What Is Truemed GLP-1? What It Means for HSA/FSA Shoppers

Published:

By The RX Index Editorial Team • Last verified: April 17, 2026 • Published April 17, 2026

The RX Index is a pricing intelligence and comparison resource for GLP-1 telehealth providers.

Not medical advice. HSA/FSA eligibility is determined by your plan administrator, not by us and not by the merchant.

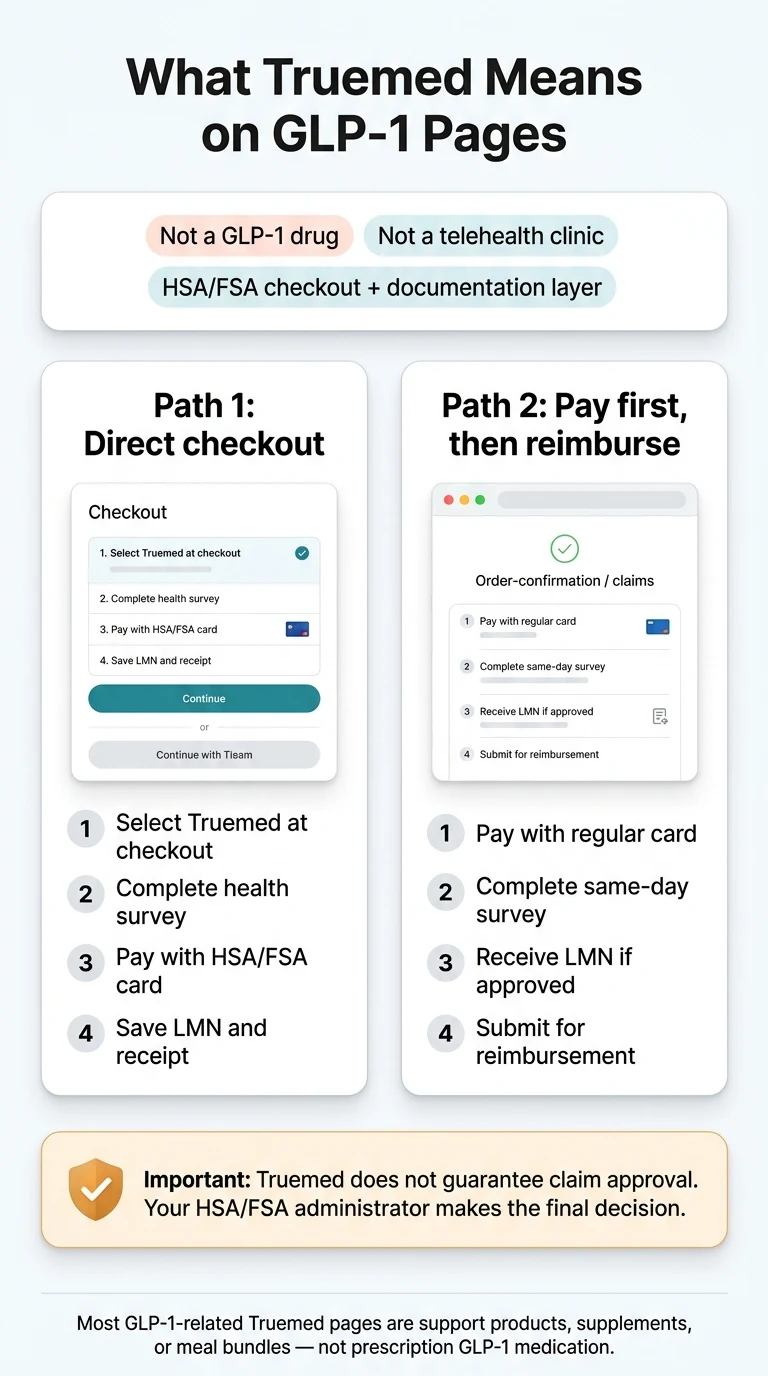

The fast answer: “Truemed GLP-1” is not a medication, not a telehealth clinic, and not a new weight-loss drug. Truemed is an HSA/FSA payment and documentation platform that shows up at checkout on certain GLP-1-related product pages — mostly supplements, companion products, coaching programs, and meal bundles aimed at people on GLP-1 medication.

For actual prescription GLP-1 medications, you usually don’t need Truemed at all. How you pay with HSA/FSA depends on the provider — and we’ve verified each one below.

| You’re buying… | Is Truemed legit here? | HSA/FSA path | Safest move |

|---|---|---|---|

| A GLP-1 supplement or companion product (BioTrust GLP-1 Elevate, Calocurb, SoWell, etc.) | Yes | Varies by merchant and order type | Read the merchant’s Truemed instructions before you enter payment info |

| A GLP-1-adjacent meal box or food bundle (Daily Harvest GLP-1 Companion Collection) | Yes | Typically one-time orders only, not subscriptions | Buy as one-time if possible; save the itemized receipt |

| A prescription GLP-1 medication (Wegovy, Zepbound, compounded semaglutide or tirzepatide) | You don’t need Truemed at all | Varies: some providers take HSA/FSA cards directly, others reimbursement-only | Use the provider-specific routing table below |

⚠️ One honest thing before you keep reading: Truemed does not pre-approve your HSA/FSA claim. Your plan administrator still has the final say, and real users report both smooth approvals and frustrating revisions. If guaranteed approval matters more to you than convenience, call your HSA/FSA administrator first — on any of these paths.

Not sure which GLP-1 path is right for your situation?

Take our free 60-second GLP-1 Path quiz →What we actually verified

- Truemed’s own general explainer, legitimacy explainer, and help center — April 2026

- Six live GLP-1-related Truemed partner or product pages and their current checkout instructions

- IRS Publication 502 and IRS guidance on nutrition, wellness, and general-health expenses

- FDA’s February 2026 update on compounded GLP-1 safety and FDA’s March 2026 warning letters to 30 telehealth companies

- HSA/FSA payment policies on official pages of Embody, MEDVi, SHED (ShedRx), MyStart Health (sponsored affiliate link, opens in a new tab), Yucca Health, Sesame Care, Ro, Hims & Hers, NovoCare Pharmacy, and LillyDirect

Where a provider’s workflow changes based on order type (one-time vs. subscription), we noted both. We did not complete transactions to test every path. Anything we couldn’t confirm on a live page is flagged in-line.

What Is Truemed GLP-1? (And What It Isn’t)

Truemed is a U.S.-based payment integration platform, founded in 2022, that lets qualified HSA and FSA holders use pre-tax dollars on health and wellness products that don’t automatically count as medical expenses. It does this through a Letter of Medical Necessity (LMN) — a short clinical survey reviewed by an independent licensed provider, who issues the LMN if your situation meets IRS medical-necessity standards.

If you remember one thing from this page: Truemed is the checkout and documentation layer, not the thing you’re actually buying.

Your HSA and FSA accounts were built so you could spend pre-tax money on things that treat, mitigate, or prevent a diagnosed medical condition. That’s easy for a prescription pill or a hospital bill — the paperwork is obvious. It gets murky for things like a supplement, a coaching program, or a meal bundle. These are called “dual-use” items: they can be health-related or not, depending on your situation.

Truemed is the layer that turns “maybe eligible” into “documented and eligible” for that middle tier. A partner merchant adds Truemed to its checkout. You pick Truemed as your payment method. You answer a short clinical intake. If an independent licensed clinician agrees your purchase is medically necessary for your specific situation, Truemed issues you an LMN, and the purchase becomes a qualified medical expense for HSA/FSA purposes.

Who’s behind it

Truemed was co-founded by Calley Means and Justin Mares and is backed by investors including Dr. Mark Hyman and early leaders from Thrive Market, Eight Sleep, and Levels. As of 2026, Truemed reports more than 1 million Americans have routed HSA/FSA dollars through its platform. Co-founder Calley Means told TechCrunch at launch that Truemed was the approved Shopify payment integration for HSA/FSA at that time. That matters less for whether you should use it and more for whether it’s a real business: yes, it is.

What Truemed is NOT

- Not a GLP-1 medication

- Not a compounding pharmacy

- Not a prescriber or telehealth clinic

- Not an insurance plan or HSA/FSA administrator

- Not a savings card or coupon

- Not a subscription you sign up for separately

- Not affiliated with Novo Nordisk or Eli Lilly

- Not the same company as “Truemeds” (the India-based online pharmacy)

Truemed vs. Truemeds — Why Your Search Results Are Showing Two Different Companies

There are two unrelated companies with near-identical names. Truemed (truemed.com) is the U.S.-based HSA/FSA payment platform this page is about. Truemeds (truemeds.in) is an India-based online pharmacy that sells generic and branded medications to Indian customers. They have no relationship — not the same people, not the same product, not the same country.

This matters because some negative reviews floating around search results for “truemed” are actually about Truemeds, the Indian pharmacy, and they get lumped together by search engines. If you’re evaluating whether to trust the Truemed badge at a U.S. checkout, make sure the reviews you’re reading are about truemed.com specifically.

| Name | What it is | Country | Related to your GLP-1 checkout? |

|---|---|---|---|

| Truemed (truemed.com) | HSA/FSA payment and documentation platform | United States | Yes — this is the one on your checkout page |

| Truemeds (truemeds.in) | Online pharmacy selling branded/generic meds | India | No — unrelated company |

| TruePill | B2B pharmacy fulfillment infrastructure | United States | No — different service, different customer |

| Trulicity | Brand-name dulaglutide (GLP-1 medication by Eli Lilly) | N/A | No — that's an actual medication |

Is Truemed Legit? The Honest Answer

Yes, Truemed is a legitimately operating U.S. business, not a scam. It integrates with household-name brands (Rogue Fitness, Peloton, Wahoo, Thorne, Apollo Neuro), offers a Shopify payment integration, and follows IRS documentation rules through independent licensed clinicians. That said, “legit” doesn’t mean “guaranteed approval.”

Structural legitimacy: green

- Operates through independent licensed healthcare providers who review each clinical intake

- Issues LMNs designed to meet IRS documentation requirements under Publication 502

- Integrates with Shopify, WooCommerce, and custom merchant platforms

- Maintains a public-facing partner merchant directory

- Provides appeals support when claims are denied (per Truemed help center)

User experience: mixed

- Trustpilot shows a polarized mix of 5-star approvals and 1-star LMN-revision complaints

- Reddit threads show the same pattern

- Truemed can only do its half — your plan administrator does the other half

- Some administrators are lenient. Some are strict. Truemed cannot override the strict ones.

“Approaching my 100th workout thanks to the LMN. Easy process, and genuinely saved me money I would have otherwise just paid in tax.” — Trustpilot reviewer, October 2025

“I’m at my fifth or sixth LMN revision because my FSA administrator keeps wanting different wording. Great idea, but the execution isn’t smooth every time.” — Trustpilot reviewer, February 2026

User-reported process experiences; included here to show both sides, not as typical outcomes or medical claims.

Honest takeaway: Truemed is real. It works for most eligible dual-use purchases tied to a documented health need. But if you expect zero friction and guaranteed reimbursement, you’ll be frustrated — and that’s true of any HSA/FSA claim, not just ones routed through Truemed.

Does Seeing Truemed at Checkout Mean Your HSA/FSA Purchase Is Automatically Approved?

No. The Truemed badge means the merchant has integrated with a platform that can produce an LMN and facilitate HSA/FSA payment — not that your specific purchase will be reimbursed by your plan. This is the single most common misunderstanding.

What Truemed checkout confirms

- The merchant has set up a compliant HSA/FSA payment path

- An independent licensed clinician will review your intake

- If you qualify, you’ll receive an LMN

- Your payment will process

What Truemed checkout does NOT confirm

- That your specific HSA/FSA plan will accept the LMN as written

- That your plan considers this product eligible under its specific rules

- That you won’t be asked for additional documentation later

- That you won’t have to revise the LMN

This isn’t a knock on Truemed — no third-party platform can bind your plan administrator to a decision. If certainty matters more than convenience for you, call your HSA/FSA administrator before you check out and ask them exactly what documentation they need for the category you’re buying.

How Does Truemed Cost Work? Are There Fees?

Truemed’s fee structure depends on the merchant and the workflow. On many partner merchant pages, Truemed states there’s no cost to the shopper. But Truemed’s own support materials acknowledge that a small fee may appear at the end of the qualification survey for some services, and certain merchant flows describe a consultation fee of around $30. Check the Truemed checkout flow as it appears on the merchant page you’re using — don’t assume it’s free in every case.

What to do before you pay:

- Read the final page of the Truemed qualification survey before confirming — any fees will be displayed there

- If you’re on a subscription flow, check the merchant’s HSA/FSA policy page for whether a clinician review fee applies

- If you need a clean paper trail, keep the fee disclosure in your records alongside the LMN and itemized receipt

How Truemed Actually Works at Checkout — The Two Paths You’ll See

Truemed has two distinct flows, and which one you’ll encounter depends on the merchant and the product type. Many GLP-1-related subscription products use path two, not path one.

Path 1: Direct HSA/FSA checkout

What most people picture when they hear “HSA/FSA at checkout.”

- Add items to cart

- At checkout, select “Truemed — Pay with HSA/FSA”

- Answer a short clinical intake (2–5 minutes)

- Independent licensed clinician reviews your answers

- If approved, pay with your HSA/FSA card (or split payment if balance is too low)

- LMN is emailed to you; keep it for records

Used by: Peloton, Rogue Fitness, Wahoo — and some one-time GLP-1 supplement purchases.

Path 2: Pay first, then reimburse

The path that trips people up. The Truemed badge is still there — but it behaves differently.

- Add items to cart

- Check out with a regular credit or debit card (the merchant usually tells you in bold: do not use your HSA/FSA card at checkout)

- Receive your order confirmation

- Click the Truemed link in the confirmation email (the survey must be taken the same day as your purchase)

- Answer the clinical intake

- If approved, receive your LMN within 1–2 business days

- Submit the LMN + itemized receipt to your HSA/FSA administrator for reimbursement

Most GLP-1-related subscription products use this path. Miss the same-day survey window and you lose the LMN.

Mixed carts and split payments

If your cart has some HSA/FSA-eligible items and some ineligible items, Truemed-integrated merchants sometimes support split payment. This isn’t universal. If it’s not supported, the safest move is to check out the eligible items in a separate order so you have a clean itemized receipt to submit.

Want the quickest path to the best-fit HSA/FSA-ready GLP-1 option?

Check your eligibility in 60 seconds →The Truemed GLP-1 Workflow Matrix: What 6 Live Pages Actually Do

We reviewed six live Truemed-integrated GLP-1-related pages in April 2026. The pattern is clear: subscription-based GLP-1 supplement pages overwhelmingly use the pay-first-then-reimburse model, while one-time purchases and meal bundles are more likely to support direct HSA/FSA checkout. Not one of the six is a prescription GLP-1 medication page — every single one is a companion product, dietary supplement, or food bundle.

| Live page / product | What it actually is | Prescription GLP-1? | Checkout behavior | LMN timing stated | Biggest thing to know |

|---|---|---|---|---|---|

| BioTrust GLP-1 Elevate | Fiber/botanical supplement marketed as supporting natural GLP-1 levels | No — dietary supplement | Subscription: pay with regular card first, then survey, then reimburse. One-time: direct Truemed checkout. | 1–2 days (subscription) | Subscription flow is reimbursement-first — don't use your HSA/FSA card at checkout |

| Calocurb GLP-1 Activator | Hops-extract dietary supplement for appetite support | No — dietary supplement | Subscription: reimbursement-first. One-time: direct Truemed checkout. | 1–2 days (subscription) | Same-day survey required; miss the window and you lose the LMN |

| Just Ingredients Crave Support | Craving-support dietary supplement | No — dietary supplement | Subscription: reimbursement-first. One-time: direct Truemed checkout. | 1–2 days (subscription) | Same-day survey required |

| Evolv | Oral capsule marketed as a "natural GLP-1" support product | No — dietary supplement (not a prescription GLP-1) | Subscription: reimbursement-first. One-time: direct Truemed checkout. | 1–2 days (subscription) | Product language can make shoppers think it's a medication — it's a supplement |

| SoWell GLP-1 Support System | Vitamin/mineral support system for people on GLP-1 medications | No — companion supplement kit (not the medication) | Subscription-reimbursement / one-time-checkout split; split payment support noted for mixed carts | 1–2 days (subscription) | Re-verify live checkout before ordering — language differs slightly between SoWell's site and Truemed's partner page |

| Daily Harvest GLP-1 Companion Collection | Meal/smoothie bundle for people on GLP-1 medication | No — food bundle | One-time only: direct Truemed HSA/FSA checkout with split payment support. Subscriptions: not HSA/FSA-eligible through Truemed on this merchant. | Under 24 hours if qualified | Only specific bundles qualify; your regular grocery cart won't |

Verified April 2026. Merchant flows change. Re-check the live checkout page before you enter payment information.

Insight 1: The “Truemed GLP-1” label is almost never on a prescription medication page.

In the six pages we reviewed, not one was a prescription GLP-1. If you landed here hoping Truemed is how you pay for Wegovy or compounded semaglutide, it probably isn’t — use the provider-specific routing table below instead.

Insight 2: Subscription flows almost always mean “don’t use your HSA/FSA card at checkout.”

The single biggest misread. The Truemed badge is there, but the merchant is routing you through pay-first, reimburse-later. If you accidentally use your HSA/FSA card on a subscription flow, you may create a payment compliance mismatch that your administrator flags.

Insight 3: LMN timing is inconsistent across merchants.

Truemed’s own general help content describes LMNs being issued in roughly 2–5 hours. GLP-1-related subscription partner pages state 1–2 business days. Daily Harvest states under 24 hours if qualified. This isn’t a red flag — it reflects different workflows — but plan your purchase accordingly, especially near an FSA year-end.

Why Truemed Shows Up on Supplements and Meal Boxes — Not on Prescription GLP-1 Pages

Truemed exists specifically to make “dual-use” products HSA/FSA-eligible through the LMN pathway. Prescription GLP-1 medications already qualify as medical expenses — your prescription is the documentation. Dietary supplements, companion products, meal bundles, and wellness programs need the extra layer of medical-necessity documentation that Truemed provides.

You don’t need a separate LMN for your Wegovy. You don’t need one for your compounded tirzepatide. You don’t need one for your Zepbound from LillyDirect or your Foundayo from Ro or your Wegovy pill from NovoCare Pharmacy. The prescription does that work.

A bottle of GLP-1-named capsules looks like a medical purchase but isn’t automatically one. A food bundle marketed to people on GLP-1 medication isn’t automatically one either. These are the “dual-use” items the IRS talks about — eligible if medical necessity is documented. That’s the gap Truemed fills. That’s why you see the Truemed badge on BioTrust GLP-1 Elevate but not on the Wegovy order page.

The practical upshot

- A prescription GLP-1 medication: You don’t need Truemed. How you pay depends on the provider — see the provider-specific table below.

- A dietary supplement, companion product, or wellness bundle: Truemed is how that purchase becomes HSA/FSA-eligible. Expect either direct checkout (one-time orders) or reimbursement-first (subscriptions). Read the merchant’s specific instructions before you pay.

- A weight-loss program with a program fee: The fee may or may not be HSA/FSA-eligible through Truemed depending on what it includes. The clinical portion is usually treated separately from coaching and supplements.

How Much You’ll Actually Save with HSA/FSA on a GLP-1

Per Truemed’s own disclosures, qualified customers save about 30% on average on eligible products when supported by an LMN. That reflects the pre-tax nature of HSA/FSA dollars — you’re paying with income that never got taxed at the federal, state, or FICA level. Most Americans land between 25% and 40% total savings. The math is similar whether you use Truemed’s LMN path for a supplement or pay for a prescription GLP-1 medication directly with your HSA/FSA card.

How the savings work, simply:

- You earn $100. Federal tax (22% bracket), FICA (7.65%), state tax (~5%) takes roughly $35.

- You’d have $65 left if you paid with after-tax money.

- If you route the purchase through your HSA or FSA, you spend the full $100 pre-tax — the product effectively costs $65 out of your take-home pay.

- The delta is your savings: roughly $35 on $100.

Worked examples using current verified pricing

| Scenario | Annual cost | Estimated annual savings |

|---|---|---|

| Compounded semaglutide at $299/mo (Embody ongoing rate) | $3,588/year | ~$897/year at 25% marginal rate |

| GLP-1 supplement (BioTrust-style) at ~$75/mo | $900/year | ~$225–$300/year depending on bracket |

| Branded Wegovy at NovoCare self-pay ($349/mo ongoing) | $4,188/year | ~$1,050–$1,500/year depending on bracket |

Estimates are illustrative. Actual savings depend on your bracket, state, filing status, and funding method. Not tax advice. NovoCare pricing verified April 2026; terms and offers change.

The savings aren’t “free money.” They’re tax that would have been paid on the income used to buy the product. But they are real, they’re significant, and they stack up fast on a recurring expense like a monthly GLP-1.

Compounded vs. FDA-Approved GLP-1s — What You Need to Know Before You Route

Prescription GLP-1 medications split into two categories. FDA-approved branded GLP-1s — Wegovy, Ozempic, Zepbound, Mounjaro, Rybelsus, and the newly approved Foundayo — have been through the FDA’s full review. Compounded semaglutide and compounded tirzepatide are prepared by licensed 503A or 503B compounding pharmacies and are not FDA-approved.

FDA warning (March 2026)

The FDA has flagged safety concerns about compounded GLP-1 products, including variability in purity, potency, and ingredients, and in March 2026 issued warning letters to 30 telehealth companies for making false or misleading claims about compounded GLP-1s. Both categories can be HSA/FSA-eligible with a valid prescription, but they are not interchangeable and should not be treated as equivalent.

- Compounded GLP-1s are legal when prescribed by a licensed provider and filled by a licensed compounding pharmacy that meets federal and state standards. The FDA’s concerns are about quality variability and deceptive marketing, not a blanket prohibition.

- Compounded products are not FDA-reviewed finished drug products. Any marketing that implies otherwise has been a specific target of FDA enforcement.

- HSA/FSA eligibility is the same in principle for both categories — a valid prescription from a licensed provider, for a diagnosed medical condition, generally substantiates the expense. Some plan administrators apply extra scrutiny to compounded medications.

- Your clinical decision should be made with your provider, not based on price alone.

See: Is compounded tirzepatide HSA/FSA eligible? and Is compounded semaglutide HSA eligible? for deeper dives.

If You Were Actually Trying to Use HSA/FSA for Prescription GLP-1 Medication — The Provider Payment Table

If you thought “Truemed GLP-1” was a medication provider and what you actually want is a prescription GLP-1 paid with HSA/FSA, you don’t need Truemed at all. But how you pay differs by provider. Here’s the verified payment-method breakdown as of April 2026.

Embody

Top PickMedication types: Compounded semaglutide and tirzepatide injections, plus a needle-free GLP-1 gum

HSA/FSA at checkout: Advertised HSA/FSA eligible — confirm with your plan administrator

Cash-pay, no membership fee. Availability varies — check availability in your state during intake.

See Embody Pricing → (sponsored affiliate link, opens in a new tab)Compounded semaglutide from $99 first month, $299/mo ongoing · Needle-free GLP-1 gum from $149 first month, $349/mo · Verified June 11, 2026

Embody’s shipped compounded GLP-1 options are not FDA-approved finished drugs. A licensed provider determines whether treatment is medically appropriate. Prices, pharmacy availability, shipping timelines, and state eligibility can change and should be confirmed during intake. Last verified June 11, 2026.

SHED (ShedRx)

Medication types: Compounded semaglutide and tirzepatide in injection, sublingual drops, and dissolvable lozenges; branded Wegovy and Zepbound

HSA/FSA at checkout: Yes — HSA/FSA accepted (listed on HSA Store and on ShedRx’s own program pages)

Strongest fit for oral/pill/sublingual options.

See SHED pricing → (sponsored affiliate link, opens in a new tab)Semaglutide injections from $199/mo · Verified April 2026

MEDVi

Medication types: Compounded semaglutide and tirzepatide (injection and tablets); branded Ozempic and Wegovy pill for qualifying patients

HSA/FSA at checkout: Yes — HSA/FSA accepted per MEDVi’s published policy; reimbursement option also available

MEDVi received an FDA warning letter in February 2026 about prior marketing language that implied MEDVi was the compounder (it isn’t — MEDVi works with licensed compounding pharmacies). The warning letter was about marketing, not medication safety, and MEDVi remains LegitScript-certified. If that context concerns you, Embody or SHED are cleaner alternatives for the same medication categories.

Compounded semaglutide from $179 first month, $299/mo ongoing · Verified April 2026

MyStart Health

Medication types: Compounded semaglutide and tirzepatide (injection and oral)

HSA/FSA at checkout: Partial — some HSA/FSA cards work directly at checkout; others require reimbursement. Price-lock model, same price at every dose, 24/7 clinician access.

See MyStart Health pricing → (sponsored affiliate link, opens in a new tab)3-month compounded semaglutide plan from $149/mo · Verified April 2026

Yucca Health

Medication types: Compounded semaglutide and tirzepatide

HSA/FSA at checkout: HSA/FSA supported via reimbursement; BNPL options via Klarna/Affirm/Afterpay. Async-first, no live visits required, value-oriented.

See Yucca Health pricing → (sponsored affiliate link, opens in a new tab)Entry pricing varies · Verified April 2026

Sesame Care

Medication types: Branded Wegovy, Zepbound, Foundayo; also compounded options through certain providers

HSA/FSA at checkout: HSA/FSA supported. Strong fit if you want FDA-approved branded medication and transparent per-visit pricing.

See Sesame Care pricing → (sponsored affiliate link, opens in a new tab)Foundayo entry from ~$149/mo per Sesame’s current page · Verified April 2026

Ro

Medication types: FDA-approved Zepbound and Foundayo; weight-loss membership model

HSA/FSA at checkout: No — Ro does not accept HSA/FSA cards at checkout. Ro instructs customers to pay with a regular card and submit for reimbursement with a detailed receipt.

Best fit if you want insurance coordination and prior authorization help. Membership fee is separate from medication cost.

See Ro pricing → (sponsored affiliate link, opens in a new tab)$39 first month; Zepbound $299 first month, $399–$449 at later doses · Verified April 2026

Hims & Hers

Medication types: Branded Wegovy via Novo Nordisk partnership; also oral weight-loss combinations

HSA/FSA at checkout: No — Hims recommends paying with a regular card and submitting for reimbursement. Availability and pricing for branded Wegovy shift with Novo Nordisk’s direct-to-consumer pricing updates.

See Hims pricing → (sponsored affiliate link, opens in a new tab)Confirm current self-pay pricing on checkout · Verified April 2026

Pharmacy-direct options

- NovoCare Pharmacy (Novo Nordisk’s direct-to-consumer option for Wegovy and Ozempic): Accepts HSA/FSA payments. As of April 2026, first-time Wegovy 0.25 mg and 0.5 mg fills are $199/month for the first two months, then $349/month for Wegovy 0.25–2.4 mg and $399/month for Wegovy HD 7.2 mg. Wegovy pill: $149/month for 1.5 mg and 4 mg doses (4 mg offer only through August 31, 2026, then $199 for 4 mg). Terms and offers change — verify on NovoCare’s current page before relying on these numbers.

- LillyDirect (Eli Lilly’s direct-to-consumer option for Zepbound vials and Foundayo): Confirm current HSA/FSA payment options on LillyDirect’s checkout at the time of purchase.

See also: GLP-1 providers that take HSA · GLP-1 providers that take FSA · Oral GLP-1 providers that take HSA or FSA

Not sure which one fits your situation, budget, and state?

Take our 60-second GLP-1 Path quiz →You’ll get a personalized recommendation based on your goals, budget, insurance status, state, and whether you want FDA-approved or a compounded option.

What to Save Before You Pay: The Claim Protection Checklist

Five documents protect your HSA/FSA claim. Most Truemed-related claim denials aren’t because the product wasn’t eligible. They’re because the paperwork didn’t match the plan administrator’s requirements.

- ☐Letter of Medical Necessity (LMN) from Truemed — sent to your email after clinical intake review. Most LMNs are valid for 12 months from issue date, covering future eligible purchases from the same merchant.

- ☐Itemized receipt — must show the merchant name, a description of what you bought (not just “Order #12345”), the amount paid, and the date of purchase. Order confirmations often aren’t itemized enough.

- ☐Proof of payment — usually the last four digits of the card used to pay, either on the receipt or in a bank/card statement.

- ☐Your prescription or provider note — if the purchase is a prescription GLP-1, keep a copy of the prescription. If the purchase is a supplement tied to a condition, keep a note from your healthcare provider referencing the condition.

- ☐Record of the health condition — a simple note about why you’re buying this. Not because you need to submit it immediately, but because if your plan audits a claim later, you’ll want the context.

Don’t submit the same expense twice. If your purchase was routed through Truemed’s direct HSA/FSA checkout, don’t also submit it to your administrator for reimbursement — that’s a duplicate claim and it will get flagged.

The 5 Most Common Truemed Claim Denial Reasons

The five most common denial reasons are: (1) the product wasn’t eligible under your specific plan, (2) documentation was incomplete or non-itemized, (3) the LMN wording didn’t match what your administrator wanted, (4) mixed-cart confusion, and (5) duplicate reimbursement. None of these are Truemed’s fault — they’re plan administration realities.

1. Product ineligibility under your specific plan

You bought a GLP-1 supplement through a Truemed-integrated checkout, got your LMN, submitted for reimbursement, and your administrator denied it because their internal rules exclude that product category regardless of medical necessity documentation.

How to avoid it: Call your HSA/FSA administrator before a large purchase and ask whether the product category is eligible on your plan. Dual-use supplements are the most commonly denied category.

2. Incomplete or non-itemized documentation

You submit an order confirmation instead of an itemized receipt. The administrator rejects the claim because the paperwork doesn't show exactly what you bought.

How to avoid it: If the merchant didn't send a true itemized receipt, request one from customer service before you submit the claim.

3. LMN wording mismatch with your administrator

Your plan administrator requires specific language on the LMN — a specific diagnosis code, a specific product name, or a specific duration of treatment. Your Truemed LMN is close but not exact.

How to avoid it: Ask your administrator what format they prefer before you apply. If your LMN gets rejected, contact Truemed support — they've seen most variations and will reissue the LMN with the right wording where possible.

4. Mixed-cart confusion

You bought three things in one order — one is clearly HSA/FSA-eligible, two aren't. You submit the full order amount. The administrator sees the ineligible items and denies the whole thing.

How to avoid it: Check out eligible items in a separate order when you can. If you can't, use the itemized receipt to submit only the eligible line items.

5. Duplicate reimbursement

You paid with your HSA/FSA card at a Truemed direct checkout, then also submitted the receipt to your administrator for reimbursement because you didn't realize the direct checkout had already applied the funds.

How to avoid it: Pick one path. Either pay with your HSA/FSA card at checkout (direct) OR pay with a regular card and submit for reimbursement (indirect). Not both.

Clean documentation, the right checkout path for your order type, and matching your administrator’s format dramatically reduce the friction on legitimate dual-use purchases.

Should You Use Truemed If You See It on a GLP-1 Page?

Use Truemed when three conditions line up: the product is a clear dual-use item tied to a documented health need, your order type matches the merchant’s flow, and your plan administrator hasn’t historically been strict with dual-use claims. Skip it when the purchase is cosmetic weight loss without a diagnosed condition, when your FSA is about to expire, or when the product you’re actually looking for is a prescription GLP-1 medication.

✅ Good fit for using Truemed

- You’re buying a GLP-1 supplement, companion product, or wellness program clearly tied to a documented health condition (obesity, prediabetes, metabolic syndrome, PCOS with weight-management goals, etc.)

- You’re buying a one-time order and the merchant supports direct HSA/FSA checkout

- You have time to wait 1–2 weeks for reimbursement if you’re on the pay-first path

- Your HSA/FSA administrator has historically accepted LMN-substantiated dual-use claims

⚠️ Proceed carefully

- You’re buying a subscription product — make sure you’re using the pay-first path, not your HSA/FSA card at checkout

- Your FSA expires soon and you can’t wait for a potentially contested reimbursement cycle

- You’ve never had a dual-use claim approved by your administrator before (call them first)

- The product has vague wellness positioning and no clear tie to a diagnosed condition

❌ Don’t use Truemed here

- You’re actually looking for a prescription GLP-1 medication — use the provider-specific payment method table above instead

- You want a product purely for cosmetic weight loss with no diagnosed medical condition

- You’re trying to use an expired FSA balance on a retroactive purchase (no backdating allowed)

- The merchant doesn’t actually have Truemed integrated and is only claiming HSA/FSA eligibility without the LMN workflow — that’s a red flag

Frequently Asked Questions

Is Truemed a GLP-1 medication company?

No. Truemed is an HSA/FSA payment and documentation platform. It does not make, prescribe, or sell GLP-1 medications. It provides the Letter of Medical Necessity workflow that makes certain dual-use health products eligible for pre-tax spending.

Does Truemed guarantee my HSA/FSA claim will be approved?

No. Truemed produces a compliant LMN based on an independent licensed clinician’s review, but your HSA/FSA plan administrator makes the final reimbursement decision. Truemed itself states it cannot guarantee reimbursement or override plan administrator decisions.

Can I use Truemed for prescription Wegovy, Ozempic, or Zepbound?

You don’t need to. Prescription GLP-1 medications are already HSA/FSA-eligible as qualified medical expenses — your prescription is the documentation. How you pay with HSA/FSA depends on the provider: some accept HSA/FSA cards directly at checkout, others require you to pay with a regular card and submit for reimbursement.

Can I use Truemed for compounded semaglutide or tirzepatide?

Usually not necessary. Most telehealth providers selling compounded GLP-1s (Embody, MEDVi, SHED, MyStart Health) accept HSA/FSA cards or support reimbursement directly. Your prescription from a licensed provider substantiates the purchase. Verify with your plan administrator if your plan applies extra scrutiny to compounded medications.

How long does it take Truemed to issue an LMN?

Truemed’s general help content describes LMNs being issued in roughly 2–5 hours. GLP-1-related subscription partner pages reviewed state 1–2 business days. Daily Harvest states under 24 hours if qualified. Plan accordingly.

Does Truemed charge me a fee?

It depends on the merchant and workflow. Truemed’s partner merchant pages often state there’s no cost to the shopper, but Truemed’s support materials acknowledge that a small fee may appear at the end of the qualification survey for some services, and some merchant flows include a consultation fee. Check the final step of the Truemed survey before confirming payment.

Can I use Truemed if I’m self-employed?

HSA access for self-employed people works through individual HSA accounts paired with qualifying high-deductible health plans. FSA access generally requires an employer-sponsored plan. Check with your HSA provider or tax advisor for your specific situation.

What if my plan administrator rejects my Truemed LMN?

Contact Truemed support. They will often reissue the LMN with wording that better matches your administrator’s requirements. Truemed states it cannot guarantee reimbursement or override administrator decisions, but it does provide appeals support and documentation revisions.

Is Truemed the same as Truemeds (the online pharmacy)?

No. Truemed (truemed.com) is a U.S.-based HSA/FSA payment platform. Truemeds (truemeds.in) is an unrelated India-based online pharmacy. Despite near-identical names, they have no relationship.

Can I use Truemed on a past purchase?

No. The Truemed clinical survey must be completed on the same day as the purchase, and LMNs don’t retroactively qualify purchases made before the LMN was issued.

What’s the difference between Truemed’s direct checkout and pay-first reimbursement?

Direct checkout processes the HSA/FSA payment in the same session as your purchase. Pay-first reimbursement means you check out with a regular card, complete the Truemed survey from your confirmation email, receive the LMN, and submit it to your HSA/FSA administrator for reimbursement later. Many GLP-1 subscription products use the pay-first model.

Do I need to use Truemed if my GLP-1 telehealth provider already accepts HSA/FSA cards?

No. If your provider’s checkout has HSA/FSA as a payment option directly, use that. Truemed is the alternative pathway for products and services that aren’t automatically eligible without additional documentation.

Related guides on The RX Index

Still not sure which GLP-1 program is right for you?

Take our free 60-second matching quiz. In under a minute, you’ll get a personalized recommendation based on your goals, budget, insurance status, state, and whether you want FDA-approved branded medication or a compounded option.

Start the GLP-1 Path Quiz →About this guide

Written by The RX Index editorial team. The RX Index is a pricing intelligence and comparison resource for GLP-1 telehealth providers. This guide draws on Truemed’s public documentation (general explainer, legitimacy FAQ, help center), IRS Publication 502, FDA’s February and March 2026 compounding updates, and direct verification of provider HSA/FSA payment policies as of April 17, 2026.

Informational content only. Not medical advice. HSA/FSA eligibility is determined by your plan administrator, not by us and not by the merchant. Pricing and program details verified as of April 17, 2026 and subject to change.

Your situation changes the answer

Find My GLP-1 Path

The right GLP-1 provider isn't the same for everyone. It depends on your state, your insurance and formulary, whether you want an FDA-approved or compounded medication, your preferred route (injection or oral), and your budget. Because a general answer can't resolve those for you, use The RX Index's Find My GLP-1 Path tool to get a personalized provider match with source-verified pricing before you choose.

- What it asks: your state, insurance situation, medication preference, budget, and support needs

- What you get: a personalized shortlist of GLP-1 providers matched to your situation, with verified pricing and the right questions to ask

- Cost: free · about 2 minutes · no signup