Is Compounded Semaglutide FSA Eligible? Yes — If These 3 Conditions Are Met

Published: · Last reviewed:

By The RX Index Editorial Team · FDA rules checked · Provider pages verified · IRS Publication 502 sourced

The RX Index is a pricing intelligence and comparison resource for GLP-1 telehealth providers. This is not medical or tax advice. Talk to your prescribing clinician and your plan administrator about your specific situation.

The short answer

Yes — compounded semaglutide can be FSA eligible when a licensed clinician prescribes it to treat a diagnosed medical condition like obesity, type 2 diabetes, or overweight with a weight-related health problem. IRS Publication 502 covers prescribed medicines and disease-based weight-loss treatment, and the rule doesn't draw a line between FDA-approved drugs and compounded drugs. Medical necessity is the test.

Two things change the answer: (1) if the prescription is purely cosmetic — no diagnosis, no chart note — it is not FSA eligible; and (2) the FDA declared the semaglutide shortage resolved on February 21, 2025, narrowing access to compounded semaglutide in 2026. Your IRS eligibility didn't change. Access did.

Your situation in one table

| Your situation | FSA path | What to keep |

|---|---|---|

| Prescribed for diagnosed obesity, type 2 diabetes, hypertension, or another condition | Strongest claim | Prescription + itemized receipt + LMN |

| FSA card declines at checkout | Still may be reimbursable | Pay normally + submit packet |

| Compounded prescription with a vague "weight loss program" receipt | High denial risk | Get a corrected itemized receipt before submitting |

| No diagnosis, cosmetic weight loss only | Not eligible | Don't submit as a medical expense |

| Bundled membership + coaching + supplements | Mixed | Itemize the medication separately; only the medical portion qualifies |

Still not sure where you stand? Take our free 60-second matching quiz → We'll send back a documentation checklist built for your exact situation. No signup.

What we actually verified for this page

As of May 11, 2026, we verified:

- IRS rules on prescribed medicines and disease-related weight-loss expenses via IRS Publication 502 (2025) and IRS Topic 502.

- 2026 HSA contribution limits via IRS Revenue Procedure 2025-19; 2026 Health FSA limits via IRS Revenue Procedure 2025-32.

- Current FDA position on compounded semaglutide including the April 30, 2026 proposed exclusion of semaglutide from the 503B bulks list.

- FDA published concerns about dosing errors, refrigeration, salt forms, and adverse-event reports as of July 31, 2025.

- The September 9, 2025 FDA warning letter to DirectMeds; September 16, 2025 wave of 55+ warning letters; February 20, 2026 warning letter #721455 to MEDVi; and March 2026 wave of 30+ letters.

- Public payment-page language at Embody, SHED, MyStart Health, DirectMeds, Enhance.MD, MEDVi, Hers, and Ro as of May 11, 2026.

Where we couldn't independently confirm a claim, the provider matrix marks it "provider-stated" or "not publicly verified." Numbers and policies change. Re-check before you pay.

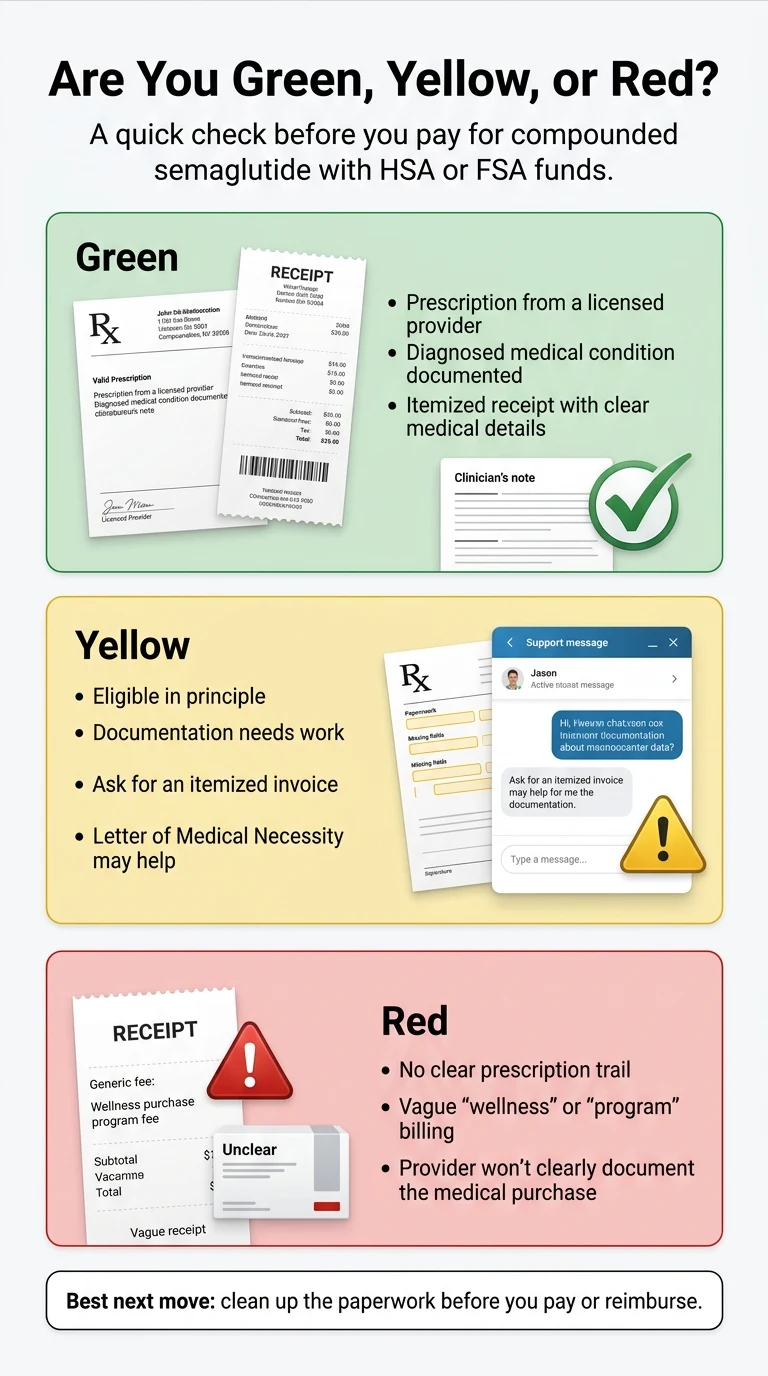

Is compounded semaglutide FSA eligible? The 3 questions every other page collapses into one

Compounded semaglutide is generally FSA eligible when prescribed for a diagnosed medical condition. But "FSA eligible" is actually three separate questions with three separate answers, and most pages mash them all together. Eligibility under IRS rules, card acceptance at checkout, and reimbursement approval are three different gates. You need all three to clear for the FSA to pay you back.

This is why one person can swipe her card with no problem at one telehealth provider and you can have your card declined at another — both for the same medication.

Question 1 — Is the expense eligible under IRS rules?

This is the federal tax rule. Under IRS Section 213(d) and Publication 502, a "qualified medical expense" is one paid mainly to alleviate or prevent a physical or mental illness. Prescribed medicines qualify. So does treatment for a specific disease diagnosed by a physician — and the IRS explicitly lists obesity as one of those diseases. Cosmetic weight loss with no diagnosis does not qualify.

Publication 502 does not require FDA approval as a condition of eligibility. Medical necessity is the test, not the manufacturing pathway.

Question 2 — Will the provider's checkout accept your FSA card?

This is a merchant question, not an IRS question. Each provider chooses how to set up their payment system. Some — like SHED — publish explicit HSA/FSA card-acceptance language. Others — like Ro and Hers — are reimbursement-first: you pay with a personal card and then submit for reimbursement. Same tax savings either way. Just different friction.

A declined card doesn't usually mean your expense is ineligible. It usually points to payment processing, merchant coding, balance, substantiation rules, or your plan administrator's specific configuration — not an automatic IRS rejection.

Question 3 — Will your plan administrator actually reimburse the claim?

This is where most claims trip. Even when the expense is eligible and the card runs cleanly, plan administrators can still flag weight-management charges for review. Bundled charges — medication + visits + coaching all on one line — can lead to partial reimbursement instead of full. FSAs flag these claims more aggressively than HSAs.

This is the reason the Letter of Medical Necessity (LMN) exists. We'll show you exactly what one needs to contain in the next section.

One reader, three different outcomes

Imagine three readers, all prescribed compounded semaglutide for diagnosed obesity at the same provider for the same price.

- Reader A has a clean prescription, a diagnosis on file, and the FSA card runs at checkout. Full success, no paperwork.

- Reader B has the same setup but the card doesn't run because the provider isn't configured for direct card processing. She pays with her personal card, submits an itemized receipt and her LMN, and the reimbursement clears. Full success, one form.

- Reader C has the same setup but the receipt only says "Weight loss program — $249." Her administrator asks for itemization, she can't get the provider to break it out fast enough, and the claim sits in pending. Tax money is fine, but the paperwork is broken.

Same drug. Same diagnosis. Three different outcomes — all controlled by paperwork and provider choice.

Claim strength by packet

| What's on file | Claim strength | What usually happens |

|---|---|---|

| Diagnosis + Rx + itemized receipt + LMN | Strongest | Approved without back-and-forth |

| Diagnosis + Rx + vague "weight loss program" receipt | Documentation risk | Administrator asks for itemization |

| "Wellness package" with no diagnosis | Partial / denial | Only the medical portion may reimburse |

| Cosmetic weight loss, no diagnosis | Not eligible | Should not be submitted as medical |

Want a documentation packet built for your situation in 60 seconds?

Take the free GLP-1 matching quiz. It returns the exact documents to ask your provider for, based on your account type and diagnosis. No signup.

Take the free quiz →What the IRS actually says about prescribed semaglutide

The IRS rule is shorter than people think. Under IRS Publication 502, you can use FSA and HSA funds for "amounts you pay for prescribed medicines and drugs" and for "amounts paid to participate in a weight-loss program for a specific disease or diseases, including obesity, diagnosed by a physician." That's the eligibility test. Publication 502 doesn't exclude compounded drugs and doesn't make FDA-approval status a condition. Medical necessity is what counts.

The exact language that matters

From IRS Publication 502 (2025 edition):

"You can include in medical expenses amounts you pay for prescribed medicines and drugs. A prescribed drug is one that requires a prescription by a doctor for its use by an individual."

And:

"Amounts paid to participate in a weight-loss program for a specific disease or diseases, including obesity, diagnosed by a physician."

Two clauses. That's the framework that controls billions of dollars in claims every year. Publication 502 does not exclude compounded drugs. Medical necessity is the test, not the manufacturing pathway.

Diagnoses that anchor a strong claim

These are the diagnoses most often on FSA-eligible GLP-1 claims. Each has an ICD-10 code — putting it on your LMN makes the claim move faster.

| ICD-10 code | Diagnosis |

|---|---|

| E66.01 | Morbid obesity due to excess calories |

| E66.9 | Obesity, unspecified |

| E11.9 | Type 2 diabetes mellitus without complications |

| R73.03 | Prediabetes |

| G47.33 | Obstructive sleep apnea (adult) |

| I10 | Essential hypertension |

| E78.5 | Hyperlipidemia, unspecified |

| E88.810 | Metabolic syndrome |

A BMI of 30 or higher generally meets the obesity threshold. A BMI of 27 or higher with a weight-related condition (high blood pressure, sleep apnea, dyslipidemia, prediabetes) generally meets the "overweight with comorbidity" threshold.

What does NOT qualify

- Cosmetic weight loss with no documented diagnosis. "I want to drop ten pounds before a wedding" doesn't pass §213(d), no matter what your scale says.

- General wellness coaching not tied to a diagnosed condition.

- Diet food that substitutes for normal nutrition.

- Gym memberships that aren't prescribed for a specific disease.

- Supplements without a clinical prescription for a diagnosed condition.

The mechanism in one line

Prescription + diagnosed condition + itemized receipt = eligible. Lose any of the three and your claim gets harder.

Sources: IRS Publication 502 (2025); IRS Topic 502; IRS FAQ on medical expenses related to nutrition, wellness, and general health (2023).

The 2026 FDA reality (what changed after the shortage ended)

Compounded semaglutide is in a narrower regulatory window in 2026 than it was in 2024. The FDA declared the semaglutide shortage resolved on February 21, 2025. Enforcement discretion for 503A state-licensed pharmacies ended April 22, 2025. For 503B outsourcing facilities it ended May 22, 2025. On April 30, 2026 the FDA proposed permanently excluding semaglutide from the 503B bulks list. Your tax eligibility under IRS rules didn't change. But the legal pathway under which most compounded semaglutide was produced over the past three years narrowed sharply.

Two key terms before we go further:

- 503A pharmacy — a state-licensed compounding pharmacy that fills patient-specific prescriptions one at a time.

- 503B outsourcing facility — a larger FDA-registered facility that can compound in bulk for office use.

When a drug is on the FDA's shortage list, both types can compound a version that's essentially a copy of the FDA-approved drug. When the shortage ends, that "essentially a copy" pathway closes — unless the prescriber determines that a change from the commercially available drug will produce a significant difference for the identified patient and documents that difference.

One honest trade-off

Compounded semaglutide is not FDA-approved and does not carry FDA premarket review for safety, effectiveness, or quality. The FDA's position is that compounded drugs should be used only when a patient's medical needs cannot be met by an FDA-approved drug. If you want zero regulatory ambiguity with your FSA dollars and your insurance covers a brand-name option, FDA-approved Wegovy or Ozempic through Ro is the cleaner path. Ro matches LillyDirect, NovoCare, and TrumpRx pricing on medication and includes an insurance concierge that handles prior-authorization paperwork for you.

But Ro does not typically run your FSA card directly at checkout — they use a pay-then-reimburse model. That trade-off is precisely why compounded semaglutide — with providers like SHED that publicly say HSA/FSA cards are accepted — still has a real role for the right reader.

See Ro's FDA-approved options → (sponsored affiliate link, opens in a new tab)Ro matches LillyDirect / NovoCare / TrumpRx pricing. Insurance concierge handles prior-auth.

The timeline, plain

| Date | What changed |

|---|---|

| March 2022 | FDA adds Wegovy to the drug shortage list. |

| August 2022 | FDA adds Ozempic to the drug shortage list. |

| Feb 21, 2025 | FDA declares the semaglutide shortage resolved. |

| Apr 22, 2025 | 503A enforcement discretion ends for semaglutide. |

| May 22, 2025 | 503B enforcement discretion ends for semaglutide. |

| Apr 24, 2025 | District court denies preliminary injunction in Outsourcing Facilities Association v. FDA. |

| Sep 9, 2025 | FDA issues warning letter to DirectMeds over compounded GLP-1 marketing claims. |

| Sep 16, 2025 | FDA publishes 55+ warning letters to online sellers of compounded GLP-1s. |

| Feb 20, 2026 | FDA issues warning letter #721455 to MEDVi over compounded GLP-1 labeling. |

| Mar 2026 | FDA issues 30+ additional warning letters to telehealth companies for compounded GLP-1 marketing. |

| Apr 30, 2026 | FDA proposes permanently excluding semaglutide from the 503B bulks list. Public comment open through June 29, 2026. |

"Significant difference for the identified patient" — what compounded semaglutide can still be prescribed for in 2026

After the shortage ended, compounded semaglutide can still be lawfully prescribed for a specific patient when the clinician determines and documents a significant difference that the FDA-approved version doesn't address. In plain language, that usually means:

- A documented allergy or intolerance to an inactive ingredient in the brand-name pen.

- A dose strength not commercially available (often for slow titration or microdosing).

- A different route of administration — oral or sublingual instead of injection — when there's a patient-specific clinical reason.

Cost and convenience alone don't meet the standard. If a telehealth provider still sells you compounded semaglutide in 2026, your prescribing clinician should have a documented clinical reason on your chart. That reason also belongs on your Letter of Medical Necessity. It's not a checkbox — it's audit defense.

What the FDA has actually flagged on safety

The FDA has publicly warned about:

- Dosing errors with compounded injectable semaglutide — patients measuring incorrect doses from multidose vials, sometimes resulting in hospitalization.

- Improper refrigeration during shipping, which can affect medication integrity.

- Fraudulent compounded GLP-1 products — counterfeits sold online, often from foreign sources, sometimes without prescriptions.

- Salt forms like semaglutide sodium and semaglutide acetate, which the FDA has flagged as different active ingredients from the semaglutide base in FDA-approved Wegovy and Ozempic.

- Adverse-event reports — as of July 31, 2025, the FDA reported receiving more than 605 reports of adverse events with compounded semaglutide and more than 545 with compounded tirzepatide, while noting that reporting is voluntary and likely undercounts events.

What about the FDA warning letters?

In September 2025 the FDA published more than 55 warning letters in one wave to online sellers of compounded GLP-1s, including DirectMeds, for misleading marketing language. In February 2026 the FDA sent warning letter #721455 to MEDVi over how the company presented compounded semaglutide and tirzepatide on its website. In March 2026 the FDA issued more than 30 additional warning letters to telehealth companies for similar marketing concerns.

These letters focused on labeling and marketing language — claims FDA said implied FDA approval of compounded products. They were not manufacturing-quality findings. But they matter because the FDA specifically objected to claims that could mislead readers about what compounded products actually are. We've factored that into our provider matrix below.

Sources: FDA, "FDA clarifies policies for compounders as national GLP-1 supply begins to stabilize"; FDA Warning Letter to DirectMeds (09/09/2025); FDA Warning Letter #721455 to MEDVi (02/20/2026); FDA Press Announcement, "FDA Warns 30 Telehealth Companies Against Illegal Marketing of Compounded GLP-1s" (Mar 2026); proposed rule, exclusion of semaglutide from 503B bulks list (Apr 30, 2026).

The documentation packet that keeps your claim from getting denied

The single most common reason a legitimate compounded semaglutide claim gets denied is paperwork — not eligibility. Keep four documents and you'll cover the core items administrators commonly ask for: a prescription, an itemized receipt, proof of payment, and a Letter of Medical Necessity (LMN). For weight-management claims, the LMN is what turns "we need more information" into "approved."

The minimum documentation packet

| Document | Why it matters | What to ask your provider for |

|---|---|---|

| Prescription | Proves it's a prescribed medical treatment | A copy of the prescription or your treatment record |

| Itemized receipt | Shows what was purchased and when | Medication name, dose, route, date, amount, prescriber, dispensing pharmacy |

| Letter of Medical Necessity (LMN) | Especially needed for weight-related claims | Statement tying the medication to your diagnosis |

| Proof of payment | Required for reimbursement | Card receipt or invoice marked paid |

| Pharmacy/source details | Reduces ambiguity on compounded meds | Dispensing pharmacy name + Rx number |

The 7 elements your LMN should contain

We built this from the FSAFEDS LMN structure (the federal government's own template), IRS Publication 502, and what we've seen actually move claims through review. Most LMN templates online include five elements. The two most templates miss — and the two that matter most in 2026 — are the ICD-10 diagnosis code and the clinical rationale for compounded over FDA-approved.

- 1. Patient identification

Your full legal name, date of birth, and any account or medical record numbers.

- 2. Specific diagnosis with ICD-10 code

Not just "obesity" — the code (e.g., E66.01) plus your BMI and any comorbid conditions.

- 3. Clinical history substantiating the diagnosis

A short narrative — two or three sentences — supporting the diagnosis.

- 4. Medication name, dose, and route

"Compounded semaglutide injection, weekly subcutaneous, dose titrating from 0.25 mg."

- 5. Statement of medical necessity

A direct sentence saying the medication is medically necessary for the diagnosed condition.

- 6. Patient-specific clinical rationale for compounded over FDA-approved

Why this specific patient is getting compounded instead of brand-name — documented inactive-ingredient allergy, a dose strength not commercially available, or a clinical reason for a different route. This is the 2026 addition most templates miss.

- 7. Provider signature, license number, NPI, and date

Required for the LMN to be treated as credentialed clinical documentation.

Missing any of these can stretch your reimbursement from days into weeks.

Copy-and-paste script to ask your provider for the LMN

Don't overthink this. Send this exact message to your prescribing clinician through your provider portal:

Most providers can have this back to you within a few business days. Some bake it into their intake — Embody and MyStart Health publish FSA/HSA documentation language on their public pages. SHED's help center explicitly says the team can provide receipts or additional documents if your administrator asks. You should not have to fight for this.

What your LMN should NOT say

Vague language hurts you. Skip these phrases — they don't help and they can hurt:

- "General wellness"

- "Lifestyle support"

- "Weight optimization"

- "Cosmetic weight loss"

You want clinical language tied to a diagnosis. Not marketing language tied to a goal.

Does this look like your documentation path?

Embody's Start Program lists compounded semaglutide injection at $99 first month, then $299/month, with compounded tirzepatide and a needle-free GLP-1 gum option (gum from $149 first month). Cash-pay, no insurance required, and advertised HSA/FSA eligible — confirm with your plan. Compounded medications are not FDA-approved; your clinician should document the patient-specific clinical reason for compounded.

Check eligibility via our quiz →FSA card at checkout vs. pay-and-reimburse

Some telehealth providers run your FSA card directly at checkout. Most don't. Both paths give you the same tax savings — they differ in friction. Direct card acceptance is faster but offers less control over how the charge is documented. The pay-and-reimburse path is slower but lets you attach an LMN and itemized receipt before submitting, which reduces documentation back-and-forth when a compounded medication claim gets reviewed.

For compounded semaglutide specifically, we generally lean toward the pay-and-reimburse path. Here's why.

Direct FSA card swipe — fast but blind

When a provider's checkout supports FSA card processing, you swipe and the charge goes through like any other payment. The merchant category code on the back end classifies the transaction as medical. No upfront paperwork.

Best for: Single, clean prescription purchases where you already have your documentation packet ready.

Risk: The card processes fine, but your administrator can still ask for proof later. If you don't have the LMN and itemized receipt saved at the time of purchase, you scramble.

Providers with the clearest public card-at-checkout language for compounded semaglutide as of May 2026: SHED (help-center page explicitly mentions HSA/FSA card acceptance for prescription purchases) and MyStart Health (says some HSA/FSA cards work directly). Embody advertises HSA/FSA eligibility across its programs but doesn't make a specific direct-card-at-checkout promise on the pages we verified. Verify the card runs in your specific situation before assuming.

Pay normally and submit for reimbursement — slower but controlled

You pay with a regular debit or credit card. You collect the prescription, itemized receipt, LMN, and proof of payment. You log into your FSA portal and submit a claim. This is the cleaner path for compounded semaglutide in 2026: an administrator that flags a compounded charge for review has all the documentation sitting in your submitted packet. There's no back-and-forth.

Best for: Compounded medication claims, bundled telehealth programs, or any claim that's likely to be flagged for documentation.

Risk: Timing — you front the money and wait for the reimbursement to clear.

Quick decision table

| If your top priority is… | Use this path |

|---|---|

| Fastest checkout | Direct FSA card (if the provider supports it) |

| Lowest denial risk | Pay normally, submit reimbursement packet |

| Your administrator already asked for documentation | Pay-and-reimburse with LMN attached |

| The provider's receipt looks vague | Don't submit until they correct the itemized receipt |

| You want FDA-approved medication instead | Switch lanes to a brand-name provider like Ro |

For the broader version of this guide across all GLP-1 medications, see Can I Use My FSA for GLP-1?

Want the FSA card path with the clearest public support?

SHED's help center says HSA/FSA cards are accepted for prescription purchases and that receipts or additional documents can be provided if an administrator asks. Compounded medications are not FDA-approved.

Check availability via our quiz →Our compounded semaglutide FSA verification matrix

"FSA eligible" on a marketing page and "card actually runs at checkout" are not the same thing. We checked public payment-page language for compounded semaglutide specifically at eight major telehealth providers as of May 11, 2026.

This isn't a generic affiliate list. For a YMYL page like this one, we lead with whoever has the cleanest public documentation right now.

How to read the matrix

- ✅ = consistent public evidence on May 11, 2026.

- ⚠️ = provider-stated; not independently verified.

- ❌ = provider does not offer this for compounded semaglutide, or actively contradicts the column claim.

Policies and prices change. Re-check before checkout.

| Provider | Dispenses compounded semaglutide? | HSA/FSA card at checkout? | Itemized receipt? | LMN on request? | Notes |

|---|---|---|---|---|---|

| Embody | ✅ Yes — compounded semaglutide & tirzepatide, weekly injection or needle-free GLP-1 gum | ⚠️ Advertised HSA/FSA eligible (confirm with your plan); direct-card-at-checkout not specifically publicly verified | ✅ Yes | ⚠️ Provider-stated | Cash-pay, no insurance required. Low first-month pricing — from $99 first month (sema injection), then $299–$449/mo by medication and form. Needle-free GLP-1 gum option. Not available in every state — check during intake. Compounded medications are not FDA-approved. |

| SHED | ✅ Yes — liquid drops, lozenges, and injections | ✅ Help center says HSA/FSA cards are accepted for prescription purchases | ✅ Yes (help center says receipts and additional documents can be provided) | ✅ Yes (per help center) | Strongest public card-acceptance language we verified. Compounded medications are not FDA-approved. |

| MyStart Health | ⚠️ Verify current product mix | ✅ Says some HSA/FSA cards work directly; publishes HSA/FSA documentation pack | ✅ Yes | ✅ Yes | Best for documentation-pack strength. |

| DirectMeds | ✅ Yes — sublingual ~$249/mo; injection ~$297/mo | ✅ Provider-stated; HSA/FSA accepted | ✅ Provider-stated | ⚠️ Provider-stated | FDA warning letter (Sept 9, 2025) over compounded GLP-1 marketing claims. Verify current claims language before signup. |

| Enhance.MD | ✅ Yes (premium clinical-feel) | ❌ Provider page states FSA/HSA cards are not accepted at this time | ✅ Provider-stated | ⚠️ Provider-stated | Reimbursement only; not a direct-card route. |

| MEDVi | ⚠️ Verify current product mix | ⚠️ Provider-stated | ⚠️ Provider-stated | ⚠️ Provider-stated | FDA warning letter #721455 (Feb 20, 2026) over compounded GLP-1 marketing claims. Not featured as a winner on this page; will re-evaluate once corrective status is publicly verifiable. |

| Hers | ❌ Largely shifted to FDA-approved Wegovy pill/pen and Ozempic following March 2026 Novo Nordisk partnership | ⚠️ Reimbursement-first; Hers says users can download receipts for HSA/FSA reimbursement | ✅ Yes | ⚠️ Provider-stated | Best if you want a female-coded FDA-approved path. |

| Ro | ❌ Does not lead with compounded; FDA-approved Wegovy pen, Wegovy pill, Zepbound pen, Zepbound KwikPen, Foundayo | ❌ Pay-then-reimburse; not a direct-card route | ⚠️ Not specifically publicly verified for FSA reimbursement | ⚠️ Not specifically publicly verified | Strong FDA-approved / insurance-concierge path. Body membership $39 first month, then $149/month — or as low as $74/month annual prepay. Free insurance coverage checker. |

For the broader provider table that includes general HSA/FSA payment paths across all GLP-1s, see GLP-1 Providers That Take FSA.

Why we're not leading with MEDVi or DirectMeds on this page

MEDVi is not a winner on this page because the FDA issued a February 20, 2026 warning letter over compounded GLP-1 marketing claims. DirectMeds is not a winner because the FDA issued a September 9, 2025 warning letter for similar marketing concerns. Both companies remain operational, both letters were about marketing language rather than manufacturing-quality findings, and both companies were part of broader FDA enforcement waves. For the specific job of making your FSA claim go smoothly today — where every receipt, every label, and every claim matters — the evidence supports leading you to providers with cleaner public FSA documentation right now.

For low-cost cash-pay compounded GLP-1 with HSA/FSA eligibility:

Embody's Start Program begins at $99 first month for compounded semaglutide injection (then $299/month), with compounded tirzepatide and a needle-free GLP-1 gum option (gum from $149 first month). Cash-pay, no insurance required. Advertised HSA/FSA eligible — confirm with your plan. Compounded medications are not FDA-approved.

See Embody Pricing → (sponsored affiliate link, opens in a new tab)For HSA/FSA card-at-checkout convenience:

Help center says HSA/FSA cards are accepted for prescription purchases. Compounded liquid drops, lozenges, and injections. Compounded medications are not FDA-approved.

See SHED options via quiz →For FDA-approved Wegovy or Ozempic instead:

Ro matches LillyDirect / NovoCare / TrumpRx pricing. Insurance specialists work directly with your plan. Pay-then-reimburse for FSA.

See Ro's coverage checker → (sponsored affiliate link, opens in a new tab)Compounded vs. FDA-approved semaglutide — what changes for your FSA claim

The IRS eligibility rule is identical for compounded and FDA-approved semaglutide. What changes is friction. FDA-approved Wegovy or Ozempic filled at a retail pharmacy is generally easier to substantiate than a bundled telehealth or compounded charge. Compounded semaglutide ordered through a telehealth provider is more likely to be flagged and asked for an LMN. Same eligibility. Different scrutiny.

Side-by-side comparison

| Aspect | Compounded semaglutide | FDA-approved Wegovy / Ozempic |

|---|---|---|

| FSA/HSA eligible under IRS rules | Yes (when prescribed for diagnosis) | Yes |

| Typical monthly cost | $149–$349 | $200–$1,300+ depending on plan/cash |

| FDA-approved as a finished product | No | Yes |

| Card at retail pharmacy | n/a (compounding pharmacy) | Generally easier to substantiate |

| Card at telehealth checkout | Some providers (SHED publicly; MyStart partially) | Some providers; Ro is pay-then-reimburse |

| LMN required by most administrators | Often yes | Sometimes; less for diabetes diagnosis |

| Insurance coverage available | Rarely | Yes, varies by plan |

| 2026 regulatory ambiguity | Yes — 'significant difference for the identified patient' required | None — fully approved |

Who should consider switching to FDA-approved

Switch lanes if any of these describe you:

- You don't have a documented "significant difference" reason for compounded.

- You want the cleanest possible audit defense.

- Your insurance covers Wegovy or Ozempic.

- Your FSA administrator has already pushed back on a compounded claim.

- You're not comfortable with the FDA's compounded-product regulatory position.

Ro is the strongest insurance-concierge route for the FDA-approved lane. Body membership is $39 for the first month, then $149/month — or as low as $74/month with annual prepay. Medication cost is separate, and Ro matches LillyDirect, NovoCare, and TrumpRx pricing on FDA-approved options. Ro's free GLP-1 Insurance Coverage Checker collects your insurance-card information and sends a personalized coverage report.

Prefer FDA-approved GLP-1s with insurance support?

Run Ro's coverage checker → (sponsored affiliate link, opens in a new tab)Ro collects your insurance-card information and sends a personalized coverage report. Insurance specialists work directly with your plan.

What you actually save

Using FSA or HSA funds for compounded semaglutide cuts your real cost by roughly 15% to 48% — depending on your federal bracket, state tax, and whether your contribution avoids FICA. The math is the same for HSA and FSA accounts. The only difference is timing — HSA balances roll over; FSA balances usually don't.

Quick savings reference

These estimates assume a state income tax rate around 5% and assume your FSA contributions avoid the 7.65% employee share of FICA. Using $249/month as the example — a common compounded semaglutide price point.

| Federal bracket | Effective discount | Monthly savings | Annual savings |

|---|---|---|---|

| 12% | ~24.65% | ~$61 | ~$737 |

| 22% | ~34.65% | ~$86 | ~$1,036 |

| 24% | ~36.65% | ~$91 | ~$1,096 |

| 32% | ~44.65% | ~$111 | ~$1,335 |

| 35% | ~47.65% | ~$119 | ~$1,425 |

- HSA contributions avoid FICA only if made through a payroll cafeteria plan. If you contribute directly outside of payroll, you save income tax but not FICA.

- State tax savings vary widely. California, New York, and Oregon add more. Texas, Florida, and Washington (no state income tax) save less.

- A $680 FSA carryover is allowed for 2026 plans that opt in. Anything above that you forfeit if you don't spend it by your plan's deadline.

- 2026 FSA contribution limit: $3,400 (per IRS Rev. Proc. 2025-32).

- 2026 HSA contribution limits: $4,400 individual; $8,750 family; plus $1,000 catch-up at age 55+ (per IRS Rev. Proc. 2025-19).

Calculate your own number

$1,035

Annual savings

$86

Monthly savings

$163

Effective monthly cost

35%

% off

Estimate only. Actual savings depend on your tax bracket, state, and payroll setup. Not tax advice. Consult a tax professional for your specific situation.

If your FSA claim for compounded semaglutide gets denied — the rescue workflow

Most first-time denials are about documentation, not eligibility. The denial letter will tell you the reason. Your appeal should include the prescription, an itemized receipt with the medication line item broken out, and an LMN with all seven elements. Don't give up — resubmit smart. The IRS rule is in your favor when the prescription and diagnosis are real.

The 5-step rescue workflow

- Read the denial reason carefully. Plan administrators usually give a specific cause — missing documentation, insufficient itemization, missing diagnosis support, or an explicit plan exclusion.

- Identify whether it's an eligibility issue, a documentation issue, a merchant-coding issue, or an LMN issue. When the prescription and diagnosis are real, many denials are fixable documentation problems.

- Request the missing piece from your provider. Itemized receipt that breaks out medication vs. visit vs. coaching. LMN with the seven elements. Prescription documentation if it wasn't included originally.

- Resubmit with a brief cover note. A short, direct cover note carries the day. See the script below.

- Call the administrator if the reason isn't clear. Sometimes the letter is vague. A two-minute phone call usually clarifies what they actually want.

The four most common denial reasons and how to fix each

| Denial reason | Missing piece | Fix |

|---|---|---|

| "This appears to be a subscription fee, not a medical expense." | Itemized receipt that separates medication from membership/coaching | Submit an itemized receipt + LMN |

| "Weight loss programs require LMN under our plan." | LMN with ICD-10 diagnosis code and BMI | Submit the seven-element LMN |

| "Compounded medications require additional documentation." | Clinical rationale for compounded over FDA-approved | Add the patient-specific compounded rationale to your LMN |

| "The receipt does not show medication name or pharmacy." | Itemized receipt listing medication, dose, route, dispensing pharmacy | Request a corrected receipt; if the provider can't produce one, consider a different lane |

Copy-and-paste appeal cover note

Know your appeal window

Check your plan document for the appeal deadline before you do anything else. FSAFEDS uses 30-calendar-day windows at later appeal stages, while other health FSA procedures may give a longer first-level appeal window. Don't assume every plan uses the same deadline.

When to stop fighting and switch paths

Stop pushing if:

- Your provider literally cannot produce an itemized receipt that lists the medication and pharmacy.

- Your prescription wasn't tied to a diagnosed condition (the IRS rule fundamentally can't help you here).

- Your plan document explicitly excludes the charge.

If any of these apply, your next step is either to get re-evaluated by a clinician for a documented diagnosis, or to switch to an FDA-approved route through Ro where the audit defense is cleaner.

Best route by situation

Four common reader situations map to four different right answers. Find yourself in the list and skip the rest.

"I have a diagnosis and a documented clinical reason for compounded."

You've got the foundation right. Keep your documentation tight, confirm your plan's rules before checkout, and make sure your clinician documents the patient-specific reason for compounded. Embody is a strong low-cost cash-pay default — compounded semaglutide injection from $99 first month (then $299/month), compounded tirzepatide and a needle-free GLP-1 gum option, advertised HSA/FSA eligibility (confirm with your plan), and no insurance required.

See Embody Pricing → (sponsored affiliate link, opens in a new tab)"I want the FSA card to actually run at checkout."

SHED's help center publishes the clearest language on this we verified: HSA/FSA cards accepted for prescription purchases, with receipts or additional documents provided if your administrator asks. Compounded liquid drops, lozenges, and injection options.

See SHED options via quiz →"I want FDA-approved — compounded ambiguity isn't worth it to me."

Ro is the cleanest insurance-concierge route. Wegovy pen, Wegovy pill, Zepbound pen, Zepbound KwikPen, and Foundayo are all available. Ro matches LillyDirect / NovoCare / TrumpRx pricing. Body membership is $39 first month, then $149/month — or as low as $74/month annual prepay.

Run Ro's coverage checker → (sponsored affiliate link, opens in a new tab)"I have no idea which fits me."

That's why the quiz exists. 60 seconds, no signup. We send back a personalized path based on your account type, diagnosis, state, and budget.

Take the free 60-second quiz →What real users are saying about this exact problem

We pull these from public Reddit threads to illustrate the friction real readers feel — not as medical, tax, or regulatory evidence. They show the documentation gap and the anxiety that drives most "is compounded semaglutide FSA eligible" searches.

"My FSA says I have to prove I medically need GLP-1 or they will deny."

— Reddit, r/SemaglutideCompound — “Tips for FSA approval?”

"I didn’t even know what a letter of medical necessity was."

— Reddit, r/SemaglutideCompound — “HSA and Compounded Semaglutide”

"Not being FDA approved gives me pause."

— Reddit, r/SemaglutideCompound — “HSA and Compounded Semaglutide”

If any of these sound like the question in your head, you're already most of the way to solving it — just by understanding which document goes where. The system isn't designed to be hostile. It's designed to verify.

These are public user comments included to illustrate common documentation concerns. They are not medical, legal, tax, or regulatory evidence.

Frequently asked questions

Still not sure which GLP-1 program is right for you?

Take our free 60-second matching quiz. Tell us your account type, diagnosis, state, and budget. We'll send back a personalized path — compounded with FSA at checkout, FDA-approved with insurance support, oral instead of injection, or something in between.

60 seconds. No signup. Free.

Related guides on The RX Index

If this page didn't answer your specific situation, one of these probably does:

- Can I Use My FSA for GLP-1? — the broader rules and payment guide across all GLP-1 medications.

- Is Compounded Semaglutide HSA Eligible? — HSA-specific version of this question.

- GLP-1 Providers That Take FSA — full provider table with FSA payment paths across all GLP-1s.

Methodology and sources

This guide was built from IRS guidance, FDA compounding policy, FDA warning letter records, current provider payment pages, and public provider help-center documentation reviewed on May 11, 2026. Reddit and forum comments were used only to identify common reader concerns and language — never as medical, tax, or regulatory evidence.

What we verified (May 11, 2026)

- IRS rules on prescribed medicines and disease-related weight-loss treatment.

- 2026 FSA limits via IRS Rev. Proc. 2025-32; 2026 HSA limits via IRS Rev. Proc. 2025-19.

- FDA position on compounded semaglutide (shortage resolution Feb 2025; 503A end Apr 2025; 503B end May 2025; proposed bulks-list exclusion Apr 30, 2026).

- FDA published concerns about dosing errors, refrigeration during shipping, salt forms, and adverse-event reports.

- September 9, 2025 FDA warning letter to DirectMeds; September 16, 2025 wave of 55+ warning letters; February 20, 2026 FDA warning letter #721455 to MEDVi; March 2026 wave of 30+ letters.

- Embody, SHED, MyStart Health, DirectMeds, Enhance.MD, Hers, and Ro: public payment-page language as of the verification date.

What we did NOT verify

- Live FSA card processing at any specific provider (depends on your card issuer and merchant).

- Approval by any specific FSA plan administrator (varies by employer).

- State-by-state availability for every provider on every formulation.

- Whether MEDVi or DirectMeds have publicly resolved their FDA warning letters as of publication.

Update log. Published May 11, 2026. Last verified May 11, 2026. We re-verify monthly during active FDA rulemaking on compounded GLP-1s; quarterly afterward.

About The RX Index. The RX Index is a pricing intelligence and comparison resource for GLP-1 telehealth providers. We don't sell medication. We compare what's publicly available, verify it on the dates we publish, and tell you what we couldn't confirm. Editorial standards · Methodology.

Primary sources

- IRS Publication 502 (2025) — Medical and Dental Expenses

- IRS Topic 502 — Medical and Dental Expenses

- IRS FAQ — medical expenses related to nutrition, wellness, and general health (2023)

- IRS Revenue Procedure 2025-19 (2026 HSA contribution limits)

- IRS Revenue Procedure 2025-32 (2026 Health FSA limits)

- FDA — "FDA clarifies policies for compounders as national GLP-1 supply begins to stabilize"

- FDA — "FDA's Concerns with Unapproved GLP-1 Drugs Used for Weight Loss"

- FDA Warning Letter to DirectMeds (09/09/2025)

- FDA Warning Letter #721455 to MEDVi, LLC (02/20/2026)

- FDA Press Announcement — "FDA Warns 30 Telehealth Companies Against Illegal Marketing of Compounded GLP-1s" (Mar 2026)

- FDA proposed rule — exclusion of semaglutide from 503B bulks list (Apr 30, 2026)

- Outsourcing Facilities Association v. FDA, 4:25-cv-00174 (N.D. Tex.)

- FSAFEDS Letter of Medical Necessity reference form

Still not sure which GLP-1 program is right for you?

60 seconds. No signup. We send back a personalized path based on your account type, diagnosis, state, and budget.

Get your personalized GLP-1 action plan →60 seconds. No signup. Free.

Your situation changes the answer

Find My GLP-1 Path

The right GLP-1 provider isn't the same for everyone. It depends on your state, your insurance and formulary, whether you want an FDA-approved or compounded medication, your preferred route (injection or oral), and your budget. Because a general answer can't resolve those for you, use The RX Index's Find My GLP-1 Path tool to get a personalized provider match with source-verified pricing before you choose.

- What it asks: your state, insurance situation, medication preference, budget, and support needs

- What you get: a personalized shortlist of GLP-1 providers matched to your situation, with verified pricing and the right questions to ask

- Cost: free · about 60 seconds · no signup