Is Wegovy HRA Eligible?

Usually yes. Sometimes no. The difference comes down to how your employer designed the HRA — not what the IRS allows.

Published:

By The RX Index Editorial Team • Last verified: April 17, 2026 • Published April 17, 2026

Not medical, legal, or tax advice. Talk to your plan administrator, benefits manager, and tax professional about your specific situation.

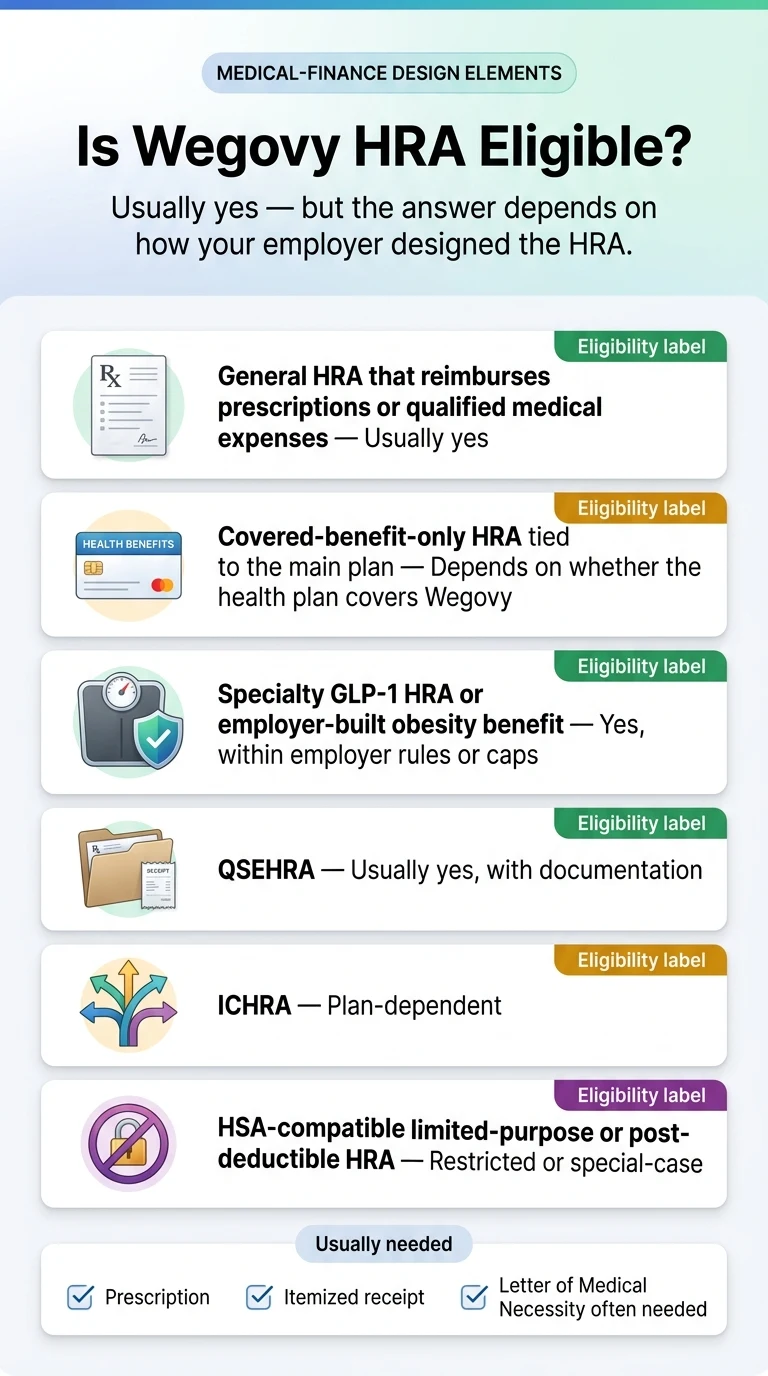

Yes — Wegovy is HRA eligible in most cases.

But the answer depends on how your employer set up the HRA, not just what the IRS allows. If your HRA reimburses prescription drugs or qualified medical expenses generally, Wegovy usually qualifies with a prescription, an itemized receipt, and often a Letter of Medical Necessity. If your HRA only reimburses cost-sharing for benefits your medical plan already covers, and your plan excludes Wegovy, the HRA probably can’t help — even though the IRS would otherwise allow it.

Quick eligibility table

| Your HRA setup | Wegovy reimbursable? | Why |

|---|---|---|

| General HRA that pays prescriptions or qualified medical expenses | Usually yes | IRS counts prescribed Wegovy as a medical expense when treating a diagnosed condition |

| Covered-benefit-only HRA tied to main plan | Often no if plan excludes Wegovy | Plan design overrides the IRS rule |

| Specialty GLP-1 HRA (employer-built obesity benefit) | Yes, within plan caps | Wegovy is the whole point of the design |

| QSEHRA (small employer, under 50 FTE) | Usually yes, with documentation | Reimburses Section 213(d) medical expenses |

| ICHRA (any employer size) | Plan-dependent | Some reimburse premiums only; some include medical expenses |

| HSA-compatible limited-purpose HRA | Usually no for the medication | Designed for dental/vision/preventive only |

| HSA-compatible post-deductible HRA | Yes, but only after HDHP deductible met ($1,700 self / $3,400 family in 2026) | Designed to preserve HSA eligibility |

Tell us your HRA setup, insurance status, and state — we’ll route you to the cleanest path.

What we actually verified for this page:

- IRS Publication 502 (Medical and Dental Expenses, 2025 edition) and IRS Publication 969 (HSAs and Other Tax-Favored Health Plans, 2025)

- IRS Revenue Procedure 2025-19 and Notice 2026-5 (2026 contribution limits)

- HealthCare.gov definitions for HRA, QSEHRA, and Individual Coverage HRA

- HealthEquity’s HRA Qualified Medical Expense list

- Three real 2025–2026 employer plan documents: Vermont Education Health Initiative (VEHI), Stillwater Area Public Schools, and Washington University in St. Louis

- NovoCare Pharmacy Terms and Conditions of Use and current Wegovy self-pay pricing

- FDA prescribing information for Wegovy injection (label revised 2026) and Wegovy tablets (2025 approval)

- Sentinel Group’s GLP-1 specialty HRA program

- Akerman LLP, “HRx: GLP-1s and Employer Health Plans” (February 2026); Sequoia Consulting Group, “GLP-1 Coverage: Group Health Plan Considerations”

Sources linked inline. Anything we couldn’t independently confirm is marked or omitted. Verified April 17, 2026.

Is Wegovy HRA Eligible? Here’s What Actually Determines the Answer

Both “yes” and “no” can be true at the same time. The IRS treats prescribed Wegovy as a qualified medical expense, which means an HRA can legally reimburse it. But your employer still controls which qualified expenses your specific HRA actually pays. That’s why one employee reimburses a $349 Wegovy fill in five minutes, and another gets denied for the same medication.

The IRS sets the floor

Under Section 213(d) and IRS Publication 502, prescribed medications used to treat diagnosed medical conditions count as qualified medical expenses. For weight-loss medications specifically, the treatment must be for a specific disease diagnosed by a physician — such as obesity, hypertension, or heart disease. Wegovy’s FDA-approved indications match those exactly.

Your employer sets the actual menu

An HRA is funded entirely by your employer. They choose what the HRA reimburses within IRS guardrails — either “any qualified medical expense” (broad) or “your share of costs for benefits already covered under the medical plan” (narrow). Same IRS rules. Two completely different answers when you submit a Wegovy receipt.

The mismatch is real and recent

In January 2026, the Vermont Education Health Initiative (VEHI) sent a notice to school employees explaining that GLP-1 medications for weight loss had been removed from the underlying health plan — and because the HRA only covers benefits the medical plan already covers, the HRA stopped reimbursing weight-loss GLP-1 prescriptions too, even though the IRS would otherwise allow it. Meanwhile, Stillwater Area Public Schools tells employees they may still use HRA or FSA dollars for GLP-1 medications even after obesity-use coverage ended on the underlying plan. Washington University in St. Louis built a separate HRA subsidy of up to $350 per month specifically for Wegovy and Zepbound.

Three employers. Same IRS rules. Three different answers for the same medication.

Which HRA Do You Actually Have?

There are six common HRA designs in use in 2026, and each one produces a different Wegovy answer. Identifying yours takes about two minutes — check your benefits portal, your summary plan description, or call HR and ask the question at the end of this section.

1. General HRA that reimburses qualified medical expenses

Usually yesThe most common design and the friendliest one for Wegovy. The HRA reimburses any qualified medical expense the IRS recognizes under Section 213(d), which includes prescription drugs.

2. Covered-benefit-only HRA (the one that traps people)

Depends on planTied directly to your major medical plan. It only reimburses your share of costs for benefits the plan already covers. If the plan covers Wegovy, the HRA can pay your copay or coinsurance. If the plan excludes Wegovy, the HRA can’t override that exclusion.

3. Specialty GLP-1 HRA / employer-created subsidy

Yes, within capsA growing 2026 design. The employer carves out a separate reimbursement lane specifically for GLP-1 medications, usually with annual or monthly caps, often tied to designated pharmacy or manufacturer channels.

4. QSEHRA (Qualified Small Employer HRA)

Usually yesFor employers with fewer than 50 FTEs that don’t offer group health coverage. Reimburses individual health insurance premiums and qualified medical expenses tax-free. You must maintain minimum essential coverage to be eligible. 2026 cap: $6,450 individual / $13,100 household.

5. ICHRA (Individual Coverage HRA)

Plan-dependentAvailable to employers of any size. Provides tax-free dollars to buy your own individual health insurance, plus optionally to cover qualified medical expenses. The Wegovy answer depends on whether the ICHRA reimburses only premiums or premiums plus medical expenses.

6. HSA-compatible HRA (limited-purpose or post-deductible)

RestrictedTwo variants, both designed to preserve your ability to contribute to a Health Savings Account.

The one question to ask HR right now:

“Does our HRA reimburse prescription drugs that are qualified medical expenses under IRS rules generally, or only my share of costs for benefits the medical plan already covers?”

That single question gives you a fast read on which bucket your HRA falls into.

Is Wegovy a Qualified Medical Expense Under IRS Rules?

Yes. IRS Publication 502 lists prescribed medicines as qualified medical expenses, and the IRS separately confirms that an HRA can reimburse Section 213 medical expenses including prescription drugs. For weight-loss medications specifically, the IRS adds a layer: the prescription must be treating a specific disease diagnosed by a physician.

Two IRS rules matter here

The prescription rule

Under Section 213(d), prescribed medicines and drugs are qualified medical expenses. Broad and uncontroversial. An HRA can legally reimburse any qualified medical expense the plan permits — and prescriptions are squarely on the list.

The weight-loss rule

Publication 502 specifically addresses weight-loss expenses: costs are deductible (and therefore reimbursable from an HRA, FSA, or HSA) only when the weight-loss treatment is for a specific disease diagnosed by a physician — including obesity, hypertension, or heart disease. Costs for “the improvement of appearance, general health, or sense of well-being” are not deductible.

Wegovy’s FDA-approved indications overlap cleanly with the IRS’s qualifying diseases

- Reducing the risk of major cardiovascular events in adults with established cardiovascular disease who are overweight or obese

- Chronic weight management in adults with obesity or overweight with at least one weight-related comorbid condition

- Weight management in children 12 and older with obesity

- Noncirrhotic MASH with moderate to advanced liver fibrosis in adults with obesity

The Wegovy tablet (FDA-approved December 2025) currently carries the adult cardiovascular risk reduction and adult weight management indications. If your prescription documents one of these, you’ve cleared the IRS bar.

Compliance note: This guide covers brand-name FDA-approved Wegovy® manufactured by Novo Nordisk. Compounded semaglutide is a separate regulatory category with its own eligibility considerations — we treat them as distinctly different products throughout. See our compounded semaglutide HSA guide for that landscape.

When Does Your Employer’s HRA Design Override the IRS Rule?

The IRS rule sets the floor for what can be reimbursed; your employer’s HRA plan document sets what will be reimbursed. The most common override is a “covered benefits only” HRA that pays only for cost-sharing on benefits the medical plan already covers. If the plan excludes Wegovy, the HRA can’t override that exclusion.

Override 1: “Covered benefits only” — the VEHI example

The Vermont Education Health Initiative (VEHI) HRA pays for “covered prescriptions and covered medical services” and explicitly states the HRA cannot be used for non-covered benefits. When VEHI’s underlying health plan stopped covering GLP-1s for weight loss in early 2026, the HRA stopped too — even though the IRS would otherwise allow reimbursement of prescribed Wegovy.

Source: VEHI plan notice to school employees, January 2026.

Override 2: “Designated channels only” — the WashU example

Washington University in St. Louis built a separate HRA subsidy that reimburses up to $350 per month for Wegovy or Zepbound, but only when purchased through designated manufacturer channels. Buying the same medication from a non-designated telehealth provider wouldn’t qualify. The eligibility is real, but the channel restriction shapes how you access the benefit.

Source: WashU HR plan documents, 2025–2026 plan year.

Override 3: “After-coverage workaround” — the Stillwater example

Stillwater Area Public Schools’ GLP-1 employee guide tells employees that even after the underlying plan ended GLP-1 coverage for obesity, employees may still be able to use HRA or FSA dollars for GLP-1 medications. This works because Stillwater’s HRA reimburses qualified medical expenses generally, not just covered-plan-benefits.

Source: Stillwater Area Public Schools GLP-1 Resource Guide for Employees.

If your card was declined or your claim denied, the first thing to check isn’t whether Wegovy is “eligible” in the abstract — it’s whether your specific HRA permits reimbursement of qualified medical expenses generally, or whether it’s restricted to covered-plan-benefits only.

Do You Need a Letter of Medical Necessity for Wegovy HRA Reimbursement?

Often yes. A Letter of Medical Necessity (LMN) is a one-page document from your prescriber that states your diagnosis and confirms Wegovy is medically necessary to treat it. Many HRA administrators request an LMN for weight-loss medications because the IRS rule for weight-loss expenses is diagnosis-based — not just prescription-based. HSAs rarely require one at the point of sale; FSAs and HRAs frequently do.

| Situation | LMN needed? |

|---|---|

| Routine prescription reimbursement, receipt shows Rx | Usually not required, but good to have |

| Weight-loss medication claim (any HRA) | LMN recommended |

| First-time Wegovy submission | LMN recommended |

| Prior denial or dispute | LMN required for appeal |

| Receipt doesn’t show a diagnosis code | LMN required |

A strong Wegovy LMN includes seven elements:

- Patient name and date of birth

- Date of letter

- Specific diagnosis with ICD-10 code (E66.01 morbid obesity, E66.09 other obesity, I10 hypertension, I25 atherosclerotic heart disease are common)

- A statement that Wegovy is being prescribed to treat the diagnosed condition — not for cosmetic weight loss

- Brief clinical rationale

- Expected duration of treatment

- Prescriber’s signature, license, and NPI

Most LMNs are valid for 12 months.

What Documents to Submit with a Wegovy HRA Claim

The cleanest claim packet has three pieces: an itemized pharmacy receipt, a copy of your prescription or prescription label, and a Letter of Medical Necessity if your administrator requires one. Reimbursement-style HRAs also need proof of payment. Submit through your administrator’s portal — HealthEquity, Inspira Financial, Optum, Navia, or whoever administers your plan.

| Document | When needed | Why it matters | Denial it prevents |

|---|---|---|---|

| Itemized pharmacy receipt | Always | Confirms what was purchased and the price | “Insufficient documentation” |

| Prescription label or copy | Most claims | Confirms the medication was prescribed, not OTC | “Not a prescribed medication” |

| Letter of Medical Necessity | Often for weight-loss meds | Ties Wegovy to a diagnosed condition, not wellness | “General wellness, not eligible” |

| Proof of payment | Reimbursement HRAs | Confirms you paid out of pocket | “Already reimbursed elsewhere” |

| Plan excerpt / denial notice | When appealing | Shows the HRA was supposed to cover this | Reverses denial-on-design grounds |

| Proof of minimum essential coverage | QSEHRA | Confirms your eligibility | “Not eligible employee” |

Itemized receipt standard (Optum Bank and HealthEquity both require these five elements):

- Provider or pharmacy name

- Patient name

- Description of the service or medication

- Date of service

- Amount charged

Build your receipt check around those five and you’ll clear most administrator documentation bars.

What If Your HRA Card Is Declined — or Approved and Then Clawed Back?

A decline usually means a substantiation problem at checkout, not an eligibility problem. A claim denial usually means missing documentation, a plan-design exclusion, or an administrator interpretation. Each has a specific fix. And there’s one scenario most pages skip entirely: your card can approve at the pharmacy and the employer can later deem the expense ineligible and require repayment.

Bucket 1

Card couldn’t substantiate at checkout

Your HRA card hit a merchant or product code it couldn’t auto-approve, even though the expense is eligible.

Fix: Pay with a personal card and submit the same expense for reimbursement with your itemized receipt and an LMN if needed. Most common cause of a card decline.

Bucket 2

Missing or insufficient documentation

The administrator wants more proof of medical necessity or expense eligibility.

Fix: Add an LMN if you didn’t include one. Make sure your receipt has all five administrator-expected elements. Resubmit through the portal.

Bucket 3

Plan-design exclusion

Your HRA can’t cover this expense because of how the employer designed it — typically a covered-benefits-only HRA paired with a plan that excludes Wegovy.

Fix: This one is unwinnable through appeal. The HRA isn’t broken; it’s working as designed. Switch payment paths using the chooser at the end of this guide.

Bucket 4

Administrator interpretation

The administrator denied based on a judgment call, often citing “weight loss is general wellness, not medical.”

Fix: Appeal with an LMN that explicitly cites the IRS Pub 502 diagnosis-based standard for weight-loss treatment expenses. Reference your specific diagnosis with the ICD-10 code.

The scenario almost nobody warns you about: approved, then clawed back

VEHI’s January 2026 notice documents the reverse problem. A pharmacy’s point-of-sale system can approve an HRA card for a prescription that qualifies under IRS rules — but the employer’s HRA design may treat it as ineligible after the fact. Employees who used HRA cards for GLP-1 weight-loss prescriptions were told that because those medications are no longer covered under the underlying plan, the HRA spending was ineligible, and reimbursement would be required.

An approved card swipe is not the same as an approved claim. If your HRA is the “covered benefits only” type and your main plan excludes Wegovy, using your HRA card at the pharmacy can create a debt to your employer months later.

Can You Use Your HRA If Your Insurance Doesn’t Cover Wegovy?

Sometimes yes — and this is the section most pages skip. If your HRA is structured to reimburse qualified medical expenses generally (not just covered benefits), you can use it for Wegovy even when the underlying medical plan excludes it.

Pattern A: Insurance excludes Wegovy, HRA still covers it

Stillwater Area Public Schools is the cleanest current example. Even after the underlying medical plan stopped covering GLP-1s for obesity, employees may still be able to use HRA or FSA dollars for the same medications because the HRA reimburses qualified medical expenses generally.

Pattern B: Insurance excludes Wegovy, employer built a specialty HRA

Washington University in St. Louis added a separate HRA subsidy of up to $350/month for Wegovy or Zepbound through designated manufacturer channels — outside the medical plan’s usual drug coverage. This is exactly the design more mid-size and large employers are adopting in 2026.

Pattern C: Insurance excludes Wegovy, HRA is also blocked

VEHI’s covered-benefits-only HRA cannot reimburse non-covered benefits, so when the medical plan stopped covering GLP-1s for weight loss, the HRA stopped too. The fix here isn’t fighting the HRA — it’s switching to a different payment path entirely.

The Wegovy Self-Pay / HRA Reimbursement Conflict Most Pages Miss

This is the most important section on this page.

If you’re using NovoCare Pharmacy’s direct self-pay program or the Wegovy Savings Offer, the official terms explicitly prohibit seeking reimbursement from any insurer — and depending on how your administrator interprets it, that may include your HRA. Confirm with your HRA administrator in writing first before combining a manufacturer self-pay price with HRA reimbursement.

NovoCare Pharmacy Terms and Conditions of Use

“Patient agrees they will not seek reimbursement or otherwise submit a claim to any insurer for any medication received through this program.”

Applies to the direct self-pay path at the advertised prices ($149 pill intro, $199 pen intro, $349 pen standard, $399 HD standard).

Wegovy Savings Offer Terms (the $25/month commercial insurance program)

“By redeeming this offer, you (and anyone else acting on your behalf) agree not to seek reimbursement from any insurance plan for out-of-pocket costs for prescriptions purchased with this offer.”

HRAs are technically group health plans

Under IRS and ERISA rules, this leans toward a conservative interpretation that NovoCare’s terms could apply to HRA reimbursement.

HSAs and FSAs are typically OK

NovoCare explicitly states FSA/HSA funds are accepted for payment at NovoCare Pharmacy. Tax-advantaged accounts you own or elect are typically not classified as insurance the same way.

The practical read

Using HSA or FSA funds to pay at NovoCare is typically fine. Using an HRA to reimburse a NovoCare self-pay purchase may or may not be, depending on how your administrator interprets the terms. The safe move is one phone call to your HRA administrator before the purchase, documenting their answer in writing through the administrator’s portal message system.

The HDHP + HSA + GLP-1 HRA Trap Most People Miss

If you have an HDHP + HSA and your employer adds an HRA that reimburses GLP-1 medications before you’ve met your HDHP deductible, you can lose HSA contribution eligibility for the entire tax year.

The IRS treats the HRA as “other health coverage” that disqualifies you from the HDHP. Two safe designs avoid this — and most employers structure them correctly, but not all.

Per IRS Publication 969: an employee covered by an HDHP and an HRA that pays or reimburses qualified medical expenses generally cannot make HSA contributions. The two main exceptions:

Safe Design 1: Limited-purpose HRA

Only reimburses dental, vision, and preventive care. Wegovy isn’t covered, so your HSA stays intact — but the HRA doesn’t help with Wegovy either.

Safe Design 2: Post-deductible HRA

Only reimburses qualified medical expenses after the HDHP deductible is met. In 2026: $1,700 for self-only, $3,400 for family (IRS Rev. Proc. 2025-19). Once you’ve spent that out of pocket, the HRA can reimburse Wegovy.

If your employer launched a “GLP-1 HRA” without making it post-deductible or limited-purpose, and you’re contributing to an HSA, the fix is three steps:

- Confirm the plan design with HR — this is the most important call you can make this quarter

- If the design disqualifies your HSA, decide whether to keep the HRA benefit or roll back HSA contributions for the year

- If you’ve already contributed to your HSA in a year you weren’t eligible, the IRS allows you to withdraw excess contributions without penalty before your tax filing deadline

Sources: IRS Publication 969 (“Other Health Coverage” section); Sequoia Consulting Group; Akerman LLP, “HRx: GLP-1s and Employer Health Plans” (February 2026).

How Much Can an HRA Actually Save You on Wegovy in 2026?

Wegovy currently costs $149 to $399 per month through Novo Nordisk’s official self-pay channels, depending on the formulation and dose. A general HRA reimbursement converts that out-of-pocket cost to tax-free employer money.

| Formulation | Self-pay price | Notes |

|---|---|---|

| Wegovy pen, 0.25–2.4 mg | $199/month for first 2 months (intro through December 31, 2026), then $349/month | Standard once-weekly injection |

| Wegovy HD pen, 7.2 mg | $399/month | Higher-dose weekly injection; no intro pricing for HD |

| Wegovy pill, 1.5 mg | $149/month | Ongoing price |

| Wegovy pill, 4 mg | $149/month through August 31, 2026, then $199/month | Higher starter dose |

| Wegovy pill, 9 mg or 25 mg | $299/month | Maintenance doses |

| With commercial insurance + Wegovy Savings Card | As low as $25/month (max $100 savings) | Government-insured patients excluded; no-insurance-reimbursement clause applies |

| Wegovy 12-month subscription (pen) | $249/month with 12-month commitment, paid upfront | Launched March 31, 2026 through Ro, WeightWatchers, and LifeMD; additional partners to follow |

Source: NovoCare Pharmacy Wegovy pricing page, verified April 17, 2026. List price for all Wegovy formulations is currently $1,349.02/month. Novo Nordisk has announced the list price will drop to approximately $675/month effective January 1, 2027.

What HRA reimbursement is worth in real dollars

A general HRA fully reimbursing Wegovy at $349/month for the standard pen converts $4,188/year of after-tax personal money into tax-free employer money — equivalent to roughly $5,400 to $6,200 in pre-tax salary depending on your bracket.

A specialty $350/month HRA (Washington University model) covers the full standard pen cost most months, with annual employer contribution of about $4,200.

An excepted-benefit HRA is capped at $2,200/year per the 2026 IRS limit — covers about four months of the standard pen or almost six months of the pill.

A QSEHRA is capped at $6,450 individual / $13,100 household for 2026. Actual employer contributions vary by plan.

For most readers, this is a $2,000 to $5,000-per-year question.

Provider-Stated vs. What We Verified (for HRA-Aware Wegovy Shoppers)

If your HRA is a good fit and you still need a provider to prescribe Wegovy, two paths are worth knowing about.

| Claim | Sesame Care | Ro |

|---|---|---|

| Provider states HSA/FSA acceptance | Yes, at checkout | “Not accepted directly — pay out of pocket and submit for reimbursement” per their FAQ |

| Provider states HRA acceptance | Yes, at checkout (on sesamecare.com/join/insured) | Not specifically named |

| Verified Wegovy cash-pay pricing | $199/mo new-patient intro, then $349/mo | $39 first month, $149/mo ongoing, as low as $74/mo with annual prepay |

| Verified itemized billing available | Yes (itemized bills on request per Sesame FAQ) | Yes (Ro publishes itemized receipts) |

| Insurance prior-authorization support | Limited | Yes — Ro publishes an insurance concierge that handles prior authorization |

| Self-pay medication source | NovoCare Pharmacy at manufacturer cash-pay prices | NovoCare Pharmacy at manufacturer cash-pay prices |

Both providers route the actual Wegovy fill through NovoCare Pharmacy at Novo Nordisk’s published self-pay prices. That means the NovoCare manufacturer self-pay terms discussed above apply to either path. If HRA reimbursement is your plan, confirm with your administrator how they treat NovoCare-sourced fills before you commit. Verified April 17, 2026.

What’s the Best Next Step for Your Situation?

The right next step depends on which HRA you have, whether your insurance covers Wegovy, and whether you’ve confirmed HRA reimbursement is a clean fit for a manufacturer self-pay purchase.

If your HRA reimburses prescriptions or qualified medical expenses generally, and your administrator has confirmed manufacturer self-pay reimbursement is OK

Pull together the claim packet (receipt, prescription, LMN) and submit through your administrator’s portal. Use our related guide on HSA eligibility documentation for the exact LMN template and submission walkthrough.

If your HRA only covers covered copays or deductible expenses, and your plan excludes Wegovy

HRA isn’t the right lane for you. Two better fallback paths:

If you might have insurance coverage for Wegovy (cardiovascular indication, a covering employer plan, or a commercial plan that covers obesity medications), Ro is the strongest path. Their insurance concierge handles prior authorization for Wegovy specifically — the documentation, the appeals, the back-and-forth most people give up on.

Pricing: get started for $39 for the first month, then as low as $74/month with annual plan paid upfront, or $149/month month-to-month. Medication billed separately.

Check Wegovy insurance coverage on Ro → (sponsored affiliate link, opens in a new tab)Verify current pricing on ro.co before signing up · Verified April 2026

If you want a provider that publishes HSA, FSA, and HRA acceptance at checkout and routes Wegovy at manufacturer self-pay pricing, Sesame Care is the cleanest fit. Sesame’s FAQ confirms HSA/FSA/HRA funds work on their platform, and their Wegovy page lists NovoCare’s $199/$349 cash-pay prices directly. Note: the NovoCare self-pay terms discussed above apply — confirm HRA reimbursement with your administrator first.

See Wegovy options on Sesame Care → (sponsored affiliate link, opens in a new tab)Care fee $59/month with annual subscription · Verified April 2026

If you don’t have a prescription yet and aren’t sure which Wegovy form is right (pen vs. pill vs. HD) → see our Wegovy HD vs. Wegovy Pill guide before picking a provider.

If your insurance is Medicare → HRA pathways generally don’t apply the same way; Medicare has its own three real paths in 2026.

Why we recommend Ro as the default pick when insurance might be in play, not Sesame: Ro does not accept HSA/FSA or HRA cards directly at checkout the way Sesame does. If HRA card-at-checkout is your priority, Sesame is the better fit. But because Ro skips the card-at-checkout feature, they can invest more in the prior authorization concierge that fights the paperwork battle most employees lose on their own. Different tool for different job.

Related guides on The RX Index

Frequently Asked Questions

Is Wegovy HRA eligible?

Usually yes when the HRA reimburses prescription drugs or qualified medical expenses generally. The IRS treats prescribed Wegovy as a qualified medical expense when used to treat a diagnosed condition such as obesity, overweight with a comorbidity, or established cardiovascular disease. The exception is HRAs that only reimburse cost-sharing for benefits already covered under the main medical plan — if the plan excludes Wegovy, that HRA usually can’t help.

Do I need a Letter of Medical Necessity for Wegovy HRA reimbursement?

Often yes for weight-loss medications. An LMN is a one-page document from your prescriber stating your diagnosis and confirming Wegovy is medically necessary to treat it. HRAs and FSAs frequently request one because the IRS rule for weight-loss expenses is diagnosis-based, not just prescription-based. Most LMNs are valid for 12 months.

Can I use my HRA for Wegovy if my insurance doesn’t cover it?

Sometimes yes. If your HRA reimburses qualified medical expenses generally — not just covered benefits — you can use it for Wegovy even when your insurance excludes it. Some employers have built specialty GLP-1 HRAs precisely to cover medications their main plans exclude. Other employers have covered-benefits-only HRAs that cannot override a plan exclusion.

Can I use my HRA with NovoCare Pharmacy self-pay or the Wegovy Savings Offer?

It depends on how your HRA administrator interprets the manufacturer’s terms. NovoCare Pharmacy’s Terms of Use state patients will not seek reimbursement from any insurer, and the Wegovy Savings Offer has similar language. HRAs are technically group health plans, which creates interpretive ambiguity. HSAs and FSAs are typically not affected the same way. Confirm with your HRA administrator in writing before combining a manufacturer self-pay purchase with HRA reimbursement.

Why did my HRA card decline if Wegovy is supposed to be eligible?

Usually it’s a substantiation problem at checkout, not an eligibility problem. Some HRAs are reimbursement-first by design and the card simply isn’t meant to swipe at the pharmacy. Others can’t auto-substantiate certain transactions even when the expense is eligible. Pay with a personal card and submit the same expense for reimbursement with an itemized receipt and an LMN if needed.

Can my HRA card approve a Wegovy charge at the pharmacy and still be deemed ineligible later?

Yes. A pharmacy system can approve an HRA card for a prescription that qualifies under IRS rules, but the employer’s HRA design may treat it as ineligible after the fact if the underlying plan doesn’t cover the medication. If your HRA is covered-benefits-only and your plan excludes Wegovy, a pharmacy-counter approval does not protect you from a later clawback.

What changes with QSEHRA, ICHRA, or HSA-compatible HRAs?

QSEHRA (small employer with under 50 FTE) typically reimburses qualified medical expenses including Wegovy when you maintain qualifying health coverage. ICHRA (any employer size) varies by plan design — some reimburse only premiums, some reimburse premiums plus medical expenses. HSA-compatible HRAs come in two variants: limited-purpose (dental, vision, preventive only — does not cover Wegovy) and post-deductible (covers Wegovy only after the HDHP deductible is met).

Will I lose HSA eligibility if my employer adds a GLP-1 HRA?

Potentially, if the HRA reimburses GLP-1 expenses before you’ve met your HDHP deductible. Safe designs make the HRA post-deductible or limited-purpose. Ask HR for the plan documents and look for the specific design language — this is avoidable if you catch it early.

Is the Wegovy pill HRA eligible too?

Yes. The Wegovy tablet is indicated for adult weight management and adult cardiovascular risk reduction. Both indications qualify under the IRS diagnosis-based standard for weight-loss treatment expenses. The Wegovy injection also has pediatric obesity and MASH indications that the tablet does not currently carry, but for adult HRA eligibility purposes, both formulations qualify under the same rules.

How long should I keep my Wegovy receipts and LMN?

Keep them for as long as your HRA administrator’s claim-documentation window plus the IRS statute of limitations on your tax return (typically 3 years for most taxpayers, up to 7 years for certain circumstances). Digital copies in cloud storage are more reliable than physical filing.

What’s the cheapest way to get Wegovy in 2026 if I’m using my HRA?

Assuming your HRA allows reimbursement for manufacturer self-pay purchases, the cheapest self-pay paths through NovoCare Pharmacy are the Wegovy pill at $149/month (both 1.5 mg and 4 mg, with 4 mg returning to $199 after August 31, 2026) and the Wegovy pen at $199/month for new patients through December 31, 2026. For ongoing use, the Wegovy 12-month subscription at $249/month (launched March 31, 2026 through Ro, WeightWatchers, and LifeMD, paid upfront as $2,988) is currently the lowest ongoing rate for branded Wegovy. Combined with general HRA reimbursement, your effective net cost can approach zero — assuming your HRA design and administrator interpretation support it.

Still not sure which GLP-1 program is right for you?

Take our free 60-second matching quiz. We’ll route you to the cleanest reimbursement, insurance, or self-pay path based on your HRA setup, insurance status, and state.

Take our free 60-second matching quiz →How we verified this page

This guide was researched and written by The RX Index Editorial Team. We don’t use medically-reviewed-by credits we can’t truthfully attribute, we don’t accept paid placement for editorial coverage, and we update commercial pricing monthly and regulatory content quarterly. Every commercial claim on this page has a “last verified” timestamp or inline source citation.

Key sources: IRS Publication 502 and 969; IRS Revenue Procedure 2025-19; HealthCare.gov HRA definitions; HealthEquity HRA Qualified Medical Expense list; employer plan documents from VEHI, Stillwater Area Public Schools, and Washington University in St. Louis; NovoCare Pharmacy Terms and Conditions and current Wegovy pricing; FDA Wegovy prescribing information (injection revised 2026, tablets 2025); Sentinel Group GLP-1 specialty HRA program; Akerman LLP and Sequoia Consulting Group benefit design analyses (February 2026).

Last verified: April 17, 2026 • Commercial pricing: monthly refresh • Regulatory and IRS content: quarterly refresh

About this guide

The RX Index is a pricing intelligence and comparison resource for GLP-1 telehealth providers. When you click links to Ro, Sesame Care, or other GLP-1 providers from this page, The RX Index may receive a commission at no additional cost to you. Our provider rankings and recommendations are determined by reader fit and current verification — not by commission rates.

This page is editorial guidance, not medical, legal, or tax advice. Talk to your plan administrator, benefits manager, and tax professional about your specific situation.

Your situation changes the answer

Find My GLP-1 Path

The right GLP-1 provider isn't the same for everyone. It depends on your state, your insurance and formulary, whether you want an FDA-approved or compounded medication, your preferred route (injection or oral), and your budget. Because a general answer can't resolve those for you, use The RX Index's Find My GLP-1 Path tool to get a personalized provider match with source-verified pricing before you choose.

- What it asks: your state, insurance situation, medication preference, budget, and support needs

- What you get: a personalized shortlist of GLP-1 providers matched to your situation, with verified pricing and the right questions to ask

- Cost: free · about 2 minutes · no signup