How to Use Truemed for Weight Loss: Exact Steps, What Qualifies, and Where Claims Fail

Published:

By The RX Index Editorial Team • Last verified: April 17, 2026 • Published April 17, 2026

The RX Index is a pricing intelligence and comparison resource for GLP-1 telehealth providers.

Not medical, legal, or tax advice. Talk to your clinician, HSA/FSA administrator, and tax professional about your specific situation.

You saw the Truemed logo at checkout. Now you’re trying to figure out whether you can actually use it to spend your HSA or FSA on weight loss — and whether you’re about to get your claim denied.

Here’s how it works: Truemed is effective, but only when three things line up. A partner merchant has Truemed at checkout. You complete the clinical survey on or before the day you buy. And your purchase ties to a specific disease diagnosed by a physician. One-time purchases often allow direct HSA/FSA payment; subscriptions almost always require pay-first, reimburse-later.

Quick decision table

| If this sounds like you | Best next step | Biggest risk |

|---|---|---|

| One-time purchase, partner merchant, Truemed visible at checkout | Use Truemed at checkout — complete the survey before payment finalizes | The clinician may not approve your survey |

| Subscription or recurring plan at a Truemed partner | Pay with a regular card, complete the same-day survey, submit the LMN + receipt for reimbursement | HSA/FSA cards commonly decline at recurring billing |

| You already bought without Truemed | Ask the merchant about refund + repurchase | Truemed does not backdate Letters of Medical Necessity |

| You want weight loss with no diagnosed condition | Verify medical necessity with a clinician before purchasing | “General wellness” framing is the #1 IRS exclusion |

| You actually want a GLP-1 medication program | Use your HSA/FSA directly with the prescriber, not through Truemed | Wrong tool for the job |

What we actually verified for this page:

- IRS Publication 502 (2025) and IRS Topic 502 weight-loss guidance

- Truemed’s customer help center: LMN access via dashboard, subscription reimbursement, same-day/no-backdating rules, HRA and LPFSA restrictions, card declines, denial reasons, administrator submission guides

- Truemed merchant resources documenting the qualification link and fee structure

- Six live Truemed weight-loss partner pages: Re:Vitalize Weight Loss, Jillian Michaels Fitness App, BioTrust GLP-1 Elevate, SoWell, Calocurb, H Lyfe Method

- FDA warning letter database, February 20, 2026 enforcement wave against compounded GLP-1 marketing (including letter #721455 to MEDVi and the letter to Lean Rx, Inc. / SkinnyRx)

- Current HSA/FSA policy pages on Embody, Sesame Care, Yucca Health, Ro, Hers, and Hims

- Trustpilot customer reviews of Truemed (process/documentation commentary only)

Verified April 17, 2026. Next scheduled refresh: May 17, 2026.

What Truemed Actually Is (and Isn’t) for Weight Loss

Truemed is an HSA/FSA documentation platform — not insurance, not a pharmacy, and not a blanket approval for weight-loss spending. It partners with merchants to embed a short clinical intake at checkout, has an independent licensed clinician review your answers, and (if you qualify) issues a Letter of Medical Necessity (LMN) — the document your HSA/FSA administrator uses to confirm a “dual-use” purchase counts as a qualified medical expense.

For weight loss specifically, Truemed’s platform is most useful for the middle tier of purchases: weight-loss programs, supplements, fitness apps, and nutritional coaching tied to a documented health condition. It’s not the right tool for prescription GLP-1 medications (your prescriber’s LMN does that work), and it’s not useful for general wellness spending with no diagnosed condition (the IRS won’t allow it regardless).

Founded in 2022–2023 by Calley Means and Justin Mares, with backing from Mark Hyman and founders from Thrive Market, Eight Sleep, and Levels, Truemed publicly launched in September 2023 and reports roughly one million Americans have used the platform. Access your Letter of Medical Necessity in the Truemed dashboard — the platform has moved away from email delivery of the LMN itself; renewal reminders may still arrive by email.

Two things to be clear on: Truemed itself doesn’t decide whether you qualify — independent licensed clinicians do, based on your survey answers. And fees vary by merchant — some pages say “no cost to you,” others describe a $30 qualification fee or co-pay. We cover the full discrepancy in the fee language audit below.

What Truemed is NOT:

- A payment processor for prescription GLP-1 medications

- An insurance plan or HSA/FSA administrator

- A guarantee that your plan administrator will reimburse you

- Useful for general wellness spending with no diagnosed condition

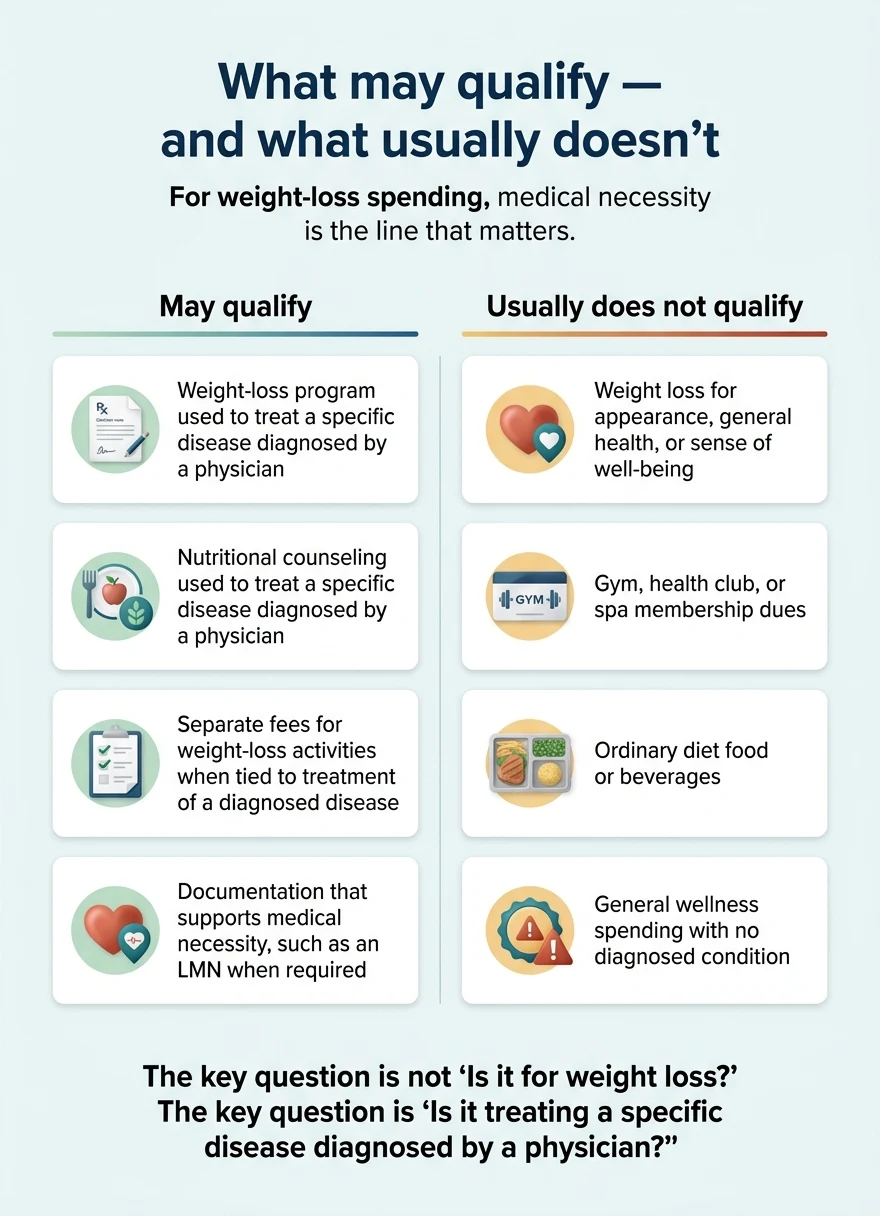

Does Your Weight-Loss Spending Actually Qualify? IRS Publication 502 in Plain English

The IRS allows weight-loss expenses as qualified medical expenses only when they treat a specific disease diagnosed by a physician — Publication 502 names obesity, hypertension, and heart disease as examples. Spending on weight loss for appearance, general health, or sense of well-being does not qualify. Gym dues and ordinary diet food do not qualify either. That single rule is the gate everything else passes through.

| May qualify (IRS Publication 502) | Usually does not qualify |

|---|---|

| Weight-loss program to treat a specific disease diagnosed by a physician | Weight loss for appearance, general health, or sense of well-being |

| Nutritional counseling to treat a specific diagnosed disease | Gym, health club, or spa membership dues (general) |

| Separate fees for weight-loss activities when tied to treatment of a diagnosed disease | Ordinary diet food or beverages |

| Documentation supporting medical necessity (e.g., an LMN) when required | General wellness spending with no diagnosed condition |

Honest tradeoff — this matters

Truemed will not turn cosmetic weight loss into a tax deduction. If you don’t have a documentable condition and a clinician willing to put it in writing, this isn’t your path. The IRS issued a 2024 alert warning taxpayers that some companies have been misrepresenting general wellness expenses as medical care. But if you do have a real condition — including something you’ve been putting off addressing formally — the proper step is to see a clinician, get the condition documented, and then apply for an LMN. That’s Truemed working as intended.

Special food exception: food only qualifies if it does not satisfy normal nutritional needs, it treats or alleviates an illness, and a physician substantiates the need — and only the amount that exceeds the cost of a normal diet. This bar is high.

If you have a diagnosis and you’re shopping at a partner merchant, you are inside the lines. If you don’t, the right next step isn’t Truemed — it’s a clinician visit to establish what’s actually going on.

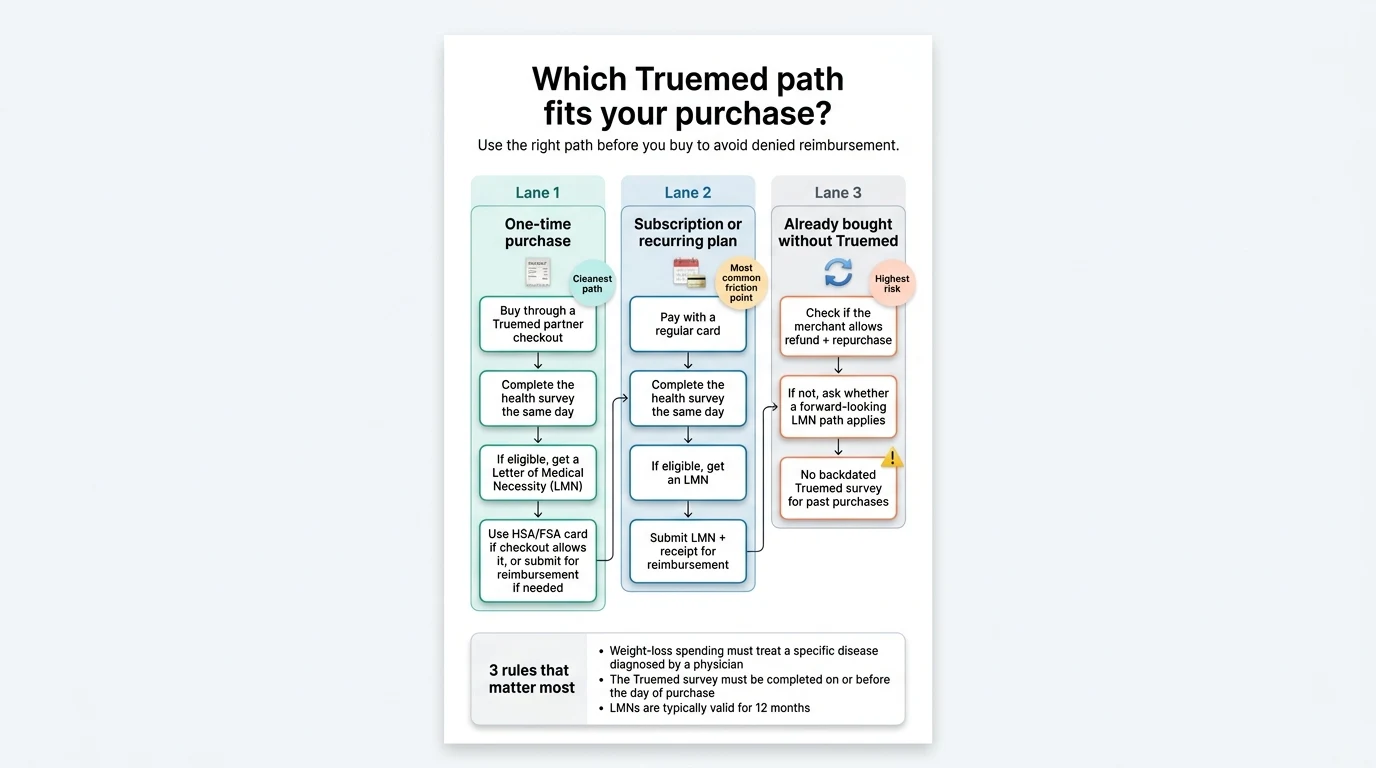

The Two Truemed Flows: One-Time Purchase vs. Subscription

Truemed runs two different workflows depending on how you’re buying. One-time purchases at partner merchants often allow direct HSA/FSA card payment at checkout. Subscriptions and recurring plans almost always require you to pay with a regular card first, complete a same-day survey, receive an LMN, and then submit for reimbursement. This split confuses more buyers than any other detail — partly because merchants tend to feature the friendlier of the two flows in their marketing.

Flow 1: One-time purchase (the clean path)

- Add eligible items to your cart at a Truemed partner merchant

- Select “Truemed — Pay with HSA/FSA” at checkout

- Complete the short clinical intake survey

- Independent licensed clinician reviews your answers

- If approved: pay with your HSA or FSA card. If not approved: the hold releases and you pay with a regular card

- Access your LMN in your Truemed dashboard (typically within 1–2 days)

Some merchants report approvals inside business hours. LMN is valid for 12 months for future purchases at the same merchant.

Flow 2: Subscription or recurring plan (pay first, reimburse later)

HSA/FSA cards commonly decline on recurring billing — this is an industry-wide rails issue, not a Truemed failure.

- Pay with a regular credit or debit card at checkout (do not use your HSA/FSA card)

- Complete the Truemed survey on the same day as the purchase

- Access your LMN in your Truemed dashboard if approved

- Save the LMN and each month’s itemized receipt

- Submit both to your HSA/FSA administrator for reimbursement

- Wait 2–4 weeks for funds to land in your account

Inside the 12-month LMN validity, the same LMN covers each subsequent month’s receipt — but you still submit each month’s receipt individually.

Mistake to avoid: double-dipping.

Don’t pay with your HSA/FSA card at checkout AND submit for reimbursement separately. That’s a duplicate claim your administrator will deny.

Merchant-specific quirks (verified April 17, 2026):

- Calocurb: The Shop Pay pop-up can interfere with the Truemed checkout option. Exit Shop Pay if prompted.

- SoWell: Automatically splits eligible and ineligible items in mixed carts.

- BioTrust: Handles one-time orders and subscriptions through different Truemed flows for the same product.

The Same-Day Survey Rule (and Why It Kills More Claims Than Anything Else)

Truemed’s clinical intake survey must be completed on or before the day of purchase.

The platform does not backdate Letters of Medical Necessity for purchases made earlier, and this single rule is the most common reason buyers end up with uncovered receipts.

The reason isn’t bureaucratic — it’s compliance. An LMN is a clinician’s documented judgment that a specific product is medically necessary for you on the date you bought it. If the clinician hasn’t seen your information until two weeks after you swiped, they can’t attest to medical necessity at that earlier moment. Truemed’s help center is explicit: the survey must happen on or before the purchase date.

What this means tactically:

- Don’t “add to cart, come back tomorrow to do the Truemed thing.” Complete the survey in the same session — or wait to buy until you’re ready to do both at once.

- Bookmark the merchant’s Truemed page before you start shopping so you don’t lose the flow.

- If you accidentally checked out without Truemed, ask that specific merchant whether they can refund and let you repurchase through the Truemed flow. Some allow it, some don’t.

The flip side: once your LMN is issued, it covers future purchases at that same merchant for the next 12 months. That’s how subscribers stay covered month after month with one approval.

What If You Already Bought Without Truemed?

If you completed a purchase without going through Truemed first, your options narrow quickly. There is no clean retroactive path through Truemed.

Option 1: Refund and repurchase at the merchant

If the merchant’s return window is open, ask for a refund, then repurchase through the Truemed flow. Truemed’s own help content points you back to the merchant for this conversation. Most likely to work for one-time physical products still in their return window; rarely helps for subscriptions already billed.

Option 2: Standalone Truemed LMN (limited categories only)

Truemed generally cannot issue standalone LMNs for purchases at non-partner merchants. The narrow exceptions publicly named include gym memberships, saunas, exercise equipment, and activity trackers. Email [email protected] to ask. Standalone LMNs only cover purchases made on or after the LMN’s issue date — they do not retroactively cover what you bought last week.

Option 3: Your own clinician writes the LMN

If you have a primary care doctor or a telehealth provider who already knows your situation, they can write you an LMN directly. You then submit the LMN plus your itemized receipt to your HSA/FSA administrator. Works particularly well for prescription GLP-1 medications.

The pattern: plan the LMN before you buy, or accept that anything purchased without one is out-of-pocket.

The RX Index Truemed Weight-Loss Friction Map

We pulled the public Truemed pages for six representative weight-loss merchants and mapped them across the variables that determine whether your experience is easy or painful. This is the single comparison view nobody else publishes, and it’s the table to consult before you sign up for anything.

| Merchant / program | Direct HSA/FSA at checkout | Subscription flow | Same-day survey rule | LMN timing stated | Reimbursement timing | Biggest friction point |

|---|---|---|---|---|---|---|

| Re:Vitalize Weight Loss | No — buy first, then survey | Reimbursement only | Yes | 1–2 days | 2–4 weeks | No HSA/FSA card at checkout; reimbursement only |

| Jillian Michaels Fitness App | No direct-card flow shown | Reimbursement for memberships | Yes | 1–2 days (24–48 hours) | 2–4 weeks | Subscription reimbursement, not instant pay |

| BioTrust GLP-1 Elevate | Yes for one-time orders | Reimbursement for subscriptions | Yes for subscriptions | 1–2 days | 2–4 weeks | One-time and subscription flows differ |

| SoWell (GLP-1 companion supplements) | Yes for one-time orders | Reimbursement for subscriptions | Yes for subscriptions | 1–2 days | 2–4 weeks | Mixed carts split into eligible/ineligible automatically |

| Calocurb (appetite supplement) | Yes for one-time orders | Reimbursement for subscriptions | Yes for subscriptions | 2–5 hours typical | 2–4 weeks | Shop Pay pop-up interferes with Truemed checkout |

| H Lyfe Method | Manual reimbursement only | Manual reimbursement | Yes | 1–2 days | 2–4 weeks | Highest manual effort: quiz, LMN, itemized receipt, admin submission each separate |

Source: live merchant Truemed pages and Truemed’s customer help center, verified April 17, 2026.

Pattern 1: One-time vs. subscription is the real fault line.

The same merchant can be effortless for a one-off bottle of supplements and a documentation slog for a subscription of the same product. Plan around the purchase type, not the brand.

Pattern 2: Reimbursement timing is uniform at 2–4 weeks.

Every partner we checked quotes the same window. If you’re racing an FSA deadline, submit at least three weeks before the cutoff.

Pattern 3: LMN delivery has shifted to the dashboard.

Older merchant pages still describe LMNs being sent by email. Current Truemed help confirms the LMN is now accessed through your Truemed dashboard, not delivered to your inbox. If the merchant page says “check your email” and nothing arrives, log in to your dashboard.

The Fee Language Audit (Why We Won’t Tell You It Costs $X)

Truemed’s consumer-facing fee disclosure is genuinely inconsistent across its own ecosystem. Three different answers appear on three categories of source. We’re not going to pretend there’s one universal number — here’s the discrepancy in full.

| Source | What it says about the fee |

|---|---|

| Truemed merchant resources / partner setup docs | Eligible customers may pay a one-time $30 fee when going through certain merchant qualification flows |

| Many partner merchant FAQs (REP Fitness, Sole, Thorne, and more) | “There is no cost to you” when shopping with a Truemed partner merchant |

| Truemed blog and consumer-facing language | The cost is included in the purchase price at integrated merchants |

| Some clinic-style merchants (e.g., H Lyfe Method) | Reference a “$30 co-pay” if the LMN is approved through their flow |

Verified April 17, 2026.

The honest reading: at most major retail partner merchants (supplements, fitness equipment, apps, programs), there is no separate fee charged to you — the cost is absorbed by the merchant or built into the catalog price. The $30 figure mostly applies to certain merchant qualification flows and to standalone LMNs outside integrated checkout, and to certain clinical-program merchants where the LMN is structured as a co-pay. Before you assume “this is free,” look at the specific merchant’s Truemed page and confirm.

How Long Truemed Takes — and What to Plan Around

LMN approval typically appears in your dashboard within 1–2 days, with some partner merchants reporting 2–5 hours during business hours. HSA/FSA reimbursement, once you submit the LMN and receipt to your administrator, typically takes 2–4 weeks for the funds to land in your account.

Where things slow down:

- Survey responses that need clarification. Vague or incomplete intake answers trigger a review request from the clinician, adding 1–3 days.

- Administrator backlogs. Larger plan administrators (Optum, HealthEquity, WEX, Navia, HSA Bank, Fidelity) have varying queue times. Processing tends to slow in November and December.

- Mixed cart submissions. Submitting a receipt with both eligible and ineligible items without separating them can get the entire claim denied.

- Year-end FSA crush. December adds delay at every step.

Plan: if you need the reimbursement by a specific date, back up at least four weeks and start then.

Why Truemed Claims Get Denied (and How to Avoid Each)

Most denials are documentation problems, not eligibility problems. Truemed’s own published guidance identifies five recurring failure modes, and all five are avoidable with a checklist.

1. “General wellness” or “preventative health” framing

The #1 denial reason Truemed support cites. Words like “general wellness,” “preventative health,” “improvement of overall health,” or “guaranteed weight loss” read as non-medical to administrators.

Fix: Tie everything to a specific diagnosed condition. “Used to manage diagnosed obesity” is citable. “For better health” is not.

2. Vague or incomplete LMN

A receipt that says “Gym Access” reads as a recreational expense. An LMN missing the patient’s identifying information, a clinician signature, or a clear clinical rationale gets bounced.

Fix: If going the standalone-LMN route, double-check the document includes: patient name, date of birth, diagnosed condition, the specific treatment, the clinician’s credentials, signature, and date.

3. Diagnosis–product mismatch

If your LMN is for hypertension and your receipt is for a fitness tracker, an administrator may ask how the tracker treats hypertension. The link needs to be explicit and clinically credible.

Fix: A heart-rate monitor for hypertension management — yes, with documentation. A novelty step counter for general fitness — much weaker case.

4. Mixed cart with ineligible items

An $80 receipt with some eligible and some ineligible items, submitted whole, can get the entire claim denied or trigger a repayment demand.

Fix: Truemed-integrated checkouts split these automatically; manual submissions are your responsibility. Check out eligible items separately when possible.

5. Timing misalignment

The LMN must be dated on or before the purchase. A purchase from May 1 with an LMN dated May 14 is a denial.

Fix: Same-day survey, every time.

Edge cases worth knowing

- NP vs. MD signatures. Some plan administrators will accept LMNs signed by nurse practitioners or physician assistants; others require an MD or DO specifically. If denied for signature reasons, ask Truemed support whether re-issuance with an MD signature is available.

- Run-out periods. Most FSA plans give you a 60–90 day run-out period after the plan year ends to submit prior-year claims. Verify your specific window with HR or your administrator.

- What to send Truemed after a denial. Compile: a screenshot of the denial notice, the denial code (if provided), your administrator’s name, your LMN, and the itemized receipt. Email the bundle to [email protected]. Truemed cannot guarantee reimbursement or override a plan administrator’s decision, but their appeal support is real.

Why Did My HSA or FSA Card Decline at Checkout?

HSA/FSA cards are programmed to authorize only at merchants coded as medical. If your card declines at a non-medical merchant code — which many supplement, fitness, and wellness sites are — that’s expected behavior, not a Truemed problem.

Cart contains ineligible items

If your cart has nothing eligible, you can’t use the HSA/FSA card. You’ll see a message that the cart is ineligible.

Fix: Use a regular card instead.

Merchant category code mismatch

Even with Truemed integrated, some merchants aren’t coded as medical. Some cards will still process; some won’t.

Fix: Pay with a regular card and submit the LMN and receipt for reimbursement instead.

Split payment not supported

Some merchants support splitting the HSA/FSA-eligible portion onto your HSA/FSA card and the ineligible portion onto a regular card. If your merchant doesn’t, pay the full amount with one card.

Fix: Reimburse the eligible portion from your HSA/FSA afterward.

Reimbursement after the fact is the safer default anyway. Every major partner supports it, and it avoids the merchant-category-code trap entirely.

Does Truemed Work with HRA, Limited Purpose FSA, or Medicare?

| Account type | Works with Truemed? | Details |

|---|---|---|

| HRA (Health Reimbursement Arrangement) | Sometimes | If your HRA has no category restrictions and covers general medical expenses, Truemed can often support the reimbursement process. If your HRA is limited (dental/vision only, or deductible-only), Truemed’s flow won’t apply. Check with HR or your plan administrator. |

| Limited Purpose FSA (LPFSA / LEX HCFSA) | No | LPFSA funds are restricted to dental and vision expenses only. This is a plan-design rule, not a Truemed rule. Use a regular Health Care FSA if you have one. |

| Dependent Care FSA (DCFSA) | No | DCFSA funds can only be used for dependent-care expenses like daycare or preschool — not for health care products or services. |

| Medicare | Existing HSA funds: Yes. New contributions: No | You can’t contribute new funds to an HSA once enrolled in Medicare. But existing HSA funds can still be spent on qualified medical expenses through Truemed. |

Is Truemed Legitimate — and What’s the Honest Catch?

Truemed is a real, operational platform with more than one million users, partnerships across 50+ product categories, and a documented compliance pathway. The platform is legitimate; the risk lives in misuse.

What makes it legitimate

- Founded by named, traceable entrepreneurs with named investors

- Independent licensed clinicians review every survey

- LMNs structured to comply with IRS Section 213(d)

- Major plan administrators have published Truemed-specific submission paths

- Real dashboard, support team, and appeals process

- Explicitly states it cannot override administrator decisions

What raises legitimate questions

- Documentation requirements are unforgiving (same-day rule, no backdating)

- Public communication around fees is inconsistent across sources

- Subscription flows are clunkier than the marketing implies

- The IRS issued a 2024 alert about companies misrepresenting general wellness as medical care

- A 2025 AP report noted Truemed had drawn IRS scrutiny over aggressive wellness-as-medical-expense positioning

The synthesis: Truemed is a legitimate compliance layer doing exactly what it says it does. The risk isn’t that the platform is fraudulent; it’s that buyers use it for general wellness rather than treatment of a diagnosed condition. Real diagnosis + real partner merchant + documented treatment of a specific disease = on solid ground. Fitness tracker because you “want to be healthier” = territory the IRS could reasonably push back on.

"Quick and easy to use my HSA funds."

"Got the LMN I was looking for and got it quickly."

"I'm at my 5th or 6th revision for a LMN."

Source: Truemed customer reviews on Trustpilot, captured April 17, 2026. These comments describe the payment and documentation process only. Individual experiences vary.

The Q4 FSA Deadline Playbook

FSA funds typically expire December 31 (some plans offer a grace period or limited carryover; verify yours). If you have a balance and weight-loss goals, here’s a sequenced playbook to deploy those funds without triggering denials.

By October 31 — Plan

- Pull your current FSA balance from your administrator’s portal

- List your eligible weight-loss spending: subscriptions, supplements, programs, fitness equipment, activity trackers, coaching

- If you’re on a GLP-1, ask your prescribing clinician whether they’ll write an LMN if your administrator requests one — now, not in December

By November 15 — Buy

- Place all Truemed-integrated purchases first so the LMN is issued during checkout

- Start subscription orders so the first month’s billing falls inside your plan year

- For non-partner items that qualify (gyms, saunas, exercise equipment, activity trackers), request any standalone documentation you’ll need

By December 1 — Document

- Save every itemized receipt

- Verify every LMN is dated on or before its corresponding purchase

- Compile receipts and LMNs into one folder per merchant

By December 20 — Submit

- Upload all claims to your HSA/FSA administrator’s portal

- Submit at least three weeks before any cash-flow deadline

- Track each claim weekly

January–March — Use the run-out period

- Most FSA plans allow 60–90 days after year-end to submit prior-year claims

- Confirm your specific run-out window with your administrator

- Use this buffer for stragglers; don’t rely on it for December purchases

The pattern: subscriptions and Truemed flows take longer than you think. Start in November, not December.

The 60-Second Eligibility Checklist (Run It Before Every Purchase)

Six yes/no questions — if any answer is no, fix that before you hit Submit.

- 1.I have a diagnosed condition (obesity, hypertension, type 2 diabetes, sleep apnea, cardiovascular disease, or another condition documented by a clinician) — not just a desire to lose weight

- 2.I have an HSA or a regular Health Care FSA with available funds (not an LPFSA or DCFSA)

- 3.The merchant is a Truemed partner (look for the Truemed logo at checkout)

- 4.I'm completing the survey today, in the same session as the purchase (no 'I'll do it tomorrow')

- 5.I know whether this is a one-time or subscription purchase and which flow that triggers

- 6.I'll save the LMN and the itemized receipt in one place I can find again

If you get denied: have this ready for a Truemed support email

LMN (from your Truemed dashboard) • Itemized receipt • Denial notice screenshot • Denial code • Administrator name • Appeal deadline

Send to: [email protected]

Can You Use Truemed for the GLP-1 Medication Itself?

Not directly with the major GLP-1 telehealth prescribers. For a prescription GLP-1 — branded Wegovy, Zepbound, Foundayo, or compounded semaglutide or tirzepatide — you use your HSA/FSA card where the provider accepts it, or you pay with a regular card and submit the itemized receipt to your HSA/FSA administrator (plus an LMN from your prescribing clinician if your administrator requests one).

A prescription GLP-1 already carries inherent medical necessity — your prescribing clinician has, by definition, decided the medication is appropriate for you. Adding Truemed into that chain doesn’t strengthen the claim and can slow it down. What administrators typically want for a GLP-1 prescription claim:

- Itemized pharmacy or telehealth receipt showing date, patient name, medication, NDC or Rx ID, quantity, and cost

- The prescription record (most providers provide a downloadable copy)

- An LMN from your prescriber if your administrator requests one

For FDA-approved branded medications, the prescription is usually sufficient. For compounded semaglutide or tirzepatide, some administrators are stricter — a proactive LMN from your prescriber heads off a denial.

HSA/FSA-friendly GLP-1 programs we’re recommending right now

Embody

Top PickOur top recommendation for an HSA/FSA-friendly GLP-1 program. Embody is a cash-pay telehealth provider offering compounded semaglutide and tirzepatide injections plus a needle-free GLP-1 gum, and advertises that purchases are HSA/FSA eligible (confirm with your administrator). Pricing starts low the first month and steps up for ongoing refills depending on medication and format. Availability varies — check availability in your state during intake.

Check Embody Eligibility → (sponsored affiliate link, opens in a new tab)Compounded semaglutide from $99 first month, $299/mo ongoing · Needle-free GLP-1 gum from $149 first month, $349/mo · Verified June 11, 2026

Embody’s shipped compounded GLP-1 options are not FDA-approved finished drugs. A licensed provider determines whether treatment is medically appropriate. Prices, pharmacy availability, shipping timelines, and state eligibility can change and should be confirmed during intake. Last verified June 11, 2026.

Sesame Care

The cleanest FDA-approved-only lane — a good fit if you specifically want Foundayo, Wegovy, or Zepbound and want to stay clear of the compounded category entirely. Pricing varies by visit and pharmacy; HSA/FSA receipts are straightforward.

See Sesame Care pricing → (sponsored affiliate link, opens in a new tab)Foundayo from ~$149/mo · Verified April 2026

Yucca Health

A value-first, async telehealth path — no live video visit, BNPL options at checkout, and many patients successfully use HSA or FSA funds. Note: Yucca does not provide itemized receipts or Letters of Medical Necessity, so if your administrator requests either, you’ll need to get them from a separate clinician. Best for buyers confident their plan won’t require extra documentation.

See Yucca Health pricing → (sponsored affiliate link, opens in a new tab)Ro

Right choice if you specifically want insurance concierge support for branded GLP-1s. Ro’s Body membership starts at $39 for the first month, with ongoing pricing of $149/month — as low as $74/month with an annual plan paid upfront. Ro carries Zepbound (tirzepatide) and Foundayo (orforglipron). Note: Ro states HSA/FSA cards are not processed directly at checkout, but itemized receipts are available for reimbursement.

See Ro pricing → (sponsored affiliate link, opens in a new tab)$39 first month · Verified April 2026 · Verify current pricing on ro.co before signing up

Hers / Hims

Mainstream telehealth options that state FSA/HSA eligibility varies by plan, and that using an HSA/FSA card may require additional steps from your provider. Receipts are available for reimbursement.

A note on compounded GLP-1 providers in 2026

MEDVi received an FDA warning letter on February 20, 2026 (#721455) citing website statements identified as false or misleading regarding compounded semaglutide and tirzepatide — specifically, language the FDA said implied FDA approval of compounded products and presented MEDVi as the compounder when it was not. MEDVi was one of more than thirty telehealth companies warned in a category-wide enforcement wave. A warning letter is not a finding of guilt; MEDVi maintains its LegitScript certification.

SkinnyRx (Lean Rx, Inc.) received a warning letter in the same enforcement wave citing similar misbranding concerns.

These providers are not off-limits. We’re saying: if you’re choosing between compounded providers in 2026, platforms with cleaner regulatory standing are the better starting point — that’s Embody and Sesame first.

Not sure which GLP-1 program fits your state, budget, and goals?

We ask about state, BMI range, insurance status, brand vs. compounded preference, budget, and oral vs. injectable preference — and route you to the program that fits, with HSA/FSA notes baked in.

Get your personalized GLP-1 action plan →Related guides on The RX Index

Frequently Asked Questions

Do I need a diagnosis to use Truemed for weight loss?

Yes, in nearly every case. IRS Publication 502 treats weight-loss expenses as medical expenses only when they are used to treat a specific disease diagnosed by a physician — examples named directly include obesity, hypertension, and heart disease. General wellness, appearance, or improving overall health do not qualify.

Can I use Truemed on a subscription?

Yes, but usually through a reimbursement flow rather than direct HSA/FSA card payment. Subscription billing systems generally do not process HSA/FSA cards reliably, so the standard pathway is to pay with a regular card, complete the same-day Truemed survey, receive your LMN, then submit the LMN and each month’s receipt to your HSA/FSA administrator for reimbursement.

Can I use Truemed after I already made the purchase?

Generally no. Truemed’s clinical intake survey must be completed on or before the day of purchase, and the platform does not backdate Letters of Medical Necessity. For one-time purchases, the practical workaround is to ask the merchant about a refund and repurchase through the Truemed flow.

How long is a Truemed Letter of Medical Necessity valid?

12 months from the date it is issued. During that window, repeat purchases at the same merchant do not require a new survey, though you still submit each new receipt to your administrator for reimbursement.

Does Truemed guarantee my HSA/FSA reimbursement?

No. Truemed publicly states it cannot guarantee reimbursement or override plan-administrator decisions. Truemed’s value is documentation and appeal support, not a reimbursement guarantee.

Where do I get my Letter of Medical Necessity — email or dashboard?

In the Truemed dashboard. The platform has moved away from emailing the LMN itself; renewal reminders may still come to your inbox.

Does Truemed work with HRA or Limited Purpose FSA?

HRA: sometimes, if your HRA has no category restrictions. Limited Purpose FSA (LPFSA / LEX HCFSA): no — those funds are restricted to dental and vision expenses only. Dependent Care FSA: no.

Why did my HSA or FSA card decline at checkout?

Most commonly, the merchant is not coded as a medical merchant, or your cart contains ineligible items. Use a regular card and submit for reimbursement instead — which works even when the card declines.

Can I use Truemed for prescription GLP-1 medications like Wegovy, Zepbound, or compounded semaglutide?

Not directly — Truemed is not integrated at checkout with the major telehealth GLP-1 prescribers. Use your HSA/FSA card at checkout where the provider accepts it, or pay with a regular card and submit the itemized receipt (plus an LMN from your prescribing clinician if your administrator requests one) to your HSA/FSA administrator.

Can Truemed work for a non-partner gym membership or fitness equipment?

Possibly — gym memberships, saunas, exercise equipment, and activity trackers are categories Truemed has publicly named as eligible for a standalone-LMN pathway when tied to treatment of a specific diagnosed condition. Contact [email protected] to start the process. Fees apply, and the LMN only covers purchases made on or after its issue date.

Can I use Truemed if I’m on Medicare?

You can still spend existing HSA funds on qualified medical expenses, but you can’t contribute new funds to an HSA once enrolled in Medicare. Truemed’s platform is designed around HSA and FSA accounts.

Is Truemed available outside the U.S.?

No. Truemed is currently only available to U.S. customers with U.S.-based HSA or FSA accounts.

What documents should I keep in case my claim is appealed or audited?

Keep, for at least three years: the LMN itself, the itemized purchase receipt (showing date, merchant, product details, quantity, and cost), documentation of your diagnosed condition (a clinician note works), and any denial notice plus appeal correspondence. Both Truemed and the IRS recommend retaining digital and hard copies.

Still not sure which GLP-1 program is right for you?

If you’ve made it this far, you probably already know whether Truemed fits your situation. If you’re still deciding on the GLP-1 side — which provider, which medication, what to do about your state, your budget, your insurance — that’s a different decision, and we built a tool for it. No login required.

Take our free 60-second matching quiz →How we verified this page

Primary sources, verified April 17, 2026. We reviewed: IRS Publication 502 (2025 tax year edition) and IRS Topic 502; Truemed’s customer support center (LMN access, subscription reimbursement, same-day/no-backdating rules, HRA and LPFSA restrictions, card declines, denial reasons, administrator submission guides); Truemed merchant resources documenting the qualification link and fee structure; six representative Truemed partner pages (Re:Vitalize Weight Loss, Jillian Michaels Fitness App, BioTrust GLP-1 Elevate, SoWell, Calocurb, H Lyfe Method); FDA warning letter database for the February 20, 2026 enforcement wave including letter #721455 (MEDVi) and the letter to Lean Rx, Inc. / SkinnyRx; current HSA/FSA policy pages on Embody, Sesame Care, Yucca Health, Ro, Hers, and Hims; and Trustpilot customer reviews of Truemed (used only for process/documentation commentary).

What we did not assume: We did not publish a single universal Truemed fee — the sources conflict and we documented the conflict. We did not state that Truemed guarantees reimbursement. We did not state that administrator acceptance is universal. We did not claim Truemed integrates with any GLP-1 prescriber it doesn’t actually integrate with.

Refresh schedule: Merchant flow details and fee language: monthly. IRS guidance and account-type rules: quarterly. Provider HSA/FSA policies: quarterly, with an extra sweep in October for FSA enrollment season. FDA enforcement and regulatory context on compounded GLP-1 providers: monthly while category is active. If the page updates, the “Last verified” date at the top changes with it.

Last verified: April 17, 2026 • Next scheduled refresh: May 17, 2026

About this guide

The RX Index is a pricing intelligence and comparison resource for GLP-1 telehealth providers. We earn affiliate commissions on some of the provider links in our content, which we disclose at the link. Our recommendations are based on verification of current pricing, policies, regulatory standing, and fit — not on payout alone. We do not accept payment to manipulate rankings or to bury material information about partners.

This page is editorial guidance, not medical, legal, or tax advice. Talk to your clinician about whether a GLP-1 program is appropriate for you. Talk to your HSA/FSA administrator about your specific plan’s reimbursement rules. Talk to a tax professional about anything that affects your filing.

Your situation changes the answer

Find My GLP-1 Path

The right GLP-1 provider isn't the same for everyone. It depends on your state, your insurance and formulary, whether you want an FDA-approved or compounded medication, your preferred route (injection or oral), and your budget. Because a general answer can't resolve those for you, use The RX Index's Find My GLP-1 Path tool to get a personalized provider match with source-verified pricing before you choose.

- What it asks: your state, insurance situation, medication preference, budget, and support needs

- What you get: a personalized shortlist of GLP-1 providers matched to your situation, with verified pricing and the right questions to ask

- Cost: free · about 2 minutes · no signup