GLP-1 Pricing · Zepbound · Cost Intelligence · Verified May 2, 2026

Zepbound Savings Card 2026: Who Pays $25, Who Pays $499 or $299, and What to Do When It’s Not Working

Published: · Last updated:

The Zepbound Savings Card is real, free, and runs through December 31, 2026. The “as low as $25” headline only applies if your commercial insurance covers the Zepbound single-dose pen. If your plan doesn’t cover it, the same Lilly card drops your cost to as low as $499/month for pens, or $299, $399, or $449 for the KwikPen by dose. Medicare, Medicaid, TRICARE, and VA patients can’t use the commercial card. Eligible Medicare Part D beneficiaries may have a separate $50/month Medicare GLP-1 Bridge path starting July 1, 2026 for Zepbound KwikPen only — not pens or vials. Medicaid, TRICARE, VA, and other government-plan patients should check their own plan rules or use a self-pay route.

Here’s the thing most people don’t realize: Lilly’s 2026 Zepbound savings setup has four practical price paths — covered commercial single-dose pen, non-covered commercial single-dose pen, non-covered or cash-pay KwikPen, and LillyDirect Self-Pay Journey for vials or KwikPen. They have different prices, different fill limits, different paperwork, and different rules at the pharmacy counter. The reason your friend pays $25 and you got quoted $700 isn’t that the card is fake — it’s that you two are in different paths. We’ll show you exactly which one applies to you, in about 60 seconds.

Your situation at a glance

| Your situation | Your price with the card |

|---|---|

| ✅ Commercial insurance covers the Zepbound single-dose pen | as little as $25 / fill |

| ⚠️ Commercial insurance, plan doesn’t cover Zepbound | $499 / mo (pen) · $299–$449 (KwikPen) |

| 🚫 Medicare / Medicaid / TRICARE / VA | Commercial card excluded · eligible Medicare Part D users may have a $50/mo Bridge path for KwikPen starting July 1, 2026 · others should check plan/self-pay options |

| 💵 No insurance at all | $299–$449 via KwikPen Self-Pay Card or LillyDirect — 7.5–15 mg can rise to $499 or $699 if the 45-day refill rule is missed |

Current 2026 terms expire 12/31/2026.

Sources verified for this page: Lilly’s full Savings Card terms (CMAT-05333 03/2026); zepbound.lilly.com/savings; zepbound.lilly.com/hcp/coverage-savings; pricinginfo.lilly.com/zepbound; CMS Medicare GLP-1 Bridge guidance; FDA-approved Zepbound prescribing information. All checked May 2, 2026.

🔧 Find My Zepbound Savings Path — Free 60-Second Quiz

Pick your insurance, pick whether your plan covers Zepbound, pick the device you were prescribed. We tell you which Lilly path applies, what you should pay, and what to watch out for.

Take the free 60-second quiz →No signup. Built and verified against Lilly’s 2026 Savings Card terms.

What this page does (and what it doesn’t)

We get the question every week: “I went to CVS, the screen said $700, the pharmacist shrugged, and now I’m reading the Zepbound Savings Card terms at midnight trying to figure out what just happened.”

This page is the answer. We’ll tell you:

- Which of the four price paths applies to your exact insurance and prescription

- What you’ll actually pay this month — with the math, not the marketing

- Exactly what to say at the pharmacy counter when the card fails

- What to do if you’re on Medicare, on Medicaid, or have no insurance at all

- The current 2026 numbers — most ranking pages still publish 2024–2025 caps that no longer apply

What we don’t do: prescribe medication, replace your doctor, or sell you anything. The Zepbound Savings Card itself is free, straight from Lilly. We only mention paid options later in the page, where they actually solve a problem the card doesn’t solve.

⚠️ This page is for cost and access navigation only. Zepbound requires a prescription and has safety warnings, including a boxed warning for thyroid C-cell tumors. Clinical eligibility must be determined by a licensed clinician.

What you actually pay in 2026, by insurance and device

The short version: Lilly’s 2026 Zepbound savings setup has four practical price paths. Three sit under the commercial Savings Card (covered pen, non-covered pen, non-covered KwikPen). The fourth is the LillyDirect Self-Pay Journey Program — same prices as the KwikPen self-pay card, but a different program with different rules. Your situation puts you in exactly one of them.

| Your situation | Lilly program | Lowest price | Device | The catch |

|---|---|---|---|---|

| Commercial insurance covers the single-dose pen | Savings Card — covered tier | as little as $25 / fill | Single-dose pen | Lilly contributes up to $100/month ($200 for a 2-month fill, $300 for a 3-month fill). Annual cap: $1,300. Max 13 fills/year. |

| Commercial insurance does not cover the single-dose pen | Savings Card — non-covered tier | as low as $499 / month | Single-dose pen | Savings = wholesale price minus $499. Max 13 fills/year. |

| Commercial insurance does not cover the KwikPen | KwikPen Savings Card — non-covered tier | $299 / $399 / $449 | KwikPen (single-patient-use) | $299 is 2.5 mg only. $399 is 5 mg. $449 covers 7.5–15 mg. Max 11 fills/year (not 13). $449 on higher doses requires refill within 45 days. |

| No insurance — paying cash | KwikPen Self-Pay Savings Card or LillyDirect Self-Pay Journey | $299 starting | KwikPen or single-dose vials | Same prices as the non-covered KwikPen tier. Refill higher doses within 45 days or the price jumps to $499 (7.5 mg) or $699 (10–15 mg). No insurance prior authorization required. |

| Medicare, Medicaid, TRICARE, VA, IHS, or any government plan | Not eligible for the commercial Savings Card | $299 (LillyDirect self-pay) · $50 / mo Medicare GLP-1 Bridge for eligible Part D (July 1, 2026) | KwikPen or vials | Bridge applies to KwikPen only — not pens or vials. Medicaid, TRICARE, and VA patients are not in the Bridge. |

Sources: Lilly’s Zepbound Single-Dose Pen and Single-Patient-Use KwikPen Savings Card Program full Terms and Conditions (CMAT-05333 03/2026); zepbound.lilly.com/savings; zepbound.lilly.com/hcp/coverage-savings; CMS Medicare GLP-1 Bridge guidance. All checked May 2, 2026.

Activate the official card if you qualify

If your commercial plan covers Zepbound, the $25 tier is the best deal in GLP-1 medicine right now. The card is free, digital, takes about three minutes to set up, and works at most major pharmacies.

Direct link to Lilly. Not an affiliate link. The card is free from the manufacturer.

What changed from 2025 to 2026

The short version: If you used the savings card last year and just got a higher bill in January 2026, you’re not crazy — Lilly tightened the program. The monthly cap shrank, the annual cap shrank, the 2025 card expired on December 31, and you have to re-enroll under the new terms.

- Monthly covered cap: 2025 was $150/month → 2026 is $100/month

- Annual covered cap: 2025 was $1,950 → 2026 is $1,300

- Non-covered pen savings: 2025 was up to $469/fill → 2026 is fixed at $499/month as the lowest price

- KwikPen self-pay program: launched February 23, 2026 — didn’t exist in 2025

- Self-pay vials: 2025 was $349 (2.5 mg) / $499 (other doses) → 2026 unified to $299 / $399 / $449 across vials and KwikPen

- Expiration: 2025 card expired 12/31/2025 → 2026 card expires 12/31/2026, and you must re-enroll

Don’t rely on getting a notice from Lilly — verify current terms on Lilly’s savings page before your next fill.

What we actually verified for this page

The short version: Drug-pricing pages go stale fast. Many of the top results on Bing right now still publish 2024 or 2025 numbers. We re-verified every figure on this page against Lilly’s primary documents in May 2026, and we re-verify quarterly.

Here’s exactly what we checked, with sources you can open and read yourself:

- ✅ Lilly’s full Savings Card Terms and Conditions (document code CMAT-05333 03/2026)

- ✅ Lilly’s consumer Savings Options page at zepbound.lilly.com/savings

- ✅ Lilly’s HCP coverage and savings page at zepbound.lilly.com/hcp/coverage-savings

- ✅ Lilly’s pricing info page at pricinginfo.lilly.com/zepbound (current wholesale list price: $1,086.37/month)

- ✅ Lilly’s Self Pay Journey Program terms at lilly.com/lillydirect

- ✅ Lilly’s Access & Coverage page for prior authorization and appeal resources

- ✅ CMS Medicare GLP-1 Bridge guidance (current as of May 2026)

- ✅ TrumpRx pricing at trumprx.gov for Zepbound vials and KwikPen

- ✅ FDA-approved Zepbound indications: chronic weight management in adults with obesity (BMI ≥30) or overweight (BMI ≥27) with at least one weight-related condition, and moderate-to-severe obstructive sleep apnea (OSA) in adults with obesity. Not type 2 diabetes — that’s Mounjaro.

- ✅ Ro’s published Zepbound pricing and program scope at ro.co/weight-loss/pricing/

Things we’re still watching: CMS has published the Medicare Bridge clinical criteria; we’re still watching for additional operational pharmacy-processing and claims guidance. We’re also tracking BALANCE Model 2027 Part D plan participation and additional state Medicaid policy changes after California removed Zepbound for weight-loss indications on January 1, 2026.

If you spot a number on this page that doesn’t match Lilly’s site today, email us at [email protected] and we’ll fix it within 48 hours.

Who qualifies for the Zepbound Savings Card in 2026?

The short version: You qualify for the $25 covered tier if you have commercial drug insurance that covers the Zepbound single-dose pen, you have a valid prescription for an FDA-approved use, you’re 18 or older, and you live in the US or Puerto Rico. If your plan doesn’t cover Zepbound, separate non-covered tiers drop the price to $499 (pens) or $299–$449 (KwikPen). Government insurance — Medicare, Medicaid, TRICARE, VA, IHS — is excluded from the commercial card.

There are basically four eligibility paths. You’re in exactly one of them.

Path 1 — You have commercial insurance and your plan covers Zepbound

This is the best path. You’ll pay as little as $25 per fill.

The card stacks on top of your insurance. Your pharmacy runs your insurance first, applies your normal copay, then the Savings Card kicks in. For a 1-month covered single-dose pen fill, the card can reduce your post-insurance cost by up to $100, subject to the $25 minimum and the annual cap. If your post-insurance cost is high enough that $100 doesn’t bring it down to $25, you pay what remains. The annual cap is $1,300 in 2026.

The annual cap mainly matters if each fill uses close to the maximum card savings, or if you use 2- or 3-month fills that draw larger savings at once. Once the $1,300 calendar-year savings cap is exhausted, the card no longer reduces remaining fills for that year. If your post-insurance cost is low enough that the card doesn’t use the full monthly savings amount, you may not reach the cap at all.

Path 2 — You have commercial insurance, but your plan doesn’t cover Zepbound

A separate tier of the same Savings Card kicks in. Instead of $25, the card brings your cost down to $499/month for the single-dose pen, or $299 / $399 / $449 for the KwikPen by dose.

This is still way cheaper than paying full list price ($1,086/month). But you have to actually be on a commercial plan that doesn’t cover the drug — having no insurance at all puts you in Path 3, not Path 2.

Path 3 — You have no insurance at all

You can’t use the standard commercial Savings Card. But Lilly runs a separate cash-pay program: the KwikPen Self-Pay Savings Card ($299 / $399 / $449) and the LillyDirect Self-Pay Journey Program (vials or KwikPen, same prices). Both are for cash patients only — you can’t seek reimbursement from any insurance after using them.

The good news: no insurance prior authorization, no insurance fight, no pharmacy back-and-forth. You upload your prescription, you pay, the medication ships. We’ll cover this path in detail later in the page.

Path 4 — You have Medicare, Medicaid, TRICARE, VA, or another government plan

You cannot use the commercial Savings Card. Lilly’s terms exclude government-funded health programs, and the OIG has long warned that manufacturer copay coupons can create anti-kickback exposure when applied to drugs paid by federal healthcare programs.

But you’re not locked out of Zepbound. Lilly’s consumer savings page routes government-plan patients to LillyDirect self-pay starting at $299. And starting July 1, 2026, eligible Medicare Part D beneficiaries can access the Medicare GLP-1 Bridge at a $50/month copay for the KwikPen. We cover the Bridge in detail below.

A quiet disqualifier: Alternate Funding Programs (AFPs)

Some employer health plans use a third-party vendor that tries to enroll high-cost specialty drug patients in manufacturer assistance programs to lower the plan’s costs. Lilly’s terms specifically bar patients in these programs from using the Savings Card.

Here’s the tell: if your employer plan recently routed you to a “patient advocate” or third-party “specialty drug program” offering to “help” you with financial assistance for Zepbound — that’s likely an AFP. The advocate will try to enroll you in the Savings Card and bill the savings back to the plan, and your plan now treats Zepbound as “non-covered” so you have to use Lilly’s program. Lilly’s terms shut this down.

If you suspect you’re in an AFP, call Lilly support at 1-866-923-1953 before your next fill.

Zepbound for OSA vs. obesity: why some plans cover one and not the other

This is one most pages miss. Zepbound is FDA-approved for two separate indications: chronic weight management and moderate-to-severe obstructive sleep apnea (OSA) in adults with obesity. Some commercial plans exclude weight-loss medications from the formulary but still cover Zepbound when it’s prescribed for diagnosed OSA.

If you have documented OSA, this is worth checking. The difference between the $499 non-covered tier and the $25 covered tier is over $5,700/year. Have your prescriber explicitly code the prescription for OSA when that’s the clinical reason.

Need help figuring out which path applies?

If your situation is unusual — partial coverage, mid-PA process, switching plans, kid on your insurance, anything — our free 60-second matching quiz asks five questions and tells you the cheapest legitimate Zepbound path for your exact situation. No signup. No pitch.

How do I check whether my insurance covers Zepbound?

The short version: Call your plan’s pharmacy benefit number — it’s on the back of your insurance card — and ask four specific questions: is Zepbound on the formulary, does it require prior authorization, which device is covered (single-dose pen, KwikPen, or vial), and does the plan use a copay accumulator or alternate funding program. The $25 Savings Card path only works when commercial insurance covers the Zepbound single-dose pen, so confirming coverage is the prerequisite to everything else.

Five minutes on the phone with your plan can save you weeks of pharmacy-counter pain.

Ask if Zepbound is covered for obesity, OSA, or both

Some commercial plans split coverage by indication. They may exclude weight-loss medications entirely but still cover Zepbound for moderate-to-severe obstructive sleep apnea in adults with obesity, since OSA is a separate FDA-approved indication. Ask: “Does my plan cover Zepbound for chronic weight management, for OSA, or both?” If the answer is “OSA only” and you have a diagnosed OSA condition, get your prescriber to code the prescription for OSA.

Ask whether prior authorization (PA) is required

Most plans require prior authorization for Zepbound. PA means your prescriber has to submit paperwork showing you meet the plan’s clinical criteria — usually a BMI threshold, documented prior weight-loss attempts, and qualifying comorbidities. Ask: “Is Zepbound on my plan’s formulary, and does it require PA?” If yes, get the PA criteria in writing from the plan and forward them to your prescriber’s office. The Savings Card cannot help until your PA is processed.

Ask which device is covered: pen, KwikPen, or vial

This is the question almost no one asks, and it’s the reason the savings card sometimes fails on a refill that worked last month. Plans cover specific NDCs (national drug codes), and each Zepbound device has a different NDC. Ask: “Which Zepbound NDC is covered on my formulary — single-dose pen, single-patient-use KwikPen, or single-dose vial?” If your plan covers only the pen and your prescriber sent a KwikPen prescription, you’re paying the wrong price.

Ask whether your plan uses a copay accumulator or alternate funding program

Copay accumulators count manufacturer card savings against you instead of crediting the savings toward your deductible. Alternate funding programs (AFPs) outright block Lilly’s commercial card. Ask: “Does my plan use a copay accumulator, copay maximizer, or specialty-drug alternate funding program for medications like Zepbound?” If yes, the $25 path may be structurally blocked, and your cleanest move is LillyDirect self-pay.

Confirm before you fill

Once you know what your plan does, take 60 seconds and run our checker against your verified answers — it’ll tell you which Lilly path applies and what to expect on the receipt.

Free. No signup. Outputs the exact program, monthly price, and next step for your situation.

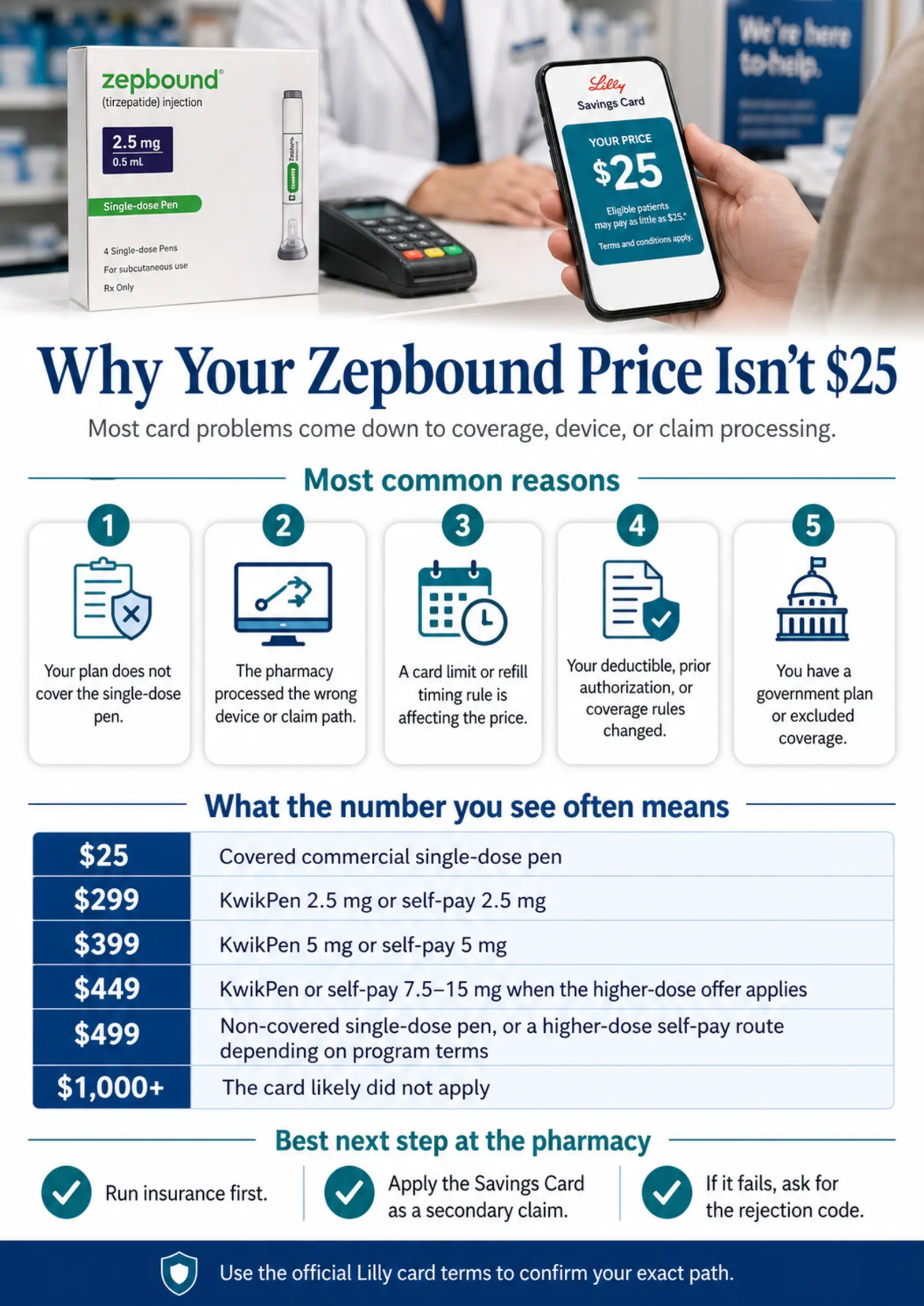

Why didn’t I get the $25 price?

The short version: The $25 price tag fails for one of five reasons in roughly this order: your plan doesn’t actually cover Zepbound; the pharmacy processed the wrong device or claim path; you hit a monthly or annual savings cap; your deductible reset or you’re in the wrong tier; or you’re in an excluded category like Medicare or an AFP. The card isn’t broken — your situation just doesn’t fit the $25 tier.

The most useful thing we can do here is decode whatever number actually showed up on the pharmacy screen. If you saw one of the prices below, here’s what it likely means and what to do next.

What the price you saw probably means

| The number on the screen | What it likely means | What to do next |

|---|---|---|

| $25 | Covered commercial pen path worked. ✅ | Check your remaining annual cap and refill timing. You’re done. |

| $50 | If this is on or after July 1, 2026, it may be the Medicare GLP-1 Bridge for eligible Medicare Part D users filling Zepbound KwikPen. Before July 1, ask the pharmacy what claim path produced the $50. | Confirm the claim path with your pharmacist. |

| ~$299 | KwikPen 2.5 mg or self-pay 2.5 mg path. | Confirm dose. If you were prescribed a higher dose, the price will go up at next fill. |

| ~$399 | KwikPen 5 mg or self-pay 5 mg path. | Confirm dose. |

| ~$449 | KwikPen or Self-Pay Journey 7.5–15 mg with the 45-day refill timing met. | Set a calendar reminder for day 30 after delivery so you don’t miss the window. |

| ~$499 | Either commercial non-covered pen path or a missed-window self-pay 7.5 mg fill. | Confirm whether you’re commercial non-covered (this is your normal price) or self-pay (you missed the 45-day window). |

| ~$650 | Could reflect older non-covered pricing, a card-not-applied scenario, or another pharmacy/coupon path. Don’t assume the 2026 Lilly card applied. | Call Lilly support at 1-866-923-1953 from the counter and ask which program path is being processed. |

| ~$699 | Self-Pay Journey 10–15 mg with missed 45-day refill window. | Refill within 45 days next time to drop back to $449. |

| $1,000+ | Card didn’t apply. Either plan exclusion, government insurance flag, AFP, or you tried to combine the card with another coupon. | Ask the pharmacist for the rejection code. Then call Lilly. |

| “Card rejected” | One of: card not activated, pharmacy ran the card alone instead of as secondary, wrong device path, or excluded plan. | Use the pharmacy script in the next section. |

This decoder is the single most useful thing we publish on this page. Save it, screenshot it, or print it before your next fill.

How much is Zepbound with the Savings Card across a full year?

The short version: Across a 12-month calendar year, Zepbound’s wholesale list price of $1,086.37 per fill equals about $13,036 if you filled once per month at retail. The savings paths don’t all use the same fill count or device, so we compare each path by its own rules instead of pretending every option is the same 12-month retail fill.

Here’s the math that actually matters:

| Path | Fill assumption | Estimated patient total | Comparison note |

|---|---|---|---|

| Covered single-dose pen + $25 card | Up to 13 fills/year | ~$325 if every fill is $25 | Annual savings cap of $1,300 still applies. |

| Non-covered single-dose pen + $499 card | Up to 13 fills/year | ~$6,487 | 13 fills at $1,086.37 retail would be about $14,123, but actual retail pricing can vary by pharmacy. |

| KwikPen 7.5–15 mg + $449 card | Up to 11 fills/year | ~$4,939 | Don’t compare directly to 13 single-dose-pen fills. KwikPen has its own fill cap and regular prices. |

| LillyDirect Self-Pay Journey, 7.5–15 mg | 12 monthly fills | ~$5,388 if every refill qualifies for $449 | Missing the 45-day rule can raise 7.5 mg to $499 and 10–15 mg to $699. |

| Medicare GLP-1 Bridge KwikPen | 12 monthly fills, if eligible | ~$600 | Starts July 1, 2026. Eligible Medicare Part D beneficiaries only. KwikPen only. |

| Retail WAC reference | 12 monthly fills | ~$13,036 at $1,086.37/fill | Use device-specific pricing when comparing self-pay vial/KwikPen paths. |

Two things to flag:

- The KwikPen card is capped at 11 fills/year, not the 13 fills allowed on the single-dose pen card. A “month” for the KwikPen is 28 days and 1 KwikPen (vs. 4 single-dose pens for the pen card). It’s a small detail Lilly buries in the fine print, but it changes your annual math.

- The $1,300 annual cap doesn’t always matter. If your real plan copay is low and the card doesn’t use the full $100 monthly savings each fill, you may never hit the cap.

The 45-day refill rule — and what happens when you miss it

The short version: For LillyDirect’s Self-Pay Journey Program (vials or KwikPen at 7.5 mg and above), you have to refill within 45 days of your last delivery to keep the $449 promotional price. Miss the window and the price jumps to $499 (7.5 mg) or $699 (10–15 mg). For 2.5 and 5 mg, the rule doesn’t apply.

Here’s the dose-by-dose penalty math:

| Dose | Journey price (refill within 45 days) | Regular price (refill after 45 days) |

|---|---|---|

| 2.5 mg | $299 | $299 |

| 5 mg | $399 | $399 |

| 7.5 mg | $449 | $499 ⚠️ |

| 10 mg | $449 | $699 ⚠️ |

| 12.5 mg | $449 | $699 ⚠️ |

| 15 mg | $449 | $699 ⚠️ |

The day your prescription arrives, set a calendar reminder for day 30. That gives you 15 days to actually order the refill before the price jumps. The $250/month difference at the 10–15 mg dose is the catch we see hurt people most often. You can lose $1,500+ a year just by refilling on day 47 instead of day 45.

How to activate the Zepbound Savings Card

The short version: Visit zepbound.lilly.com/savings, attest you meet the eligibility criteria, and you’ll get a digital card with four numbers — Card ID, BIN, PCN, and Group — that the pharmacy needs to process the discount. The whole thing takes about three minutes. You can save the card to Apple Wallet or Google Pay.

If you used the 2025 card, it expired December 31, 2025. You must re-enroll under the 2026 terms. The old card won’t work even if you saved it.

The four-step walkthrough

- Go to zepbound.lilly.com/savings from any phone or computer.

- Confirm you meet the eligibility criteria — commercial insurance, valid Zepbound prescription, 18+, US or Puerto Rico resident, not on a government plan.

- Receive your digital card with four critical numbers:

- Card ID (your unique member number)

- BIN (the bank identification number that routes the claim)

- PCN (processor control number)

- Group (group number — required by some pharmacy systems)

- If prompted, complete activation separately at lillycardactivation.com. Some flows now combine activation into the enrollment step, but if you see a separate activation prompt, do it before you go to the pharmacy.

Save those four numbers somewhere you can pull up at the counter. The pharmacy will need all four. Some pharmacy systems require manual entry, so don’t assume just showing the digital card on your phone is enough.

What you don’t need to provide

You don’t need to upload your insurance card, your prescription, your doctor’s information, or your prior auth paperwork to enroll. You only attest to eligibility — Lilly verifies the rest at the point of sale through the pharmacy claim.

How to use the card at the pharmacy

The short version: Hand the pharmacist both your commercial insurance card and your Zepbound Savings Card. Ask them to run insurance first, then apply the Savings Card as a secondary claim using coordination of benefits (the standard pharmacy term for stacking a secondary payer after primary insurance). The card’s BIN, PCN, and Group numbers tell the pharmacy system how to route the secondary claim.

If the pharmacist looks confused — that’s normal. Manufacturer copay cards are processed as a secondary insurance claim, not as a coupon. Don’t leave the counter. That moment of “let me figure this out” is where most of the $700-fill stories start.

What to say at the counter (copy this)

Use this script, word for word if you want:

“I have commercial insurance and a Lilly manufacturer Savings Card for Zepbound. Please run my insurance first, then apply the Savings Card as a secondary claim using coordination of benefits. Here are the BIN, PCN, and Group numbers from the card. If it rejects, can you please tell me the rejection code and whether the issue is insurance coverage, the device, NDC, refill timing, or card eligibility?”

The “rejection code” line is the most important piece. The rejection code is the fastest way to identify whether the problem is eligibility, insurance coverage, device or NDC, refill timing, or processing.

Lilly support numbers — save these before you go

- Main Lilly support: 1-800-545-5979

- Zepbound-specific Savings Card support: 1-866-923-1953

- Post-transaction reimbursement portal: eversana-ptr.virtualrx.co (for KwikPen Self-Pay claims that should have applied but didn’t)

If the pharmacy is stuck and you’ve tried everything, call Lilly from the counter. They can troubleshoot the specific rejection code while you wait.

Why your Zepbound Savings Card isn’t working at the pharmacy

The short version: The most common reason is the pharmacy ran the card alone instead of as a secondary claim after your insurance. Other frequent causes: the card wasn’t activated, your prescribed device is in a different card tier than the pharmacist entered, your plan uses a copay accumulator or alternate funding program, or you have government insurance on file that’s blocking the commercial card. Each failure has a specific fix.

Before the troubleshooting table, here’s what real Zepbound patients have publicly reported. These are direct quotes from public r/Zepbound threads, shared as anecdotal pharmacy-counter experiences — not as Lilly policy or as medical claims:

“I spent about 2 1/2 hours at CVS today trying to work with the pharmacist in getting my savings card to go through.”

— r/Zepbound, “Savings Card not working” thread, accessed May 2, 2026

“January 24.99 out of pocket — February over 700 out of pocket — March switched to savings card, 499 out of pocket.”

— r/Zepbound, “Savings Card confusion” thread, accessed May 2, 2026

“CVS could apply neither the eVoucher, nor the Lilly Savings Card, so I used the reimbursement process.”

— r/Zepbound, “PSA: Use the official Lilly Zepbound Savings Card” thread, accessed May 2, 2026

What those three reports have in common: the card wasn’t fake. It worked some months and broke in others. The breakage was always at the pharmacy processing layer, the deductible reset, or the device path. Here’s the decoder.

The seven most common pharmacy failures, mapped to fixes

| What’s happening at the counter | Most likely cause | What to try |

|---|---|---|

| “Card not recognized” | Card never got activated | Ask the pharmacist to confirm activation at lillycardactivation.com and re-run. |

| “Can’t process with primary insurance” | Card was run alone instead of as secondary | Ask them to run insurance first, then apply the Savings Card with coordination of benefits using the BIN, PCN, and Group. |

| “BIN not found” or “Group invalid” | Data entry error on the card numbers | Have the pharmacist re-enter all four numbers (Card ID, BIN, PCN, Group) exactly as shown. |

| “Patient not eligible” | Government insurance on file, AFP flagged, or you live in MA/CA with a generic restriction | Confirm you have commercial insurance only. If not the issue, call Lilly at 1-866-923-1953 to troubleshoot. |

| “Plan rejected — manufacturer assistance blocked” | Your plan uses a copay accumulator or AFP | Call your plan and ask if they have a copay accumulator or alternate funding program for specialty drugs. If yes, switch to LillyDirect self-pay. |

| Price is higher than expected (more than $25 when you expected $25) | Monthly $100 cap, annual $1,300 cap exceeded, or your deductible reset | Ask the pharmacist or Lilly support whether monthly or annual savings limits are affecting this fill. |

| Claim denied — prior authorization required | Your insurance hasn’t approved Zepbound yet | The Savings Card only works after insurance processes the claim. Start the PA with your prescriber first. |

What about my specific PBM?

Five pharmacy benefit managers (PBMs — the companies that process drug claims for your insurance plan) handle most U.S. commercial pharmacy claims: CVS Caremark, Express Scripts, OptumRx, Humana Pharmacy, and Anthem/Elevance. Each can process Lilly manufacturer cards differently depending on plan setup, accumulator use, and specialty pharmacy routing.

If your card has been rejected and you’ve ruled out activation issues, ask your plan one specific question:

“Does my plan use a copay accumulator, copay maximizer, or specialty-drug alternate funding program?”

If the answer is yes, the card may be structurally blocked at the plan level — not at the pharmacy counter. Your fastest fix is LillyDirect self-pay, which doesn’t depend on your plan.

One PBM-specific fact worth knowing: starting July 1, 2026, Humana is the CMS central processor for the Medicare GLP-1 Bridge ($50/month for KwikPen). The Bridge BIN is 028918 and the PCN is MEDDGLP1BR — Medicare patients can give those numbers to any participating pharmacy.

When the card is structurally blocked, you have a real next step

If you’ve called the pharmacy, called Lilly, called your plan, and the card still won’t apply — or if your insurance is denying coverage entirely and the appeal feels like a second job — there’s a path that doesn’t involve fighting paperwork.

Ro operates a Zepbound pathway with a dedicated insurance concierge. Ro publicly states that its insurance concierge “fights for coverage and submits all paperwork on your behalf,” including prior authorization paperwork. If coverage isn’t available, Ro’s provider can suggest FDA-approved cash-pay GLP-1 options. Get started for $39, then as low as $74/month with annual plan paid upfront. Ongoing monthly is $149 if you don’t prepay.

Honest tradeoff: Ro is not the cheapest path if you’re a confirmed cash-pay patient who already has a working prescription — for that, LillyDirect self-pay is more direct and doesn’t add a membership fee. Ro earns its keep when insurance is the bottleneck, not when cost is. Ro’s Zepbound path also centers on FDA-approved Zepbound, not compounded tirzepatide — so if compounded is your priority, Ro isn’t your fit. But if your PA has been denied and your prescriber’s office isn’t returning your calls, Ro’s concierge handles the part of the fight that no one else will.

Does the Savings Card work on the pen, KwikPen, or vials?

The short version: The Savings Card covers the single-dose pen and the KwikPen — but with different terms, different fill limits, and different price tiers. Lilly explicitly states the $299 / $399 / $449 pricing applies to the KwikPen, not the single-dose pen. Single-dose vials are accessed only through the LillyDirect Self-Pay Journey Program — that’s a separate program, not the Savings Card. Confusing the device is the number one reason people get quoted the wrong price.

Here’s how the device options break down.

Single-dose pen, commercial insurance covers it

- Price: as little as $25/fill

- Card: standard Savings Card, covered tier

- Fill limit: up to 13 fills/year

- What a “month” means: 28 days and up to 4 single-dose pens

Single-dose pen, commercial insurance does NOT cover it

- Price: as low as $499/month

- Card: Savings Card, non-covered tier

- Fill limit: up to 13 fills/year

KwikPen, commercial insurance does NOT cover it

- Price: $299 (2.5 mg) / $399 (5 mg) / $449 (7.5–15 mg)

- Card: KwikPen Savings Card, non-covered tier

- Fill limit: up to 11 fills/year, not 13

- What a “month” means: 28 days and 1 KwikPen (not 4 devices)

- Catch: $449 pricing for 7.5 mg and above requires refill within 45 days

KwikPen, no insurance, paying cash

- Price: same $299 / $399 / $449 as above

- Card: KwikPen Self-Pay Savings Card

- Fill limit: see Lilly terms — 11 fills/year cap applies

- Catch: cash patients only. You can’t seek reimbursement from any payer afterward, and you cannot apply your out-of-pocket cost toward a deductible or true out-of-pocket requirement. No insurance prior authorization required (a valid prescription still is).

Single-dose vials, self-pay through LillyDirect

- Price: $299 / $399 / $449 through the Self-Pay Journey Program

- Not the Savings Card — this is LillyDirect’s separate cash-pay program

- Catch: same 45-day refill window for the $449 price. Miss it and higher doses jump to $499 (7.5 mg) or $699 (10–15 mg).

LillyDirect vs. Savings Card at retail — which is better?

LillyDirect is Lilly’s direct-to-patient pharmacy. It ships KwikPen or vials to your door at fixed cash prices and doesn’t involve a savings card at all. The Savings Card is what you use at a retail pharmacy (CVS, Walgreens, Kroger, Walmart) alongside your commercial insurance.

They’re different programs with different pricing structures. You can’t use both at once.

If you’re a cash patient with no insurance, LillyDirect is usually the simpler path — no card activation, no pharmacy confusion, no coordination of benefits. The prescription goes straight to LillyDirect and the medication ships to you within a few days. Walmart retail pickup is documented for self-pay Zepbound vials through LillyDirect; KwikPen prescriptions can be sent to LillyDirect Pharmacy or a local pharmacy of choice under applicable terms.

Direct manufacturer link. Not an affiliate link.

Can you use the Savings Card without insurance, with Medicare, or with Medicaid?

The short version: The commercial Savings Card requires commercial insurance. Without insurance, you can use the KwikPen Self-Pay Savings Card ($299–$449) or LillyDirect Self-Pay Journey Program ($299–$449) — same prices, different programs. With Medicare, Medicaid, TRICARE, or VA, the commercial card is excluded under Lilly’s terms, but you have three alternatives plus the new Medicare GLP-1 Bridge ($50/month for eligible Medicare Part D beneficiaries) starting July 1, 2026.

If you’re on Medicare

You have three real paths:

1. LillyDirect Self-Pay Journey Program

- $299 for 2.5 mg, $399 for 5 mg, $449 for 7.5–15 mg

- KwikPen or single-dose vials, your choice

- Must refill within 45 days to keep the higher-dose price

- No insurance prior authorization required (a valid prescription still is)

- Available now

2. TrumpRx

- The federal direct-to-consumer pricing platform at trumprx.gov

- Lists Zepbound vials and KwikPen starting at $299

- No insurance or income requirements

- TrumpRx routes Zepbound orders through LillyDirect for fulfillment

- Pricing tracks LillyDirect’s Self-Pay Journey terms

3. Medicare GLP-1 Bridge (July 1, 2026 – December 31, 2027)

Eligible Medicare Part D beneficiaries get Zepbound KwikPen only (not pens, not vials) at a $50/month copay with no deductible. The $50 copay does not count toward your Part D deductible or out-of-pocket spending cap.

Eligibility requires a prior authorization attesting the drug is prescribed for weight reduction with ongoing lifestyle modification, plus one of these clinical paths:

- BMI ≥ 35, or

- BMI ≥ 30 with heart failure with preserved ejection fraction, uncontrolled hypertension, or chronic kidney disease stage 3a or above, or

- BMI ≥ 27 with prediabetes, previous myocardial infarction, previous stroke, or symptomatic peripheral artery disease.

PA processes through CMS’s central processor (Humana — BIN 028918/PCN MEDDGLP1BR).

Important Bridge carveout: if your Zepbound prescription is for moderate-to-severe OSA with obesity, CMS says that use may be coverable under the basic Medicare Part D benefit and would not be routed through the Bridge. Your plan’s normal formulary, exception, and appeal process applies in that case.

The Bridge runs through December 31, 2027. Watch for BALANCE 2028 announcements during fall 2027 open enrollment (October 15 – December 7, 2027).

For the full Medicare picture, see our Medicare Zepbound coverage guide and our Medicare GLP-1 Bridge program walkthrough.

If you’re on Medicaid

It’s state-dependent and getting tighter. California’s Medi-Cal stopped covering Zepbound for weight-loss indications on January 1, 2026 — though prior authorization for OSA may still be considered. Several other states are reconsidering coverage. Check your state’s current formulary directly.

The CMS BALANCE Model opens to state Medicaid agencies starting May 2026, which may expand access in participating states.

If you’re on TRICARE or VA

Government-funded, so the commercial card doesn’t apply. TRICARE and VA patients are not in the Medicare GLP-1 Bridge either — that program is Medicare Part D only. TRICARE has historically had limited GLP-1 coverage for weight loss; VA coverage varies by facility.

Your cleanest self-pay paths are LillyDirect ($299–$449) or TrumpRx (starting at $299). Most TRICARE and VA patients we hear from end up using LillyDirect direct delivery.

Not sure which non-commercial path applies to you?

Our 60-second matching quiz asks about your insurance, state, and budget, and shows you the cheapest legitimate Zepbound path for your exact situation. No product pitches, just a clear recommendation.

What if your commercial insurance denies Zepbound?

The short version: You have three real options: (1) have your prescriber submit a prior authorization with a letter of medical necessity, (2) use the Savings Card’s non-covered tier at $499/month (pens) or $299–$449 (KwikPen) while you appeal, or (3) switch to LillyDirect self-pay at $299–$449/month if you’d rather stop fighting insurance. The denial is usually about formulary restrictions, not whether you qualify clinically.

Why plans deny Zepbound even when they “cover” it

- Prior authorization — your doctor has to submit paperwork showing you meet the plan’s clinical criteria (BMI thresholds, documented weight-loss attempts, qualifying comorbidities)

- Step therapy — the plan wants you to fail a cheaper alternative first (Wegovy, Saxenda, generic phentermine)

- Quantity limits — you can only fill at certain intervals or amounts

- Indication-based exclusion — some plans cover Zepbound for OSA but not for obesity alone

How to handle a denial

- Get the written denial letter. You need the specific reason — “not covered” isn’t enough. Ask for the plan’s citation in writing.

- Your prescriber submits a prior authorization or appeal. Include a letter of medical necessity documenting BMI, weight history, comorbidities, prior weight-loss attempts, and clinical rationale for Zepbound specifically. Lilly publishes PA and appeal templates at zepbound.lilly.com/access-coverage.

- Check if OSA changes the picture. Zepbound is FDA-approved for moderate-to-severe OSA in adults with obesity. Some plans cover it for OSA when they don’t cover it for obesity alone. If you have diagnosed OSA, make sure it’s documented in the PA.

- Use the card while you wait. While your PA is pending, enroll in the Savings Card anyway. If the PA is approved, you land in the $25 tier. If it’s denied, you’re at $499/month (pens) or $299–$449 (KwikPen). Either way, the card beats paying list price.

When to stop fighting insurance and switch to self-pay

Be honest with yourself about the tradeoff. If your plan is actively blocking Zepbound through an alternate funding program, if you’ve already appealed once and lost, or if the documentation bar is higher than you can clear — LillyDirect self-pay at $299–$449/month is often the cleaner answer. The monthly math is similar to the $499 non-covered tier, you skip the paperwork entirely, and no insurance prior authorization is required.

For more detail, see our guides on appealing a Zepbound denial and the cheapest Zepbound paths without insurance.

When the appeals fight is the actual bottleneck

If your prescriber doesn’t handle PAs well — or you don’t have a prescriber yet and you’d rather not start from scratch — Ro operates a Zepbound pathway specifically built to handle the insurance fight on your behalf. Ro publicly states its insurance concierge “fights for coverage and submits all paperwork on your behalf.” Get started for $39, then as low as $74/month with annual plan paid upfront.

If insurance coverage isn’t available, Ro’s provider can suggest FDA-approved cash-pay GLP-1 options at LillyDirect-equivalent pricing. Compare the final medication price and fulfillment route against LillyDirect before you start so you know what you’re getting.

Savings Card vs. LillyDirect vs. TrumpRx vs. GoodRx vs. Medicare Bridge: which is cheapest?

The short version: If you have commercial coverage for Zepbound, the Savings Card (as low as $25) wins by a wide margin. If your plan doesn’t cover it, the non-covered card tier ($499 pens/$299–$449 KwikPen) is usually cheapest. For cash and government-insurance patients, LillyDirect ($299–$449) and TrumpRx (starting at $299) are the cleanest paths. GoodRx at retail Costco currently runs around $995 — only use it if nothing else is available. The Medicare GLP-1 Bridge at $50/month wins for eligible Medicare Part D beneficiaries, hands down.

| Access path | Typical monthly price | Who wins with it | The fine print |

|---|---|---|---|

| Savings Card + commercial coverage | as low as $25/fill | Commercially insured with Zepbound coverage | $100/month cap, $1,300/year cap, 13 fills max |

| Savings Card — non-covered (pens) | as low as $499/month | Commercial insurance, plan denies Zepbound | 13 fills/year |

| KwikPen card — non-covered | $299/$399/$449 | Commercial insurance, plan denies, filled as KwikPen | 11 fills/year. Higher-dose refill within 45 days. |

| KwikPen Self-Pay Savings Card | $299/$399/$449 | Uninsured cash-pay patients | Can’t seek reimbursement from any payer. Available at participating retail pharmacies including Kroger. |

| LillyDirect Self-Pay Journey Program | $299/$399/$449 | Cash-pay or government-insurance patients wanting home delivery | Must refill within 45 days for $449 higher-dose price. No insurance PA. |

| TrumpRx | starting at $299 | Anyone — no insurance or income requirements | Routes through LillyDirect for Zepbound fulfillment. |

| Medicare GLP-1 Bridge (Jul 2026 – Dec 2027) | $50/month copay | Eligible Medicare Part D beneficiaries meeting BMI/comorbidity criteria | KwikPen only — not pens or vials. PA through CMS processor. |

| Ro Body + Zepbound | $39 first month, then $74–$149/mo membership + medication cost | Anyone needing PA paperwork support | Insurance concierge handles paperwork. Medication billed separately. |

| GoodRx at retail (Costco) | ~$995/month | Last resort only | Most expensive legitimate option. (GoodRx, accessed May 2, 2026) |

Sesame Care also offers Zepbound through provider-choice booking with Costco-member-style pricing. If you specifically want to pick your prescriber, that’s an alternative to consider. For most readers landing on this page, Ro’s insurance concierge is the better fit because the most common reason the $25 tier never activates is a denied or unfiled prior authorization, and that’s exactly what Ro’s concierge handles.

Why your first fill of 2026 cost more than expected

The short version: If you used the card in 2025 and just got a higher bill in January 2026, three things probably happened: your plan deductible reset on January 1, Lilly’s 2026 monthly cap dropped from $150 to $100, or your employer switched PBMs at renewal and the new PBM doesn’t process manufacturer cards as smoothly.

Your deductible reset on January 1. Most commercial plans restart the annual deductible every year, so early-year fills can be priced as if you have no insurance until you meet the deductible. The Savings Card still applies, but if your plan deductible is high (say, $3,000), your “copay” before the card kicks in is the full negotiated drug price. Once the deductible is met, you drop back to your normal copay.

Lilly’s 2026 terms changed. The covered-tier monthly cap dropped from $150 to $100. If your real plan copay is between $100 and $200, your out-of-pocket went up — even though “the card still works.” The annual cap also shrank from $1,950 to $1,300, so you’ll hit it earlier in the year.

Your employer switched PBMs at renewal. Some PBMs block manufacturer cards through copay accumulators or alternate funding programs. If your benefits changed at the start of the year — even if you didn’t notice — that’s often the real culprit.

The fix: run your first fill, confirm the actual price, call Lilly support if it’s unexpectedly high, and if the issue is structural (AFP, accumulator, formulary change), price out LillyDirect self-pay as your fallback before next month’s fill.

Pages still getting the Zepbound Savings Card wrong in 2026

We audited the top results for “zepbound savings card” in May 2026. Several high-traffic pages still publish 2024–2025 numbers, and one cites the wrong FDA indication. Here’s what’s stale, with verification dates so you can spot-check.

- SingleCare publishes a $1,950/year annual cap and claims non-covered patients save up to $469/fill. Lilly’s 2026 covered-tier annual cap is $1,300, and Lilly now separates the $499 single-dose pen lane from the $299+ KwikPen lane — they’re not the same program. Verified May 2, 2026.

- Drugs.com (last major update March 2025) still shows older savings amounts and states that Zepbound’s FDA-approved indication is “type 2 diabetes in adults.” That’s factually wrong — type 2 diabetes is Mounjaro’s indication. Zepbound is FDA-approved for chronic weight management and moderate-to-severe OSA in adults with obesity. Verified May 2, 2026.

- PrescriberPoint still shows the $1,950 annual maximum and an expiration of 12/31/2025. The current program runs through 12/31/2026 with a $1,300 cap. Verified May 2, 2026.

- Doctronic cites older “$550 to $650” self-pay framing. The current self-pay structure is $299/$399/$449 by dose under LillyDirect’s Self-Pay Journey Program. Verified May 2, 2026.

- Ro’s own Zepbound coupon page (sponsored affiliate link, opens in a new tab) cites the older “$25 or $650” framing. The 2026 card uses different non-covered tiers ($499 pens, $299–$449 KwikPen). Verified May 2, 2026.

If you’ve been pricing Zepbound off any of those pages, that’s probably why your pharmacy number didn’t match what the article promised. Drug-pricing pages go stale fast — it’s the nature of this space. We re-verify our own page quarterly. The next refresh date is published in the byline at the top.

Frequently asked questions about the Zepbound Savings Card

What is the Zepbound Savings Card?

The Zepbound Savings Card is Eli Lilly's official manufacturer copay assistance program for FDA-approved Zepbound (tirzepatide). It's free, digital, and acts as a secondary payer at the pharmacy after your commercial insurance. It is not insurance. The current card runs through December 31, 2026.

Is the Zepbound coupon the same as the Savings Card?

Yes. "Zepbound coupon," "Zepbound copay card," "Zepbound manufacturer coupon," "Zepbound discount card," and "Eli Lilly Zepbound savings" all refer to the same Lilly program. Third-party discount sites like GoodRx and SingleCare run their own separate coupons that are not the Lilly card.

How much does Zepbound cost with the Savings Card?

As little as $25/fill if your commercial insurance covers the single-dose pen. As low as $499/month for pens if your plan doesn't cover it. $299/$399/$449 for KwikPen by dose if not covered. The annual cap of $1,300 applies to the covered single-dose pen tier.

Can I use the Zepbound Savings Card without insurance?

Not the standard commercial card. But Lilly has a separate KwikPen Self-Pay Savings Card ($299/$399/$449) and the LillyDirect Self-Pay Journey Program (vials or KwikPen, same prices) for cash-pay patients.

Can I use the Zepbound Savings Card with Medicare?

No — Lilly's terms exclude government-funded health programs. But eligible Medicare Part D beneficiaries can access the new Medicare GLP-1 Bridge at $50/month for the KwikPen starting July 1, 2026. Medicare patients can also use LillyDirect self-pay ($299–$449) or TrumpRx (starting at $299) today.

Does the Zepbound Savings Card work on vials?

No. The Savings Card covers single-dose pens and the KwikPen. Single-dose vials are accessed through the LillyDirect Self-Pay Journey Program at $299–$449/month — that's a separate program with different terms.

Why didn't I get the $25 price?

The most common reasons: your insurance doesn't actually cover Zepbound (you fall into the $499 pen tier or $299–$449 KwikPen tier), the pharmacy processed the card alone instead of as a secondary claim, you hit the monthly $100 or annual $1,300 cap, your deductible reset, or your plan uses a copay accumulator. Call Lilly at 1-866-923-1953 from the counter for real-time troubleshooting.

Why is my Zepbound Savings Card not working at CVS or Walgreens?

Usually a processing issue. Ask the pharmacist to run insurance first, then apply the card as a secondary claim with coordination of benefits using the BIN, PCN, and Group numbers from your card. If it still fails, Lilly's post-transaction reimbursement portal lets you pay the pharmacy price, keep the receipt, and submit for reimbursement at eversana-ptr.virtualrx.co.

Can I refill after 45 days and keep the same price?

Only on the 2.5 mg and 5 mg doses, which don't have the 45-day rule. For 7.5 mg and above on the Self-Pay Journey Program, missing the 45-day window jumps the price to $499 (7.5 mg) or $699 (10–15 mg). Set a phone reminder for day 30 after delivery so you have a 15-day buffer.

Can I combine the Savings Card with GoodRx or SingleCare?

No. Lilly's terms specifically state the Savings Card cannot be combined with another program, discount card, coupon, or incentive involving Zepbound. Use one or the other. The Lilly card almost always saves more if you have commercial insurance.

Can I use HSA or FSA funds to pay for Zepbound?

It depends on which Lilly program you're using. For the commercial Savings Card, Lilly says you may not seek reimbursement from an HSA, FSA, health insurance, or other reimbursement account for the savings amount Lilly contributed. You may still be able to use HSA/FSA funds for the portion you personally owe — check with your account administrator. For the KwikPen Self-Pay Savings Card, the terms are stricter: you agree not to seek or accept reimbursement for any out-of-pocket costs from any third-party payer.

Does the Zepbound Savings Card work with the OSA indication?

Yes, when prescribed for an FDA-approved use consistent with Lilly's labeling. Zepbound is FDA-approved for both chronic weight management and moderate-to-severe OSA in adults with obesity, and the Savings Card applies to both. Some commercial plans cover Zepbound for OSA when they don't cover it for weight loss alone, so if you have documented OSA, make sure your prescription is coded for it.

How is the Zepbound Savings Card different from LillyDirect?

The Savings Card is used at retail pharmacies (CVS, Walgreens, Kroger, Walmart) alongside your commercial insurance — it's a copay reduction that runs through your plan. LillyDirect is Lilly's direct-to-patient pharmacy that ships medication to your door at fixed cash prices regardless of insurance. Different programs, different pricing structures. You can't use both at once.

How do I appeal a Zepbound coverage denial?

Ask your prescriber to submit a prior authorization with a letter of medical necessity documenting your BMI, weight history, comorbidities, and prior weight-loss attempts. Lilly publishes appeal templates and PA support resources at zepbound.lilly.com/access-coverage. For a step-by-step walkthrough, see our Zepbound denial appeal guide.

Does the Savings Card expire?

Yes — December 31, 2026. Lilly has historically renewed the program annually, but check Lilly's 2027 terms before assuming a new card or reset.

Still not sure which Zepbound program is right for you?

The four-program decision matrix above should answer most situations cleanly. But if your insurance is unusual, you’re cross-shopping insurance, LillyDirect, self-pay, or provider-support paths, you’re switching from Wegovy or Mounjaro, or you want one personalized recommendation instead of four options — our 60-second quiz asks about your insurance, state, dose, and budget and shows you the cheapest legitimate Zepbound path for your exact situation.

Free. No signup. No product pitch. Just a clear recommendation.

About this page

The RX Index is a pricing intelligence and comparison resource for GLP-1 telehealth providers. We re-verify this page quarterly against Eli Lilly’s official savings terms, pricing pages, access and coverage resources, and CMS program updates. If you spot a number that doesn’t match Lilly’s site today, email us at [email protected] — we fix it within 48 hours.

Last verified: .

Next scheduled review: August 2026.

Affiliate disclosure

The RX Index may earn a commission when readers begin care with providers we recommend (currently Ro). The free Lilly Savings Card, LillyDirect, and TrumpRx links on this page are not affiliate links. Commissions never influence our editorial rankings — our recommendations are based on verified program fit and accuracy, not payout. See our full affiliate disclosure.

Medical disclaimer

Information on this page is for cost and access navigation. It is not medical advice, diagnosis, or treatment. Zepbound requires a prescription, and clinical eligibility must be determined by a licensed healthcare provider. Zepbound has a boxed warning for thyroid C-cell tumors and is not for use in patients with a personal or family history of medullary thyroid carcinoma (MTC) or Multiple Endocrine Neoplasia syndrome type 2 (MEN 2). See full prescribing information at zepbound.lilly.com.

Zepbound® is a registered trademark of Eli Lilly and Company. Mention of any provider on this page does not imply endorsement by or affiliation with Eli Lilly.

The RX Index is a pricing intelligence and comparison resource for GLP-1 telehealth providers. This page is educational and is not medical advice. Talk to a licensed clinician before starting, stopping, or changing any medication.

Last verified: .

Related guides from The RX Index

- Does Medicare cover Zepbound? Full 2026 guide

- How to appeal a Zepbound insurance denial

- Cheapest Zepbound without insurance (2026)

- How to switch from compounded tirzepatide to Zepbound

- Zepbound providers that take HSA or FSA

- How the Medicare GLP-1 Bridge works (July 2026)

- How to check if GLP-1 is covered by insurance

Your situation changes the answer

Find My GLP-1 Path

The right GLP-1 provider isn't the same for everyone. It depends on your state, your insurance and formulary, whether you want an FDA-approved or compounded medication, your preferred route (injection or oral), and your budget. Because a general answer can't resolve those for you, use The RX Index's Find My GLP-1 Path tool to get a personalized provider match with source-verified pricing before you choose.

- What it asks: your state, insurance situation, medication preference, budget, and support needs

- What you get: a personalized shortlist of GLP-1 providers matched to your situation, with verified pricing and the right questions to ask

- Cost: free · about 2 minutes · no signup