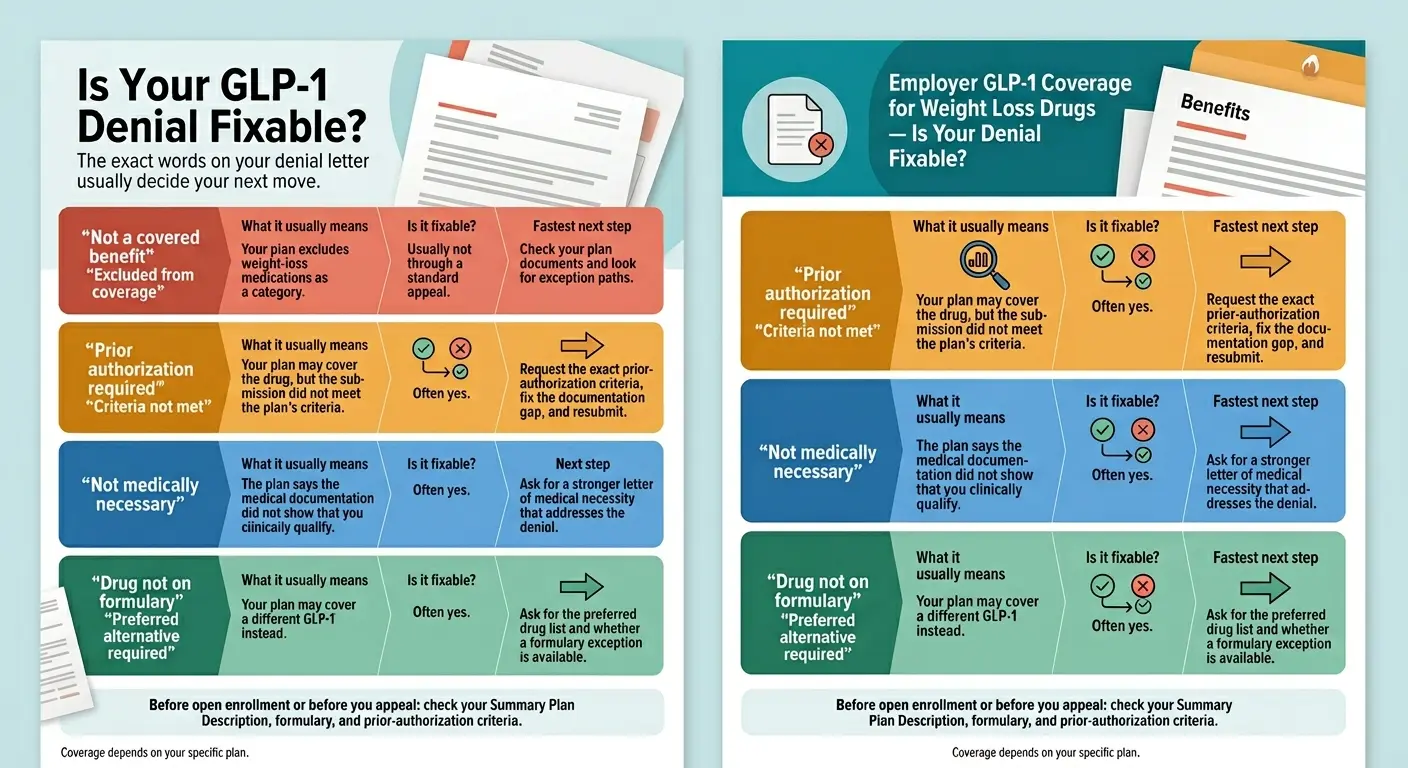

Decode your denial letter: the three buckets

“Not a covered benefit” is different from “prior authorization required” is different from “not medically necessary.” The exact phrase tells you what kind of problem you’re actually solving.

Bucket 1: Benefit exclusion

What it looks like in writing:

- “Not a covered benefit”

- “Excluded from coverage”

- “Weight-loss medications are not covered under this plan”

- “Anti-obesity medications are not a covered service”

What it means: The plan document itself contains an exclusion for this category. A doctor’s strongest letter of medical necessity typically cannot override a benefit-level exclusion.

What to do:

- Pull your Summary Plan Description and search for “weight loss,” “anti-obesity,” “obesity medications,” or “weight management.” Confirm you’re looking at a true exclusion, not a PA requirement.

- Check the FDA-approved exception paths in the next section.

- If no exception applies, don’t spend 180 days on a doomed appeal. Pivot to cash-pay and consider changing plans at next open enrollment.

Bucket 2: Prior authorization / criteria denial

What it looks like in writing:

- “Prior authorization required”

- “Criteria not met”

- “Documentation insufficient”

- “BMI threshold not met”

- “Step therapy not documented”

What it means: The plan covers this medication — but only when specific clinical thresholds are met. Your request didn’t demonstrate them. This is where the majority of denials happen, and also where the majority of reversals happen on appeal.

What to do:

- Request the exact prior-authorization criteria the plan used. You have a legal right to this.

- Compare your medical records to those criteria, line by line. Common gaps: BMI not recorded with a date, a comorbidity not coded, step-therapy attempts not documented with dose and duration.

- Ask your prescriber for a Letter of Medical Necessity that addresses each failed criterion specifically.

- Resubmit, or appeal with the corrected package.

Bucket 3: Formulary exclusion

What it looks like in writing:

- “Drug not on formulary”

- “Non-preferred medication”

- “Try preferred alternative first”

- “Formulary exception required”

What it means: Your plan covers GLP-1s for weight loss, but not the specific brand you’re on. In 2025–2026, many PBMs dropped Zepbound in favor of Wegovy (the CVS Caremark / Zepbound situation that hit millions). The plan isn’t saying “no weight-loss drugs” — it’s saying “not this one.”

What to do:

- Identify which GLP-1 the plan prefers and check the effective date of the change.

- Review the preferred alternative with your prescriber. Switching from Zepbound to Wegovy (or vice versa) is often clinically straightforward — different active ingredients, comparable clinical endpoints for most patients.

- If switching isn’t appropriate, request a formulary exception — a separate process from a standard appeal. Reasons that support an exception: documented side effects on the preferred drug, contraindication, lack of response, or dose/titration issues.

- Plan a cash-pay fallback if the exception fails. The current self-pay floor is in the next section.

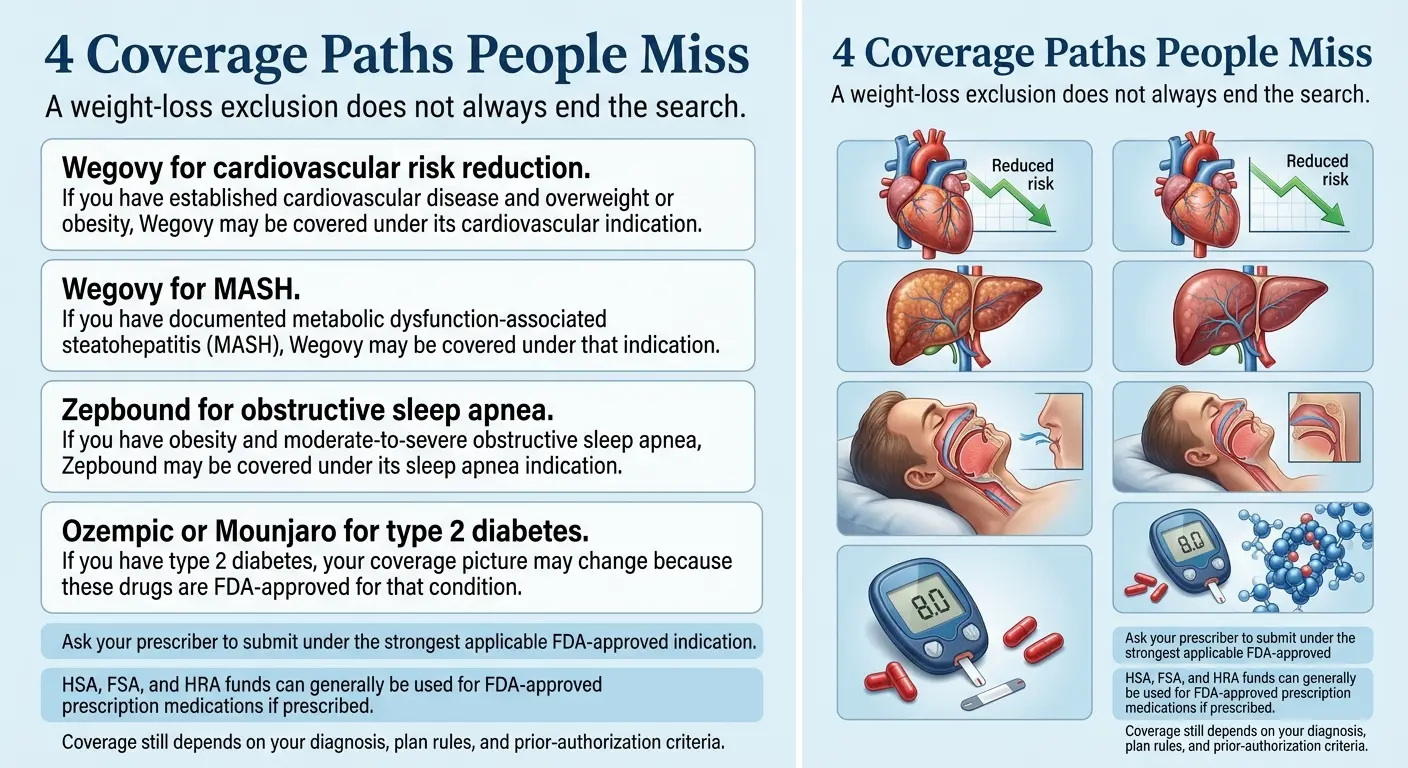

Four FDA-approved exception paths most people miss

A weight-loss exclusion does not always end the search. If the medication you’re prescribed has another FDA-approved indication that your plan does cover, the prior authorization can be submitted under that indication instead. Four paths exist for four real diagnoses.

Four real FDA indications that can change your coverage picture. Talk to your prescriber about which applies to your chart.

Path 1 — Wegovy for cardiovascular risk reduction

The FDA approved Wegovy in March 2024 to reduce the risk of major cardiovascular events (cardiovascular death, non-fatal heart attack, non-fatal stroke) in adults with established cardiovascular disease who are also overweight or obese. This is a separate FDA indication from weight management.

You may qualify if: You have documented established CVD (prior heart attack, stroke, or peripheral arterial disease) and a BMI of 27 or higher. Your cardiologist or primary care provider should submit using the CVD indication if this fits your chart.

Path 2 — Wegovy for MASH

The FDA approved Wegovy for MASH (metabolic dysfunction-associated steatohepatitis) in eligible adults. If your medical record documents MASH (previously called NASH), this is a separate indication from weight loss and falls under different plan rules.

You may qualify if: Your hepatologist or gastroenterologist has documented MASH and you meet the FDA criteria for the indication.

Path 3 — Zepbound for obstructive sleep apnea

Zepbound (tirzepatide) is FDA-approved for moderate-to-severe obstructive sleep apnea in adults with obesity. Employer plans that exclude weight-loss coverage may still cover Zepbound under this indication.

You may qualify if: You have a documented OSA diagnosis (ideally supported by a sleep study — polysomnography or home sleep test) and your BMI places you in the obesity range. Ask your prescriber whether Zepbound can be submitted under the OSA indication rather than weight loss.

Path 4 — Ozempic or Mounjaro for type 2 diabetes

Ozempic (semaglutide) and Mounjaro (tirzepatide) are FDA-approved for type 2 diabetes. Employer plans that cover GLP-1s for diabetes — which is common — may cover these even when they exclude anti-obesity coverage.

You may qualify if: You have a documented type 2 diabetes diagnosis, and your clinical notes reflect that indication. Many denials happen because the prior authorization was submitted under “weight loss” rather than “type 2 diabetes” for people who have both.

Important: These exception paths are about real diagnoses already documented in your chart, not about gaming the system. Don’t ask your doctor to code something that isn’t true. What we’re pointing out is that many people have one of these conditions, their chart reflects it, and their denial happened because the prior authorization was submitted under “weight loss” rather than the indication that would actually get covered. Fixing that submission is legitimate, and it often works.

Not sure what your plan will cover? Check before you commit.

Check my GLP-1 coverage with Ro — free report → (sponsored affiliate link, opens in a new tab)Ro’s free GLP-1 Insurance Coverage Checker contacts your insurer and returns a personalized written coverage report before you pay for anything. Useful even if you end up going elsewhere. We earn a commission if you enroll through our link, at no cost to you.

How to check your employer GLP-1 coverage in 10 minutes

The four documents that tell you exactly what your employer covers are the Summary Plan Description (SPD), the Summary of Benefits and Coverage (SBC), the drug formulary, and the prior-authorization criteria. Pull all four and search them for “weight,” “obesity,” “GLP-1,” and specific drug names.

Pull the Summary Plan Description (SPD).

Your SPD is a legal document that spells out what your plan covers, what it excludes, and how to appeal a denial. The Department of Labor requires plan administrators to provide it to any participant who asks. Ask HR or find it on your benefits portal. Search for “weight loss,” “anti-obesity,” “obesity,” and “weight management.” An explicit exclusion = Bucket 1. A PA requirement = Bucket 2.

Pull the Summary of Benefits and Coverage (SBC).

A shorter, standardized document required under the ACA. It won’t list every drug, but it summarizes covered categories and cost-sharing. Required to be provided within 7 business days of a request; often available on your benefits portal.

Pull the current drug formulary.

Search for “semaglutide,” “tirzepatide,” “orforglipron,” “Wegovy,” “Zepbound,” “Ozempic,” “Mounjaro,” and “Foundayo.” If a drug is listed, note its tier and any restrictions (PA, quantity limits, step therapy). If it’s not listed, it may be on a separate exclusion list or simply absent — absence is not always an exclusion.

Request the prior-authorization criteria.

Under federal rules, you have a right to the actual PA criteria, clinical guidelines, or protocols the plan used to evaluate your request. Ask for them in writing before you submit an appeal. Specific questions produce specific answers. Vague questions produce vague denials.

How to appeal a GLP-1 denial

Under federal rules for most non-grandfathered health plans, you have a right to a full and fair internal appeal — typically with at least 180 days from the denial date — and, if that’s upheld, a right to independent external review by a third-party clinician.

Before you file

- Re-read your denial notice. It must state the specific reason for the denial, cite the plan provision it relies on, describe any additional appeal levels, and describe your right to request free copies of documents relevant to your claim.

- Request the clinical criteria used. You have a right to see the actual PA criteria the reviewer applied and any internal rule, protocol, or guideline they relied on.

- Determine your plan type. ACA external-review rights apply to most non-grandfathered plans. Your SPD or denial notice should tell you.

Internal appeal — the anchor

Who reviews: Usually clinical staff at your insurer or TPA who were not involved in the initial decision. Some plans have a second level of internal review.

Timeline: Federal rules generally require plans to give you at least 180 days to file. Response timelines: 30 days is common for PA appeals, 60 days for claims already incurred, 72 hours for urgent cases.

What to submit:

- The original denial letter

- A Letter of Medical Necessity from your prescriber that addresses each criterion the plan cited

- BMI records with dates, comorbidity diagnosis codes, prior weight-loss attempts (programs, medications, duration), relevant labs

- Sleep-study or cardiology workup if invoking an FDA-exception indication

How to write an appeal that actually works: The strongest appeals cite the plan’s exact PA criteria line by line, address each one with specific evidence from your chart, reference the FDA label and relevant clinical studies, and include a clear clinical rationale. Match the letter to the plan’s criteria — not the other way around.

Peer-to-peer review

Most plans allow your prescriber to request a peer-to-peer review — a direct conversation with the insurer’s medical director about your case. Use it when the clinical story wasn’t fully captured in the written submission, because a physician-to-physician conversation can resolve nuances that paperwork loses.

External review

If your internal appeal is upheld and you’re in a non-grandfathered plan, you typically have a right to external review by an independent third-party reviewer under ACA rules. Standard external review takes up to 45 days; urgent review is typically 72 hours. Consumer-advocacy research suggests roughly 30–40% of external reviews result in the denial being overturned when the clinical case is strong.

What doesn’t work

- Arguing emotionally without clinical documentation

- Appealing a true benefit exclusion with a medical-necessity argument alone

- Submitting a generic “my doctor thinks I need this” letter without criteria-matched evidence

- Missing your filing window

What works

- Identifying the exact bucket (exclusion vs PA vs formulary) before filing

- Matching every piece of evidence to every criterion, by name

- Invoking an exception indication if you have a qualifying diagnosis

- Requesting peer-to-peer when the clinical story is strong

If coverage is truly a dead end: the 2026 cash-pay floor

Your realistic options are (1) FDA-approved brand at manufacturer self-pay prices through LillyDirect or NovoCare, (2) FDA-approved brand through a telehealth platform with insurance concierge support (Ro, Sesame Care (sponsored affiliate link, opens in a new tab), Hers (sponsored affiliate link, opens in a new tab), Hims), and — as a separate non-FDA-approved category — compounded semaglutide or tirzepatide. Brand-name self-pay floor: $149/month for Foundayo, $199/month intro for Wegovy pen, $299/month for 2.5 mg Zepbound vial.

Brand-name FDA-approved self-pay options (verified April 22, 2026)

| Medication | Cash-pay starting price | Notes | Source |

|---|---|---|---|

| Foundayo (orforglipron, oral pill) | $149/month | Higher doses priced up; some high-dose offers depend on refill timing | foundayo.lilly.com |

| Wegovy pen (injection) | $199/month intro | Intro offer for 0.25 mg and 0.5 mg through December 31, 2026; then standard doses | NovoCare |

| Wegovy pill (oral) | $149/month | For 1.5 mg and 4 mg doses; 4 mg rises to $199 after Aug 31, 2026; higher strengths priced up | NovoCare |

| Zepbound vial (via LillyDirect) | $299/month | 2.5 mg starting dose via Self Pay Journey Program (refill within 45 days); $399 for 5 mg; $449 for 7.5–15 mg | zepbound.lilly.com |

| Zepbound KwikPen | $449/month | 7.5–15 mg doses via Self Pay Journey Program; 2.5 mg is a starting dose only | zepbound.lilly.com |

Program terms and prices are time-bounded and can change. Verify the current offer on the manufacturer page before purchase.

Telehealth platforms that pair with FDA-approved brand access

Manufacturer self-pay is the cheapest mathematical option if you already have a prescription. But if you’re still fighting a denial, want help coordinating prior authorization, or need a prescriber, a telehealth platform becomes the more practical path.

For this specific situation — employer coverage denied and you want FDA-approved brand with coverage support — Ro is our primary recommendation. Ro carries Zepbound and Foundayo, matches LillyDirect / NovoCare / TrumpRx pricing on medication, offers a free GLP-1 Insurance Coverage Checker, and has an insurance concierge who coordinates prior-authorization paperwork. Ro Body starts at $39 for the first month, then $149/month ongoing, or as low as $74/month with annual plan paid upfront. Medication price stacks on top of the membership but matches manufacturer self-pay.

The honest caveat: If you already have a prescription and only want the lowest monthly medication cost, buying Zepbound vials directly through LillyDirect or Wegovy through NovoCare will be cheaper (no membership fee). Ro’s value is the coverage support: the checker, the PA paperwork, the fallback plan. If you want help navigating a messy coverage situation, Ro is the better fit.

Start Ro for $39 — then as low as $74/month with annual plan

Check eligibility and current pricing on Ro → (sponsored affiliate link, opens in a new tab)Ro carries Zepbound (tirzepatide) and Foundayo (orforglipron). Medication pricing matches LillyDirect / NovoCare / TrumpRx. Verify current pricing at ro.co/weight-loss before purchase. We earn a commission if you sign up through our link, at no cost to you.

If Ro isn’t the right fit

- Sesame Care — Broadest FDA-approved formulary: Wegovy, Zepbound, Ozempic, Mounjaro, Foundayo, Saxenda. Success by Sesame subscription starts at $59/month annually; medication billed separately. Good fit if you want provider choice or are comparing multiple brands.

- Hers / Hims — Following a March 2026 Novo Nordisk partnership, both offer FDA-approved Wegovy pill, Wegovy pen, and Ozempic. Good fit if you specifically want a female-coded (Hers) or male-coded (Hims) consumer telehealth brand.

- LillyDirect or NovoCare direct — Cheapest mathematical option if you already have a prescription and don’t need telehealth support.

A note on compounded semaglutide and tirzepatide

Compounded semaglutide and tirzepatide are not the same as FDA-approved Wegovy, Ozempic, Zepbound, or Mounjaro. Compounded medications are prepared by licensed compounding pharmacies and are regulated differently from brand-name drugs — they are not FDA-approved finished products and have not undergone the same clinical trials. The FDA has issued safety communications about compounded semaglutide and has warned against marketing compounded products as equivalent to FDA-approved drugs. If your monthly budget can’t support brand-name cash-pay and you’re comfortable with a non-FDA-approved alternative, discuss compounded options with a licensed clinician. See our compounded GLP-1 alternatives guide for the full clinical and regulatory picture.

What’s changing with Medicare and Medicaid in 2026–2027

For the first time, Medicare will cover GLP-1s used to reduce excess body weight — through a short-term CMS demonstration called the Medicare GLP-1 Bridge. The Bridge operates July 1 – December 31, 2026, with eligible beneficiaries paying a $50 monthly copay. Coverage continues January 1, 2027 through the BALANCE Model.

This section doesn’t change your current employer denial. It matters because it reshapes the anti-obesity-drug access landscape — and because some readers are close to Medicare eligibility and should factor in the timing.

The Medicare GLP-1 Bridge (July 1 – December 31, 2026)

Per CMS’s Medicare GLP-1 Bridge page, the demonstration gives eligible Medicare Part D beneficiaries early access to certain GLP-1 drugs for weight reduction. Eligible drugs: Wegovy (injection and tablets) and Zepbound. Eligible beneficiaries pay a $50 monthly copay; CMS covers the difference against a participating-manufacturer net price of $245 per monthly supply. The $50 copay does not count toward True Out-of-Pocket (TrOOP) costs.

Important: Beneficiaries who qualify for Zepbound under its OSA indication or Wegovy under its CVD indication continue going through their Part D plan’s normal coverage process — those uses fall under the basic Part D benefit, not the Bridge demonstration.

The BALANCE Model (starting May 2026 for Medicaid, January 1, 2027 for Medicare Part D)

Per the CMS BALANCE Model page, CMS negotiates directly with manufacturers for pricing offered to state Medicaid agencies and participating Part D plans. Bridge beneficiaries who want to continue GLP-1 weight-management coverage into 2027 will need to enroll in a Part D plan that opts to participate in BALANCE.

Medicaid by state

Per KFF, 13 state Medicaid programs cover GLP-1s for obesity as of January 2026 — down from 16 in October 2025, after California, New Hampshire, Pennsylvania, and South Carolina eliminated coverage. Michigan limited coverage to “morbidly obese” adults. Other states are considering further restrictions.

If you can bridge 6–18 months on cash-pay, a more affordable path may be arriving. That doesn’t help today’s denial — but it does reframe the planning horizon.

What we actually verified (primary sources, April 22, 2026)

- KFF 2025 Employer Health Benefits Survey — employer coverage rates by firm size, lifestyle-program requirement, self-funded share

- Peterson-KFF Health System Tracker, January 2026 — employer cost commentary

- NPR / GoodRx research, April 22, 2026 — 12M + 12M coverage-loss figures

- CMS Medicare GLP-1 Bridge page — Bridge dates, drugs, eligibility, copay

- CMS BALANCE Model page — BALANCE timeline

- KFF Medicaid GLP-1 tracker — state Medicaid coverage

- FDA press releases and labels — Wegovy CVD (March 2024), Wegovy MASH, Zepbound OSA, Foundayo approval

- North Dakota Insurance Department — state EHB update language

- U.S. Department of Labor EBSA — SPD rights, claims and appeals procedures

- Manufacturer pricing pages: foundayo.lilly.com, novocare.com, zepbound.lilly.com — verified April 22, 2026

Employer benefit plan coverage and drug pricing change frequently. If any figure on this page doesn’t match what you see after clicking through, trust the primary source. We re-verify pricing and policy data monthly. Email [email protected] if you spot an error.

Frequently asked questions: employer GLP-1 coverage

Does my employer have to cover GLP-1s for weight loss?

No. There is no federal law requiring employer-sponsored health plans to cover GLP-1 medications for weight loss. Self-funded plans -- which cover 67% of workers with employer-sponsored coverage per KFF 2025 -- are governed by ERISA and are generally not bound by state insurance mandates. North Dakota added GLP-1s to its ACA Essential Health Benefit benchmark effective January 1, 2025, but only for qualifying individual and small-group plans, not self-funded large-group employer plans.

What is the difference between a benefit exclusion and a prior authorization denial?

A benefit exclusion means the plan document itself excludes the drug category -- anti-obesity medications are simply not a covered benefit, and a medical necessity appeal typically cannot override that. A prior authorization denial means the plan covers the drug category, but your specific request did not meet the clinical criteria the plan requires. Benefit exclusions are best addressed by looking for FDA-approved exception indications or pivoting to cash-pay. Prior authorization denials are addressed by correcting the clinical documentation and resubmitting.

Can I appeal a GLP-1 denial if my employer plan excludes weight-loss drugs?

You can submit an appeal, but a standard medical-necessity argument is unlikely to succeed against a true benefit exclusion. Your best paths are: (1) check whether you qualify for a different FDA-approved indication such as Wegovy for cardiovascular risk reduction or MASH, or Zepbound for obstructive sleep apnea; (2) pivot to cash-pay at manufacturer self-pay prices; or (3) change plans at next open enrollment. If the denial is a prior authorization or formulary issue -- not a benefit exclusion -- appeals have a strong track record of working when clinical documentation is complete.

What FDA-approved indications other than weight loss might help me get GLP-1 coverage?

Four paths: (1) Wegovy was FDA-approved in March 2024 to reduce cardiovascular event risk in adults with established cardiovascular disease and overweight or obesity. (2) Wegovy was FDA-approved for MASH (metabolic dysfunction-associated steatohepatitis). (3) Zepbound was FDA-approved for moderate-to-severe obstructive sleep apnea in adults with obesity. (4) Ozempic and Mounjaro are FDA-approved for type 2 diabetes, and plans that cover GLP-1s for diabetes may cover them under that indication. These paths require a real documented diagnosis -- talk to your prescriber about whether the submission should reference the applicable FDA indication.

What is the cheapest cash-pay option if my employer will not cover GLP-1s?

Manufacturer self-pay programs are usually cheapest on pure math: Foundayo starting at $149/month, Wegovy pen $199/month intro, Zepbound 2.5 mg vial $299/month via LillyDirect. Telehealth platforms (Ro, Sesame Care, Hims, Hers) layer a membership fee on top of medication pricing but add insurance concierge support and coverage-checker tools. Compounded semaglutide and tirzepatide from licensed compounding pharmacies are a separate non-FDA-approved category that may cost less but carries different regulatory and safety considerations.

Can I use HSA or FSA money for GLP-1 drugs?

Yes for FDA-approved prescription GLP-1s (Wegovy, Zepbound, Ozempic, Mounjaro, Foundayo) when prescribed by a licensed clinician. Rules for compounded medications vary by plan administrator -- check your specific HSA or FSA provider before using account funds for compounded GLP-1s.

Will Medicare cover Wegovy or Zepbound for weight loss?

Per the CMS Medicare GLP-1 Bridge page, eligible Medicare Part D beneficiaries can access Wegovy (injection and tablets) and Zepbound for weight reduction through the Bridge demonstration between July 1, 2026 and December 31, 2026, subject to Bridge-specific prior-authorization criteria, at a $50 monthly copay. Coverage continues beginning January 1, 2027 through the BALANCE Model for beneficiaries who enroll in a participating Part D plan.

What if my BMI is under 30?

Most GLP-1 prior-authorization criteria accept a BMI of 27 or higher with at least one weight-related comorbidity such as type 2 diabetes, hypertension, cardiovascular disease, or obstructive sleep apnea. If you meet the comorbidity threshold, make sure your medical record clearly documents both the BMI and the qualifying condition, with dates.

Related guides

- How to ask your employer to cover GLP-1s: script and strategy

- Does CVS Caremark cover Wegovy? 2026 formulary and PA guide

- Does TRICARE cover GLP-1 medications in 2026?

- GLP-1 providers that accept HSA and FSA in 2026

- Is compounded semaglutide HSA eligible?

- Compounded GLP-1 alternatives: real prices and tradeoffs

- Best telehealth providers for GLP-1 access in 2026

Last verified: April 22, 2026. Next scheduled refresh: May 22, 2026. The RX Index is a pricing intelligence and comparison resource for GLP-1 telehealth providers. This page was researched and written by The RX Index Research Team. We earn affiliate commissions when readers sign up with Ro through our links. We do not earn commissions from the manufacturer programs (LillyDirect, NovoCare), Sesame Care, Hers, or Hims links above. Our editorial analysis is applied before commercial considerations. Information on this page is for general educational purposes only and does not constitute legal, benefits, or medical advice. Consult a licensed healthcare provider before starting or stopping any medication, and consult a benefits attorney or HR professional for advice specific to your plan.

Your situation changes the answer

Find My GLP-1 Path

The right GLP-1 provider isn't the same for everyone. It depends on your state, your insurance and formulary, whether you want an FDA-approved or compounded medication, your preferred route (injection or oral), and your budget. Because a general answer can't resolve those for you, use The RX Index's Find My GLP-1 Path tool to get a personalized provider match with source-verified pricing before you choose.

- What it asks: your state, insurance situation, medication preference, budget, and support needs

- What you get: a personalized shortlist of GLP-1 providers matched to your situation, with verified pricing and the right questions to ask

- Cost: free · about 2 minutes · no signup