Is Compounded Semaglutide HSA Eligible? Yes — Here’s the 2026 Rule

Published:

By The RX Index Editorial Team • Last verified: April 17, 2026 • Published April 17, 2026

Not medical or tax advice. Consult a licensed tax professional for your specific situation.

Yes. Compounded semaglutide is HSA and FSA eligible when a licensed provider prescribes it to treat a diagnosed medical condition — obesity, overweight with comorbidities like type 2 diabetes or hypertension, or another qualifying diagnosis. The IRS rule (Publication 502, Section 213 of the Internal Revenue Code) doesn’t turn on whether your semaglutide is FDA-approved or compounded. It turns on whether your prescription treats a real medical condition.

Here’s what trips most readers up: “HSA-eligible” and “HSA card works at checkout” are not the same question. Compounded medications don’t carry the same standardized billing identifiers that retail pharmacies use for automatic substantiation. That’s why the card sometimes declines even when the expense qualifies. Documentation is what moves your claim from “flagged” to “paid.”

This page walks you through the three questions that actually matter, shows the exact receipt language that clears review, and ends with a green/yellow/red check so you know which lane you’re in before you pay.

What we actually verified for this page

Before you trust another word on this page, here is the source stack behind it:

- IRS Publication 502 (medical and dental expenses)

- IRS Publication 969 (HSA 2026 contribution limits)

- IRS FAQ on nutrition, wellness, and general health expenses

- FDA statement on semaglutide shortage resolution (February 21, 2025)

- FDA clarification on compounder policies for GLP-1 products (April 1, 2026)

- FDA safety page on unapproved GLP-1 drugs used for weight loss

- FDA Warning Letter #721455 to MEDVi, dated February 20, 2026

- Live provider payment pages and FAQs for Embody, SkinnyRx, Shed, MEDVi, and Sesame Care (reviewed April 16–17, 2026)

- Administrator substantiation guidance (HealthEquity, FSA Store, HSA Store)

What we did not do: we did not invent testimonials, we did not claim compounded semaglutide contains the same active ingredient as FDA-approved Wegovy, and we did not recommend any provider whose payment and HSA/FSA language we did not verify directly in April 2026.

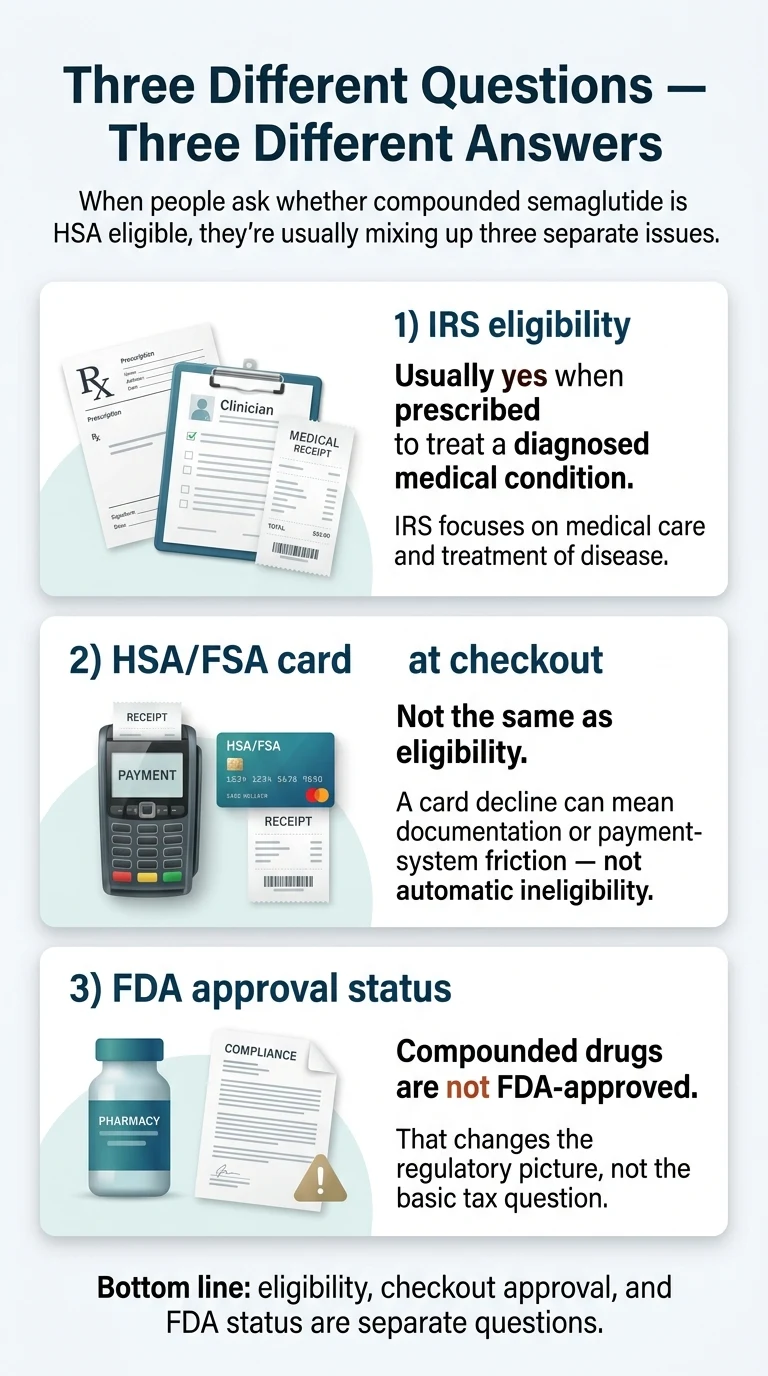

The three questions people are actually asking

When readers type “is compounded semaglutide HSA eligible,” they’re really asking three separate questions — and the answer changes depending on which one they mean. IRS eligibility, checkout card acceptance, and FDA compounding status are governed by three different authorities and have three different answers.

Keep these three questions separate in your head. Most reader mistakes start with collapsing them into one.

Question 1 — Is compounded semaglutide a qualified medical expense under IRS rules?

→ Usually yes, when prescribed for a diagnosed condition. The IRS governs this. Answered in the IRS rule section.

Question 2 — Will my HSA or FSA card actually work at checkout?

→ Sometimes, depending on the provider’s payment processor. This is a merchant/system question, not a tax question. A declined card does not mean the expense is ineligible. Answered in the card decline section.

Question 3 — Is compounded semaglutide still legal and legitimate in 2026?

→ Yes, through state-licensed 503A compounding pharmacies on a patient-specific basis, when your prescriber documents a significant clinical difference for your case. Answered in the 2026 legal status section.

If you only take one thing from this page, it’s this: these are three different questions. Don’t answer one with the other.

Is compounded semaglutide HSA eligible under IRS rules?

Under IRS Publication 502 and Section 213 of the Internal Revenue Code, a medication qualifies as a medical expense when a licensed provider prescribes it to treat a diagnosed medical condition. Publication 502 does not separately exclude compounded prescriptions, and it doesn’t require FDA approval for a prescribed drug to qualify as a medical expense.

Here’s the IRS framework that actually applies. Publication 502 defines medical expenses as costs paid for the diagnosis, cure, mitigation, treatment, or prevention of disease. Prescribed drugs for those purposes qualify. There is no separate IRS carveout excluding compounded drugs from medical-expense treatment.

Where the IRS does draw a line is between medications for general health and medications for treating a specific disease. Pub 502 explicitly treats weight-loss treatment for a specific disease diagnosed by a physician — naming obesity, hypertension, and heart disease as examples — as includible medical care. Treatment for general health, appearance, or weight loss without an underlying diagnosis is not.

Clinical situations commonly considered qualifying when documented by a clinician:

- Obesity (body mass index of 30 or higher)

- Overweight (BMI 27–29.9) with at least one weight-related comorbidity such as type 2 diabetes, hypertension, obstructive sleep apnea, or cardiovascular disease risk

- Type 2 diabetes

- PCOS with obesity or insulin resistance

- Metabolic syndrome diagnosed by a provider

- Prediabetes with documented insulin resistance

What does not qualify: a prescription written for general weight management, appearance, or wellness without a diagnosed underlying condition. That’s the bright line.

The American Medical Association recognized obesity as a disease in 2013, and the IRS’s Pub 502 framework treats it consistently with that — a prescription for compounded semaglutide documented to treat obesity is a medical-expense question, not a lifestyle-spending question.

The part that trips people up

A lot of telehealth intake flows use soft language like “start your weight loss journey” on the signup page. That’s marketing copy, not medical documentation. What matters for HSA eligibility is what goes on your chart and your prescription — the diagnosed condition your clinician documents as the clinical reason for treatment.

If your intake never asks whether you have a qualifying condition and never documents one, your prescription sits on thinner ice when it’s time to substantiate a claim.

The fix is simple: before you buy, confirm that your provider’s medical review will document your condition with an appropriate diagnosis. Reputable telehealth providers do this during the clinical intake — they just don’t advertise it on the landing page.

Does compounded status change the HSA answer?

Compounded status changes the regulatory picture, not the IRS picture. The qualified-medical-expense rule for a prescription medication stays the same. But compounded drugs are not FDA-approved, which means your HSA or FSA administrator may scrutinize the claim more carefully and ask for better documentation.

The FDA and the IRS are different authorities with different jobs. The FDA regulates drug safety, effectiveness, and manufacturing. The IRS regulates what counts as a tax-favored medical expense. Compounded semaglutide can be a real, lawfully dispensed prescribed medical treatment — but it’s one the FDA has not reviewed for safety, effectiveness, or quality.

What this means for your HSA claim:

- Tax eligibility: unchanged under the Pub 502 framework.

- Administrator scrutiny: generally higher. Compounded medications don’t use the same standardized billing codes as brand-name drugs, so claims are more likely to receive a manual review instead of automatic approval.

- Documentation burden: heavier. Plan to have a Letter of Medical Necessity on file for weight-management indications, and request itemized receipts that name the medication, dose, prescriber, and dispensing pharmacy.

That’s the whole difference. The IRS rule doesn’t shift. Your paperwork standard does.

We’re not going to soft-pedal this. Compounded medications take more care. The tradeoff is real — compounded semaglutide costs $149–$299 per month through reputable telehealth providers, versus $997+ per month retail for Wegovy or Ozempic. For most cash-pay buyers, a tighter paper trail is a fair price for a meaningful cost reduction. See our full HSA for GLP-1 guide for the broader picture.

Why your HSA or FSA card declines (even when the expense is eligible)

An HSA or FSA card decline at checkout almost never means the expense is ineligible. It usually means the merchant’s payment system doesn’t support automatic substantiation — the process where an electronic system confirms to your administrator that a purchase is a qualified medical expense. Pay with a regular card, obtain an itemized receipt, and file for reimbursement. You get the same tax-free result.

Here’s the mechanic underneath your HSA card. Major retail pharmacies — CVS, Walgreens, Rite Aid — run an approved electronic substantiation system. When you swipe your HSA card for Wegovy at a CVS counter, the system checks the product against its eligible-item database and tells your administrator “this is a qualified prescription — approved.” No paperwork. No review.

Telehealth compounded semaglutide skips that chain entirely. The compounding pharmacy that fills your prescription usually doesn’t run the same kind of merchant integration. Your card processor sees only “$299 to [Provider Name]” — no product detail. Some providers have built custom substantiation workflows; others haven’t.

What actually happens when your card declines

Three scenarios, ordered by how common they are:

- Your provider doesn’t accept HSA/FSA cards at all. The processor rejects the card. Pay with a regular card and file for reimbursement.

- Your provider accepts the card but can’t auto-substantiate. The card goes through, then your administrator flags it and requests documentation within a set window. Send the itemized receipt and it clears.

- Your provider accepts and fully substantiates HSA/FSA. The card works cleanly. SkinnyRx, MEDVi, Shed, and Willow have all published language supporting HSA/FSA card acceptance; we re-verify their current payment pages quarterly.

The 5-step playbook if your card is declined

- Pay with a personal credit or debit card. Don’t panic. Don’t cancel.

- Download your itemized receipt from the provider’s portal. If the default receipt is thin, message support and request a more detailed invoice. Use this template:

“Can you send me an itemized invoice that includes the medication name and strength, prescription number, prescribing provider’s name, and the dispensing pharmacy? I need it for HSA/FSA substantiation.”

- Request a Letter of Medical Necessity (LMN) from your prescriber if the prescription is for weight management or if your administrator is strict. Most telehealth clinicians generate these on request.

- File the reimbursement claim through your HSA or FSA administrator’s portal. Processing time varies by administrator.

- If denied, appeal with the LMN, itemized receipt, prescription copy, and a one-paragraph cover note naming the diagnosed condition being treated. Most denials are documentation problems that can be resolved with better paperwork.

A card decline is a speed bump, not a stop sign.

Want a low-cost cash-pay program to start compounded semaglutide?

See Embody’s compounded semaglutide plan → (sponsored affiliate link, opens in a new tab)Cash-pay · From $99 first month · Advertised HSA/FSA eligible — confirm with your plan

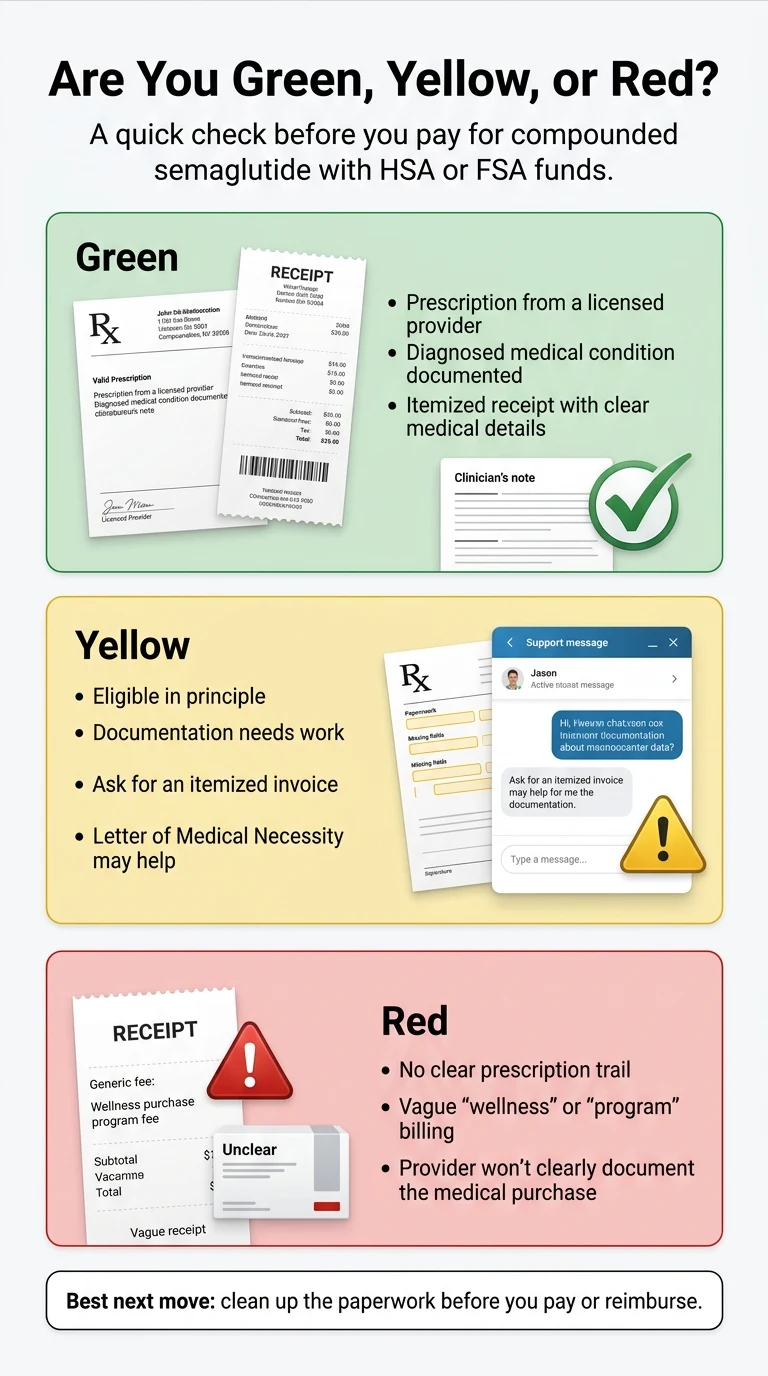

Your situation: green, yellow, or red?

Most readers fall into one of three buckets: green-light (you’re on solid ground, submit the claim), yellow-light (eligible in principle, but you need better documentation), or red-light (the way this is framed will likely be denied — fix it before you pay). The difference is documentation, not the drug.

This is the fastest way to know where you actually stand. Scan for your situation.

🟢 Green light — you’re on solid ground

You have all of these:

- A prescription from a licensed provider

- A diagnosed qualifying condition (obesity, overweight with comorbidity, type 2 diabetes, PCOS with obesity, or similar) documented in your chart

- An itemized receipt that names the medication, dose, prescriber, and prescription number

- A dispensing pharmacy identified by name on the receipt

- A Letter of Medical Necessity on file (recommended, not always required for HSA)

What to do: swipe your card if supported, or pay with a personal card and reimburse yourself. Save the documentation for at least three years per IRS recordkeeping guidance.

🟡 Yellow light — eligible in principle, get better documentation first

You have most of the above, but at least one of these is true:

- Your prescription is documented “for weight loss” with no underlying diagnosis named

- Your receipt says something vague like “Weight Loss Program,” “Wellness Membership,” or “GLP-1 Package”

- You have an FSA (which administrators scrutinize more aggressively than HSA) and no LMN on file

- The charge on your statement bundles medication with coaching or lifestyle services that aren’t clearly medical

What to do: contact your provider before your next billing cycle. Request (a) an itemized invoice that names the medication and prescriber, and (b) a Letter of Medical Necessity from your prescribing clinician. Most telehealth providers generate both on request. Once they’re in hand, you’re green.

🔴 Red light — fix it before you pay, or step away

You have one or more of these:

- No prescription, or a prescription without a named diagnosed condition

- The program is explicitly marketed as “wellness,” “body reset,” or “metabolic refresh” with no clinical intake or diagnosis

- Your provider won’t disclose the dispensing pharmacy, uses “research-grade” ingredients, or sources from outside legitimate 503A/503B channels

- Your provider uses semaglutide sodium or semaglutide acetate. Per FDA’s safety page on unapproved GLP-1 drugs, these salt forms are different active ingredients than the base form used in approved semaglutide products, and FDA has stated they have not been shown to be safe and effective. Reputable compounders use semaglutide base only.

What to do: don’t force this one. If the provider won’t disclose their API source or is using salt forms, this is a safety issue before it’s a tax issue. Switch providers.

Yellow or green, but not sure which provider makes the clean path easiest?

Take our 60-second matching quiz →Personalized path based on your insurance, budget, and HSA/FSA status.

Brand-name vs. compounded semaglutide — the HSA differences that actually matter

Brand-name semaglutide (Ozempic, Wegovy) and compounded semaglutide are held to the same IRS rule for HSA/FSA eligibility. What differs is operational friction: billing codes, card acceptance rates, receipt quality expectations, and administrator scrutiny. Everything material is in this table.

| Factor | Brand-name (Ozempic / Wegovy) | Compounded semaglutide |

|---|---|---|

| IRS eligibility rule | Qualified medical expense with prescription + diagnosed condition (Pub 502, Section 213) | Same IRS rule — prescription + diagnosed condition |

| FDA approval status | Yes | No — prepared by licensed pharmacies; not reviewed by FDA for safety, effectiveness, or quality |

| Standardized billing code for auto-substantiation | Yes (NDC code) | No — often triggers manual review at HSA/FSA administrators |

| Card swipe at retail pharmacy | High success rate (CVS, Walgreens, Rite Aid) | Not applicable — not dispensed through retail pharmacy |

| Card swipe at online provider checkout | Generally not applicable | Variable — SkinnyRx, Shed, MEDVi, and Willow publish explicit support; others require reimbursement |

| Letter of Medical Necessity needed? | Often not required for Ozempic + T2D; recommended for Wegovy + weight management | Strongly recommended, especially for FSA claims and weight-management indications |

| Administrator scrutiny level | Low to moderate | Moderate to high |

| Typical cash price (April 2026) | $997–$1,349 per month retail | $149–$299 per month via telehealth |

| HSA tax savings at 22% bracket, annual | ~$2,634 on $11,976 annual spend | ~$789 on $3,588 annual spend |

| Legal availability in April 2026 | Commercially available post-shortage | Available through 503A patient-specific compounding when the prescriber documents a significant clinical difference for the individual patient (per FDA April 1, 2026 guidance) |

| Audit defensibility | Clean with itemized receipt | Clean if diagnosed condition, lawful pharmacy, and itemized receipt are all in place |

| Best for | Insurance holders and those prioritizing zero administrator friction | Cash-pay buyers prioritizing lower price who maintain clean documentation |

Sources: IRS Publication 502; IRS Section 213; FDA statement on semaglutide shortage resolution (February 21, 2025); FDA guidance on compounders (April 1, 2026); provider pricing and payment page verification (April 16–17, 2026).

When you need a Letter of Medical Necessity (and when you don’t)

You don’t always need a Letter of Medical Necessity (LMN) for HSA claims on compounded semaglutide — your prescription plus a documented diagnosed condition often satisfies HSA substantiation. But for FSA claims and for any weight-management indication, an LMN meaningfully improves your approval odds. If your prescription is for weight management or your administrator has flagged a claim before, plan to have an LMN on file.

An LMN is a formal letter from your prescriber stating the diagnosis, the treatment, and why the treatment is medically necessary. It’s the single most useful piece of paperwork for a weight-management HSA or FSA claim.

What a good LMN includes

- Specific diagnosis. A clinical diagnosis by name, not “weight loss.” Your provider can include the ICD-10 code associated with your condition.

- Specific treatment recommended. For example: “compounded semaglutide injection, titrated from 0.25 mg to 1.0 mg weekly.”

- The medical rationale. How the treatment addresses the diagnosed condition.

- Prescriber credentials. Provider name, license information, and clinic.

- Signature and date. LMNs typically cover 12 months; your administrator may require annual renewal.

When to ask for one

- Before starting if you know you’ll be reimbursing from an FSA

- Before starting if the prescription will be documented for weight management rather than type 2 diabetes

- Immediately if your administrator has previously flagged a prescription claim

- Proactively if you’re buying through a telehealth provider whose receipts bundle services

Most reputable compounded-semaglutide telehealth providers — including Embody, SkinnyRx, Shed, MEDVi, and Willow — issue LMNs on request as a standard part of patient support.

The FSA angle specifically

FSA administrators tend to be stricter than HSA administrators. The reason is structural: FSA funds are employer-administered and use-it-or-lose-it, which motivates employers and administrators to verify each dollar. Expect a possible “upload documentation” request on a compounded charge. Be ready with the itemized receipt plus LMN and most claims resolve in a single round. See our FSA for GLP-1 guide for the FSA-specific rules.

Receipt language that clears vs. gets flagged

The single biggest predictor of whether your compounded semaglutide HSA claim clears is the quality of your receipt. Administrator substantiation guidance generally requires provider name, patient name, date of service, itemized description of the service or product, and cost. For compounded prescriptions specifically, adding medication name, prescriber, dispensing pharmacy, and a link to the diagnosed condition dramatically reduces manual-review friction.

Minimum substantiation fields (per general administrator guidance)

Every receipt should include:

- Provider name (the practice or telehealth brand)

- Patient name

- Date of service

- Itemized description of the product or service

- Cost

That’s the floor. If your receipt is missing any of these, it’s underbuilt for substantiation — regardless of FDA approval status or drug type.

Helpful extras that make compounded claims sail through

For compounded prescriptions specifically, these additional details reduce friction:

- Medication name and strength (e.g., “compounded semaglutide 2.5 mg/mL injection”)

- Prescription number

- Prescribing provider’s name

- Dispensing pharmacy name (and license number, when available)

- Diagnosed condition or associated ICD-10 code

- Letter of Medical Necessity attached or referenced

❌ Receipt language that gets flagged

- “Weight Loss Program — $299”

- “Wellness Membership — $299”

- “GLP-1 Package — $299”

- “Monthly Subscription — $299”

- No diagnosis reference and no prescriber name

- Bundled charge mixing medication with coaching/community without line items

✅ Receipt language that clears review

- “Compounded semaglutide 2.5 mg/mL injection, 30-day supply, prescribed by Dr. [Name], for treatment of obesity — $299”

- “Prescription medication (compounded semaglutide) + physician consultation + clinical monitoring, itemized invoice attached”

- “Compounded semaglutide injection, dispensed by [Pharmacy Name], Rx #XXXXXX — $299”

The email to send your provider’s support team

Paste this into your provider’s support chat or email:

“Hi — for HSA/FSA substantiation, can you send me an itemized invoice for my last payment that includes (1) medication name and strength, (2) my prescription number, (3) my prescribing provider’s name, and (4) the dispensing pharmacy? My account administrator needs this. Thanks.”

Reputable providers have this on file or can generate it on request. If a provider refuses or can’t produce one, that’s a meaningful signal about whether they should be handling your prescription at all.

Your real tax savings on compounded semaglutide in 2026

Paying for compounded semaglutide with HSA or FSA funds reduces your effective cost by your combined marginal tax rate. Most working adults with HSA-eligible high-deductible health plans fall in the 22–32% federal bracket, plus state income tax in most states, plus 7.65% FICA if the HSA is funded through payroll. On a $299 per month program, that’s roughly $720–$1,100 in annual federal tax savings.

The savings math is the same whether your semaglutide is compounded or brand-name. The IRS doesn’t tax differently based on FDA-approval status.

Tax savings by compounded semaglutide price point

| Monthly price | Annual spend | 22% bracket savings | 32% bracket savings | +7.65% FICA (payroll HSA) |

|---|---|---|---|---|

| $149 | $1,788 | $393/yr | $572/yr | +$137/yr |

| $179 | $2,148 | $473/yr | $687/yr | +$164/yr |

| $199 | $2,388 | $525/yr | $764/yr | +$183/yr |

| $249 | $2,988 | $657/yr | $956/yr | +$229/yr |

| $299 | $3,588 | $789/yr | $1,148/yr | +$274/yr |

2026 federal marginal tax brackets range from 10% to 37%. Most HSA users fall in the 22–32% range; the table shows both. State income tax benefit adds on top in most states. FICA benefit applies only if your HSA is payroll-funded through a cafeteria plan.

2026 HSA contribution limits (per IRS Publication 969)

- Self-only HDHP coverage: $4,400 per year

- Family HDHP coverage: $8,750 per year

- Catch-up contribution (age 55+): additional $1,000 per year

Reality check: a full year of compounded semaglutide at $299/month ($3,588) fits under the self-only HSA contribution limit. If you’re contributing near the maximum already, you’re paying for this with pre-tax money anyway — the tax benefit is automatic.

Why FSA deadlines matter

FSAs are use-it-or-lose-it at plan year end. Some FSA plans allow a carryover of up to $680 into the next year for 2026; others use a 2.5-month grace period; others allow neither. It depends on your employer’s plan design. If you have an FSA balance expiring December 31 and you’re considering compounded semaglutide, starting treatment with those funds is one of the highest-value eligible expenses you can use them on. HSAs don’t have this pressure — they roll over indefinitely — but FSAs punish inaction. See our FSA for GLP-1 guide for the details.

Provider-stated vs. verified snapshot

Here’s the one-page snapshot of what each provider publicly says about HSA/FSA, plus what we verified directly on their pages in April 2026. Use this before choosing a provider — it’s the fastest way to see who matches your payment style.

| Provider | HSA/FSA language on their site | Direct card at checkout | First-month price seen | Verified |

|---|---|---|---|---|

| Embody | Advertised HSA/FSA eligible (confirm with your plan) | Cash-pay; confirm with plan | $99 (sema injection) | June 2026 |

| SkinnyRx | FAQ states HSA/FSA cards accepted | Yes | $199 | April 2026 |

| Shed | Listed on FSA Store | Yes (via FSA Store where applicable) | $199 | April 2026 |

| MEDVi | Advertises HSA/FSA eligibility at checkout | Yes | $149–$179 (varies by landing page) | April 2026 |

| Sesame Care | HSA/FSA cards accepted on Sesame per FAQ; some plans may require receipt submission | Variable by plan | Varies (brand-name) | April 2026 |

This is a verification snapshot, not a full provider review. See our semaglutide providers that take HSA or FSA guide for the full comparison.

Which compounded semaglutide providers make HSA and FSA actually work

Among providers verified, Embody offers the lowest first-month price ($99 for compounded semaglutide injection) and is the only one on this list with a needle-free GLP-1 gum option — though it is a cash-pay program whose HSA/FSA eligibility you should confirm with your own plan. SkinnyRx has the most explicit “HSA/FSA card accepted at checkout” language. Shed is listed on the FSA Store. MEDVi remains operational and widely used but received an FDA warning letter in February 2026 over marketing language. Sesame Care is the cleanest FDA-approved alternative if you want brand-name medication with less paperwork.

We’re not going to parade 15 providers in front of you. These are the ones whose payment pages and HSA/FSA language we verified this month.

Embody — lowest first-month price + needle-free gum

Low-Cost Starter- Entry price: compounded semaglutide injection from $99 first month, then $299/mo; tirzepatide injection from $149 first month, then $399/mo

- Needle-free option: semaglutide GLP-1 gum ($149 first month → $349/mo) for needle-averse patients — “one minty piece per day”

- HSA/FSA: advertised as HSA/FSA eligible — confirm acceptance with your own plan administrator

- Why consider it: cash-pay (no insurance required), no separate membership fee, 24/7 messaging support, and fast online intake reviewed by a licensed provider (often within 24 hours, if approved)

- Best for: the reader who wants the lowest entry price for compounded GLP-1, or a needle-free gum instead of weekly injections

Cash-pay · From $99 first month · Check availability in your state during intake

Honest note: Embody’s shipped compounded products, like all compounded medications, are not FDA-approved finished drugs and are not FDA-reviewed for safety, effectiveness, or quality.

SkinnyRx — most explicit card-at-checkout language

- Entry price: from $199 per month (compounded semaglutide)

- HSA/FSA: SkinnyRx’s FAQ explicitly states they accept HSA/FSA cards at checkout, and product pages display HSA/FSA eligible badges

- Trust signal: 4.8 Trustpilot rating across approximately 5,000 reviews (verified April 2026)

- Best for: the reader whose non-negotiable is seeing “HSA/FSA card accepted” in writing before entering payment information — particularly useful if you’ve had a card declined elsewhere

HSA/FSA card accepted · Verified April 2026

Honest note: individual results on any GLP-1 vary significantly. Set expectations with your prescriber based on your specific situation.

Shed — FSA Store listed with format flexibility

- Entry price: $199 per month (compounded semaglutide)

- Why it matters: Shed is listed on the FSA Store — an independent third-party eligibility signal that adds external validation to their HSA/FSA workflow

- Menu: injectable semaglutide plus additional format options

- Best for: the reader who wants third-party FSA Store validation or format flexibility

FSA Store listed · Verified April 2026

MEDVi — operational and widely used, with an important disclosure

- Entry price: $149 seen on promotional landing pages; $179 seen on MEDVi’s main semaglutide FAQ page

- Ongoing price: $299 per month for compounded semaglutide

- Menu: compounded semaglutide injection, semaglutide tablets, tirzepatide injection, tirzepatide tablets

- HSA/FSA: advertises HSA/FSA eligibility; accepts cards at checkout

- Trust signal: 4.4 Trustpilot rating across more than 11,000 reviews; LegitScript certified

Material disclosure — FDA Warning Letter #721455

On February 20, 2026, FDA issued MEDVi a warning letter over website language the agency identified as false or misleading regarding compounded semaglutide and tirzepatide. The letter cited statements that suggested MEDVi itself was the compounder and claims the agency said implied FDA approval or evaluation of compounded products. MEDVi was one of more than 30 telehealth companies warned during a broader enforcement action. The letter addresses marketing practices, not medication safety. MEDVi remains operational in April 2026. You can read the full warning letter on the FDA’s public database (FDA Warning Letters, #721455, February 20, 2026).

HSA/FSA accepted · Verified April 2026 · See FDA disclosure above

For a deeper look: our MEDVi HSA/FSA deep-dive guide

Sesame Care — the cleanest FDA-approved alternative

If your priority is FDA-approved medication with less administrator friction, Sesame Care connects you with clinicians who can prescribe brand-name GLP-1s like Wegovy or Zepbound. Sesame’s FAQ states that HSA/FSA cards can be used on Sesame, and the Sesame weight-loss page indicates support can provide an itemized bill for subscription services when requested. Some plans may still require receipt submission depending on your specific administrator.

Check FDA-approved GLP-1 options on Sesame Care → (sponsored affiliate link, opens in a new tab)Brand-name Wegovy and Zepbound · HSA/FSA cards accepted on Sesame · Verified April 2026

If your priority is the cleanest paperwork — not the lowest price

Here’s the damaging admission on this page. We’re being direct about it.

Compounded semaglutide does NOT give you the one-swipe HSA experience that Wegovy gets at a CVS pharmacy counter.

If your absolute non-negotiable is zero paperwork, zero reimbursement forms, and zero administrator questions, compounded isn’t the cleanest path — FDA-approved semaglutide through a provider that routes to a retail pharmacy is cleaner.

If that’s you, Sesame Care is the alternative we’d point you to. Sesame connects you with licensed clinicians who can prescribe brand-name GLP-1s like Wegovy or Zepbound, and the resulting prescription fills through a retail pharmacy where the standardized billing integration is more likely to handle HSA/FSA smoothly.

Check FDA-approved GLP-1 options on Sesame Care → (sponsored affiliate link, opens in a new tab)HSA/FSA cards accepted on Sesame · Verified April 2026

But here’s the whole pivot. Because compounded skips the insurance maze and the retail pharmacy channel entirely, the cash price drops from $997+ per month to $149–$299 per month. That’s a difference of roughly $8,000–$10,000 per year for most readers. For someone paying cash and saving that much annually, a tighter paper trail is a reasonable trade.

The right answer depends on what you actually value. If you have strong insurance coverage for Wegovy and you never want to file a reimbursement claim, Sesame’s lane is cleaner. If you’re cash-pay and you can handle an itemized receipt plus an LMN on file, compounded wins on price by a huge margin. Both are legitimate choices.

Is compounded semaglutide still legal in April 2026?

Yes, compounded semaglutide remains legal in April 2026 through state-licensed 503A compounding pharmacies on a patient-specific basis, when the prescriber documents a significant clinical difference that produces a benefit for the individual patient. The FDA removed semaglutide from its drug shortage list on February 21, 2025, which ended the shortage-based enforcement discretion window and the routine “essentially a copy” compounding that was widespread before.

The timeline, short version

| Date | What changed |

|---|---|

| March 2022 | Semaglutide added to FDA drug shortage list during demand surge |

| February 21, 2025 | FDA declared semaglutide shortage resolved |

| April 22, 2025 | Enforcement discretion window ended for 503A state-licensed compounding pharmacies compounding "essentially a copy" of Ozempic/Wegovy |

| May 22, 2025 | Same window ended for 503B outsourcing facilities |

| April 1, 2026 | FDA issued clarifying guidance on what counts as "essentially a copy," including that compounding semaglutide with vitamin B12 is considered essentially a copy when the semaglutide strength is within 10% of a commercially available product, unless the prescriber documents a significant difference for an identified patient |

Patient-specific 503A compounding continues when the prescriber documents a significant clinical difference for the individual patient. That clinical difference might be a dosing variation for titration tolerance, an ingredient change for a documented allergy, a route change, or another medically documented reason.

Legitimate compounded semaglutide providers in April 2026 operate through state-licensed 503A pharmacies, document the clinical rationale on the prescription, use semaglutide base (the validated active ingredient), and disclose their dispensing pharmacy.

Red flags that a provider isn’t operating lawfully

- Refuses to disclose the dispensing pharmacy

- Uses “research-grade” ingredients or semaglutide sodium / semaglutide acetate (FDA-flagged salt forms)

- Sources from outside legitimate 503A/503B channels

- Markets products as direct copies of Ozempic or Wegovy without documented individualized prescriptions

Source: FDA statement on semaglutide shortage resolution (February 21, 2025); FDA clarification on compounder policies (April 1, 2026); FDA safety page on unapproved GLP-1 drugs.

What to do if your reimbursement is denied

An initial denial almost always means “prove it better,” not “impossible forever.” The fix is usually a better-itemized receipt plus a Letter of Medical Necessity plus a one-paragraph cover note. Most denials are documentation issues rather than underlying eligibility issues.

Denial messages often say “not a qualified medical expense” even when the expense is, in fact, qualified. The administrator is flagging inadequate substantiation, not ruling on your IRS eligibility. Read the denial literally — what documentation did they ask for?

The appeal packet

- Itemized receipt with medication name, dose, prescriber, dispensing pharmacy, and diagnosed condition

- Copy of the prescription (request from your provider if you don’t have one)

- Letter of Medical Necessity from the prescribing clinician

- Brief cover note (two or three sentences) stating that this prescription was written to treat a diagnosed medical condition — name the condition — rather than for general health or appearance

When to stop arguing and switch paths

If your administrator rejects a complete, properly documented appeal, you have two options:

- Continue paying out of pocket and accept the tax benefit loss on that provider.

- Switch to a provider whose documentation workflow fits your administrator’s preferences. Providers with explicit HSA/FSA card support and clean itemized invoices — SkinnyRx, Shed, Embody — tend to have fewer downstream denial issues than providers whose receipts are thin.

Don’t let a denial from a strict administrator convince you compounded semaglutide is ineligible. It isn’t. You might just need to change where you buy it. See our full semaglutide providers that take HSA or FSA guide for a side-by-side comparison.

Frequently asked questions

Is compounded semaglutide HSA eligible if prescribed for weight loss?

Yes, when the prescription is documented as treatment for a qualifying medical condition such as obesity (BMI 30+), overweight with comorbidities (BMI 27+ with type 2 diabetes, hypertension, or sleep apnea), type 2 diabetes, or PCOS with obesity. The IRS requires the prescription to treat a diagnosed disease, not a cosmetic or general wellness goal. A Letter of Medical Necessity strengthens the claim for weight-management indications.

Do I need a Letter of Medical Necessity for compounded semaglutide?

Not always for HSA claims, but strongly recommended for FSA claims and for any weight-management prescription. Most telehealth providers issue a Letter of Medical Necessity on request. LMNs typically cover 12 months.

Does a declined HSA or FSA card mean the expense is ineligible?

No. Card acceptance and tax eligibility are separate questions. A card decline usually means the merchant's payment system doesn’t support automatic substantiation. Pay with a regular card, obtain the itemized receipt, and file for reimbursement. You get the same tax-free result.

Is compounded semaglutide still legal in 2026?

Yes, through state-licensed 503A compounding pharmacies on a patient-specific basis when the prescriber documents a significant clinical difference for the individual patient. The FDA removed semaglutide from the drug shortage list on February 21, 2025, ending the routine shortage-based compounding pathway. Patient-specific compounding continues within current FDA guidance.

Does FDA approval determine HSA eligibility?

No. FDA approval and HSA eligibility are governed by different authorities with different standards. The IRS looks at whether a prescription treats a diagnosed medical condition. The FDA regulates drug safety, effectiveness, and manufacturing. A prescription for compounded semaglutide can be HSA-eligible even though compounded drugs are not FDA-approved.

Is compounded tirzepatide HSA eligible too?

Yes, under the same IRS rules. A prescription for compounded tirzepatide to treat a diagnosed medical condition qualifies the same way compounded semaglutide does. Brand-name or compounded, semaglutide or tirzepatide, the IRS rule is the same.

What receipt do I need for HSA reimbursement on compounded semaglutide?

At minimum: provider name, patient name, date of service, itemized description, and cost. For compounded prescriptions specifically, adding medication name and strength, prescription number, prescriber, dispensing pharmacy, and linked diagnosis significantly reduces manual-review friction. Any reputable provider can generate an itemized invoice with these details on request.

Can I use FSA funds for compounded semaglutide?

Yes, under the same IRS rules as HSA. FSA administrators tend to require more upfront documentation because FSA funds are employer-administered and use-it-or-lose-it. Plan to have a Letter of Medical Necessity on file for weight-management prescriptions.

How much can I save with HSA or FSA on compounded semaglutide?

Your savings equal your combined marginal tax rate. Most HSA users fall in the 22–32% federal bracket, plus state income tax in most states, plus 7.65% FICA if your HSA is payroll-funded through a cafeteria plan. On a $299 per month program, that’s roughly $720–$1,100 in annual federal savings.

What if my provider uses semaglutide acetate or semaglutide sodium — is that HSA eligible?

Per FDA’s safety page on unapproved GLP-1 drugs, semaglutide sodium and semaglutide acetate are salt forms that are different active ingredients than the base form used in FDA-approved semaglutide products, and FDA has stated they have not been shown to be safe and effective. Beyond tax eligibility, this is a safety issue. If you cannot confirm the form of semaglutide being dispensed, switch providers. Reputable compounders use semaglutide base.

Will I get audited for using HSA on compounded semaglutide?

Most HSA and FSA expenses are never audited individually, but keep records for at least three years per IRS recordkeeping guidance. If audited, you need the original prescription, itemized receipts, any Letter of Medical Necessity, and documentation of the diagnosed condition. Missing records can result in the expense being reclassified as a non-qualified distribution — taxable income plus a 20% penalty for HSA holders under 65.

Still not sure which GLP-1 program is right for you?

Tell us about your insurance, your budget, and your HSA/FSA situation, and we’ll show you the path that fits. No email required to see your match.

Take our free 60-second matching quiz →Verified editorial note

Written by The RX Index Editorial Team. The RX Index is a pricing intelligence and comparison resource for GLP-1 telehealth providers. We verified the IRS rules on this page against IRS Publication 502, IRS Publication 969, and the IRS medical-expense FAQ. We verified the regulatory context against FDA statements dated February 21, 2025, April 1, 2026, and the FDA safety page on unapproved GLP-1 drugs, as well as FDA Warning Letter #721455 to MEDVi dated February 20, 2026. We verified provider HSA/FSA acceptance language and pricing against live provider payment pages on April 16–17, 2026.

Refresh cadence: quarterly, or immediately on any material regulatory change. Last verified: April 17, 2026.

This page is not medical advice or tax advice. Consult your prescribing clinician for medical questions about GLP-1 treatment, and consult a qualified tax professional for your specific HSA or FSA situation.

Your situation changes the answer

Find My GLP-1 Path

The right GLP-1 provider isn't the same for everyone. It depends on your state, your insurance and formulary, whether you want an FDA-approved or compounded medication, your preferred route (injection or oral), and your budget. Because a general answer can't resolve those for you, use The RX Index's Find My GLP-1 Path tool to get a personalized provider match with source-verified pricing before you choose.

- What it asks: your state, insurance situation, medication preference, budget, and support needs

- What you get: a personalized shortlist of GLP-1 providers matched to your situation, with verified pricing and the right questions to ask

- Cost: free · about 2 minutes · no signup