How to Ask Your Employer to Cover GLP‑1 (2026 Letter, Script & Full Playbook)

By The RX Index Editorial Team · Last verified: · Published:

The RX Index is a pricing intelligence and comparison resource for GLP-1 telehealth providers.

Not medical, legal, or financial advice. Coverage policies and employment law vary — always verify with a licensed professional before acting.

Published:

The short answer (if you only read this)

If you’re searching how to ask your employer to cover GLP-1, here’s the bottom line: yes, you can ask, and it can work — but only if you do it in the right order and treat it as a business request, not a personal one.

First, figure out whether your denial is a hard plan exclusion or a fixable prior authorization problem, because each has a completely different solution. Then confirm whether your plan is self-funded (your employer decides coverage) or fully-insured (the insurer and state mandates decide). Request five specific plan documents. Time your ask to land in the pre-renewal window — typically 3 to 4 months before your plan year starts. Send a short, document-based email to HR with clinician support and a structural compromise that de-risks the decision for them. And if they still say no, five legal bridge paths exist in 2026 to keep you on therapy while the employer conversation continues.

That’s the playbook. The rest of this page gives you the scripts, letters, documents, and decision trees — plus honest odds, because we’re not going to waste your time if the answer’s probably no.

The answer at a glance

| Your situation | What it usually means | Best next move |

|---|---|---|

| Denial says "excluded" or "not a covered benefit" | Hard plan design problem | Ask HR with ROI memo + timing for next renewal |

| Denial says "prior authorization denied" | Documentation problem | Clinician appeal, usually appealable within 180 days |

| Denial says "step therapy required" | Access exists with gates | Request written criteria, meet them, resubmit |

| Plan covers GLP-1 for diabetes only | Business-case fairness argument available | Ask why the same molecule is treated differently by indication |

| Plan excludes weight-loss meds entirely | Category exclusion | Request Excepted Benefit HRA ($2,200/yr) as compromise |

| New job / open enrollment decision | Plan choice problem | Get SPD + formulary before you pick a plan |

Letter, ROI memo & document checklist · Free · 60 seconds

Step 1 — First, figure out what you’re actually dealing with

Answer capsule: Before you write anyone, identify two things: (1) what your denial actually says (exclusion vs. prior authorization vs. step therapy vs. wrong indication), and (2) whether your plan is self-funded or fully-insured. These two data points determine whether HR can help you at all, how fast, and what you should ask for. Most people skip this step and send a generic letter — then wonder why nothing happens.

The 4 kinds of “no”

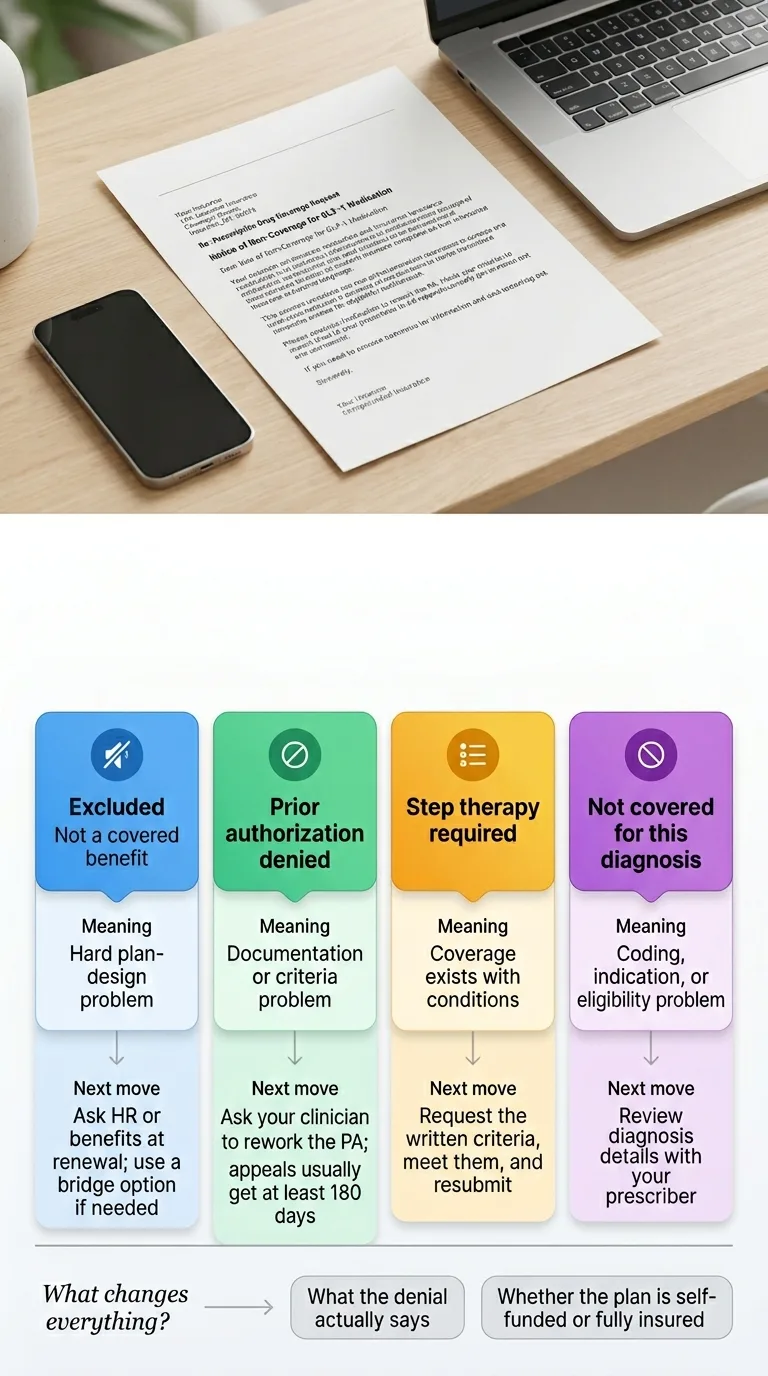

There are four different kinds of denial and each one has a different fix. Pulling the wrong lever wastes weeks.

"Excluded" / "Not a covered benefit" / "Weight loss medications not covered under this plan"

Meaning: This is a true plan exclusion. The plan doesn't cover the drug for your use, period. Appeals almost never work here because there's no medical necessity path when the benefit doesn't exist.

Next move: Employer escalation. Renewal-cycle ask. Bridge options while you wait. This is what the HR email templates below are for.

"Prior authorization denied" / "Criteria not met"

Meaning: The plan covers the drug, but your documentation didn't meet the insurer's checklist. This is fixable.

Next move: Ask your clinician to rework the PA with the insurer's written criteria in hand. You generally have at least 180 days to appeal under Department of Labor rules.

"Step therapy required" / "Must try [other drug] first"

Meaning: The plan covers GLP-1 but requires you to try cheaper options first.

Next move: Get the written step-therapy criteria from HR or the insurer, meet them, and resubmit. Our guide on bypassing step therapy covers this in full.

"Not covered for this diagnosis"

Meaning: You've been coded wrong, or you genuinely don't meet FDA-approved indications.

Next move: Talk to your prescriber about diagnosis coding. If you have comorbidities (hypertension, prediabetes, sleep apnea, cardiovascular disease), the diagnosis framing may change.

The honest part: If your plan is a true exclusion, one email to HR probably isn’t going to create coverage this month. Employer change is slower than appeals. Coverage usually moves at the next plan year renewal. Ro, Embody, Sesame Care, and others exist specifically to bridge this gap. We’ll cover that in the “if they say no” section.

Related: How to bypass step therapy for GLP-1 · How to check if GLP-1 is covered by insurance

Step 2 — Self-funded vs. fully-insured (the question that changes everything)

About 67% of covered U.S. workers are in self-funded plans per the KFF 2025 Employer Health Benefits Survey — meaning the employer pays medical claims directly and only hires an insurance company (Aetna, Cigna, UnitedHealthcare, BCBS) to administer them. In self-funded plans, your employer makes the coverage decision. In fully-insured plans, the insurer and state mandates do, and your employer has less room to move.

The 3-question self-funded vs. fully-insured test

- Does your employer have 1,000+ employees? If yes, self-funded is more likely.

- Does your Summary Plan Description call the insurer “claims administrator” or “insurer”? “Claims administrator” = self-funded. “Insurer” = fully-insured.

- Ask HR directly: “Is our health plan self-funded or fully-insured?” They’ll tell you in one email.

| Plan type | Who decides coverage | How to frame your ask |

|---|---|---|

| Self-funded (most large employers, ERISA-governed) | Your employer, annually at renewal | Go to HR/benefits directly with ROI memo — this is the high-leverage ask |

| Fully-insured (smaller employers, state-regulated) | Insurer + state mandates | Ask about a rider, a buy-up option, or switching carriers at next renewal |

| Self-funded + Integrated HRA | Employer, within IRS/ACA rules | Ask for an excepted-benefit HRA as a compromise pathway |

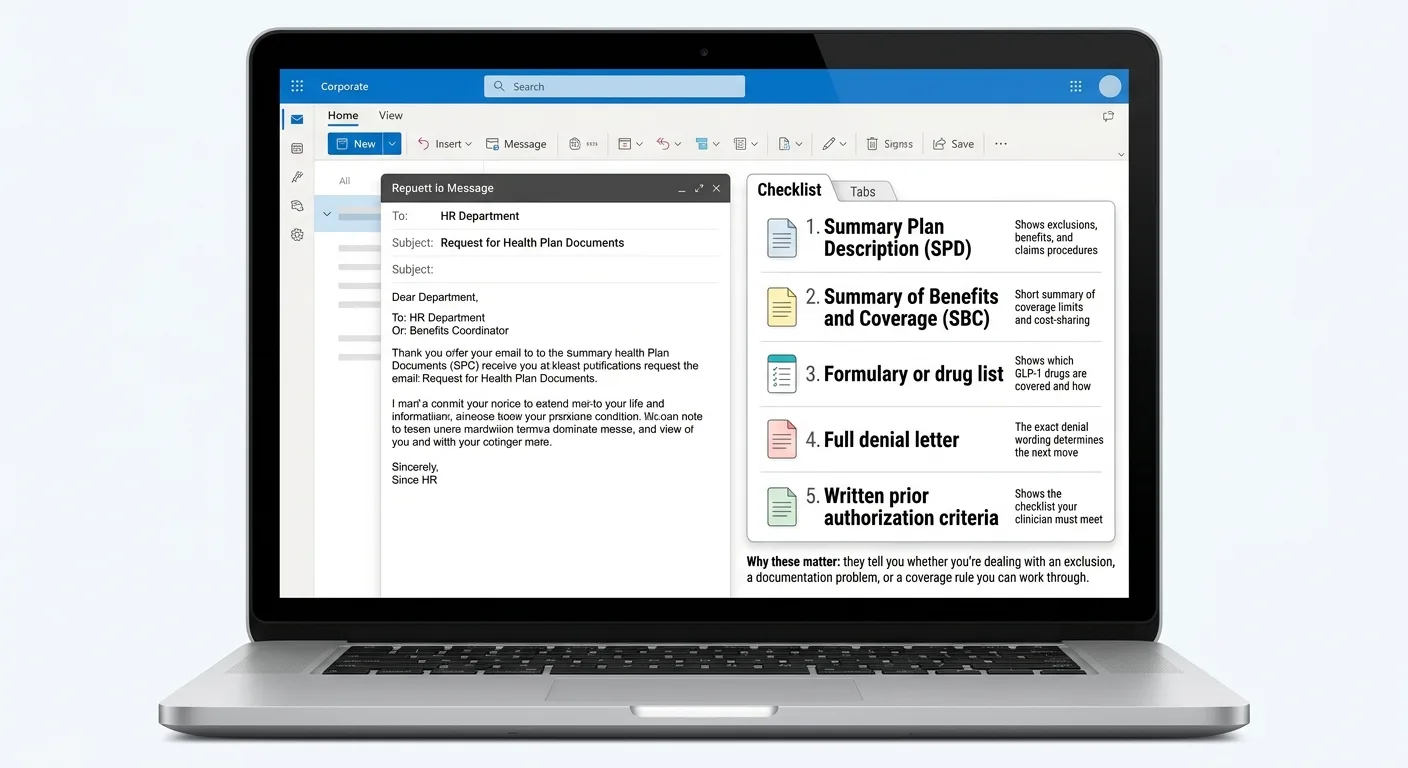

The 5 documents to request before you email HR

Answer capsule: Do not email HR asking for coverage before you have your actual plan documents in hand. Requesting the Summary Plan Description, Summary of Benefits and Coverage, formulary, your full denial letter, and the written prior authorization criteria takes one email and completely changes your approach. It’s the difference between a vague plea and a targeted business request.

The Department of Labor confirms you have a legal right to the Summary Plan Description (SPD) free of charge, and plans must also provide a Summary of Benefits and Coverage (SBC) that accurately describes what’s covered. Asking for these isn’t weird. It’s your right.

Summary Plan Description (SPD)

The full document. Look for the "Exclusions" section and any language about "weight loss," "anti-obesity," or "weight management medications."

Summary of Benefits and Coverage (SBC)

A standardized short form. Less detail than the SPD but faster to scan. Required by law to be accurate.

Formulary or prescription drug list

Tells you which GLP-1s are on the plan, at what tier, with what restrictions. Check: Wegovy, Zepbound, Foundayo, Ozempic, Mounjaro, Saxenda, Rybelsus.

Your full denial letter

Most people only read the first page. The exact phrase matters. "Not a covered benefit" behaves very differently from "does not meet medical necessity criteria." Read to page 3.

Written prior authorization criteria

If PA is required, the insurer has to tell you what it is. Most publish it online in a "medical policy" or "coverage determination" document.

The one email that gets you all five

Subject: Request for plan documents — pharmacy benefit review

Hi [HR contact],

I’m reviewing my pharmacy benefits and would appreciate copies of the following for the current plan year: the Summary Plan Description, the Summary of Benefits and Coverage, the current prescription drug formulary, and — if applicable — any written prior authorization criteria for GLP-1 medications. If our pharmacy benefits are administered by a PBM (Express Scripts, CVS Caremark, Optum Rx), the PBM’s medical policy document for GLP-1s would also be useful.

Happy to clarify if helpful. Thanks in advance.

[Your name]

What to look for once you have them

- In the SPD Exclusions section, phrases that indicate a hard exclusion: “weight loss medications excluded,” “anti-obesity medications not covered,” “drugs used for weight management excluded.”

- In the formulary, whether any GLP-1 appears at all, and at what tier. Specialty tier (Tier 4 or 5) often means high copay or coinsurance even if the drug is technically “covered.”

- In the denial letter, the exact reason code. The specific cited policy or plan section is usually buried on page 2 or 3. Our GLP-1 insurance coverage guide walks through how to read a denial line by line.

- In the PA criteria, the exact BMI thresholds, comorbidity requirements, and step-therapy rules. You want to know if you already meet them or need additional documentation.

When to ask: the pre-renewal window nobody tells you about

Answer capsule: Most employer health plans lock their design 3 to 4 months before the plan year starts. For a January 1 renewal (the most common), that means July through September is your window. Asking in December is too late for next year. Know your renewal date — it’s on your Summary Plan Description — and work backward.

| Timeline before renewal | What's happening on the employer side | Your window? |

|---|---|---|

| 150+ days out | Broker/consultant analysis; plan-design options modeled | Good — get on record early |

| 90–120 days out | Plan design decisions typically get locked | ✅ Best window — ask now |

| 60–90 days out | Open enrollment communications drafted | Narrow — push for exceptions |

| 30–60 days out | Open enrollment opens | Too late for current year |

| 0–30 days out | Final enrollment; no more changes | Next cycle only |

Three scenarios, three timelines

Renewal is 3–4 months away

Send the ask now. Coverage can start at renewal.

Renewal is 6–12 months away

Send now anyway. You want to be on the list before the broker meeting.

Renewal just happened

Still send it. Ask about mid-year exception options (HRA, excepted benefit HRA), and get yourself on record for next cycle. Paper trail matters.

How to ask your employer to cover GLP‑1 (the email that actually gets read)

Answer capsule: The email that gets HR to act is short, document-based, and professional. Four paragraphs: (1) the ask in one sentence, (2) the business case in 2–3 bullets, (3) a structural proposal that de-risks the decision, (4) a 15-minute meeting request with the plan documents attached.

The 4-paragraph structure

The ask in one sentence. Clear, specific, no preamble.

The business case in 2–3 bullets. Use data, not feelings. Peer coverage percentages. Workforce demand. Structural guardrails.

A structural proposal that de-risks it. Give HR a path to yes — a tiered coverage model, an HRA, a pilot. Something they can approve without open-ended financial exposure.

The meeting ask + the attachments. 15 minutes. Bring the documents. Offer to include other interested colleagues.

Variant A — Self-funded employer, no GLP-1 weight-loss coverage (highest-leverage situation)

Subject: Proposal — GLP-1 coverage at next plan-year renewal

Hi [HR contact],

I’d like to formally request that our next plan year add coverage for FDA-approved GLP-1 medications used for chronic weight management — Wegovy (semaglutide), Zepbound (tirzepatide), and Foundayo (orforglipron, FDA-approved in April 2026).

Three data points for the business case:

- 43% of employers with 5,000+ workers cover GLP-1 for weight loss in their largest plan per KFF 2025; Mercer’s 2026 findings show 49% of employers with 500+ employees cover GLP-1s for obesity. Not covering is increasingly the minority at peer-sized firms.

- 44% of large employers say GLP-1 coverage is “important” or “very important” to their employees (KFF 2025). Benefits competitiveness affects retention and recruiting.

- Coverage can be structured with clinical guardrails — BMI thresholds, wellness-program participation, step therapy, quarterly utilization review — so exposure is predictable. 96% of employers currently covering use prior authorization; 88% require BMI minimums; 60% require obesity plus a chronic comorbidity per IFEBP 2025.

I’d welcome a 15-minute conversation to discuss structural options — a tiered coverage design, a rider, or an Excepted Benefit HRA of up to $2,200/year per IRS 2026 limits as a compromise middle ground. I’ve attached a one-page ROI summary with the peer-coverage and utilization-management data.

Happy to coordinate with other interested colleagues if that’s helpful.

Best, [Your name]

Variant B — Fully-insured plan

“...Because our plan is fully-insured, I recognize the carrier’s formulary and state insurance rules drive much of the design. I’d welcome a conversation about whether adding a rider, exploring a carrier that includes GLP-1 coverage at the next renewal, or offering an Excepted Benefit HRA as a supplemental benefit would be feasible.”

Variant C — Plan covers GLP-1 for diabetes, excludes for weight loss

Variant D — Open enrollment / new hire plan selection

Clinician letter prompt — what to send your doctor

Hi Dr. [name],

I’m asking my employer to consider adding coverage for GLP-1 medication for chronic weight management. Could you write a brief letter of medical necessity I can include with the request? If helpful, it should cover: current BMI, any comorbidities (hypertension, prediabetes, sleep apnea, cardiovascular risk), prior weight-loss attempts and outcomes, why GLP-1 therapy is medically appropriate in my case, and that this is the recommended treatment per current obesity medicine guidelines.

Thanks so much.

What NOT to say in any of these emails

| What not to say | Why it backfires |

|---|---|

| "Other people are on it and I deserve it too." | Weak. Personal. No business case. |

| "You cover bariatric surgery that costs way more." | True, adversarial, makes HR defensive. |

| "If you don't cover this, I'll leave." | Only if you genuinely mean it. Otherwise ignored. |

| "This is discrimination." | Don't raise unless you've talked to an attorney. It changes the conversation from benefits design to legal risk. |

| Apologies, minimizing, excessive preamble. | Signals low confidence. Weakens the ask. |

The business case that actually moves HR

Answer capsule: HR didn’t deny your coverage. Finance did. Your ask needs to speak Finance’s language — cost per member per year, structural guardrails to prevent utilization runaway, retention/recruiting value, and a tiered path that lets the employer say yes without open-ended exposure.

What your employer is actually worried about

Cost

Net cost per covered GLP-1 user runs approximately $617–$766/month per EBRI modeling — after rebates and PBM dynamics. Average employer-sponsored health cost hit $17,496 per employee in 2025 per Mercer, with Rx up 9.4%. Your letter should acknowledge this, not pretend it's nothing.

Utilization runaway

KFF's 2025 focus groups repeatedly heard employers cite unexpected utilization. GLP-1 year-over-year spend grew 50% at one large manufacturer. IFEBP found GLP-1s made up 10.5% of total annual claims at employers that cover them, with 27% of employers saying GLP-1 costs exceeded 15% of annual claims.

Precedent

"If we add this, what's next?" Address this by proposing a narrow, well-defined benefit — not open-ended future commitments.

ROI timing

The CBO estimates net obesity-treatment costs exceed savings for roughly 10 years. Most HR budgets aren't measured on 10-year horizons. Frame your ROI around retention, recruiting, productivity, and the wellbeing-competitive landscape.

The four structural compromises — give HR a path to yes

| Compromise tier | What it means in practice | Why it de-risks the decision |

|---|---|---|

| Tier 1 — Full coverage with guardrails | Cover GLP-1 with BMI thresholds (≥30, or ≥27 with comorbidity), prior authorization, step therapy, and quarterly utilization review | 96% of current employer GLP-1 plans use PA; 88% require BMI minimums; 60% require comorbidity |

| Tier 2 — Excepted Benefit HRA | Employer funds up to $2,200/year (IRS 2026 limit) for employees to buy non-covered benefits — including GLP-1 if the plan is designed for it | Fixed employer cost; no claims exposure; employees choose their own pharmacy |

| Tier 3 — Pilot program | Cover GLP-1 for a defined cohort (e.g., employees in a company wellness program) for one plan year with a utilization review at month 6 | Time-limited commitment; creates evidence base for full adoption decision |

| Tier 4 — Wellness-linked formulary exception | Employees who complete a certified weight-management program qualify for a formulary exception or reduced tier placement | Aligns cost with outcome; reduces off-label or casual-use claims |

A Reddit thread about a successfully added employer GLP-1 benefit put it this way: “What moved them was not the weight loss argument.” The business case moves decisions, not the personal case.

If they say no: 5 bridge options for 2026

If HR says no today — or says “not this cycle” — you have five legal paths to stay on therapy while the employer conversation continues. These aren’t workarounds. They’re the options the system actually built for this situation.

Option 1 — HSA or FSA self-pay

Tax-advantagedGLP-1 prescribed for a diagnosed medical condition is eligible for both HSA and FSA funds per IRS Publication 502. You still pay list or cash price, but you save your marginal tax rate (typically 22–35%). An HSA is your personal account; an FSA is employer-established with use-it-or-lose-it rules. Confirm with your plan administrator before claiming.

Best fit: You have savings in your HSA, you’re in a higher tax bracket, and you’re comfortable with cash-pay medication while the employer conversation continues.

Option 2 — Excepted Benefit HRA

Ask HR about thisAn Excepted Benefit HRA (EBHRA) lets your employer fund up to $2,200/year (IRS 2026 limit) for employees to use on non-covered benefits — including, with proper plan design, GLP-1 medications. This is a specific compromise you can propose to HR that doesn’t require changing the main plan design.

Best fit: Your employer is open to a compromise but won’t change the main formulary. A good option if your employer already offers HRA products or works with a benefits administrator that supports EBHRAs.

Option 3 — Manufacturer savings programs

Brand-name, lower costWegovy Savings Card (Novo Nordisk): eligible commercially-insured patients can pay as little as $25/month under current NovoCare offers, subject to eligibility and terms. Uninsured/self-pay: Wegovy pill starts at $149/month for certain doses; Wegovy pen $199/month for first two fills at starter doses. Verify current pricing at NovoCare.com.

Zepbound Savings Card (Eli Lilly): eligible commercially-insured patients get similar savings support. LillyDirect offers self-pay Zepbound vials. Verify current pricing at LillyDirect.com.

Best fit: You want the FDA-approved brand-name version with the cleanest regulatory profile, and you qualify for the manufacturer savings program.

Option 4 — FDA-approved telehealth

Ro & Sesame CareIf you want brand-name FDA-approved GLP-1 with a faster, insurance-friendly path than going back through your doctor and your plan:

Ro — Zepbound® & Foundayo™

Ro carries FDA-approved branded GLP-1s and can work with your existing insurance when eligible, handling the prior authorization for you. Get started for $39, then as low as $74/month with annual plan paid upfront. Medication priced separately.

Check eligibility on Ro → (sponsored affiliate link, opens in a new tab)$39 to start · Commercial insurance only for concierge · Verified April 2026

Sesame Care — FDA-approved only

Marketplace-style approach with transparent upfront pricing for branded GLP-1 access. Success by Sesame starts at $59/month with annual subscription; medication costs handled separately.

See Success by Sesame → (sponsored affiliate link, opens in a new tab)Option 5 — Licensed-pharmacy compounded GLP-1

Cash-pay, lower costEmbody — broad default for most readers

Cash-pay and advertised HSA/FSA eligible, offering compounded semaglutide and tirzepatide injections plus a needle-free GLP-1 gum, with a cancelable subscription. If you want a low first-month price without locking into one modality, this is usually where we route. Availability varies — check availability in your state during intake.

Check Embody Eligibility → (sponsored affiliate link, opens in a new tab)From $99 first month (sema injection), $299/mo ongoing · GLP-1 gum from $149/mo · HSA/FSA eligible · No lock-in · Verified June 11, 2026

Embody’s shipped compounded GLP-1 options are not FDA-approved finished drugs. A licensed provider determines whether treatment is medically appropriate. Prices, pharmacy availability, shipping timelines, and state eligibility can change and should be confirmed during intake. Last verified June 11, 2026.

SHED — specialist pick for oral/needle-free

Best if you’re interested in Foundayo (orforglipron), oral semaglutide options, or the newer Wegovy pill formats and want a specialist provider focused on that modality.

Check SHED eligibility → (sponsored affiliate link, opens in a new tab)MEDVi — deepest compounded menu

Injections, tablets, multiple dosing formats — cash-pay with HSA/FSA language. Best if you want breadth of options in one place.

See MEDVi options → (sponsored affiliate link, opens in a new tab)SkinnyRx — value-oriented option

Particularly for oral tablet and HSA/FSA access at lower price points. Honest disclosure: we include SkinnyRx as a cost-focused option, not as our recommendation for the cleanest safety/regulatory profile. It’s a different risk/cost tradeoff than Embody or SHED.

See SkinnyRx pricing → (sponsored affiliate link, opens in a new tab)| Your situation | Best bridge fit |

|---|---|

| Cost is the only barrier, OK with compounded | Embody (broad default) |

| Want FDA-approved only, want PA handled | Ro (concierge + cash-pay fallback) |

| Want FDA-approved only, oral preference | Sesame Care or SHED |

| Want deepest compounded menu | MEDVi |

| Cost-first, oral tablet, comfortable with tradeoffs | SkinnyRx |

| Want brand-name, already have savings card | NovoCare / LillyDirect directly |

| Have substantial HSA funds | Use HSA at any pharmacy; no affiliate revenue to us |

Frequently Asked Questions

Can my employer legally refuse to cover GLP-1 for weight loss?▾

Yes. Federal law — including ERISA — does not require employer-sponsored plans to cover GLP-1 for weight loss. Only North Dakota has a state-level benchmark requirement as of April 2026, and it applies to certain fully-insured individual and small-group plans; it does not generally control self-funded employer plans. Most employers can legally exclude GLP-1 for weight loss while still covering it for diabetes.

Should I ask HR or my insurance company first?▾

It depends on what your denial says. If it's an exclusion ('not a covered benefit,' 'weight-loss medications excluded'), HR owns the problem — it's benefit design. If it's a prior authorization denial or medical necessity denial, the insurer owns it — your clinician needs to rework the PA. Read the denial letter carefully before you send anything.

Do I have to disclose my BMI or weight to ask for coverage?▾

No. You can frame the entire request as a plan-design conversation — 'I'd like to see GLP-1 for chronic weight management covered at the next renewal' — without sharing your personal clinical details. Keep it in the framework of workforce benefit improvement. Share personal context only if you choose to.

How long does it actually take for an employer to add coverage?▾

Typically the next plan year. Ask 3–4 months before renewal and coverage can start at the next plan year. Ask after renewal is locked and you're usually waiting for the following year. At larger employers, benefit design can be planned 1 to 3 years in advance, so getting on record early still matters even if the immediate answer is no.

What's the difference between 'excluded' and 'prior authorization denied'?▾

Huge difference. 'Excluded' means the plan doesn't cover the drug for your use, period — appeals rarely work because there's no medical-necessity path when the benefit doesn't exist. 'PA denied' means the plan covers the drug but your documentation didn't meet the criteria — your clinician can rework the PA, and you usually have 180 days to appeal under DOL rules.

Can my doctor write a letter of medical necessity for my employer?▾

Yes, and it helps. A clinician letter isn't required for a benefits-design request, but it adds professional weight. Keep it clinical: BMI, comorbidities, prior attempts, rationale for GLP-1, why alternatives aren't sufficient. For a true plan exclusion, the letter won't create coverage this month — but it becomes part of the record for the next renewal discussion.

Can I use my HSA or FSA if my plan doesn't cover GLP-1?▾

Generally yes. GLP-1 prescribed for a diagnosed medical condition — including chronic weight management meeting BMI criteria — is eligible for both. An HSA is your personal account (you own it); an FSA is employer-established, so reimbursement follows your employer's FSA rules. You still pay list or cash price, but you save your marginal tax rate (typically 22–35%). Confirm with your plan administrator.

What if several coworkers and I all ask together?▾

A coordinated group ask is one of the most effective tactics. Employers track request volume. Five letters within two weeks lands very differently than one. Each person should write their own letter (no copy-paste), and the group approach should be parallel professional requests, not coordinated pressure.

Does Medicare cover GLP-1 for weight loss?▾

Not directly. Federal law has long prohibited Medicare from covering drugs used for weight loss. Medicare Part D covers GLP-1 for diabetes and certain cardiovascular and kidney indications. A limited Medicare/Medicaid GLP-1 demonstration program is expanding access through specific pathways during 2026, but broad weight-loss coverage for Medicare is still not available.

What's the single most effective thing I can do right now?▾

Request your five plan documents (SPD, SBC, formulary, full denial letter, PA criteria). Confirm whether your denial is an exclusion or a PA issue. Time your ask to land in the pre-renewal window. Send the letter with clinician support and the 4-tier compromise proposal. And if they say no, explore bridge options like HSA/FSA self-pay, manufacturer savings programs, or an FDA-approved telehealth provider.

Your next step

If you’re ready to ask your employer:

Download the free 2026 Employer Coverage Advocacy Kit — 4 letter variants, one-page ROI memo, document-request email, doctor-letter prompt, and the plan-type diagnostic flowchart. Personalize in about 15 minutes.

Get the Advocacy Kit →If you’re not sure what your denial means or which bridge fits you:

Take our free 60-second matching quiz. We’ll route your exact situation to the right next move — and the right provider if that’s where this ends.

Take the Quiz →If you already know what you want and just need a clean path: our GLP-1 provider comparison ranks every 2026 telehealth option by price, medication type, and reader fit. Related guides: how to get insurance to cover GLP-1, how to check if GLP-1 is covered, and how to bypass step therapy.

Related Guides

About this page

This page is researched and maintained by The RX Index editorial team. We verify pricing, medication sourcing, regulatory status, and provider terms on a rolling quarterly basis.

Not medical, legal, or tax advice

GLP-1 medications have risks. See FDA prescribing information for Wegovy (which includes a boxed warning for risk of thyroid C-cell tumors) and Zepbound before starting any medication. Consult a licensed clinician for medical decisions, an employment attorney for legal questions about plan exclusions or disability claims, and a tax professional for HSA/FSA or HRA questions specific to your situation.

© 2026 The RX Index. All rights reserved. This page is reviewed and updated regularly as employer benefit policies change. Last comprehensive review: April 2026.