Brand-Name GLP-1 Patient Savings Card Comparison 2026

Published: · Last reviewed:

By The RX Index Editorial Team

Some provider links on this page are sponsored, and we may earn a commission if you start care through one. Manufacturer savings cards are free and come straight from the drugmaker — those links are never sponsored, and commissions never change what we recommend.

The $25 price on a brand-name GLP-1 patient savings card is real — but it’s conditional. In this 2026 comparison, every major card (Wegovy, Zepbound, Foundayo, Ozempic, and Mounjaro) can drop your cost to about $25 a month — but only when you have commercial insurance and your plan covers that exact drug. If your plan doesn’t cover it, there are separate self-pay prices. If you’re on Medicare or Medicaid, a regular card won’t work for you at all — but a new $50 Medicare GLP-1 Bridge launches July 1, 2026.

If you’ve seen the “as little as $25” ad and wondered whether it’s real or bait, here’s the honest answer: it’s real — it’s just conditional. The thing that actually decides your price isn’t the coupon. Find your lane below, then we’ll show you the one thing worth checking before you fill a single prescription.

Two quick definitions so the rest of this page is easy:

Commercial insurance = a plan from a job, or one you buy yourself. Not a government plan like Medicare or Medicaid.

Savings card (a.k.a. copay card or coupon) = a discount from the drugmaker that lowers your price at the pharmacy. It is not insurance — it works on top of a plan you already have.

Find your lane in 10 seconds

| Your situation | What a savings card can usually do | Your best next step |

|---|---|---|

| Commercial insurance, and your plan covers the drug | Lower your cost toward ~$25/month, up to a monthly cap | Confirm coverage and prior authorization |

| Commercial insurance, but your plan does not cover the drug | A smaller discount — you’ll still owe a real balance | Compare self-pay prices instead |

| No insurance at all | The $25 card usually won’t apply (Wegovy is the exception — see below) | Compare the drugmaker’s self-pay programs |

| Medicare (Part D) | A regular card is blocked by federal law | Check the new $50 Medicare GLP-1 Bridge |

| Medicaid, VA, or TRICARE | A regular card is blocked by federal law | Check your plan’s covered-drug list |

| The pharmacy says your card “didn’t work” | Could be coverage, a cap, a processing mistake, or a plan rule | Use our rejection checklist below |

Have commercial insurance?

Before you chase a coupon, find out whether your plan actually covers the drug — that’s the thing that decides everything else. Ro’s free GLP-1 Insurance Coverage Checker contacts your plan and sends back a written report, no prescription and no commitment.

Check my coverage free → (sponsored affiliate link, opens in a new tab)Which brand-name GLP-1 savings card is best in 2026?

For weight loss, the three cards worth comparing first are Foundayo, Wegovy, and Zepbound, because those are the GLP-1s the FDA has approved for weight management. Ozempic and Mounjaro have cards too, but they’re diabetes drugs and their cards require a diabetes prescription. The “best” card depends less on the drug name and more on whether your plan covers it.

When your plan covers the drug, all of these cards land you in about the same place — roughly $25 a month. So crowning one “winner” on the $25 number alone is almost pointless. The real differences show up in two places: how big the monthly savings cap is, and what the price falls back to if your plan doesn’t cover the drug.

Skip the trophy and think by your situation:

- If your plan covers the drug: Foundayo, Wegovy, or Zepbound can all get you near $25. Pick with your prescriber based on what fits your body and health history — not the coupon.

- If your plan doesn’t cover it (or you’re paying cash): Foundayo has the lowest published brand-name starting price right now — about $149/month to self-pay through LillyDirect. That makes it the strongest “coverage is uncertain” pick on price alone.

- If you have type 2 diabetes: Ozempic and Mounjaro belong in your comparison — but as diabetes drugs, not a weight-loss shortcut. More on why that matters below.

- If you’re on Medicare: skip the regular cards. The new Bridge gives you a flat $50 a month for Wegovy, Foundayo, or the Zepbound KwikPen starting July 1, 2026.

Not sure which lane you’re in?

Take our free 60-second GLP-1 path quiz and get your next step before you chase the wrong coupon. The RX Index gives independent guidance for choosing your GLP-1 path.

Find my GLP-1 path →Brand-Name GLP-1 Patient Savings Card Comparison 2026: the full table

Every brand-name GLP-1 savings card shares one core rule: it drops your cost to about $25 a month when your commercial plan covers the drug, and it does nothing on government insurance. What changes from card to card is the savings cap, whether a diabetes diagnosis is required, and the cash price if your plan won’t cover it.

We pulled the numbers below straight from each drugmaker’s official savings pages.

| Brand (medicine) | Maker | FDA-approved for | If your plan covers it | If your plan doesn’t cover it / self-pay | Government plans? |

|---|---|---|---|---|---|

| Wegovy® (semaglutide; pen + pill) Full Wegovy savings guide → | Novo Nordisk | Weight management (also heart-risk reduction) | As little as $25/month (max savings $100/month) | Self-pay via NovoCare: pill $149/mo (1.5 mg & 4 mg; 4 mg price holds through Aug 31, 2026, then $199); pen $199/mo intro for 0.25 & 0.5 mg (through December 31, 2026), then $349/mo up to 2.4 mg, $399/mo for HD 7.2 mg | No |

| Zepbound® (tirzepatide; vial, pen, KwikPen®) Full Zepbound savings guide → | Eli Lilly | Weight management (also sleep apnea) | As little as $25/fill (max $100/mo, $1,300/yr, 13 fills; expires 12/31/2026) | Self-pay via LillyDirect: $299 (2.5 mg), $399 (5 mg), $499 (7.5 mg), $699 (10–15 mg). Purchase offer: 7.5–15 mg doses $449/mo if you refill within 45 days | No |

| Foundayo™ (orforglipron; pill) Full Foundayo savings guide → | Eli Lilly | Weight management (FDA-approved Apr 1, 2026) | As little as $25/month (max $100/mo, $1,000/yr, 10 fills; expires 12/31/2026) | Self-pay via LillyDirect: $149 (0.8 mg), $199 (2.5 mg), $299 (5.5–17.2 mg). Top two doses revert to $349 without 45-day refill | No commercial card — but Bridge-eligible ($50/mo) |

| Ozempic® (semaglutide) Full Ozempic savings guide → | Novo Nordisk | Type 2 diabetes (not weight loss) | As little as $25/month with a covered diabetes prescription (max $100/month) | Self-pay via NovoCare; compare cash prices | No |

| Mounjaro® (tirzepatide) Full Mounjaro savings guide → | Eli Lilly | Type 2 diabetes | As little as $25/fill with coverage (max $150/mo, $1,950/yr, 13 fills; expires 12/31/2026) | If commercial plan doesn’t cover it: $499/month (max savings $647/mo, $8,411/yr) | No |

| Also: Rybelsus® and Trulicity® (diabetes), and Saxenda® (weight; older) | Novo / Lilly | Diabetes (Rybelsus, Trulicity); weight (Saxenda) | Diabetes cards: about $25 with coverage. Saxenda’s savings offer ended for new patients (June 30, 2023) | Varies | No |

What we verified — and what we didn’t.

We pulled these numbers from the drugmakers’ official savings pages (NovoCare for Wegovy and Ozempic; Lilly for Zepbound, Mounjaro, and Foundayo) and from CMS for the Medicare program. We checked covered-plan prices, monthly and yearly caps, fill limits, expiration dates, self-pay prices, and the Medicare rules. We could not verify your specific plan, your pharmacy’s system, your diagnosis, or whether a prior authorization will be approved. Confirm all prices with your pharmacist and the manufacturer before filling.

The one thing that decides your price

A manufacturer savings card is not insurance, and the headline “$25” only applies if your commercial plan actually covers the drug. If your plan excludes it — which many employer plans still do for weight-loss drugs — the card’s help shrinks. And if you’re on any government plan, federal law blocks the card entirely. So the real question isn’t “which coupon.” It’s “can I get covered.”

The drugmaker’s ad can be 100% true, the card can work exactly as designed — and you can still pay more than $25. That’s not a scam. That’s the cap meeting your copay. Any page that shouts “as little as $25” without showing you this math is leaving you half-informed.

If your plan covers your drug, you’re basically done — grab the card. If it doesn’t, don’t give up. The next sections show you how to get covered, and the cash options if you can’t.

Do you actually qualify for a $25 GLP-1 savings card?

You usually qualify if you’re a U.S. adult, you have a valid prescription, you have commercial insurance, and your plan covers that exact drug. You’re shut out if you have Medicare, Medicaid, the VA, or TRICARE — that’s a federal rule, not the drugmaker being difficult. There’s no income limit on the card itself; the gate is your insurance type.

Run yourself through this checklist:

- You have a prescription for the drug’s FDA-approved use.

- You’re 18 or older and live in the U.S. (or Puerto Rico, where the card allows).

- You have commercial drug insurance.

- Your plan covers that medication — or the card has a separate, smaller “not-covered” offer.

- You’re not on a government plan.

Why government insurance is blocked.

A federal anti-kickback law bars drugmakers from using coupons to lower costs for people on government insurance. This shuts out Medicare, Medicaid, the VA, and TRICARE. There’s no workaround — but if that’s you, the new Medicare path below may help.

Good news if you’re on a marketplace, federal, or state-employee plan.

Novo Nordisk notes that ACA marketplace plans, the Federal Employees Health Benefits (FEHB) program, and state-employee plans count as commercial — not government — for the Wegovy offer. So if you’re in one of those, you may still qualify.

The two biggest mistakes.

First, assuming “I have insurance” is enough — the card needs commercial insurance that covers the exact drug. Second, assuming the card creates coverage. It doesn’t. A card lowers your copay after your plan agrees to cover the drug; it can’t force a plan to say yes.

Why “as little as $25” doesn’t always mean you’ll pay $25

“As little as $25” means $25 is the lowest price you could get — not the price you will get. Every card has a cap, which is the most it will pay for you each month. If your insurance copay is higher than that cap, you pay the difference. So the card can work perfectly and you can still pay more than $25.

Here’s the math that actually changes your bill:

Example 1 — the card gets you close to $25

- Your insurance copay: $120

- The card’s monthly cap: $100

- The card pays $100. You pay about $25. 🎉

Example 2 — same card, very different result

- Your insurance copay: $300

- The card’s monthly cap: $100

- The card pays $100. You still owe about $200. 😬

Same card. Same rules. Wildly different price — because your plan’s copay is what decides it. This matters more in 2026 because the weight-loss cards cap monthly savings around $100. Lilly’s Zepbound card, for example, lists a $100-per-month savings cap and a $1,300-per-year maximum for covered commercial patients.

So when your number isn’t $25, it’s almost never the coupon’s fault. It’s usually one of two things: your plan doesn’t cover the drug, or a prior authorization is stuck. (Prior authorization — “PA” — is your insurer’s permission slip, an extra OK your doctor sends in before the plan will cover certain drugs.) A denied or missing PA is one of the top reasons people get quoted hundreds instead of $25. The card can’t fix that. Getting the PA approved can.

Think a denial or a missing prior authorization is what’s standing between you and $25?

Ro’s insurance team submits the prior-authorization paperwork for you, so you’re not fighting your insurer alone — and if coverage is denied, you can switch to a cash price without starting over.

See how Ro handles coverage → (sponsored affiliate link, opens in a new tab)Diabetes cards vs. weight-loss cards: why Ozempic and Mounjaro are different

Ozempic and Mounjaro are FDA-approved for type 2 diabetes — not weight loss. Their savings cards require a diabetes prescription, and your plan has to be covering the drug for diabetes. The FDA-approved weight-loss brands are Wegovy, Zepbound, and Foundayo. If a doctor prescribed Ozempic or Mounjaro for weight loss, the card terms may not apply, and coverage is unlikely.

This sounds like fine print, but it’s the most expensive mix-up on the topic. Here’s the simple map:

| Brand | Medicine | FDA-approved for |

|---|---|---|

| Wegovy® | semaglutide | Weight management (also heart-risk reduction) |

| Zepbound® | tirzepatide | Weight management (also sleep apnea) |

| Foundayo™ | orforglipron | Weight management |

| Ozempic® | semaglutide | Type 2 diabetes (not weight loss) |

| Mounjaro® | tirzepatide | Type 2 diabetes |

| Rybelsus® | semaglutide (pill) | Type 2 diabetes |

| Saxenda® | liraglutide | Weight management (older; savings offer ended for new patients) |

Notice that the famous pairs share a medicine but not a use: semaglutide is in Ozempic, Rybelsus, and Wegovy; tirzepatide is in Mounjaro and Zepbound. Foundayo (orforglipron) is a different molecule. Same medicine does not mean the same prescription, dose, coverage, or savings card.

Want a single-drug deep dive? See our full Ozempic savings card guide and Mounjaro savings card guide for the diabetes side.

Each card up close (the verdict first, then the details)

Wegovy® savings card — the best-known semaglutide weight-loss card

Verdict

The most recognizable FDA-approved weight-loss brand. If your commercial plan covers Wegovy, the card gets you to about $25 a month. If it doesn’t, you can still use NovoCare’s program to self-pay — and the Wegovy pill is the lowest-cost branded entry at $149/month.

Through NovoCare, commercially insured patients whose plan covers Wegovy pay as little as $25/month, with savings capped at $100/month. Government plans are excluded. Wegovy is a little different from the others: its program also covers self-pay — even uninsured patients with a valid prescription can use it. Self-pay prices are $149/month for the Wegovy pill (1.5 mg and 4 mg, with the 4 mg price holding through August 31, 2026, then $199), and $199/month as an intro for the pen (0.25 and 0.5 mg, through December 31, 2026), then $349/month up to the 2.4 mg dose and $399/month for Wegovy HD (7.2 mg).

Full Wegovy savings guide →Zepbound® savings card — the strongest tirzepatide weight-loss card

Verdict

The leading brand-name tirzepatide option for weight loss, and it also carries an FDA approval for obstructive sleep apnea in adults with obesity. Great value if your plan covers it; if not, the LillyDirect self-pay vials are your fallback — but watch the refill window.

From Lilly’s official terms: covered commercial patients pay as little as $25 per fill, capped at $100/month and $1,300/year, for up to 13 fills, with the card expiring 12/31/2026. If your plan doesn’t cover Zepbound, self-pay through LillyDirect runs $299 (2.5 mg), $399 (5 mg), $499 (7.5 mg), and $699 (10–15 mg). A purchase offer drops the 7.5–15 mg doses to $449/month — but only if you complete each refill within 45 days of your last one. Miss that window and the price jumps back up.

Full Zepbound savings guide →Foundayo™ savings card — the newest option, and the lowest cash floor

Verdict

The new kid, and a strong “coverage is uncertain” pick — a once-daily pill with the lowest published brand-name self-pay price ($149/month). The catch: it’s so new that plan coverage is still spreading.

The FDA approved Foundayo (orforglipron) on April 1, 2026 for adults with obesity, or overweight with a weight-related condition. It’s the first GLP-1 pill you can take any time of day with no food or water rules. With commercial coverage, eligible patients pay as little as $25/month, capped at $100/month and $1,000/year, for up to 10 fills, expiring 12/31/2026. Without coverage, LillyDirect self-pay is $149 (0.8 mg), $199 (2.5 mg), and $299 (5.5–17.2 mg), with the top two doses reverting to $349 unless you refill within 45 days.

Full Foundayo savings guide →Ozempic® savings card — a diabetes card, not a weight-loss shortcut

Verdict

Worth knowing about if you have type 2 diabetes. It is not a back door to cheap weight-loss medication.

Through NovoCare, commercially insured patients with a covered diabetes prescription pay as little as $25/month, up to a $100/month cap. There’s no income limit — just the insurance and diabetes-prescription requirements. If you don’t have diabetes, this card almost certainly won’t help; look at Wegovy, Zepbound, or Foundayo instead.

Full Ozempic savings guide →Mounjaro® savings card — the strongest diabetes card on price

Verdict

A strong value for people with type 2 diabetes, with a higher monthly savings cap than the weight-loss cards. Again — diabetes only.

Lilly’s terms let eligible commercially insured diabetes patients pay as little as $25 for a 1-, 2-, or 3-month fill, capped at $150/month and $1,950/year, up to 13 fills, expiring 12/31/2026. If your commercial plan doesn’t cover Mounjaro, the card sets the price at $499/month (with savings up to $647/month and $8,411/year).

Full Mounjaro savings guide →The rest, briefly

Rybelsus® (a semaglutide pill for diabetes) and Trulicity® (an older Lilly diabetes shot) both have manufacturer savings cards for eligible, covered commercial patients — useful if you’re treating diabetes. Saxenda® (liraglutide) is an older daily weight-loss injection; its manufacturer savings offer was discontinued for new patients on June 30, 2023, so an old Saxenda coupon won’t help new starters.

What to do if your savings card is rejected at the pharmacy

A rejected card doesn’t always mean you don’t qualify. The most common causes are: your plan doesn’t cover the drug, the pharmacy didn’t run the card behind your insurance, you hit a cap, the card expired, or you’re on a government plan. Many of these are fixable on the spot or with one call — but some need a prior authorization, plan coverage, or a different payment lane.

Pharmacy rejection checklist:

- Confirm the prescription is for the exact drug and form on your card.

- Confirm the card is activated (some need a quick sign-up first).

- Ask: “Did you run my insurance first, then the card?”

- Ask the pharmacist to process the card as a secondary payer (after your insurance).

- Ask whether your plan covers the drug at all.

- Ask whether a prior authorization is required and not yet approved.

- Ask whether you’ve hit a monthly, yearly, or fill limit.

- Ask whether a plan rule — like a “copay accumulator” — is blocking the card. (A copay accumulator is a plan setting that stops manufacturer card dollars from counting toward your deductible, which can make the card look like it “stopped working.”)

- Ask whether your plan type is excluded (a government plan will be).

- Still stuck? Call the manufacturer support number printed on the card.

Copy-and-paste pharmacist script:

“Can you please run my primary commercial insurance first, then process the manufacturer savings card as secondary? If it still rejects, can you tell me the rejection reason — is it coverage, prior authorization, a plan accumulator, a plan exclusion, or card eligibility?”

Then ask the pharmacist to write down the rejection code and which bucket it falls in (coverage, PA, cap, plan type, or accumulator). That one note tells you exactly which fix you need.

What not to do: don’t quietly pay full price without learning the reason. Don’t switch medications just because one card failed. And don’t assume a GoodRx coupon will stack on top of the manufacturer card — it won’t (more below).

Card rejected and still not sure why?

Take our free 60-second quiz and we’ll route you to the right fix — a coverage check, an appeal, a cash-pay option, or the Medicare path.

Get my next step →Can you use a GLP-1 savings card without insurance?

Usually not — the $25 commercial card needs commercial insurance and drug coverage. If you’re uninsured, or your plan won’t cover the drug, your real options are the drugmaker’s own self-pay programs, the government’s TrumpRx site, and patient-assistance programs if your income is low.

First, an important difference people miss: “my plan doesn’t cover it” is not the same as “I have no insurance.” Some drugmaker offers are written for one and not the other, so read which one applies to you.

Where to look if you’re paying cash:

- LillyDirect (Zepbound, Mounjaro, Foundayo): Zepbound vials $299–$699/month by dose (with the $449 refill offer on higher doses); Foundayo from $149/month.

- NovoCare (Wegovy, Ozempic): the Wegovy pill starts at $149/month and the pen at $199/month intro — and for Wegovy, the uninsured can use the same NovoCare program to get those prices.

- TrumpRx (TrumpRx.gov): a government site that links to direct cash-pay discounts for people not using insurance. Headline prices include the Wegovy pill at $149/month, the Wegovy pen at $199/month, Ozempic at $199/month, and Zepbound at $299/month (Foundayo routes through LillyDirect). These aren’t coupons and don’t need insurance.

- Patient-assistance programs: for low-income uninsured patients, NovoCare runs a program that can provide medication free if you qualify.

If you also still need a prescription, a telehealth provider can bundle the doctor visit with the medication. For paying-cash, brand-name shoppers who want to compare options or check Costco-member pricing on Wegovy and Ozempic, Sesame Care is a solid fit.

Paying cash and want provider choice?

Compare Sesame Care’s branded GLP-1 options and Costco-member pricing — and confirm the current price at checkout. (Need a prescription and want someone to chase coverage first? That’s Ro — see below.)

Compare cash-pay options on Sesame → (sponsored affiliate link, opens in a new tab)Can Medicare, Medicaid, VA, or TRICARE patients use these cards?

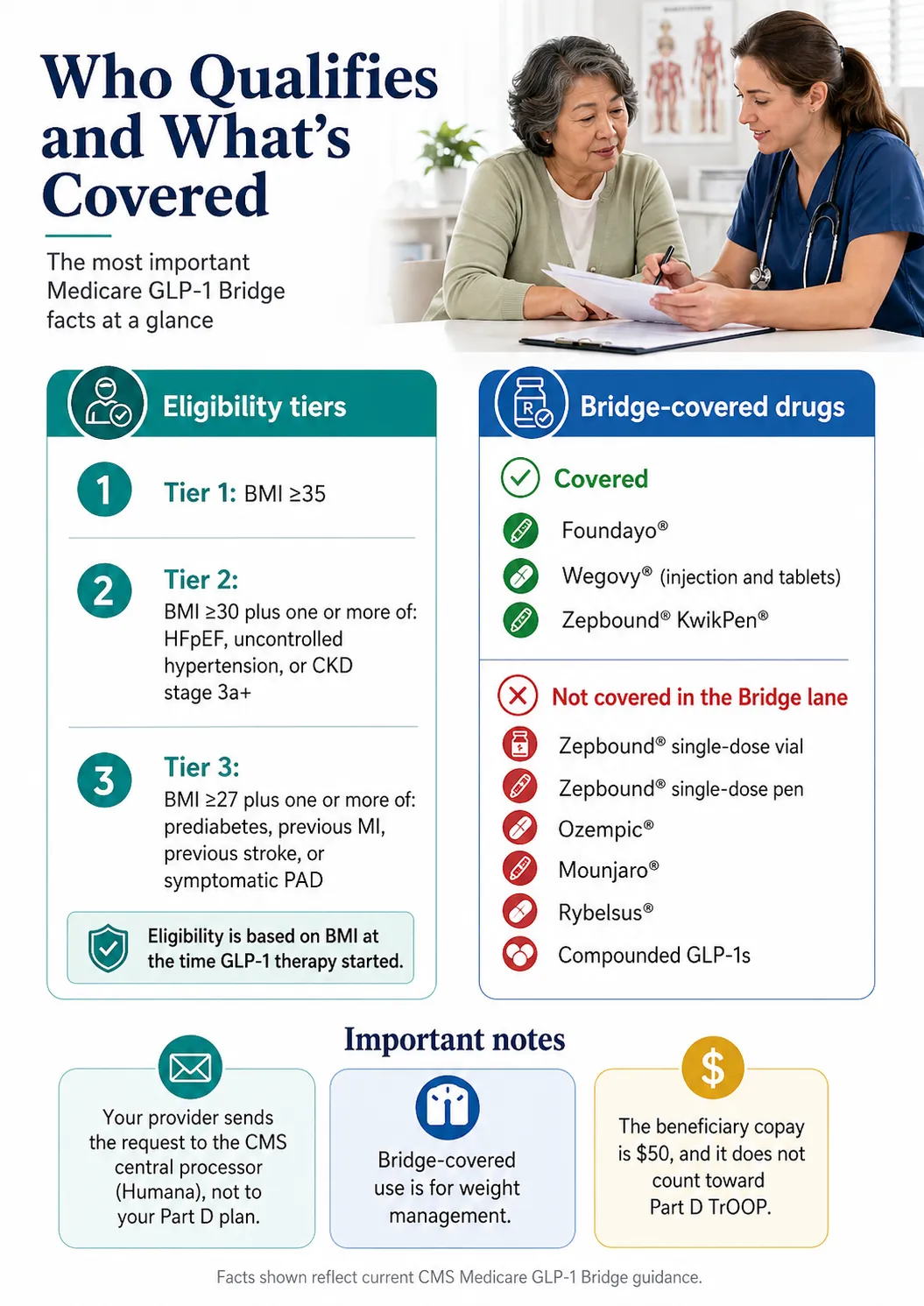

No — regular manufacturer savings cards are blocked for everyone on a government plan. But starting July 1, 2026, eligible Medicare Part D members can get Wegovy, the Zepbound KwikPen, or Foundayo for a flat $50 a month through the new Medicare GLP-1 Bridge. The $50 stays the same no matter your dose, and you can’t add a coupon on top of it.

If you’re on Medicare, don’t waste an hour trying to force a commercial card to work. You have your own path now — and it’s genuinely new.

The Medicare GLP-1 Bridge, straight from CMS:

- What it is: a short-term Medicare program that covers select weight-loss GLP-1s for a flat $50/month.

- When: July 1, 2026 through December 31, 2027.

- Which drugs (for weight only): all forms of Foundayo, all forms of Wegovy, and the Zepbound KwikPen. Zepbound vials and pens, plus Ozempic and Mounjaro, are not in the Bridge.

- Who qualifies: you must be in a Medicare Part D plan (a standalone drug plan or a Medicare Advantage plan with drug coverage) and meet the medical rules:

- BMI 35 or higher, or

- BMI 30 or higher with heart failure (preserved ejection fraction), uncontrolled high blood pressure, or chronic kidney disease (stage 3a or above), or

- BMI 27 or higher with prediabetes, a past heart attack, a past stroke, or symptomatic peripheral artery disease.

- The fine print that matters: the Bridge runs outside your regular Part D benefit. The $50 doesn’t count toward your deductible or out-of-pocket max, Extra Help doesn’t apply, and you can’t stack a manufacturer coupon. Your doctor submits a prior authorization — and requests can’t be processed before July 1, 2026.

- One important exclusion: if your GLP-1 is for a use Medicare Part D already covers (type 2 diabetes, obstructive sleep apnea, MASH, or Wegovy for heart-risk reduction), you use your Part D plan, not the Bridge.

For diabetes GLP-1s like Ozempic and Mounjaro, Medicare Part D has long covered them for diabetes. In 2026, your total out-of-pocket spending on covered drugs is capped at $2,100 for the year.

On Medicare?

Don’t chase a commercial coupon — check the Medicare GLP-1 Bridge path and ask your doctor whether you meet the BMI rule.

See the Medicare GLP-1 Bridge guide →Can you stack GoodRx, SingleCare, HSA/FSA, and a savings card?

Usually no. A manufacturer card works behind your commercial insurance. GoodRx and SingleCare are cash-discount coupons that replace insurance for that fill. You compare them and pick the lower one — you don’t combine them. And the card terms say you can’t get reimbursed through an HSA or FSA for the savings the card gave you.

| Payment type | How it works | Stackable with manufacturer card? |

|---|---|---|

| Commercial insurance | Your plan’s benefit. Usually the first payer. | Yes — card rides on top |

| Manufacturer savings card | From the drugmaker; needs commercial insurance; secondary payer. | — |

| GoodRx / SingleCare | Cash-discount coupons; used instead of insurance for that fill. | No — pick one or the other |

| Patient-assistance program | Income-based help from the manufacturer; separate process. | Separate — not combined |

On HSA/FSA: some out-of-pocket medical costs can be paid with HSA or FSA money, but the savings a manufacturer card gives you generally can’t be reimbursed — Lilly’s terms say you can’t seek HSA, FSA, or other account reimbursement for the discount the card provided. Don’t double-dip by accident.

Who can help you make a savings card actually work?

A savings card doesn’t prescribe medication, check whether a drug is safe for you, submit a prior authorization, or call your insurer. If you need those steps handled, Ro is the strongest first stop for coverage checks and prior-authorization help, and Sesame is the better option for cash-pay, brand-name shoppers who want provider choice.

First, an honest question

Do you even need a provider here? If you already have a prescriber, your plan already covers your drug, your prior authorization is done, and your pharmacy runs the card right — no. Use the free manufacturer card directly and skip any membership. We’d rather tell you that than sell you something you don’t need.

Ro — best when coverage is your roadblock

| Ro says… | What we checked | What it means | What it doesn’t mean |

|---|---|---|---|

| The GLP-1 coverage checker is free to everyone | ro.co | You can check coverage with no prescription and no commitment | It doesn’t guarantee your plan will cover the drug |

| Cash prices match LillyDirect, NovoCare, and TrumpRx | ro.co (Ro’s stated claim) | The medication price is the same as buying direct | The Ro Body membership is billed on top, separately |

| Membership is $39 first month, then as low as $74/mo on an annual plan | ro.co | A predictable membership fee with coaching and care | Medication is not included in the membership fee |

In plain terms: Ro carries Foundayo™, the Wegovy® pill, the Wegovy® pen, the Zepbound® pen, and the Zepbound® KwikPen®, runs a free GLP-1 Insurance Coverage Checker plus an insurance concierge that submits prior-authorization paperwork, and prices its medication to match LillyDirect, NovoCare, and TrumpRx. Membership is $39 for the first month, then $149/month — or as low as $74/month if you prepay for the year — with medication billed separately.

The honest trade-off: Ro is not the rock-bottom cash sticker price, and you don’t need it if your coverage and prescription are already sorted. If paying the absolute lowest price with no membership is your only goal, the drugmaker’s own self-pay program or Sesame’s pay-per-visit option will suit you better. But because Ro bundles the prescriber, the free coverage check, and the prior-authorization help, it’s the right call when “my plan keeps denying it” is your real problem.

Want someone to fight the coverage battle for you?

Run Ro’s free coverage checker and see current pricing — you’ll get a written report before you pay anything.

Check my coverage with Ro → (sponsored affiliate link, opens in a new tab)Sesame — best for cash-pay, brand-name comparison

Sesame is the better fit if you’re paying cash, want to choose your own provider, and want to compare branded options without making insurance the center of everything. It lists brand-name GLP-1 options and is known for Costco-member pricing on Wegovy and Ozempic. Confirm the current price and any program fee at checkout before you commit.

Why people get blindsided by GLP-1 savings cards

The number-one reason people feel tricked isn’t a scam — it’s the gap between “as little as $25” and what their specific plan charges. Coverage changes, missing prior authorizations, monthly caps, and government-plan exclusions are the usual culprits.

- Someone whose employer plan dropped weight-loss coverage for the new year, so a card that worked in December leaves them paying full price in January.

- Someone who activates a Zepbound or Mounjaro card and gets no discount at the counter — because their plan doesn’t cover the drug, so the covered-tier price never applies.

- Someone on Medicare who assumes a coupon will work, not realizing federal law blocks it.

What changed for GLP-1 savings cards in 2026?

2026 made the old “which coupon is cheapest” question incomplete. A new oral drug (Foundayo) arrived, a new $50 Medicare path opened, and tighter monthly caps mean the headline price matters less than your coverage.

| Date | What happened |

|---|---|

| April 1, 2026 | FDA approves Foundayo (orforglipron) — the first GLP-1 pill with no food-or-water timing rules and the lowest-priced brand-name self-pay option in our table. |

| April 6, 2026 | CMS updates the Medicare Bridge to add Foundayo and to clarify that only the Zepbound KwikPen is included. |

| July 1, 2026 | The Medicare GLP-1 Bridge launches ($50/month), and prior-authorization requests start being accepted. |

| December 31, 2026 | The 2026 Lilly cards (Zepbound, Mounjaro, Foundayo) expire and reset for the new year. |

| December 31, 2027 | The Medicare GLP-1 Bridge is scheduled to end. |

Brand-name GLP-1 savings card FAQs

Short, direct answers to the follow-up questions people ask after comparing cards.

Which brand-name GLP-1 savings card is best in 2026?

For weight loss, compare Foundayo, Wegovy, and Zepbound first — they are the FDA-approved weight-management brands with active savings cards. If your plan covers the drug, they all land near $25 a month, so the better tiebreaker is the monthly cap and the cash fallback price. Foundayo has the lowest published self-pay starting price at about $149 a month through LillyDirect.

Can I really get a GLP-1 for $25 a month?

Yes — if you have commercial insurance, your plan covers the drug, and you meet the card's eligibility rules. Because every card has a monthly savings cap (around $100 on the weight-loss cards), $25 is the lowest possible price, not a guarantee. A higher insurance copay can leave you paying more even when the card works exactly as designed.

Can I use a GLP-1 savings card without insurance?

Usually not for the $25 card, which requires commercial insurance that covers the drug. If you are uninsured, compare the drugmaker's self-pay programs (LillyDirect for Zepbound, Foundayo, and Mounjaro; NovoCare for Wegovy and Ozempic), the government's TrumpRx site, and patient-assistance programs. For Wegovy specifically, uninsured patients can use NovoCare's program to reach self-pay prices starting at $149 a month.

Can Medicare patients use GLP-1 savings cards?

No. Federal law blocks manufacturer savings cards for all government plans, including Medicare, Medicaid, the VA, and TRICARE. Eligible Medicare Part D members can instead use the new $50 a month Medicare GLP-1 Bridge for Wegovy, Foundayo, or the Zepbound KwikPen starting July 1, 2026, if they meet the BMI and clinical eligibility rules.

Do I need type 2 diabetes to use the Ozempic or Mounjaro savings card?

Yes. Both Ozempic and Mounjaro are FDA-approved for type 2 diabetes, and their manufacturer savings cards require a diabetes prescription that your commercial plan covers. For weight loss, the savings-card-eligible brands are Wegovy, Zepbound, and Foundayo.

Which GLP-1 has the lowest cash price if I am not covered?

Among brand-name options, Foundayo's self-pay starts lowest at about $149 a month through LillyDirect for the 0.8 mg dose. Wegovy's pill also starts at $149 a month through NovoCare. Higher doses of any brand cost more, so confirm the price for your specific dose before filling.

Why did my savings card get rejected at the pharmacy?

Common reasons include: the card expired, you hit a yearly or monthly fill limit, your plan coverage changed, a prior authorization was denied or missing, the pharmacy processed it incorrectly (did not run insurance first), you are on a government plan, or a plan accumulator rule blocked the manufacturer discount from applying. Work through the rejection checklist on this page and ask the pharmacist for the specific rejection code.

Can I use GoodRx and a manufacturer savings card together?

No. Manufacturer savings cards work behind your commercial insurance as a secondary payer. GoodRx and SingleCare are cash-discount coupons that replace insurance for that fill. Compare the two and use whichever gives you the lower price — you cannot stack them on the same prescription.

Do compounded GLP-1s have manufacturer savings cards?

No. Manufacturer savings cards apply only to the FDA-approved brand-name drug from the original maker. Compounded GLP-1 programs are a separate category — they do not have manufacturer savings cards and should not be compared as manufacturer-card products.

I still do not know which GLP-1 path fits me. What now?

Take our free 60-second matching quiz at The RX Index. The right move depends on your insurance type, coverage status, diagnosis, budget, and whether you need a prescriber or prior-authorization help. The quiz routes you to the option that fits your specific situation.

Still not sure which GLP-1 program is right for you?

If you’ve read this far and you’re still not certain whether you’re in the savings-card lane, the self-pay lane, the Medicare lane, or the coverage-appeal lane — that’s okay. The right answer depends on your exact insurance and your prescriber, and a 60-second quiz can sort it faster than another hour of reading.

Find my GLP-1 path →Sources we checked

- Eli Lilly — Zepbound full terms (lilly.com/lillydirect) and Zepbound Savings (zepbound.lilly.com/savings)

- Eli Lilly — Mounjaro Savings & Coverage (mounjaro.lilly.com/savings-coverage)

- Eli Lilly — Foundayo Coverage & Savings (foundayo.lilly.com); FDA approval (accessdata.fda.gov; investor.lilly.com, April 1, 2026)

- Novo Nordisk — NovoCare Wegovy Savings Offer and Diabetes Savings Card (novocare.com)

- CMS — Medicare GLP-1 Bridge, Information for Beneficiaries (cms.gov)

- TrumpRx (trumprx.gov)

- Ro — Weight Loss Pricing and GLP-1 Insurance Coverage Checker (ro.co)

This page is general information, not medical or insurance advice. Talk to a licensed clinician about whether any medication is right for you, and confirm coverage and pricing with your plan and the drugmaker before you fill.

This page was built from drugmaker official savings pages, CMS documentation, and direct review of card terms. Prices and caps are verified as of the date above; they change at year-end when new card programs launch. No manufacturer paid for placement or influenced the comparison order. See how we evaluate providers.

Your situation changes the answer

Find My GLP-1 Path

The right GLP-1 provider isn't the same for everyone. It depends on your state, your insurance and formulary, whether you want an FDA-approved or compounded medication, your preferred route (injection or oral), and your budget. Because a general answer can't resolve those for you, use The RX Index's Find My GLP-1 Path tool to get a personalized provider match with source-verified pricing before you choose.

- What it asks: your state, insurance situation, medication preference, budget, and support needs

- What you get: a personalized shortlist of GLP-1 providers matched to your situation, with verified pricing and the right questions to ask

- Cost: free · about 2 minutes · no signup