Check Zepbound coverage — free

Personalized report, no commitment.

Does Insurance Cover Zepbound for Prediabetes?

Last verified:

Published: · Last reviewed:

Affiliate disclosure: The RX Index may earn a commission if you use some of the provider links on this page. It costs you nothing extra, and it never changes our answer. We recommend based on what fits your situation — not on who pays us.

Does insurance cover Zepbound for prediabetes? Usually no — not for prediabetes by itself. Here's the part most pages skip: prediabetes is not a condition Zepbound is approved to treat. So a request that just says “Zepbound for prediabetes” almost always gets denied. But there's a main path that does work — Zepbound for weight management — and your prediabetes can actually help you on it. If your BMI is 30 or higher, or 27 or higher with a qualifying health problem like prediabetes, the weight-management door may be open. And starting July 1, 2026, the Medicare GLP-1 Bridge will cover the Zepbound KwikPen for $50 a month, with prediabetes at a BMI of 27+ as a qualifying path. Whether you have commercial insurance, Medicare, Medicaid, or no coverage at all, this guide tells you which door is yours.

Quick verdict: when prediabetes helps your Zepbound coverage

| Your situation | Does prediabetes help? | What to do next |

|---|---|---|

| Commercial plan that covers weight-loss drugs | Yes — as supporting proof, not the main reason | Check the prior authorization rules before your doctor submits |

| Commercial plan that excludes weight-loss drugs | Usually no | Check the sleep apnea path, an employer exception, or cash-pay |

| Regular Medicare Part D (for weight loss) | Usually no | Look at the Medicare GLP-1 Bridge or the sleep apnea path |

| Medicare GLP-1 Bridge (starts July 1, 2026) | Yes, if your BMI is 27+ and you meet the rules | Ask your prescriber about the Bridge after July 1, 2026 |

| Medicaid | Depends on your state | Check your state's drug list and obesity-med rules |

| No coverage at all | Not the issue — you skip insurance | Compare FDA-approved cash-pay options |

Most people land in one of these six rows. We'll go through each one in plain English, with the real numbers and the exact words that get a “yes” instead of a “no.”

Check how your plan covers Zepbound — free, in minutes

Ro's free GLP-1 Insurance Coverage Checker gives you a personalized report on your plan's GLP-1 coverage — including whether prior authorization is required and any copay or cost estimates. New accounts also get a $50 credit toward getting started.

Check how your plan covers Zepbound, free →(Sponsored.) Coverage isn't guaranteed.

“I'm prediabetic, not diabetic” — and that feels like a wall

If a pharmacy or your insurer told you that you need a diabetes diagnosis before they'll pay for Zepbound, you're not imagining it, and you're not alone. This is the single most common wall people hit.

The pattern shows up again and again. Someone is told they have prediabetes. Their doctor brings up Zepbound. They feel hopeful — maybe this is the thing that stops them from becoming diabetic. Then the prior authorization comes back denied, or they read a benefits document that says “weight-loss drugs are not covered,” and the wind goes out of them. The unfair part stings the most: Do I really have to wait until I'm actually sick before my insurance cares?

Here's the honest answer, and the hope inside it. Plenty of denials aren't really about prediabetes at all — they're about a request built on the wrong foundation. Once you understand the difference between prediabetes as a diagnosis, prediabetes as a weight-related condition, and prediabetes as your specific plan's rule, the paths that were invisible become visible. That's what this guide does.

Does insurance cover Zepbound for prediabetes? The full answer

Usually not for prediabetes alone. Insurance can cover Zepbound when prediabetes is part of a covered pathway — chronic weight management, the Medicare GLP-1 Bridge, certain state Medicaid rules, or a separate covered diagnosis like sleep apnea with obesity. A request written only as “Zepbound for prediabetes” is weak, because prediabetes is not the FDA-approved use. The same request written as “Zepbound for weight management, with prediabetes documented as a weight-related condition” is built on the right foundation.

The simple rule to remember

Prediabetes can support your Zepbound request. It usually does not replace your plan's main coverage requirement.

Think of it like a college application. Prediabetes is a good extra on your file. But the school still has its own admissions rule — the BMI threshold and the covered use. Prediabetes helps you clear that bar. It doesn't remove the bar.

The three things that actually decide it

- Does your plan cover Zepbound for weight management at all? Many do. Many don't. Some plans flatly exclude every weight-loss medication, no matter your diagnosis. This is the first thing to find out, because it changes everything else.

- Do you meet the weight criteria? Zepbound's approved use is a BMI of 30 or higher, or 27 or higher with a qualifying weight-related condition. Your BMI is the number the plan checks first.

- Can your doctor document the right path? Coverage often comes down to paperwork quality — the right use, the BMI, the lab proof — not just the drug name. A clean first submission beats a messy one you have to fix later.

Your coverage path matrix

Built so you don't have to open ten tabs and make your own spreadsheet. Pulls together the FDA's approved use, the Medicare GLP-1 Bridge rules, one real Medicaid example, commercial-plan logic, and the cash-pay fallback.

| Coverage path | Does prediabetes alone get it covered? | What actually matters | Proof to gather | Best next step |

|---|---|---|---|---|

| Commercial plan that covers obesity meds | Usually no by itself, but it helps | Zepbound must be covered for weight management; most look for BMI ≥30, or ≥27 with a qualifying condition | Current BMI, starting BMI, A1C or glucose labs, weight history, the plan's PA form | Confirm the formulary and PA rules before submitting |

| Commercial plan that excludes weight-loss drugs | Usually no | A hard exclusion can block coverage even with obesity or prediabetes | The benefit document showing whether obesity meds are excluded | Ask HR/benefits if it's excluded or just PA-restricted |

| Regular Medicare Part D | No, for weight management | A sleep apnea prescription may be handled differently | Diagnosis, indication, your plan's rules | Check whether your script is for sleep apnea, the Bridge, or cash-pay |

| Medicare GLP-1 Bridge | Yes, if Bridge criteria are met | Starts July 1, 2026; covers the Zepbound KwikPen; BMI ≥27 with prediabetes can qualify | Part D enrollment, BMI at start of GLP-1 therapy, prediabetes proof, Bridge PA through the Bridge central processor | Use the Bridge pathway, not regular Part D |

| Medicaid | State-specific | Some states name prediabetes in their rules; many limit obesity coverage | State Medicaid drug list, managed-care formulary, BMI, A1C | Check your state's drug list and PA form |

| Cash-pay (FDA-approved) | Insurance not required | Dose, channel, savings-card eligibility, and any membership fee drive the price | Dose, pharmacy channel, provider fee, savings-card eligibility | Compare Ro, Sesame Care, or LillyDirect |

Sources: FDA Zepbound prescribing information; CMS Medicare GLP-1 Bridge; current MassHealth Drug List; KFF Medicaid GLP-1 tracking; Eli Lilly pricing pages; Ro and Sesame Care pages. Verified June 11, 2026.

Not sure which row is yours?

Answer a few quick questions — your insurance type, your BMI, your A1C, whether you have sleep apnea, and any past denial reason — and we'll point you to the path that fits.

Start the free Coverage Path Checker →Is Zepbound even approved for prediabetes? (No — here's what that means)

No. Zepbound is not FDA-approved to treat prediabetes. Its approved uses are chronic weight management in adults with obesity (or overweight with a weight-related condition) and moderate-to-severe obstructive sleep apnea in adults with obesity. Insurance coverage usually follows the FDA-approved use, which is why “prediabetes” alone is a weak reason and “weight management” is the strong one.

The FDA label reality

Here's exactly what the FDA approved, in plain terms, straight from the Zepbound label:

- Chronic weight management, used with a reduced-calorie diet and more activity, for adults with a BMI of 30 or higher, or 27 or higher with at least one weight-related condition. The label names examples like high blood pressure, high cholesterol, type 2 diabetes, sleep apnea, and heart disease.

- Moderate-to-severe obstructive sleep apnea (OSA) in adults with obesity.

Notice what's not on that list: prediabetes. The big trial that earned Zepbound its weight-loss approval even left out people who already had type 2 diabetes. So when a plan reviews “Zepbound for prediabetes,” it doesn't match the label, and it gets treated as off-label — which insurers rarely pay for.

| Product | Current FDA-approved use | Approved for prediabetes? |

|---|---|---|

| Zepbound | Chronic weight management; moderate-to-severe sleep apnea in adults with obesity | No |

| Mounjaro | Type 2 diabetes (blood sugar control) | No |

Which name should you ask about: Zepbound, Mounjaro, or Foundayo?

This trips people up, and getting it wrong can trigger an instant denial. Zepbound and Mounjaro contain the same active drug — tirzepatide, made by Eli Lilly — but they're different FDA-approved brands with different approved uses:

- Zepbound is approved for weight management and sleep apnea.

- Mounjaro is approved for type 2 diabetes.

- Foundayo is the brand name for the oral form of tirzepatide, approved for weight management.

Here's the rule. For Zepbound's weight-management path, you usually do not need a type 2 diabetes diagnosis — but you do need to meet the BMI and plan rules. For a diabetes-labeled drug like Mounjaro, most plans do want a type 2 diabetes diagnosis. If your request got routed through “diabetes drug” logic, that may be why you were told “no diabetes, no coverage.” The fix isn't to chase a diagnosis you don't have. It's to make sure the request is built as Zepbound for weight management.

This page is about FDA-approved Zepbound. Compounded tirzepatide is a different product made by a pharmacy and is not the same as FDA-approved Zepbound. We don't treat it as an insurance-covered substitute.

But does Zepbound actually work for prediabetes? (What the research shows)

In adults who have both excess weight and prediabetes, the active drug in Zepbound sharply cut the odds of progressing to type 2 diabetes in a major trial. The catch for coverage: those people also had obesity or overweight, and Zepbound still isn't FDA-approved to treat prediabetes — so the science is real, but it isn't a coverage ticket on its own.

| SURMOUNT-1 fact | Verified detail |

|---|---|

| Original trial enrollment | 2,539 adults with obesity or overweight |

| 176-week prediabetes analysis | The 1,032 participants who had both excess weight and prediabetes |

| New type 2 diabetes at 176 weeks | 1.3% on tirzepatide vs. 13.3% on placebo |

| Risk reduction | About 94% lower risk of progressing to type 2 diabetes |

| What it means for coverage | Strong science — but not a standalone FDA-approved prediabetes use |

Source: New England Journal of Medicine, SURMOUNT-1 three-year results. Verified June 11, 2026.

That's a striking result, and it's probably why your doctor brought it up. But read the fine print with us: every one of those participants also had obesity or overweight. They're exactly the people who could qualify under Zepbound's weight-management approval. The benefit is genuine. It just doesn't change the fact that “prediabetes” isn't an approved use, and your insurer makes its decision on the approved use, not the research headline.

When does prediabetes actually help your prior authorization?

Prediabetes helps most when your plan already covers Zepbound for weight management and asks for a BMI of 27+ plus a qualifying condition. It helps least — or not at all — when your plan has a hard exclusion for weight-loss drugs. The job is to match your prediabetes to a covered pathway, not to lead with it.

Prior authorization (PA) is just the approval step where your plan checks that a drug is medically necessary and covered before the pharmacy can fill it. Your doctor's office submits it. You don't.

BMI 30 vs. BMI 27-plus-a-condition

- BMI 30 or higher: Many plans treat obesity by itself as enough for the weight-management path.

- BMI 27 to 29.9: Plans usually want a documented weight-related condition on top of the BMI — and prediabetes can be one of the conditions some plans accept.

- BMI under 27: Coverage gets very hard unless another approved use applies (like sleep apnea).

This is the most important place prediabetes does work for you: if your BMI is in that 27-to-29.9 “overweight plus a condition” range, prediabetes can be the documented condition that gets you over the line — if your plan accepts it.

Prediabetes means lab proof, not “my doctor mentioned it”

Plans want numbers. Make sure your doctor attaches the actual lab result and date. Here are the standard ranges, from the CDC and the American Diabetes Association:

| Test | Prediabetes range |

|---|---|

| A1C | 5.7% to 6.4% |

| Fasting plasma glucose | 100 to 125 mg/dL |

| 2-hour oral glucose tolerance test | 140 to 199 mg/dL |

Source: CDC prediabetes ranges. If your A1C is 5.9%, that's the proof — not a sentence in a visit note saying “patient is prediabetic.”

A real example: how MassHealth handles it (and a big change coming)

MassHealth (Massachusetts Medicaid) does list prediabetes as a qualifying condition for a weight-loss medication at a BMI of 27 or higher — defined as an A1c of 5.7% or higher and below 6.5%. But there's a catch: prediabetes counts only if you're “not a candidate for an anti-diabetic GLP-1.” In plain terms, if your prediabetes makes you a fit for a diabetes-type GLP-1, MassHealth points you toward that instead of Zepbound.

And here's the plan-specific part most coverage pages skip: MassHealth is changing these rules on July 1, 2026. Statewide, it's adding Wegovy as a preferred drug alongside Zepbound, dropping the old “try phentermine first” step, and — for members with diabetes or prediabetes — steering them toward a diabetes-type GLP-1 for continued coverage. Some MassHealth managed-care plans are going further: Tufts Health Together, for example, will stop covering Zepbound and Wegovy for obesity or overweight entirely on that date.

The lesson: whether prediabetes counts, and which drug you end up on, depends on your exact plan and the exact month — because these rules shift constantly. Don't assume. Check.

The honest part most pages bury

Let's say the thing nobody selling you a subscription wants to say first: prediabetes by itself is a weak insurance argument, and if your plan completely excludes weight-loss drugs, a prediabetes diagnosis won't fix that. If your BMI is under 27 with no other qualifying condition, or your benefits document has a hard “no weight-loss meds” exclusion, no checker, no appeal, and no telehealth service can create coverage that your plan simply doesn't offer. If that's you, the most useful move is to start with lifestyle change and possibly metformin through your own doctor — and to use our checker so we can point you to the option that actually fits.

But — and this is the real hope — if your plan does cover Zepbound for weight management, prediabetes becomes valuable documentation, especially in that BMI 27-to-29.9 range. The thing standing between you and a “yes” usually isn't your diagnosis. It's the prior authorization maze: the right use, the BMI proof, the lab proof, and sometimes proof you tried other steps first. That maze is solvable.

If you qualify on weight, don't fight the paperwork alone

Ro can verify your benefits and have its insurance concierge submit the prior authorization — for the Zepbound pen, Wegovy pen, or Ozempic — and handle the back-and-forth if it's denied. Ro Body is $39 for the first month, then $149/month, or as low as $74/month with the annual plan paid upfront. The membership fee is on top of your medication cost. But that fee buys an insurance concierge whose whole job is to fight for your coverage, and if your plan covers GLP-1s, that can be the difference between a $25 copay and a $1,000 bill.

See if you qualify — let Ro handle the prior authorization →(Sponsored.) Coverage isn't guaranteed.

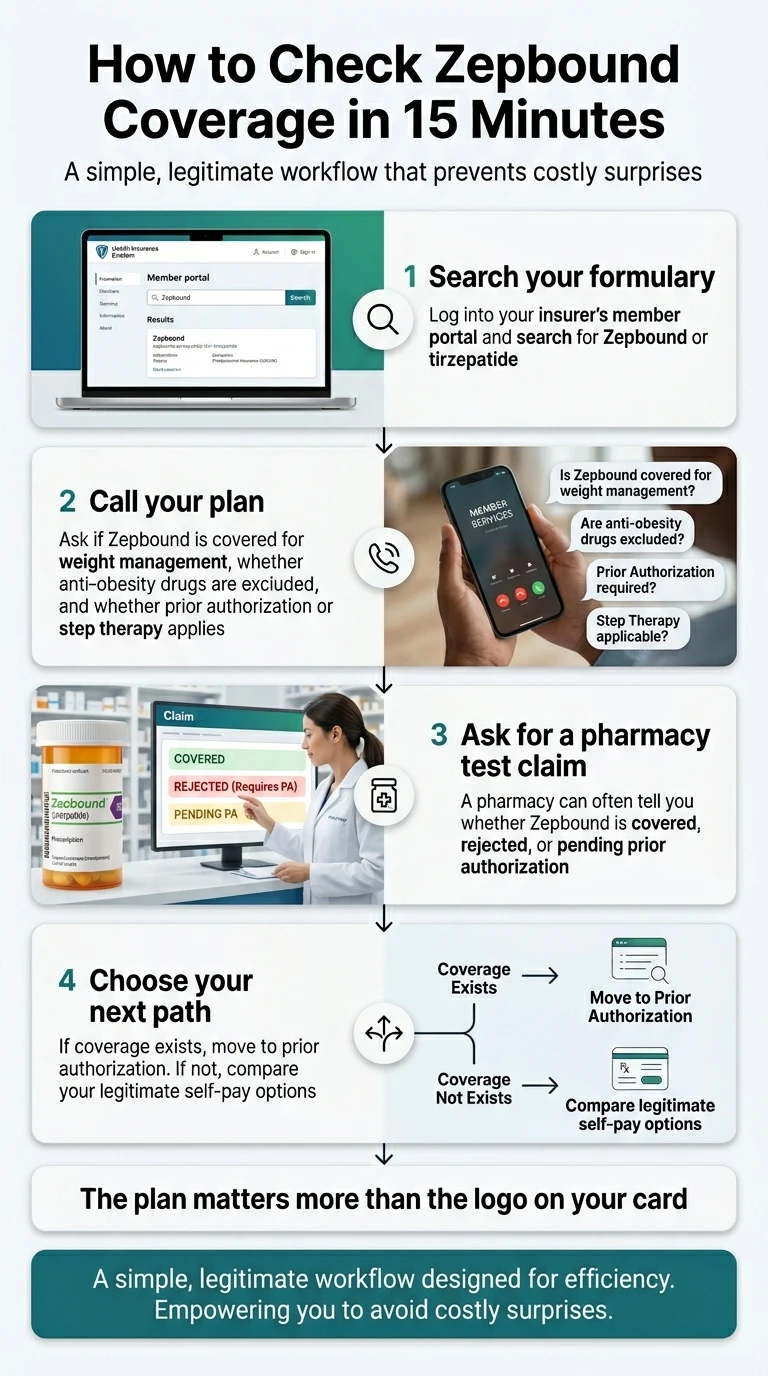

The fastest way to check if your plan covers Zepbound

The fastest path is to check your formulary and PA rules before the prescription goes in. A denied PA can sometimes be fixed, but a clean first submission almost always beats repairing a vague one later. You can call your insurer with the right questions, or use a free tool that does the checking for you.

A formulary is just your plan's list of covered drugs. If Zepbound isn't on it, that tells you a lot before you spend a dime on a visit.

Copy this and call the number on your insurance card

Ask these, in order:

- Is Zepbound on my formulary?

- Is it covered for chronic weight management?

- Is it excluded as a weight-loss medication under my employer or plan benefit?

- Does it require prior authorization?

- What BMI threshold do you require?

- Does prediabetes count as a qualifying weight-related condition?

- Do you require proof of a lifestyle or weight-management program first?

- Is Zepbound covered differently for sleep apnea than for weight loss?

- Which form is covered — KwikPen, single pen, or vial?

- What denial reason should my doctor be careful to avoid?

Write down the answers. They tell you whether your battle is winnable and how to win it.

When Ro is the cleanest shortcut

If you'd rather not sit on hold and decode insurance-speak, this is where a coverage checker earns its place. Ro's GLP-1 Insurance Coverage Checker is free, checks your specific plan, and gives you a personalized report on how your plan covers GLP-1 medications like Zepbound — including whether prior authorization is required and any copay or cost estimates. New accounts also get a $50 credit. It's the rare next step that literally answers the question you came here to ask.

Check your Zepbound coverage — free, personalized to your plan

Ro contacts your insurer directly and sends back a written report, including PA status and estimated cost. No commitment. New accounts get a $50 credit toward getting started.

Check your Zepbound coverage, free →(Sponsored.) Coverage isn't guaranteed.

When your own doctor is the better move

Your own doctor may actually be your strongest play — if they already have your weight history, your A1C labs, your other conditions, and records of any programs you've tried. Coverage often hinges on documentation quality, and the person who already holds your records can sometimes build the strongest file. If you have a doctor like that and your plan covers GLP-1s, start there.

What your doctor should submit (weak wording vs. strong wording)

The paperwork should match the covered pathway, not the diagnosis that feels most urgent to you. A strong Zepbound request usually documents the FDA-approved use (weight management), your BMI, your lab proof, any required prior attempts, and why Zepbound is appropriate for you. The wording isn't a trick — it's about matching your plan's actual rule.

The documentation checklist (print this)

Bring or gather these for your doctor's office:

- Current BMI

- BMI at the start of treatment

- Weight history

- A1C, fasting glucose, or oral glucose tolerance test result (with the date)

- Date of prediabetes diagnosis

- Any other weight-related conditions

- Sleep apnea diagnosis, if you have one

- Medications you've already tried

- Lifestyle or weight-program records, if your plan requires them

- Your plan's specific PA form

- A letter of medical necessity, if required

- Your denial letter, if you're appealing

- If you're using the Medicare Bridge: the note “SEND TO BRIDGE FOR WEIGHT MANAGEMENT”

Weak wording vs. stronger documentation

| Weak | Stronger |

|---|---|

| “Zepbound for prediabetes” | “Zepbound for chronic weight management, with BMI and prediabetes documented” |

| “Patient wants a weight-loss shot” | “Patient meets plan criteria for an anti-obesity medication” |

| “Not diabetic but wants Zepbound/Mounjaro” | “Use the FDA-approved brand and use that match the patient's diagnosis and the plan's rules” |

| “A1C is high” | “Attach the actual A1C value, the date, and the diagnostic category” |

| “Patient tried diet” | “Attach the required lifestyle-program records if the plan requires them” |

This is not medical, legal, or coding advice. Your prescriber decides what is accurate and medically right for you.

Does Medicare cover Zepbound for prediabetes in 2026?

Regular Medicare Part D generally does not cover Zepbound for weight management or prediabetes. But starting , a new program called the Medicare GLP-1 Bridge will cover the Zepbound KwikPen for $50 a month, and a BMI of 27 or higher with prediabetes is one way to qualify. It's a weight-management program, not “coverage for prediabetes” — but for many people, it's the most affordable door that exists.

The Medicare GLP-1 Bridge, at a glance

| Bridge detail | What it means |

|---|---|

| Start date | |

| End date | |

| Covered Zepbound form | KwikPen only — single-dose vials and single-dose pens are not included |

| Also covered | All forms of Wegovy and Foundayo |

| Your cost | A flat $50 per month, even as your dose goes up |

| How it's structured | Outside your regular Part D benefit — the $50 does not count toward your deductible or the $2,100 out-of-pocket cap |

| Prediabetes pathway | BMI 27+ with prediabetes can qualify; BMI 35+ qualifies on its own |

| Prior authorization | Submitted through the Medicare GLP-1 Bridge central processor after the pharmacy routes the claim; not accepted before July 1, 2026 |

Source: CMS Medicare GLP-1 Bridge. The Bridge is a temporary pilot. The price is real, the savings are large (the list price is over $1,000/month), and prediabetes is genuinely one of the qualifying conditions.

How to make sure your Zepbound script actually goes through the Bridge

This is the detail most people miss, and it can make or break your claim. For the Bridge, CMS tells prescribers to put an obesity diagnosis code (from the E66 family) on the prescription, plus the note “SEND TO BRIDGE FOR WEIGHT MANAGEMENT.” That tells the pharmacist to route your claim to the Bridge's central processor instead of your regular Part D plan. The prior authorization goes through that Bridge central processor — not to CMS directly, and not through your Part D plan. Ask your prescriber for this, and it can save you a failed claim.

The sleep apnea exception

CMS says GLP-1 prescriptions written for type 2 diabetes, moderate-to-severe sleep apnea, or a liver condition called noncirrhotic MASH go through your regular Part D rules, not the Bridge. For Zepbound specifically, the one current non-weight-loss path through regular Part D is moderate-to-severe sleep apnea in adults with obesity — and some plans cover it that way even when they won't cover weight loss. If you snore heavily, wake up gasping, or feel exhausted despite sleeping, it's worth asking your doctor about a sleep study. See our full guide: Does insurance cover Zepbound for sleep apnea?

Medicare coverage depends on which path you're actually on

The Bridge, the sleep apnea route, regular Part D, or cash-pay — they're different doors, and the right one depends on your situation. Take our free quiz and we'll point you toward the path that fits.

Take the free 60-second GLP-1 path quiz →Does Medicaid cover Zepbound for prediabetes?

Medicaid coverage is state-specific, and many programs still limit GLP-1 coverage for obesity. Some states name prediabetes in their rules; many don't. The only way to know is your state's Medicaid drug list or your managed-care plan's PA form.

The national reality

Coverage is patchy and tightening. According to KFF, as of January 2026, only 13 state Medicaid fee-for-service programs covered GLP-1 medications for treating obesity, and the ones that do usually pile on requirements. So for many people on Medicaid, the honest answer is that Zepbound for weight loss simply isn't covered in their state — though a diabetes-type GLP-1 may be, if they have diabetes.

The MassHealth example

MassHealth's rules do reference prediabetes (A1c 5.7% to under 6.5%) at a BMI of 27+ — which proves some Medicaid programs treat prediabetes as relevant. It does not prove your state does. And remember the July 1, 2026 changes: even where prediabetes is named, the program may route you to a diabetes-type GLP-1 instead of Zepbound.

Your Medicaid checklist

- The state Medicaid drug list

- Your managed-care plan's formulary

- The anti-obesity medication PA form

- Whether Zepbound has specific criteria

- Whether your state covers obesity meds at all

- Whether prediabetes is listed as a qualifying condition

- Whether BMI must be documented within a set time window

Denied because you're “prediabetic, not diabetic”? Here's what to do

Don't appeal blindly. First figure out why you were denied — a hard drug exclusion, the wrong drug-or-diagnosis path, missing BMI proof, missing lab proof, a “try this first” rule, or a fixable plan requirement. The reason tells you whether to fight or pivot.

Zepbound denial decoder

| Denial language | What it may mean | Best next move |

|---|---|---|

| “Drug excluded” | Your plan may not cover weight-loss meds at all | Ask HR/benefits about an exception; check the sleep apnea or cash-pay route |

| “No type 2 diabetes diagnosis” | The request may have used diabetes-drug logic | Confirm it was submitted as Zepbound for weight management, not a diabetes drug |

| “BMI criteria not met” | The plan wants BMI 30+, or 27+ with a condition | Attach current and starting BMI documentation |

| “No qualifying comorbidity” | Your prediabetes may not have been documented clearly | Attach the actual A1C or glucose result, if accurate |

| “Lifestyle program required” | The plan wants proof you tried diet/exercise or a program | Submit those records if you have them |

| “Step therapy required” | The plan wants proof you tried another medication first, or a reason you can't | Your prescriber documents prior therapy or why it's not appropriate |

| “Not medically necessary” | The plan wants a stronger clinical case | Ask your prescriber whether a letter of medical necessity fits |

When an appeal makes sense

If the denial is about missing or incorrect documentation, that's a fixable fight — and a common one. Resubmit with your BMI proof, your lab proof, and the covered use (weight management). A strong letter of medical necessity usually documents your diagnosis, your weight and BMI history, the treatments you've already tried, your lifestyle efforts and their results, and the clinical reason Zepbound is right for you.

When it's a dead end (and that's okay to know)

If the denial is a hard exclusion for weight-loss drugs, an appeal will usually fail unless you have a separate covered diagnosis (like sleep apnea) or your employer offers an exception process. We're telling you this so you don't burn three weeks and a lot of hope on a plan that has plainly closed the door. If that's your situation, jump to the cash-pay section below.

Before you appeal, find out whether the problem is fixable

A quick coverage check with Ro shows whether Zepbound appears covered, whether PA is likely, and whether your “no” is a paperwork issue or a hard exclusion — so you spend your energy on the fight you can win.

Check whether your Zepbound denial is fixable, free with Ro →(Sponsored.)

What does Zepbound cost if insurance won't cover it?

Without insurance, Zepbound's retail list price still runs about $1,086 a month — but most people don't pay that. Eli Lilly's self-pay program, LillyDirect, sells Zepbound vials and the KwikPen for $299/month at the 2.5 mg dose, $399 at 5 mg, and $449 for 7.5–15 mg, as long as you refill within 45 days. And people with commercial insurance that covers Zepbound can pay as low as $25/month with the savings card. The smart comparison isn't just the medication price — it's medication price plus any visit or membership fee plus whether you get help with paperwork.

| Route | Best for | Pricing signal | What to verify |

|---|---|---|---|

| Ro | Commercial-insurance users who want coverage checking and PA help | Membership $39 first month, then $149/month, or as low as $74/month annual; medication separate | Current medication price, the coverage report, annual-plan terms |

| Sesame Care | Shoppers who want provider choice and transparent cash-pay pricing | Marketplace with a low-cost membership option and Zepbound cash prices listed by dose; medication separate | Current program fee, dose pricing, provider availability, PA help |

| LillyDirect (Lilly self-pay) | People who want brand Zepbound with no insurance | Vials and KwikPen: $299 (2.5 mg), $399 (5 mg), $449 (7.5–15 mg) when you refill within 45 days | The current dose prices and the 45-day refill rule; can't be combined with insurance |

| Zepbound Savings Card | Commercial-insurance users whose plan covers it | Eligible patients may pay as low as $25/month | Eligibility, card terms, government-insurance exclusions |

| Your own doctor + pharmacy | People with a clinician who can manage the PA | Depends on your plan and pharmacy | PA support, availability, plan rules |

Prices change often. Pricing verified . Verify the current numbers on each provider's page before you decide.

Why the lowest sticker price isn't always the right answer: If you need insurance paperwork done, a low medication price doesn't help much when you're stuck filing prior authorizations alone. That's exactly where Ro fits better than a “cheapest pill” link — it pairs FDA-approved Zepbound with a coverage check and a concierge who handles the PA. If you don't need any of that and just want the lowest brand price, LillyDirect is the straightest line. If you want to shop providers and compare cash prices yourself, Sesame Care is built for that.

Insurance said no? Compare the FDA-approved cash-pay path first

Don't switch plans or give up before comparing what FDA-approved Zepbound actually costs through legitimate routes.

(Sponsored.)

Safety: don't chase coverage harder than you chase fit

Coverage isn't the only gate — a clinician still has to decide Zepbound is right for you. It carries warnings that matter even when insurance says yes, and a covered medication can still be the wrong medication for a specific person.

Keep this in mind before you push hard for approval. Zepbound carries a boxed warning (the FDA's most serious warning) about a risk of thyroid C-cell tumors seen in animal studies. It should not be used by people with a personal or family history of medullary thyroid cancer (MTC) or a condition called Multiple Endocrine Neoplasia syndrome type 2 (MEN 2). The current Zepbound label also lists warnings for severe stomach and intestinal reactions, acute kidney injury from dehydration, gallbladder problems, pancreatitis, serious allergic reactions, low blood sugar (especially if you also take insulin or a sulfonylurea), diabetic eye disease in people with type 2 diabetes, and a risk of breathing food or liquid into the lungs during anesthesia. You should never share a Zepbound KwikPen with anyone. The most common side effects are stomach-related — nausea, diarrhea, constipation, and vomiting.

One piece of good news worth knowing: in February 2026, the FDA removed the old “suicidal behavior and ideation” warning from the Zepbound label — along with Wegovy and Saxenda — after a comprehensive review found no increased risk. If that warning worried you from older articles, the agency has since cleared it.

So here's our honest line: don't chase coverage harder than you chase the right fit. Talk with a licensed clinician about whether Zepbound makes sense for you and your prediabetes before you spend weeks fighting your insurer. The goal isn't to get approved for a drug. The goal is to get healthier.

How we verified this guide

We built this from official FDA, CMS, CDC, payer, and manufacturer sources, then organized it into a decision framework. The RX Index is a pricing intelligence and comparison resource for GLP-1 telehealth providers — not an insurer or a medical practice — so your specific plan documents and your clinician's judgment always have the final say.

What we actually verified:

- Zepbound's FDA-approved uses — chronic weight management and moderate-to-severe sleep apnea in adults with obesity — and that prediabetes is not an approved use

- The February 2026 removal of the suicidal-ideation warning from the Zepbound label

- The SURMOUNT-1 three-year results on diabetes progression (about a 94% lower risk; 1.3% vs. 13.3% new diabetes; 1,032 prediabetes participants)

- CDC and ADA prediabetes lab ranges

- Current MassHealth anti-obesity criteria, including the prediabetes language and the July 1, 2026 changes

- Medicare GLP-1 Bridge dates, $50 copay, covered Zepbound form (KwikPen only), the BMI 27+ prediabetes pathway, and the central-processor routing, from CMS

- KFF's count of state Medicaid GLP-1 coverage for obesity (13 states as of January 2026)

- Eli Lilly's list price, LillyDirect self-pay pricing, and the $25 savings-card terms

- Ro's coverage checker, concierge, and membership pricing; Sesame Care's program structure

What we could not verify (only you can):

- Your specific plan's formulary and exclusions

- Your exact copay

- Your pharmacy's stock

- Whether your clinician will prescribe Zepbound

- Whether your PA or appeal will be approved

- Every state Medicaid program's current rules

Frequently asked questions about Zepbound, insurance, and prediabetes

Most Zepbound prediabetes questions come down to one idea: prediabetes can support your coverage, but it usually doesn't replace your plan's main rule. These answers cover the edge cases that send people back to search.

Is Zepbound approved for prediabetes?

No. Zepbound is FDA-approved for chronic weight management in adults with obesity or overweight with a weight-related condition, and for moderate-to-severe sleep apnea in adults with obesity. It is not approved specifically to treat prediabetes.

Can I get Zepbound covered if I'm prediabetic but not diabetic?

Sometimes. Prediabetes can help if your plan covers Zepbound for weight management and you meet the BMI and documentation rules. It usually will not help if your plan flatly excludes weight-loss drugs.

What A1C counts as prediabetes?

An A1C of 5.7% to 6.4% is the prediabetes range. A fasting glucose of 100 to 125 mg/dL or a 2-hour glucose tolerance result of 140 to 199 mg/dL also fall in the prediabetes range, per the CDC.

Does prediabetes count as a weight-related condition for coverage?

It can, depending on the plan. Some payer rules name prediabetes directly, such as MassHealth; others do not, and some plans exclude obesity medications entirely. Confirm with your plan.

Does Medicare cover Zepbound for prediabetes?

Not through regular Part D for weight loss. But the Medicare GLP-1 Bridge, starting July 1, 2026, covers the Zepbound KwikPen for $50 per month, and a BMI of 27 or higher with prediabetes is one way to qualify.

Does regular Medicare Part D cover Zepbound for prediabetes?

Generally no for weight management. If Zepbound is prescribed for sleep apnea, your Part D plan may cover it. CMS routes diabetes, sleep apnea, and noncirrhotic MASH prescriptions through regular Part D rather than the Bridge.

Can prediabetes override a weight-loss drug exclusion?

Usually no. If your plan excludes weight-loss medications, prediabetes will not matter unless you have another covered diagnosis, an employer exception process, or a benefit change.

Does the Zepbound Savings Card work if insurance denies coverage?

The $25 savings card is for eligible patients with commercial insurance that covers Zepbound. If your plan does not cover it, the card generally does not apply, and government-insurance patients are excluded. Verify current terms before relying on the price.

How often should I re-check my Zepbound coverage?

At least at every plan-year renewal, after any denial, after an FDA or CMS update, and whenever your diagnosis or BMI documentation changes. Plan exclusions and prior authorization rules often change during annual benefit updates.

What if my plan says I need type 2 diabetes?

That usually means the request was judged under diabetes-drug rules, or your plan excludes weight-loss meds. Ask whether Zepbound is covered specifically for chronic weight management and whether prediabetes counts as a qualifying condition.

Should my doctor prescribe Mounjaro instead?

Not just to dodge coverage rules. Mounjaro and Zepbound contain the same active drug but have different approved uses, and insurers usually want the diagnosis to match the product. Your clinician decides what's accurate and appropriate.

What if I was denied because I didn't complete a weight-management program?

Some plans require documented diet, exercise, or program attempts first. Ask exactly what records they need and whether your prior efforts count, then resubmit.

Does Ro check insurance before I join?

Yes. Ro's GLP-1 Insurance Coverage Checker is free and gives you a personalized report on whether GLP-1 medications may be covered and whether prior authorization is likely. Ro also says its insurance concierge can submit the PA paperwork when needed.

Does Sesame Care handle prior authorization?

Sesame says its providers can work with your insurance on prior authorization. Confirm current pricing, provider participation, and availability before you rely on it.

Should I use compounded tirzepatide if insurance won't cover Zepbound?

This page is about FDA-approved Zepbound. Compounded tirzepatide is made by a pharmacy and is not the same as FDA-approved Zepbound, and it isn't an insurance-covered substitute. Look for a separate, carefully sourced guide on compounded options.

Still deciding? Let's find your path.

You came here for a straight answer, and here it is one more time: insurance usually won't cover Zepbound for prediabetes alone — but the weight-management door is real, prediabetes can help you through it, and if that door is closed, there's a cash-pay path that works. The next step depends on you. If you've got commercial insurance, a free coverage check tells you where you stand in minutes. If your plan excludes the drug, the cash-pay comparison is your move. And if you're not sure which path fits your BMI, your labs, and your budget — we built something for exactly that.

Still not sure which GLP-1 program is right for you?

Take our free 60-second matching quiz and get a personalized action plan for your situation — insurance type, BMI, labs, and budget.

Start the free quiz →Keep reading

- How insurance treats GLP-1 medications for prediabetes overall →

- The best Zepbound providers that accept insurance →

- The Medicare GLP-1 Bridge, explained step by step →

- Does insurance cover Zepbound for sleep apnea? →

- The Zepbound Savings Card: who really gets $25 →

- Does insurance cover Zepbound for PCOS? →

- Best brand-name GLP-1 telehealth providers 2026 →

- Find my GLP-1 path — free 60-second quiz →

Sources

Last verified: . All claims link to their primary source.

- U.S. Food and Drug Administration / Eli Lilly — Zepbound prescribing information and approval: accessdata.fda.gov/drugsatfda_docs/label/2026/217806s042lbl.pdf

- U.S. Food and Drug Administration — Drug Safety Communication, removal of suicidal behavior and ideation warning from GLP-1 RA medications (February 2026): fda.gov/drugs/drug-safety-and-availability/fda-requests-removal…

- New England Journal of Medicine — SURMOUNT-1 three-year results, “Tirzepatide for Obesity Treatment and Diabetes Prevention” (NEJMoa2410819): nejm.org/doi/abs/10.1056/NEJMoa2410819

- Centers for Disease Control and Prevention — Prediabetes ranges: cdc.gov/diabetes/diabetes-testing/index.html

- MassHealth Drug List (Conduent MHDL) — Anti-obesity agents criteria including prediabetes language and July 1, 2026 changes: mhdl.pharmacy.services.conduent.com/MHDL/pubtheradetail.do?id=478

- Centers for Medicare & Medicaid Services — Medicare GLP-1 Bridge program details: cms.gov/medicare/coverage…/information-medicare-beneficiaries

- KFF — Medicaid coverage of GLP-1s (13 state fee-for-service programs, January 2026): kff.org/medicaid/medicaid-coverage-of-and-spending-on-glp-1s/

- Eli Lilly — LillyDirect Self Pay Journey pricing ($299/$399/$449 by dose, 45-day refill rule) and Zepbound Savings Card terms. Lilly self-pay and savings pages.

- Ro — GLP-1 Insurance Coverage Checker, insurance concierge, and Ro Body membership pricing: ro.co/weight-loss/glp1-insurance-checker/ (sponsored affiliate link, opens in a new tab)

- Sesame Care — Online weight-loss program and prior-authorization support: sesamecare.com/service/online-weight-loss-program (sponsored affiliate link, opens in a new tab)

This guide is for general information, not medical, legal, or insurance advice. Coverage, pricing, and program rules change frequently and vary by plan and state. Confirm current details with your insurer, your clinician, and the official sources above before making decisions.

Your situation changes the answer

Find My GLP-1 Path

The right GLP-1 provider isn't the same for everyone. It depends on your state, your insurance and formulary, whether you want an FDA-approved or compounded medication, your preferred route (injection or oral), and your budget. Because a general answer can't resolve those for you, use The RX Index's Find My GLP-1 Path tool to get a personalized provider match with source-verified pricing before you choose.

- What it asks: your state, insurance situation, medication preference, budget, and support needs

- What you get: a personalized shortlist of GLP-1 providers matched to your situation, with verified pricing and the right questions to ask

- Cost: free · about 2 minutes · no signup