FDA-Approved GLP-1 Out-of-Pocket Maximum Comparison (2026): Does Your Drug Actually Count?

Published: · Last reviewed:

By The RX Index Editorial Team

Here’s the FDA-approved GLP-1 out-of-pocket maximum comparison most pages won’t give you straight, with the part they bury put first: there is no single cap. For many people taking these drugs for weight loss, the spending never ends up protected by an insurance out-of-pocket maximum at all — because coverage for weight loss is far from guaranteed, and the cash-pay programs most people use don’t count toward the cap. It only counts in one case: your plan covers the drug and you’re paying copays or coinsurance on a covered claim.

FDA-approved GLP-1 out-of-pocket maximum comparison by route

Whether FDA-approved GLP-1 spending counts toward your out-of-pocket maximum depends on how you pay. For a covered claim under a plan that includes the drug, it counts and your cap applies. For self-pay, manufacturer cash programs, and the Medicare GLP-1 Bridge, it does not. In 2026, a Marketplace plan’s out-of-pocket maximum can’t exceed $10,600 for an individual or $21,200 for a family (HealthCare.gov), but that cap only protects covered, in-network care.

Find your row. Then keep reading for the details that change the number.

| Your situation | Your real “maximum” | First move |

|---|---|---|

| Plan covers the GLP-1 | Your plan’s out-of-pocket max (2026 ceiling: $10,600 individual / $21,200 family) | Confirm coverage, prior authorization, and remaining deductible |

| Plan excludes it for weight loss | No insurance cap — you’re comparing monthly cash prices | Compare FDA-approved self-pay prices |

| Medicare Part D covers it (e.g., for diabetes) | 2026 Part D cap of $2,100 | Confirm covered use and your plan’s rules |

| Medicare GLP-1 Bridge applies | $50/month — but it doesn’t count toward your Part D cap | Compare the Bridge against normal Part D |

| Not sure | Unknown until you check | Run a free coverage check (below) |

The single most useful next step

If you don’t know whether your plan covers an FDA-approved GLP-1, that’s the first thing to nail down — everything else depends on it. Ro’s GLP-1 Insurance Coverage Checker is free (you don’t have to be a member). You enter your insurance details, Ro checks with your plan, and you get a personalized coverage-and-cost report — plus a $50 credit for new Ro accounts.

What we actually verified for this page

This comparison is built on primary and high-authority sources checked in June 2026, not recycled blog claims. We separated three kinds of facts: verified prices, federal insurance rules, and our own editorial judgments — and we label which is which. We did not sign up for these plans ourselves; this is a verification of published prices, policies, and regulations.

- The 2026 out-of-pocket maximum — $10,600 individual / $21,200 family — from HealthCare.gov.

- That self-pay and cash programs don’t count toward your deductible or out-of-pocket maximum — from manufacturer and telehealth self-pay disclosures.

- That manufacturer copay cards can be blocked from counting, through “copay accumulator” and “maximizer” programs — from KFF and patient-advocacy organizations.

- Current self-pay prices for Wegovy, Zepbound, and Foundayo — straight from the manufacturers (NovoCare, LillyDirect).

- The Medicare GLP-1 Bridge rules and dates — from CMS and KFF.

- Foundayo’s FDA approval (April 1, 2026) and safety labeling — from the FDA and Eli Lilly.

Do FDA-approved GLP-1s count toward your out-of-pocket maximum?

Usually no. Your out-of-pocket maximum only caps what you pay for covered, in-network care, so it applies to a GLP-1 only if your plan covers that drug and you’re paying copays or coinsurance on a covered claim. Coverage for weight loss is inconsistent, and cash-pay programs sit outside insurance — so for many weight-loss users, these prescriptions never reach the cap.

If you came here hoping that your plan’s out-of-pocket maximum — that comforting number like $10,600 — will quietly cap what GLP-1s cost you this year and then make them free, you may be let down. For a lot of people using these drugs to lose weight, it doesn’t work that way.

Your out-of-pocket maximum is a real, powerful protection. On most job-based and Marketplace plans in 2026, once your in-network spending on covered care hits $10,600 for one person or $21,200 for a family, the plan pays 100% of covered care for the rest of the year (HealthCare.gov). The whole thing hinges on one word: covered. The cap only counts money you pay on something your plan agrees to pay for.

Point that at GLP-1s, and three clean outcomes fall out:

- Your plan doesn’t cover the drug for weight loss. You pay full price, and none of it counts toward your cap — there’s no covered claim to attach it to.

- You pay cash through a manufacturer program (LillyDirect, NovoCare), TrumpRx, or a telehealth program. You’re outside insurance, so none of it counts either.

- Your plan does cover the drug and you pay a copay or coinsurance on the covered claim. Now it counts — and your out-of-pocket maximum genuinely caps your year. This is the scenario you’re hoping for, and it’s worth two minutes to find out if you’re in it.

What counts toward your deductible and out-of-pocket maximum (and what doesn’t)

Covered, in-network prescription costs can count toward your deductible and out-of-pocket maximum; premiums, out-of-network care, and non-covered services do not. If a GLP-1 is excluded from your plan, or you pay through a cash program outside insurance, those dollars generally don’t count toward either number.

Plain-English definitions (a lot of sticker shock comes from mixing these up):

Premium

What you pay monthly just to have the plan. Never counts toward your out-of-pocket maximum.

Deductible

What you pay before your plan starts chipping in. On a covered drug, you can pay full price until you hit this.

Copay

A flat fee per fill (e.g., $40). Simple and predictable.

Coinsurance

A percentage of the cost (e.g., 25%). On a $1,000 drug, that's $250 a month until you hit your cap.

Out-of-pocket maximum

The ceiling. Once your covered cost-sharing reaches it, covered care is free the rest of the year.

Formulary

Your plan's list of covered drugs. If your GLP-1 isn't on it, the cap usually won't help.

Prior authorization (PA)

Your plan's permission slip — your doctor proves you meet the rules before the plan covers the drug.

Does it count? FDA-approved GLP-1 payments and your insurance caps (2026):

| How you’re paying | Typical monthly cost | Counts toward your out-of-pocket max? | Counts toward your deductible? |

|---|---|---|---|

| Plan covers it; you pay copay/coinsurance | Varies by plan | ✅ Yes | ✅ Yes |

| Plan covers it; $25 manufacturer copay card; plan has no accumulator | ~$25 | ✅ Yes (card value counts) | ✅ Yes |

| Plan covers it; $25 copay card; plan runs an accumulator/maximizer | $25 until card empties, then full cost-share | ⚠️ No (card value doesn’t count) | ⚠️ No |

| Manufacturer self-pay (LillyDirect / NovoCare) | $149–$699 | ❌ No | ❌ No |

| TrumpRx cash-pay | ~$149–$499 | ❌ No | ❌ No |

| Telehealth cash-pay at matched prices (e.g., Ro) | $149+ medication + membership | ❌ No | ❌ No |

| Medicare GLP-1 Bridge ($50 copay) | $50 | ❌ No (also not toward the $2,100 Part D cap) | ❌ No |

Here’s why people say, “I’m covered, but I’m still paying $349 a month.” Covered doesn’t mean cheap. Early in the year, before you meet your deductible, you can pay the full negotiated price on a covered drug. If your plan uses coinsurance instead of a flat copay, you keep paying a slice of a four-figure price until you hit the cap. The cap is real — it’s just often a long climb, and only if the drug is covered at all.

That’s the gap this page closes. Everyone else compares monthly stickers. We compare your worst-case yearly exposure, route by route — including whether each dollar even counts toward your ceiling.

What each FDA-approved GLP-1 actually costs in 2026

Without insurance, brand-name GLP-1s still list around $1,000–$1,650 a month, but most self-pay shoppers no longer pay full list. Through manufacturer cash programs, oral Wegovy and Foundayo start near $149/month and Zepbound vials run $299–$449/month. None of those self-pay prices counts toward your out-of-pocket maximum, but they’re usually far below what you’d pay against an unmet deductible.

FDA-approved GLP-1 price matrix (verified against manufacturer pages, June 2026):

| Medication | Form | FDA-approved for weight loss? | List price (no insurance) | Manufacturer self-pay | Counts toward OOP max if self-pay? |

|---|---|---|---|---|---|

| Wegovy® (semaglutide) | Oral pill | ✅ Yes (Dec 2025) | $1,349/mo | $149/mo (lower doses); 4 mg offer is $149 until Aug 31, 2026, then $199; $299/mo (higher doses) | ❌ No |

| Wegovy® (semaglutide) | Injection pen | ✅ Yes | $1,349/mo | $349/mo (0.25–2.4 mg); $399/mo for Wegovy HD 7.2 mg; $199 intro on two lowest doses through December 31, 2026 | ❌ No |

| Zepbound® (tirzepatide) | Single-dose vial | ✅ Yes | ~$1,086/mo (pen) | $299 (2.5 mg), $399 (5 mg), $449 (7.5–15 mg) on Self Pay Journey Program if refill within 45 days — else $499 (7.5 mg) or $699 (10/12.5/15 mg) | ❌ No |

| Zepbound® (tirzepatide) | KwikPen® | ✅ Yes | — | Same structure: $299–$449 on program; $499–$699 if 45-day window is missed | ❌ No |

| Foundayo™ (orforglipron) | Oral pill | ✅ Yes (Apr 1, 2026) | — | $149–$349/mo depending on dose | ❌ No |

| Ozempic® (semaglutide) | Injection | ❌ No — diabetes drug | ~$998/mo | $349/mo (0.25–1 mg); $499/mo (2 mg); $199 intro on two lowest doses through December 31, 2026 | ❌ No (self-pay) |

| Mounjaro® (tirzepatide) | Injection | ❌ No — diabetes drug | ~$1,000–$1,100/mo | Not compared here as a weight-loss self-pay route | ❌ No (self-pay) |

Pills reset the floor. Oral Wegovy and Foundayo both start near $149/month at lower doses. Important caveat: pills and injections aren’t interchangeable — they have different dosing, and which one fits you is a medical decision for your clinician, not a cost decision.

Zepbound vials beat the pen on price. The 45-day refill window is the trap: miss it on higher doses and the price jumps to $499 or $699/month. Screenshot the terms before you commit.

Ozempic and Mounjaro are diabetes drugs. Using them for weight loss is off-label, and there’s no obesity-specific savings program. We keep them separate — blurring an FDA-approved weight-loss drug with an off-label one would be misleading.

A list-price cut is coming. Novo Nordisk will cut the U.S. list price of semaglutide medicines (Wegovy, Ozempic, Rybelsus) to $675/month effective January 1, 2027. That mainly helps people on high-deductible or coinsurance plans.

The honest trade-off — and your move

If you’ve realized you’ll likely be paying cash, the real question is: cheapest sticker, or cheapest with help? Ro is not the cheapest sticker price — if you want the rock-bottom cash number and will handle everything yourself, going straight to LillyDirect or NovoCare costs less. But because Ro adds a small membership, you get a free coverage checker and an insurance concierge that runs your prior-authorization paperwork — and Ro lists FDA-approved GLP-1s at the same cash prices as LillyDirect, NovoCare, and TrumpRx, with new patients starting an oral GLP-1 at $149/month. *(Ro Body membership: $39 the first month, then as low as $74/month on an annual plan paid upfront.)*

See current FDA-approved GLP-1 self-pay pricing on Ro → (sponsored affiliate link, opens in a new tab)Your real yearly cost if you pay cash

Cash-pay has a monthly price, not an insurance cap, so the number that matters is your annualized cost: starting dose, maintenance dose, refill-timing penalties, and any separate membership fee. For FDA-approved options in 2026, a realistic full-year cash range runs from roughly $1,788 (a low-dose oral GLP-1) to about $5,400 (higher-dose injectable routes) — more if you miss a refill window.

A monthly price is easy to underestimate. Here’s the 12-month math — the honest version, where starter doses become maintenance doses (intro offers excluded):

| Medication / form | Standard self-pay (intro offers excluded) | Rough 12-month cost | The catch |

|---|---|---|---|

| Wegovy pill | $149–$299/mo by dose | ~$1,788–$3,588/yr | 4 mg dose moves from $149 to $199 after Aug 31, 2026 |

| Foundayo | $149–$349/mo by dose | ~$1,788–$4,188/yr | Price rises with dose |

| Zepbound vial/KwikPen | $299 start; $399–$449 maintenance on program | ~$4,788–$5,388/yr at maintenance | Miss 45-day refill and higher doses jump to $699/mo (~$8,388/yr) |

| Wegovy injection | $349/mo (most doses); $399/mo HD 7.2 mg | ~$4,188–$4,788/yr | $199 intro is only for first two months, through December 31, 2026 |

| Ozempic (off-label) | $349/mo (0.25–1 mg); $499/mo (2 mg) | ~$4,188–$5,988/yr | Diabetes drug; off-label for weight loss |

Three reasons the first-year number fools people:

- Starter doses aren’t maintenance doses. Most people climb to a higher dose, where the price often climbs too.

- Intro offers expire. That low first-month number can be a limited promotion, not your steady rate.

- Refill windows bite. Miss Lilly’s 45-day rule on higher Zepbound doses and the price jumps to $699/month.

Before you pay a cent, screenshot it: the exact price, the dose it applies to, the offer’s expiration date, the refill window, and the cancellation policy.

The copay accumulator trap: why your $25 card may not count

A “copay accumulator” (or “maximizer”) lets you use a manufacturer’s copay card but stops the card’s value from counting toward your deductible or out-of-pocket maximum. When the card runs out mid-year, you can suddenly owe the full cost-share with no progress banked. In 2024, KFF found copay accumulators in 17% of large employer plans, 34% of firms with 5,000+ workers, and two-thirds of individual Marketplace plans in states that allow them.

This is the most expensive surprise in GLP-1 billing — and the reason the answer is “it depends” even for people with coverage.

How it’s supposed to work

Lilly’s Zepbound Savings Card and Novo’s Wegovy Savings Card can drop eligible patients to ~$25/fill. Traditionally, the manufacturer’s contribution counted toward your deductible and cap, helping you climb faster.

How it actually plays out on many plans

Under a copay accumulator, you can still swipe the card — but the manufacturer’s dollars don’t count toward your deductible or max. You pay $25 for months until the card’s annual value runs dry — then suddenly owe full cost-share with nothing banked.

The legal picture is unsettled. A federal court struck down the rule that broadly let insurers exclude manufacturer assistance, and the reinstated approach generally says assistance should count when there’s no medically appropriate generic — which describes Wegovy, Zepbound, and Foundayo. But there’s still no final clarifying federal rule, copay maximizers and self-funded employer plans operate in the gray area, and enforcement varies. Many plans still run these programs, and you can’t assume yours doesn’t. Ask your benefits team, in writing.

What to actually do:

- Read your pharmacy benefit for the words copay accumulator, maximizer, out-of-pocket protection program, variable copay, or patient assurance program. You should get a written notice if your plan uses one.

- Ask directly: “Does manufacturer copay assistance count toward my deductible and out-of-pocket maximum for this drug?”

- Model the back half of the year, not just the $25 months. The card running out is the moment that hurts.

Your move

The only way to know whether your plan runs an accumulator on your GLP-1 is to check the specific benefit. Ro’s free Insurance Coverage Checker contacts your plan and returns your real copay and cost estimate — so you see what you’ll actually pay before the card runs out, not after.

Check my plan’s GLP-1 coverage and copay free → (sponsored affiliate link, opens in a new tab)Medicare, Medicaid, and the GLP-1 Bridge: a different rulebook

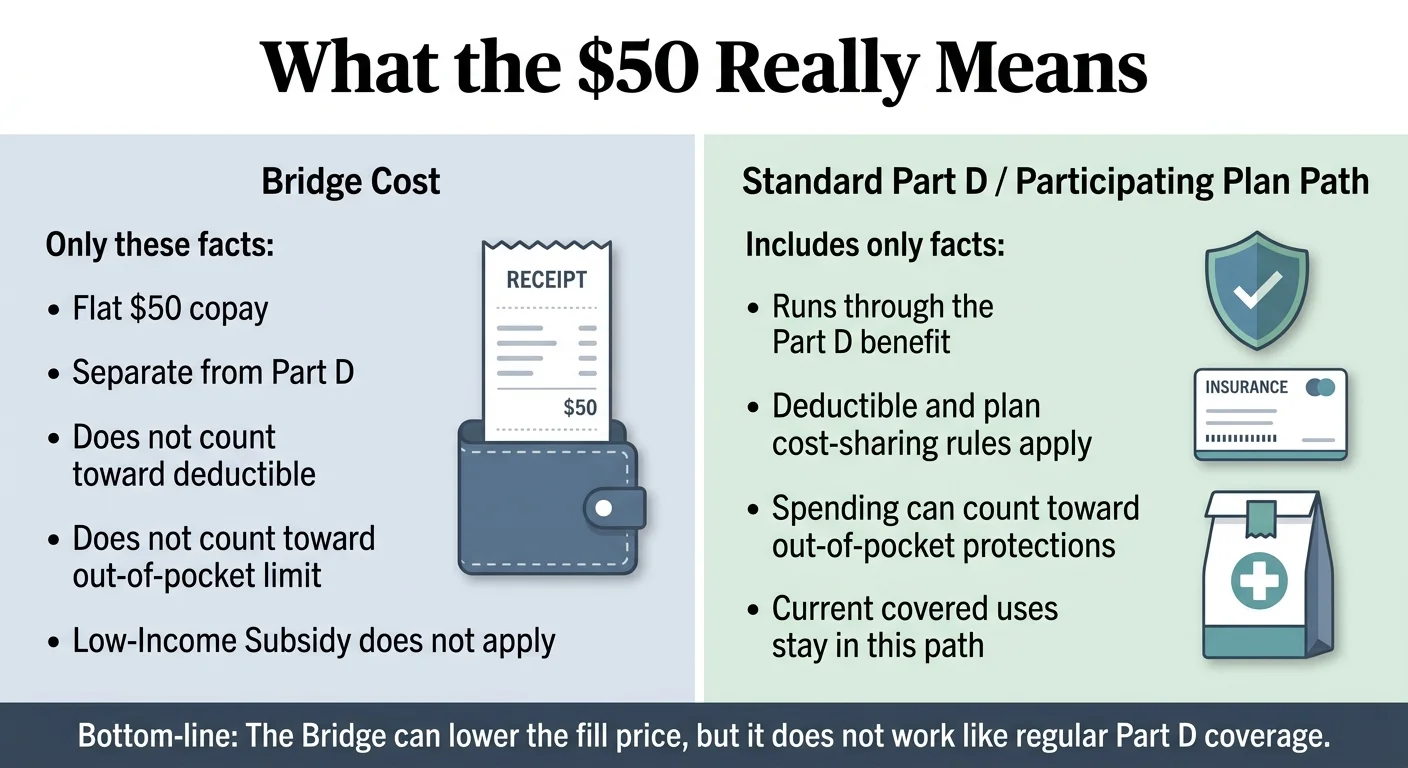

Medicare and Medicaid don’t follow commercial rules. By federal law, standard Medicare can’t cover GLP-1s prescribed solely for weight loss — but a separate, temporary CMS demonstration called the Medicare GLP-1 Bridge lets qualifying Part D members get certain GLP-1s for a flat $50/month starting July 1, 2026. That $50 is provided outside the normal Part D payment flow and does not count toward the Part D deductible or the $2,100 annual cap.

If you’re on Medicare or Medicaid, set aside everything above and start here.

Normal Medicare Part D (covered GLP-1 uses like diabetes):

- Part D does cover GLP-1s for approved conditions like type 2 diabetes, heart-risk reduction, or sleep apnea.

- In 2026: a deductible of up to $615, then 25% coinsurance, until your out-of-pocket spending on covered drugs hits $2,100 — after which covered Part D drugs are $0 for the rest of the year (Medicare.gov).

- That $2,100 is your real Medicare cap for covered drugs.

The Medicare GLP-1 Bridge — the big 2026 change:

- Runs July 1, 2026 through December 31, 2027 (recently extended through end of 2027).

- What’s covered: the Wegovy pill and injection, the Zepbound KwikPen®, and the Foundayo pill. The Zepbound single-dose vial and auto-injector pen are not in the Bridge.

- Cost: a flat $50/month copay. The Bridge drugs are provided outside the Part D payment flow at a $245 net price.

- The critical catch: the $50 does not count toward your Part D deductible or the $2,100 cap.

- Eligibility: must be enrolled in a Medicare Part D plan; qualify on weight/health status; doctor must submit prior authorization. Requests can’t be processed before July 1, 2026.

- It’s temporary. The longer-term BALANCE model has been delayed indefinitely — don’t bank on what comes after 2027.

Quick decision guide for Medicare:

| Your Medicare situation | Look here first | Why |

|---|---|---|

| GLP-1 covered under Part D, and you take other costly drugs | Normal Part D | Those costs help you reach the $2,100 cap |

| Eligible for the Bridge, not near the Part D cap | The Bridge | $50/month is likely cheaper |

| On Medicare and hoping to use a manufacturer coupon | Neither — coupons are barred for government plans | Federal rules exclude Medicare/Medicaid |

| Not sure you qualify | Talk to your doctor about PA before July | The Bridge needs prior authorization |

Medicaid (state by state)

Medicaid isn’t required to cover weight-loss drugs even when they’re FDA-approved. As of January 2026, KFF counted 13 state Medicaid programs covering GLP-1s for obesity — down from 16 in October 2025, after California, New Hampshire, Pennsylvania, and South Carolina dropped coverage (North Carolina reinstated it in December 2025). Every state Medicaid program still covers GLP-1s for type 2 diabetes. Coverage is shifting fast — check your state’s current status: our Medicaid GLP-1 coverage tracker lists it state by state →

So which route is cheapest for your situation?

The cheapest route comes down to one fact: whether your plan covers the drug. If it does and there’s no copay accumulator, use your benefit plus a copay card — that’s the only route where your out-of-pocket maximum truly protects you. If it doesn’t, the lowest reliable cash prices come from manufacturer programs and the telehealth providers that match them, starting near $149/month for pills.

Plan covers GLP-1s for weight loss AND has no accumulator

Use your insurance plus a manufacturer copay card. This is the only scenario where your out-of-pocket maximum caps your year, so it's usually cheapest over 12 months. Confirm the no-accumulator part before you bank on it.

Plan covers it BUT runs an accumulator/maximizer

Do the math both ways. The $25 card is great until it empties; after that you face full cost-share. Sometimes a flat self-pay price ($149–$449/mo) beats grinding through a reset deductible. A coverage check gives you the real copay to compare.

Plan doesn't cover it

Skip the insurance maze and go cash. Lowest reliable prices: oral Wegovy or Foundayo from ~$149/month, Zepbound vials $299–$449/month — through manufacturer programs or the telehealth providers that match them. None counts toward your cap, but the sticker is far below list.

You want the absolute lowest sticker and will DIY everything

Go straight to LillyDirect, NovoCare, or TrumpRx — no membership fee. You give up insurance-fighting help and clinical support, but you pay the rock-bottom cash price. See our cheapest self-pay GLP-1 guide →

On Medicare and qualify

The GLP-1 Bridge at $50/month (from July 2026) will likely beat cash — start the prior-authorization conversation with your doctor now.

Not sure which bucket you’re in?

Take the 60-second matching quiz → and we’ll map your situation to a specific next step.

Where to start with the least friction

If you want a brand-name, FDA-approved GLP-1 — and especially if you want help finding out whether insurance will cover it — the most complete starting point is Ro. It matches manufacturer cash prices, runs your prior-authorization paperwork, and offers a free coverage checker. Sesame Care is a strong second if you’d rather pick your own provider.

An honest question first

Do you even need a provider here? If you already have a prescriber, your plan covers your drug, your PA is done, and your pharmacy runs the card right — no. Use the free manufacturer card directly and skip any membership. We’d rather tell you that than sell you something you don’t need.

Ro — best when coverage is your roadblock

The thing this reader needs most: a free GLP-1 Insurance Coverage Checker plus an insurance concierge that fights for coverage and handles prior-authorization paperwork — the single most useful service if you’re trying to land a covered claim.

Two ways to pay: if you use insurance, Ro’s concierge pursues coverage on brand injection pens (Wegovy pen, Zepbound pen, Ozempic) and you pick up at your pharmacy. If you pay cash, Ro ships at matched manufacturer prices.

Matched cash pricing: same prices as LillyDirect, NovoCare, and TrumpRx — new patients start an oral GLP-1 at $149/month.

Membership, stated plainly: get started for $39 the first month, then as low as $74/month with an annual plan paid upfront — and you’re only charged if you’re approved for treatment.

One honest limit: Ro doesn’t coordinate coverage with government plans like Medicare or TRICARE, and Medicaid enrollees generally can’t use Ro.

Sesame Care — best for picking your own provider

Instead of being matched, you browse licensed providers, read patient feedback, and choose one. Sesame carries FDA-approved Wegovy and Zepbound (plus off-label Ozempic and Mounjaro). It separates a $99/month clinical subscription from the medication, and the Wegovy pill starts around $149/month for lower doses. If provider choice matters more to you than having a concierge do the work, it’s a sensible pick.

Before you pay your first dollar

Before starting an FDA-approved GLP-1, confirm the exact drug and form, whether it’s covered for your diagnosis, whether prior authorization is required, whether your payment counts toward your deductible and cap, and your cash-pay fallback if coverage is denied. The goal is to know both your first-month cost and your worst-case yearly cost before you authorize a single charge.

Your 7-step pre-payment checklist:

- Name the exact drug and form — Wegovy pill, Wegovy pen, Zepbound vial, Zepbound KwikPen, Foundayo, and so on.

- Confirm it’s FDA-approved for your intended use.

- Ask your insurer whether it’s covered for your diagnosis.

- Ask whether prior authorization is required.

- Ask whether your cost counts toward your deductible and out-of-pocket maximum.

- Get the cash-pay price in case coverage is denied.

- Screenshot every price, offer term, expiration date, dose, refill window, and cancellation policy.

Copy-paste phone script for your insurance:

“Can you check whether [drug name, dose, and form] is on my formulary for [your diagnosis]? Does it require prior authorization? If it’s approved, will my payment count toward my deductible and out-of-pocket maximum? And if I use a manufacturer savings card or a cash-pay program instead, will any of that count toward my plan maximum?”

Copy-paste script for any telehealth provider:

“Before I continue — is the medication included in your fee or billed separately? Do you check my insurance coverage? Is prior-authorization help included? And what would my FDA-approved cash-pay fallback cost if my insurance denies coverage?”

Want the insurance side handled for you?

Want someone to check coverage and run the prior-authorization paperwork before you commit? That’s what Ro’s free coverage check is for.

Start my free GLP-1 coverage check on Ro → (sponsored affiliate link, opens in a new tab)How we compared maximum out-of-pocket risk

This comparison doesn’t rank medications by expected weight loss or popularity. It ranks payment routes by how clearly you can know your ceiling, whether your payment counts toward an insurance cap, the strength of the verified cash fallback, the friction between you and the medication, and how exposed the route is to policy or coupon changes.

| Factor | Weight | What it measures |

|---|---|---|

| Clarity of your maximum | 30% | Can you actually know your ceiling, or is it vague |

| Payment counts toward a cap | 25% | This decides whether insurance protects you. |

| Verified cash fallback | 20% | If insurance fails, the cash price becomes your real path. |

| Access friction | 15% | Prior authorization, prescription access, and refill windows all change your true cost. |

| Policy and coupon risk | 10% | Government exclusions, expiration dates, and changing terms can flip the answer. |

What we did not score: expected weight loss, medical superiority, compounded GLP-1 providers, unverified coupon claims, or invented ratings.

What this comparison can’t decide for you

Cost shouldn’t be the only factor in choosing a GLP-1. FDA-approved medications still require a clinician’s evaluation, label-specific eligibility, screening for contraindications, side-effect counseling, and ongoing follow-up. This page compares money, not medical fit.

FDA-approved doesn’t mean right for everyone.

Your clinician decides whether a GLP-1 fits your history. These drugs carry real warnings — for example, Foundayo’s labeling includes a boxed warning about a risk of thyroid C-cell tumors and says it shouldn’t be used by people with a personal or family history of medullary thyroid carcinoma (MTC) or MEN 2, and that it should be avoided with certain strong drug-interaction medicines such as ritonavir (FDA labeling). Wegovy’s prescribing information says it shouldn’t be used with other semaglutide products or other GLP-1 medicines. Talk to a clinician before you start, especially if you have a history of pancreatitis, gallbladder disease, serious stomach or kidney problems, thyroid concerns, an eating disorder, or if you’re pregnant or planning to be.

Why we don’t include compounded GLP-1 prices here.

This page is about FDA-approved medications. Compounded GLP-1 products are not FDA-approved finished drugs, and we won’t compare them as if they’re the same category — the FDA has warned about unapproved and counterfeit compounded GLP-1 products, dosing errors, and adverse-event reports. If you’re weighing a compounded option, that’s a different comparison, and mixing the two would only muddy a decision you’re trying to get clear on.

Frequently asked questions

Short, direct answers to the most common questions about GLP-1 costs and insurance caps.

Is there one FDA-approved GLP-1 out-of-pocket maximum?

No. Your maximum depends on the route: covered insurance, an excluded benefit, manufacturer cash-pay, Medicare Part D, or the Medicare GLP-1 Bridge. For 2026 Marketplace plans, the cap on covered in-network care cannot exceed $10,600 for an individual or $21,200 for a family.

Do FDA-approved GLP-1s count toward your out-of-pocket maximum?

Only if your plan covers the drug and you are paying copays or coinsurance on a covered claim. Coverage for weight loss is inconsistent, and cash-pay programs sit outside insurance — so for many weight-loss users, the answer is no.

What is the cheapest FDA-approved GLP-1 without insurance in 2026?

At self-pay prices, the oral options start lowest — around $149 per month for starting doses of the Wegovy pill and Foundayo. Zepbound vials start at $299 per month. The cheapest choice for you also depends on dose, refill timing, and whether the price is a promotion or your steady rate.

Why am I covered but still paying hundreds a month?

Because covered is not the same as cheap. Before you meet your deductible you can pay the full negotiated price on a covered drug, and if your plan uses coinsurance you keep paying a percentage of a four-figure price until you reach your out-of-pocket maximum.

Does the Medicare GLP-1 Bridge count toward TrOOP?

No. CMS says the Bridge's $50 monthly copay is outside the normal Part D payment flow and does not count toward your true out-of-pocket (TrOOP) costs or the 2026 Part D cap of $2,100.

Can I use a Wegovy or Zepbound savings card with Medicare or Medicaid?

No. The manufacturers' savings cards require commercial insurance, and federal rules bar them for Medicare, Medicaid, and other government programs. If you are on Medicare, look at the GLP-1 Bridge instead.

Is the cheapest cash price the same as my out-of-pocket cost?

No. Out-of-pocket cost is what you actually pay; the out-of-pocket maximum is an insurance cap that only applies to covered claims. A $149 per month cash price is real money you will pay, but it does not count toward your insurance cap.

Do Ro membership fees count toward my insurance out-of-pocket maximum?

No. A telehealth membership fee is separate from your insurance. Insurance coverage applies to eligible medications, not the membership.

Is compounded semaglutide included in this comparison?

No. This page covers FDA-approved GLP-1 medications only. Compounded products are not FDA-approved finished drugs and should not be treated as interchangeable with them.

Still deciding which GLP-1 program is right for you?

Take our free 60-second matching quiz and get a personalized action plan — including whether your situation is one where insurance is worth fighting for, and the cheapest legitimate path for you.

Get my personalized GLP-1 action plan →About this comparison

Published by The RX Index — independent guidance for choosing your GLP-1 path. We evaluate providers and treatment routes on what actually matters — clinical legitimacy, care quality, transparency, access, and cost — and help you decide where to start.

How we made it: We verified every price and policy here against primary and high-authority sources in June 2026 — HealthCare.gov and CMS/Medicare.gov for insurance rules, the manufacturers (NovoCare, LillyDirect) and ro.co for prices, FDA approval and labeling for drug status, and KFF for coverage data. We did not sign up for these plans ourselves; this is a verification of published prices, policies, and regulations, refreshed monthly during 2026.

Sources

- HealthCare.gov — 2026 out-of-pocket maximum ($10,600 / $21,200); what counts toward the cap

- Medicare.gov / CMS — 2026 Part D deductible (up to $615) and $2,100 cap; Medicare GLP-1 Bridge page (dates, $50 copay, $245 net price, outside Part D payment flow; extended through 12/31/2027)

- KFF — copay accumulator prevalence (17% large employers, 34% of 5,000+ firms, ~66% of Marketplace plans); Medicaid count (13 states Jan 2026, down from 16); BALANCE model delayed

- Crohn's & Colitis Foundation; Patients Rising — copay accumulator/maximizer mechanics and 2026 legal status

- NovoCare (novocare.com) — Wegovy pill and pen prices; Ozempic prices; Wegovy list $1,349

- LillyDirect / Lilly — Zepbound Self Pay Journey prices and 45-day rule; Foundayo approval (4/1/2026) and prices $149–$349

- FDA — oral Wegovy approval Dec 2025; Foundayo labeling (boxed warning); unapproved compounded GLP-1 warnings

- ro.co — Ro Body membership ($39 first month / as low as $74/mo annual); matched pricing; free Insurance Coverage Checker; concierge; government plan limits

- Sesame Care — $99/mo subscription; FDA-approved Wegovy and Zepbound; Wegovy pill from ~$149/mo

- U.S. News; KFF Health News — TrumpRx.gov (cash-pay portal, doesn't count toward OOPM); Novo list-price cut to $675 for Wegovy/Ozempic/Rybelsus effective 1/1/2027

🗓️ Last verified: June 16, 2026. Written by The RX Index editorial team. This page is information, not medical or financial advice.

This page was verified against primary sources (HealthCare.gov, CMS, NovoCare, LillyDirect, FDA, KFF) in June 2026. Prices and policy rules are re-checked monthly during 2026 because they are moving fast this year. No manufacturer or telehealth provider paid for placement or influenced the route comparison. See how we evaluate providers.

Your situation changes the answer

Find My GLP-1 Path

The right GLP-1 provider isn't the same for everyone. It depends on your state, your insurance and formulary, whether you want an FDA-approved or compounded medication, your preferred route (injection or oral), and your budget. Because a general answer can't resolve those for you, use The RX Index's Find My GLP-1 Path tool to get a personalized provider match with source-verified pricing before you choose.

- What it asks: your state, insurance situation, medication preference, budget, and support needs

- What you get: a personalized shortlist of GLP-1 providers matched to your situation, with verified pricing and the right questions to ask

- Cost: free · about 2 minutes · no signup