Does Insurance Cover GLP-1? Your 2026 Plan-by-Plan Guide to Wegovy, Zepbound, and Medicare Coverage

Does insurance cover GLP-1? Yes — sometimes — and the answer flips depending on what you’re treating, not just which drug you’re on. In 2026, most U.S. insurance plans cover GLP-1 medications when prescribed for type 2 diabetes, cardiovascular risk reduction, or moderate-to-severe sleep apnea. Coverage for weight loss alone (Wegovy, Zepbound, Foundayo, Saxenda) is far narrower, and it tightened on January 1, 2026 — several major plans dropped or restricted weight-loss GLP-1 coverage on that date.

Coverage by plan type at a glance

| Your plan | Bottom line | Best next step |

|---|---|---|

| Commercial / employer | About 1 in 5 large-employer plans cover GLP-1s for weight loss; nearly all require prior authorization. | Run a free coverage check. |

| Medicare Part D | The Medicare GLP-1 Bridge starts July 1, 2026 with a $50 monthly copay — now extended through December 31, 2027. | Confirm Bridge eligibility with your prescriber. |

| Medicaid (fee-for-service) | 13 states cover GLP-1s for obesity. California, New Hampshire, Pennsylvania, and South Carolina eliminated coverage January 1, 2026. | Check your state’s Preferred Drug List. |

| Marketplace / ACA | Coverage for weight-loss GLP-1s is rare. KFF found Wegovy was covered by only 1% of Marketplace prescription drug plans in 2024. | Read your plan’s formulary before enrolling. |

| No coverage at all | FDA-approved oral GLP-1 cash-pay options now start at $149/month; injection options start at $199–$349/month. | Compare verified manufacturer-direct paths. |

Breaking update — April 21, 2026

CMS announced that the BALANCE Model is not launching in Medicare Part D in 2027 as originally planned. The Medicare GLP-1 Bridge has been extended through December 31, 2027 instead. Most coverage guides still say “Bridge ends December 2026” and “BALANCE takes over in 2027.” Both are now outdated. We cover what actually changed below.

Free coverage check

Want a personalized answer for your exact plan?

Ro’s GLP-1 Insurance Coverage Checker has specialists call your insurer for you and email you a personalized report with copay estimates and prior-authorization details. No Ro membership required.

Check your GLP-1 coverage on Ro for free → (sponsored affiliate link, opens in a new tab)Ro is one of our affiliate partners. Using our link doesn’t change your price.

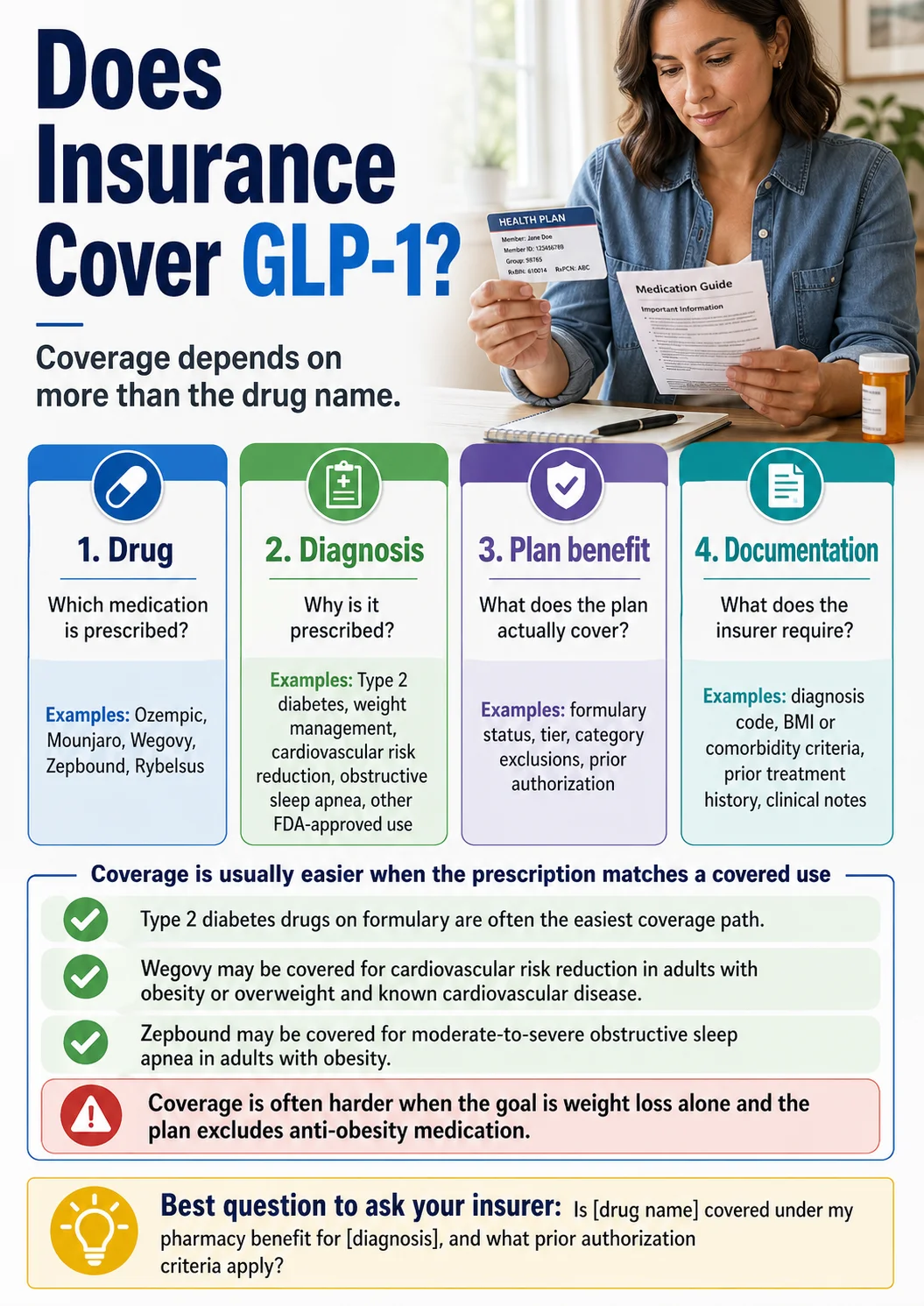

Does insurance cover GLP-1 medications? The four levers that decide

Coverage isn’t decided by the drug. It’s decided by four things working together. Most readers ask “does my insurance cover Wegovy?” and walk away with a confused answer because the question itself is too narrow. The same drug, prescribed for a different reason, on a different plan, with different documentation, gets a completely different answer.

Drug + Diagnosis + Plan benefit + Documentation = Real coverage

Change any one and the answer can flip from “$25 copay” to “$1,349 retail.”

Two coworkers can both have BCBS, both ask for Wegovy, and get opposite answers — because their employers picked different formularies, or because one prescription supports an additional indication that the other doesn’t.

So the question to ask isn’t “do you cover GLP-1?” The question is:

“Do you cover [specific drug] under my pharmacy benefit for [specific diagnosis], and what prior authorization criteria apply?”

That single rephrase will unlock more useful answers from your insurer than anything else on this page.

1. Drug

Same molecule, different label, different coverage. Ozempic (semaglutide) is FDA-approved for type 2 diabetes — widely covered. Wegovy is also semaglutide, but FDA-approved for chronic weight management and cardiovascular risk reduction — much lower coverage rates for weight loss alone. Same story for tirzepatide: Mounjaro for diabetes is widely covered; Zepbound for obesity often is not.

2. Diagnosis

Wegovy prescribed only for “obesity” may be denied. The same Wegovy, where the patient also has established cardiovascular disease, prescribed for “cardiovascular risk reduction in an adult with established CVD and overweight,” may be approved through standard Part D and most commercial plans. The drug doesn’t change. The clinical picture you and your prescriber document does.

3. Plan benefit

Your plan sponsor (the employer) chooses the formulary. The insurer just administers it. That’s why Mass General Brigham Health Plan, Health New England, BCBS of Massachusetts, and Fallon Health all dropped weight-loss GLP-1 coverage on January 1, 2026 — those weren’t insurer-wide decisions, they were plan-design decisions. Your booklet always overrides any general “BCBS covers it / doesn’t” article you read online.

4. Documentation

Many denials aren’t denials of eligibility — they’re denials of paperwork. The right ICD-10 codes, supporting labs, and a clean Letter of Medical Necessity will overturn a meaningful share of first-pass denials.

(sponsored affiliate link, opens in a new tab)

(sponsored affiliate link, opens in a new tab)Which GLP-1 medications are most likely to be covered

The drugs most likely to be covered depend on the diagnosis, not the brand alone. Diabetes-labeled GLP-1s tend to be covered for type 2 diabetes. Obesity-labeled drugs tend to be covered only when the plan includes anti-obesity medications, or when the prescription matches a non-weight-loss FDA-approved use.

| Medication | Active ingredient | What it’s FDA-approved for | Coverage reality in 2026 |

|---|---|---|---|

| Ozempic | Semaglutide | Type 2 diabetes; reducing risk of major cardiovascular events in adults with T2D and known CVD; reducing risk of kidney disease progression in adults with T2D and CKD | Widely covered for T2D. Off-label weight-loss requests are commonly denied. |

| Mounjaro | Tirzepatide | Type 2 diabetes | Widely covered for T2D. Weight-loss intent typically routes to Zepbound. |

| Wegovy (injection + pill) | Semaglutide | Chronic weight management; reducing cardiovascular event risk in adults with established CVD and obesity or overweight; Wegovy injection also approved for MASH with moderate-to-advanced liver fibrosis (Aug 2025) | Coverage for obesity alone is patchy. Coverage for CV risk reduction is much more common. |

| Zepbound (pen + KwikPen + vial) | Tirzepatide | Chronic weight management; moderate-to-severe obstructive sleep apnea in adults with obesity (added Dec 2024) | Coverage for obesity alone is patchy. Coverage for OSA is more accessible — and often the path that wins. |

| Foundayo | Orforglipron | Chronic weight management (FDA-approved April 2026 — first oral non-peptide GLP-1) | Newest FDA-approved GLP-1. Included in CMS’s Medicare Bridge eligible-drug list as of April 6, 2026. Commercial coverage still forming. |

| Rybelsus | Semaglutide (oral) | Type 2 diabetes | Covered for T2D. Not for weight loss. |

| Saxenda | Liraglutide | Chronic weight management (and pediatric obesity 12+) | Older obesity option. Coverage limited. |

| Trulicity, Bydureon, Victoza, Byetta | Various GLP-1s | Type 2 diabetes | Covered for T2D where on formulary. |

What qualifies you for GLP-1 insurance coverage?

Plan qualification depends on diagnosis, FDA-approved use, BMI and comorbidity criteria, formulary placement, prior authorization rules, and supporting documentation. No single number qualifies you on its own.

For weight-loss coverage (Wegovy, Zepbound, Foundayo, Saxenda):

- BMI ≥ 30, or BMI ≥ 27 with at least one weight-related comorbidity (type 2 diabetes, hypertension, dyslipidemia, established cardiovascular disease, obstructive sleep apnea, PCOS — exact list varies by plan)

- Documented prior attempts at lifestyle modification (some plans require 6+ months)

- Step therapy: some plans require a documented trial of phentermine, metformin, or naltrexone-bupropion before a GLP-1

- Reauthorization criteria: many plans require documented response (5%+ weight loss at 6 months) to renew approval

For diabetes coverage (Ozempic, Mounjaro, Trulicity, Rybelsus, Victoza):

- A type 2 diabetes diagnosis (ICD-10 E11.x)

- A1C threshold or other glycemic criterion (varies by plan)

- Step therapy: many plans require metformin first

- Plan formulary placement (preferred vs non-preferred tier affects copay)

For Medicare Bridge coverage:

The Medicare GLP-1 Bridge has its own three-tier eligibility structure that’s stricter and more specific than commercial-plan rules. See the Medicare section below — don’t assume commercial PA criteria apply.

The fastest way to know whether you qualify for your specific plan:

See if you qualify on your specific plan — free check on Ro → (sponsored affiliate link, opens in a new tab)Does private (commercial / employer) insurance cover GLP-1 in 2026?

Sometimes — and 2026 has been a tougher year, not a better one. Per KFF’s 2025 Employer Health Benefits Survey, about 19% of large firms (200+ workers) covered GLP-1s for weight loss; 57% did not, and 24% were unsure. Coverage was more common at very large employers — roughly 43% of firms with 5,000+ workers included weight-loss GLP-1 coverage. Among firms that covered them, about a third required participation in a dietitian, case manager, therapy, or lifestyle program.

Several plan-level changes hit in early 2026:

- Mass General Brigham Health Plan dropped GLP-1 coverage for weight management for fully insured commercial members on January 1, 2026. Coverage continues for type 2 diabetes.

- Health New England dropped Saxenda, Wegovy, and Zepbound coverage for weight loss on January 1, 2026.

- Blue Cross Blue Shield of Massachusetts announced GLP-1 coverage except for type 2 diabetes ends upon plan renewal starting January 1, 2026.

- Fallon Health Community Care plans no longer cover weight-loss medications as of January 1, 2026.

- CVS Caremark removed Zepbound from its standard formulary on July 1, 2025 in favor of Wegovy and Saxenda. Employers can still negotiate custom coverage.

2026 commercial-insurer landscape (verified examples)

| Insurer / PBM | What we verified | Source basis |

|---|---|---|

| Mass General Brigham Health Plan | Dropped GLP-1 weight-management coverage for fully insured commercial members effective January 1, 2026; T2D coverage continues | MGB Health Plan official |

| Health New England | Dropped Saxenda, Wegovy, and Zepbound weight-loss coverage in 2026 | Health New England official |

| BCBS of Massachusetts | GLP-1 coverage except for T2D ends upon plan renewal in 2026 | BCBSMA official |

| Fallon Health | Community Care plans dropped weight-loss coverage January 1, 2026 | Find Honest Care 2026 tracker |

| CVS Caremark (PBM) | Removed Zepbound from standard formulary July 1, 2025; prefers Wegovy and Saxenda; employers can override with custom coverage | AP News, July 2025 |

| Aetna | Plan-design dependent; employers can customize to include or exclude GLP-1 weight-management coverage; PA used for cost management | Aetna employer/sponsor documentation |

| Cigna | Evernorth/Cigna previously introduced a pharmacy-benefit approach that could cap out-of-pocket costs around $200/month for participating plans; not all members | Reuters, September 2025 |

| BCBS plans (other states) | Many plans removed default weight-loss GLP-1 coverage in 2026 absent an employer rider | Multiple plan policy bulletins |

| UnitedHealthcare, Humana, Kaiser, Express Scripts, OptumRx | Plan-by-plan; verify your specific plan booklet — we did not confirm a 2026 default coverage stance for these insurers across all states | — |

The honest read: the brand on the front of your insurance card matters less than what your plan booklet says. Two BCBS plans can be a world apart. Two UnitedHealthcare plans can be a world apart. The only reliable answer is the one your specific plan documents give you.

Ro’s coverage checker calls your insurer directly and emails you a personalized coverage report. Free, no Ro membership required.

Does Medicare cover GLP-1 in 2026? (The Bridge was just extended through 2027)

Medicare can cover GLP-1s through two distinct paths. Standard Part D may cover GLP-1s for FDA-approved or otherwise coverable non-weight-loss uses — for example, Zepbound for moderate-to-severe OSA and Wegovy for cardiovascular risk reduction are typically handled through standard Part D, not the Bridge. The newer Medicare GLP-1 Bridge — a temporary nationwide demonstration starting July 1, 2026 — covers Wegovy, Zepbound (KwikPen), and Foundayo for obesity at a $50 monthly copay for eligible Part D enrollees.

What changed on April 21, 2026

The original plan was a two-step rollout: Bridge runs July–December 2026, then the BALANCE Model takes over in Medicare Part D in 2027. That’s not what’s happening anymore. CMS confirmed:

- The BALANCE Model will NOT launch in Medicare Part D in 2027 as originally planned.

- The Medicare GLP-1 Bridge has been extended through December 31, 2027, keeping the $50 copay path available for an additional 12 months.

- The Medicaid side of BALANCE is still on schedule — state Medicaid agencies can apply through July 31, 2026.

Source: CMS HPMS memo April 21, 2026; CMS Medicare GLP-1 Bridge program page; KFF brief on the BALANCE Model; AHA News; Avalere Health Advisory. Rechecked April 28, 2026.

Are you eligible for the Bridge?

CMS published three distinct eligibility tiers. The provider must attest the drug is prescribed for excess body weight reduction, the beneficiary must be 18 or older, and must meet one of:

Tier 1 — BMI ≥ 35

No comorbidity required.

Tier 2 — BMI ≥ 30 with one or more of:

- Heart failure with preserved ejection fraction (HFpEF)

- Uncontrolled hypertension on two or more medications

- Chronic kidney disease, stage 3a or greater

Tier 3 — BMI ≥ 27 with one or more of:

- Prediabetes (per ADA guidelines)

- Previous myocardial infarction

- Previous stroke

- Symptomatic peripheral artery disease

Which drugs are Bridge-eligible

| Drug | Bridge eligible? | Notes |

|---|---|---|

| Foundayo | Yes — all formulations | Added April 6, 2026 |

| Wegovy | Yes — all formulations (injection + tablets) | Confirmed April 6, 2026 |

| Zepbound | KwikPen formulation ONLY | Single-dose vials and pens are NOT eligible. Need a KwikPen prescription for $50 access. |

The fine print most pages skip

- The $50 Bridge copay does NOT count toward your Part D deductible, TrOOP, or annual out-of-pocket cap.

- Low-Income Subsidy (LIS) cannot be applied to the $50 Bridge copay — the program operates outside the standard Part D benefit.

- Pharmacies and Part D plans don’t need to opt in. CMS is running this through Humana as the nationwide central processor.

- Coupons and manufacturer copay cards generally cannot be combined with Bridge pricing.

Medicare coverage outside the Bridge

You may not need the Bridge at all. Standard Part D may cover:

- GLP-1s for type 2 diabetes: Ozempic, Mounjaro, Trulicity, Rybelsus, Bydureon, Victoza, Byetta — subject to plan formulary, often with PA.

- Wegovy injection for cardiovascular risk reduction in adults with established CV disease and obesity or overweight — through standard Part D as a non-weight-loss indication.

- Zepbound for moderate-to-severe OSA in adults with obesity — through standard Part D.

- Wegovy injection for MASH with moderate-to-advanced liver fibrosis — covered through standard Part D since the August 2025 FDA approval.

Does Medicaid cover GLP-1? It depends on your state

Medicaid coverage of GLP-1s for weight loss is state-by-state, and the trend in 2026 was contraction, not expansion. As of January 2026, 13 state Medicaid programs cover GLP-1s for obesity under fee-for-service — down from 16 in October 2025, after California, New Hampshire, Pennsylvania, and South Carolina eliminated coverage. KFF says Medicaid coverage is required for drugs prescribed for medically accepted indications such as diabetes, certain cardiovascular uses, and OSA — while obesity-treatment coverage remains optional for states.

What changed in late 2025 and early 2026

- California (Medi-Cal) eliminated GLP-1 weight-loss coverage for adults 21+ effective January 1, 2026. Wegovy, Zepbound, and Saxenda were removed from the Medi-Cal Rx Contract Drugs List for weight-loss indications.

- Pennsylvania eliminated obesity-treatment coverage of GLP-1s effective January 1, 2026, citing the rise in GLP-1 prescription spending from $223M in 2022 to $650M in 2024. Coverage continues for type 2 diabetes and other medically-accepted indications.

- New Hampshire and South Carolina also eliminated weight-loss GLP-1 coverage in late 2025 / early 2026.

- North Carolina briefly eliminated coverage in October 2025 due to a state budget stalemate, then reinstated it in December 2025. NC is back on the “covering” list as of January 2026.

- Michigan issued updated pharmacy guidance restricting GLP-1 coverage for weight loss with transition rules for existing patients. Verify against the current MDHHS pharmacy bulletin.

If your state isn’t covering, you still have three real paths

- Medically accepted indication coverage. If your prescription is for type 2 diabetes (Ozempic, Mounjaro, Rybelsus), cardiovascular risk reduction (Wegovy injection), or OSA (Zepbound), Medicaid generally covers it.

- Manufacturer patient assistance programs. Novo Nordisk’s PAP and Eli Lilly’s PAP both provide free or reduced-cost medication for income-qualifying patients.

- Cash-pay routes. 2026 prices are dramatically lower than they were two years ago. FDA-approved oral GLP-1s now start at $149/month.

Does Marketplace, TRICARE, VA, or IHS coverage include GLP-1?

Coverage in these buckets is the most variable and the most often misunderstood.

Marketplace (ACA) plans

Coverage for weight-loss GLP-1s is rare on individual-market plans. KFF previously found Wegovy was covered by only 1% of Marketplace prescription drug plans in 2024. Weight-loss medications are not an Essential Health Benefit requirement under the ACA, so they’re typically excluded. Your best move before enrolling: use the formulary tab on healthcare.gov to search for the specific drug you’re considering.

TRICARE

TRICARE covers certain weight-loss drugs including Wegovy, Saxenda, and Zepbound when plan-specific criteria are met, with revised PA criteria. TRICARE For Life and certain other beneficiary groups are not eligible for weight-loss-drug coverage. Verify your eligibility class and current TRICARE formulary before assuming.

VA (Veterans Affairs)

Access is product- and criteria-driven. Verify the exact product through VA Formulary Advisor and with the veteran’s VA pharmacy or primary-care team. Wegovy weight-management access may require non-formulary or prior-approval steps. See our full VA GLP-1 coverage guide for the complete 2026 criteria.

IHS (Indian Health Service)

Access is facility- and formulary-driven. Verify through the local IHS pharmacy or facility formulary.

Why was my GLP-1 denied? The denial-letter decoder

A denial isn’t always a “no” — it’s often a “not yet, with this paperwork.” Per KFF Marketplace data, fewer than 1% of denied claims are ever appealed, and when they are, insurers upheld about 66% of denials — meaning roughly one in three appealed denials are overturned in the patient’s favor. The math is on your side if you actually file.

| What your denial says | What it usually means | Fixable? | What to do next |

|---|---|---|---|

| “Prior authorization required” | Your insurer wants documentation before deciding. This isn’t a denial yet. | Often, yes. | Ask for the exact PA criteria. Have your prescriber submit BMI, ICD-10 codes, comorbidities, prior treatments, and required labs. |

| “Criteria not met” | The submitted documentation didn’t match the plan’s rules. | Often, yes. | Ask which specific criterion failed: BMI threshold, diagnosis, comorbidity, step therapy, or lifestyle program. Resubmit only the missing piece. |

| “Not medically necessary” | The plan disagrees that the drug is necessary under its policy. | Sometimes. | Ask for the policy basis. Request a peer-to-peer review where your prescriber speaks directly with the plan’s reviewing clinician. |

| “Not on formulary” | The drug isn’t preferred or listed on your plan. | Sometimes. | Ask whether there’s a preferred alternative covered. If you medically need this specific drug, request a formulary exception with documentation. |

| “Forced switch” (e.g., “We prefer Wegovy”) | The plan covers a different GLP-1 than the one prescribed. | Often. | Document why the alternative won’t work — prior failure, side effects, or clinical differentiation (Zepbound is dual GIP/GLP-1; Wegovy is GLP-1 only). |

| “Weight-loss medications excluded” | Your plan excludes the entire category of anti-obesity medications. | Harder. | Confirm the exclusion in writing. If employer-sponsored, escalate to HR. Consider whether a non-weight-loss FDA-approved indication applies to your clinical picture. |

| “Coverage stopped after weight loss” | Reauthorization criteria require documented ongoing response. | Sometimes. | Ask what continuation criteria apply. Your prescriber can often document maintenance need. |

The most important distinction: prior authorization denial (criteria can be met with paperwork) vs. a plan exclusion (the benefit doesn’t exist). Internal appeals work great for the first; they rarely overturn the second.

For a deeper, denial-type-specific appeal walkthrough, see our How to get insurance to cover GLP-1 tactical guide.

How to get prior authorization approved on the first try

Many fixable denials happen because the file is incomplete, not because the patient is ineligible. A clean PA submission generally needs five things — exact requirements vary by plan, so always confirm your insurer’s specific criteria first.

- 1Recent BMI documentation. Many plans require recent BMI/weight documentation (some require two measurements 30+ days apart, both within the last 90 days). Ask your insurer their specific rule.

- 2ICD-10 diagnosis codes. Not just “obesity” — the actual code, plus comorbidity codes (E11 for type 2 diabetes, I10 for hypertension, E78 for dyslipidemia, G47.33 for OSA, etc.). Plain text in the chart doesn’t trigger automated approvals; codes do.

- 3Supporting labs. A1C for diabetes/prediabetes, lipid panel for dyslipidemia, sleep study for OSA, CMP, TSH, and (for women of childbearing age) a pregnancy test.

- 4A real Letter of Medical Necessity. Not a template with your name dropped in. The LMN should address: why GLP-1 is appropriate, expected benefit beyond weight loss alone, why alternatives are insufficient or were tried, and the monitoring plan.

- 5The right drug on the formulary tier the plan prefers. If the plan prefers Wegovy, the preferred option may be easier than fighting a forced switch. If you medically need Zepbound (OSA, prior semaglutide failure), document that and request the exception.

Don’t want to manage this yourself?

Ro’s insurance concierge handles benefit verification, PA submission, and appeals as part of the Ro Body membership. Per Ro’s own coverage checker report: about 43% of users had coverage for GLP-1 weight-loss treatment, nearly 70% of covered patients pay less than $100/month in copay, and over half pay $50/month or less. The PA process typically takes about 2–3 weeks. Ro Body is $39 for the first month, then as low as $74/month with annual prepay.

Let Ro’s insurance concierge fight the prior auth for you → (sponsored affiliate link, opens in a new tab)How much does a GLP-1 cost with insurance — and without?

With coverage, your out-of-pocket cost can be as low as $25/month. Without it, FDA-approved cash-pay options now start at $149/month for oral GLP-1s and $199–$349/month for injection options. The cash-pay landscape changed dramatically in late 2025 and early 2026 — and it’s the single biggest piece of news that hasn’t fully reached people who got priced out two years ago.

$25/mo

With commercial insurance + manufacturer savings card (Wegovy or Zepbound)

$50/mo

Medicare GLP-1 Bridge for eligible Part D enrollees (extended through Dec 2027)

$149/mo

Cash-pay floor for FDA-approved oral GLP-1 (Wegovy pill or Foundayo, lowest dose)

2026 cash-pay price map (verified Feb–Apr 2026)

| Path | Wegovy injection | Wegovy pill | Zepbound vials | Zepbound KwikPen | Foundayo |

|---|---|---|---|---|---|

| Ro (cash-pay, FDA-approved) | $199–$349/mo by dose | $149–$299/mo by dose | $299–$499/mo by dose | $299–$499/mo with refill check-in | $149/mo (0.8 mg) – $299/mo by dose |

| NovoCare Pharmacy direct | $199–$349/mo by dose | $149–$299/mo by dose | n/a | n/a | n/a |

| LillyDirect / Lilly self-pay | n/a | n/a | $349 starter / $499 maintenance | $499/mo standard; $449/mo (7.5–15 mg with refill check-in) | $149 (0.8 mg) / $199 (2.5 mg) / $299 (5.5–17.2 mg with refill check-in) |

| TrumpRx (gov. cash-pay portal) | $199/mo (limited intro) – $349/mo standard | $149/mo (intro) | $299/mo | $299/mo | Catalog expanding — verify current page |

| Costco / Sesame member program | $199 for first two low-dose fills through December 31, 2026; then $349 for most doses | n/a | n/a | n/a | n/a |

| List price (no program) | ~$1,349/mo | ~$1,349/mo | ~$1,087/mo | ~$1,087/mo | Varies by dose |

When to use insurance vs cash-pay

Use insurance when: Your plan covers the drug, your manufacturer savings card brings it under $50/month, and prior authorization isn’t a six-month nightmare.

Use cash-pay when: Your plan excludes weight-loss medications outright, your post-savings-card price is over $200/month, you’re stuck in PA limbo, or you have a high deductible and the cash price is lower. Cash-pay GLP-1s prescribed for a documented medical condition are also HSA- and FSA-eligible, which effectively cuts the cost another 25–30%.

What if your plan flat-out excludes GLP-1s for weight loss?

A coverage checker can’t override a hard plan exclusion. If your employer-sponsored plan excludes anti-obesity medications as a category, no insurance concierge can force the plan to cover something it didn’t buy. Ro’s insurance concierge will fight a denial; it can’t rewrite a plan booklet. Pretending otherwise wastes your time.

If that’s where you are, you have four real options:

- Indication change. If your clinical picture supports it, your prescriber may be able to write the prescription for a covered indication: Wegovy injection for cardiovascular risk reduction in eligible patients, Zepbound for OSA, or Wegovy injection for MASH. This only works if you actually have one of these conditions and your prescriber documents it truthfully.

- HR escalation. Your employer can add a weight-management rider at next plan-year renewal. The HR ask: “Does our plan exclude anti-obesity medications entirely, or is there a path to coverage with documentation?”

- Plan switch at open enrollment. Look for “anti-obesity medication coverage” or “weight management benefit” in the SBC.

- Cash-pay. With Wegovy pill at $149–$299/month and Foundayo starting at $149/month, the cash-pay route is no longer the financial cliff it was in 2024.

Ro — primary recommendation for plan-exclusion cases

If cash-pay is the route, Ro is our primary recommendation because their pricing matches LillyDirect and NovoCare directly, and you get bundled monthly provider check-ins, dose adjustments, and a single platform. Ro carries FDA-approved options including Foundayo, Wegovy, and Zepbound. $39 for the first month, then as low as $74/month with annual prepay. Medication billed separately.

See if Ro’s bundled cash-pay GLP-1 program fits you → (sponsored affiliate link, opens in a new tab)Sesame Care — broad formulary, Costco-member pricing

If you want maximum provider choice and the option to use a Costco-member price, Sesame Care is the secondary FDA-approved cash-pay option. Sesame’s marketplace covers the broadest branded formulary (Wegovy, Zepbound, Ozempic, Mounjaro, Foundayo, Saxenda).

Compare cash-pay GLP-1 options on Sesame Care → (sponsored affiliate link, opens in a new tab)Are compounded GLP-1 medications covered by insurance?

No, in nearly every case. Compounded GLP-1 preparations are not on insurer formularies, and they are not FDA-approved finished products. Insurance pays for FDA-approved drugs on the plan’s formulary; that excludes compounded preparations as a category.

Two practical points:

- Insurance won’t pay for compounded GLP-1s. If insurance coverage is your priority, compounded is not your path.

- Compounded GLP-1s may be HSA/FSA-eligible when prescribed by a licensed provider for a diagnosed medical condition. Confirm with your plan administrator.

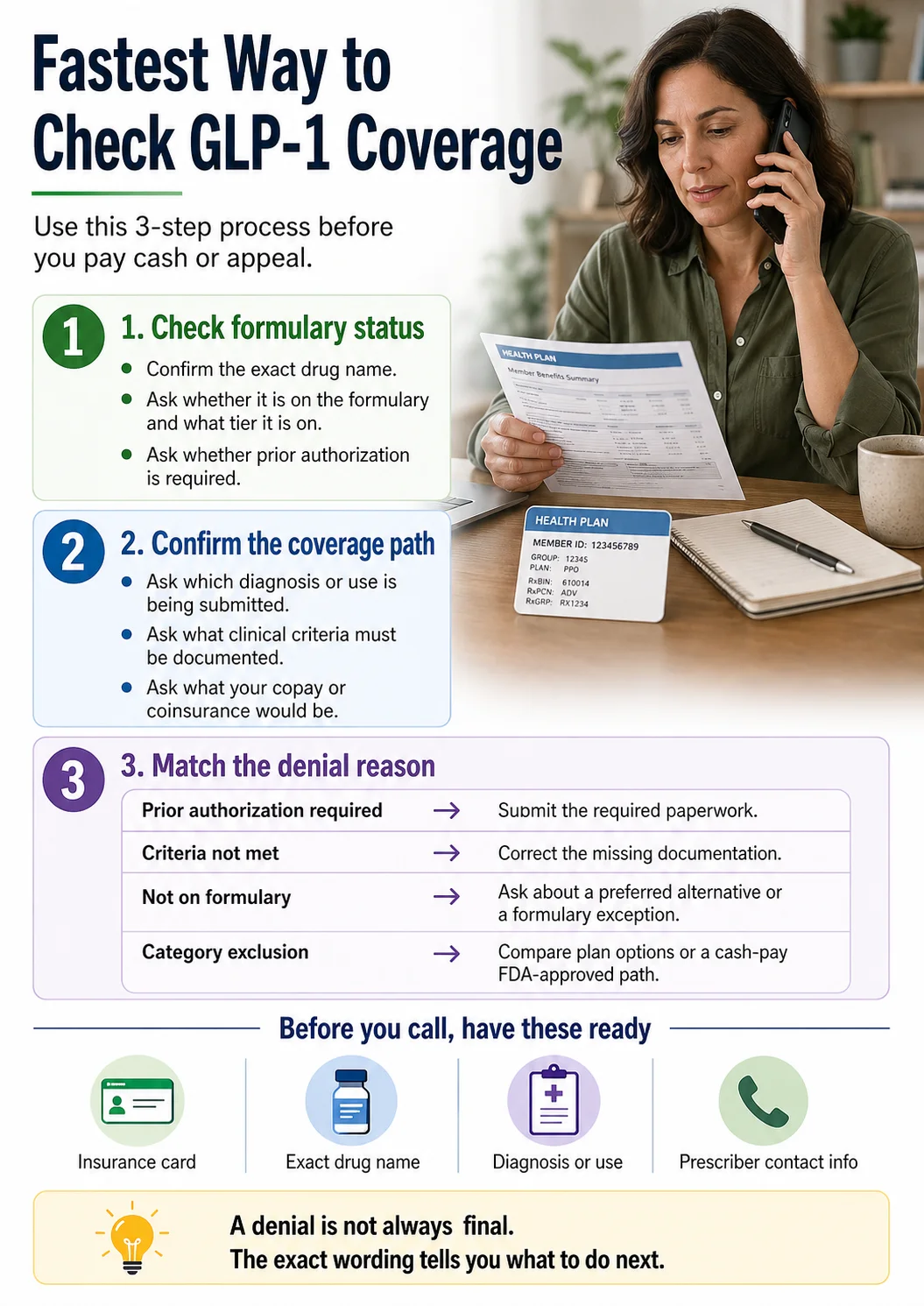

The fastest way to find out if your specific plan covers GLP-1

Three options, in order of speed. Most people overcomplicate this and waste a week.

(sponsored affiliate link, opens in a new tab)

(sponsored affiliate link, opens in a new tab)Option 1: Use a free coverage checker (fastest)

Ro’s GLP-1 Insurance Coverage Checker is the cleanest version of this tool publicly available. You enter your insurance card information, Ro’s specialists call your plan, and Ro emails you a personalized report with tier, PA requirements, copay estimates, and next steps. Free, no Ro membership required.

Run Ro’s free GLP-1 Insurance Coverage Checker → (sponsored affiliate link, opens in a new tab)Option 2: Call your insurer with the right script

Call the member services number on the back of your insurance card and ask specifically for the pharmacy benefit team. The script:

“Hi, I’m calling to ask whether [exact drug name] is covered under my pharmacy benefit for [diagnosis or use]. Specifically:

- Is it on the formulary, and which tier?

- Is prior authorization required? If so, what specific criteria does my prescriber need to document?

- Are weight-loss medications excluded from my plan as a category? If yes, please send me that exclusion in writing.

- What would my copay or coinsurance be — before deductible, and after?

- If denied, what’s the appeals process, and how do I request a peer-to-peer review?”

Option 3: Ask your prescriber before the prescription is submitted

Before your prescriber writes the prescription:

- “Which diagnosis are you submitting?” (This affects coverage more than the drug name.)

- “Which drug best matches my diagnosis and my plan’s preferred formulary?”

- “Does your office handle prior authorization, or do I need to chase that?”

- “What happens if it’s denied — do you do peer-to-peer reviews?”

- “How do reauthorization renewals work?”

HSA, FSA, and GLP-1: what’s eligible, what gets denied

GLP-1 medications prescribed by a licensed provider for a diagnosed medical condition are generally HSA- and FSA-eligible. This includes Wegovy, Zepbound, Ozempic, Mounjaro, Rybelsus, Saxenda, and Foundayo. The IRS standard from Publication 502: the cost of “diagnosis, cure, mitigation, treatment, or prevention of disease” is a qualified medical expense. This is not tax advice — keep your receipts and confirm with your HSA/FSA administrator.

- HSAs generally don’t require additional documentation at checkout. Save your receipts and the LMN if your provider issued one.

- FSAs more often require a Letter of Medical Necessity, especially for weight-loss prescriptions. Get one proactively.

- Compounded GLP-1s may be reimbursable when prescribed for a diagnosed medical condition. Confirm with your FSA/HSA administrator before assuming.

- Stacking HSA/FSA + cash-pay is the most underused win here. A $299/month Wegovy pill paid through an HSA at a 25% effective tax bracket is a real cost of about $224/month — not far off the $50 Bridge copay.

Frequently asked questions about GLP-1 insurance coverage

Does insurance cover GLP-1 for weight loss?

Does insurance cover GLP-1 for type 2 diabetes?

Does insurance cover Ozempic for weight loss?

Does insurance cover Wegovy?

Does insurance cover Zepbound?

Does insurance cover Foundayo?

Does Medicare cover GLP-1 in 2026?

Does Medicaid cover GLP-1?

What qualifies you for GLP-1 insurance coverage?

What BMI do you need for GLP-1 coverage?

Why did my insurance deny my GLP-1?

Why did my insurance stop covering my GLP-1 after I lost weight?

Can my employer override a GLP-1 exclusion?

Are compounded GLP-1 medications covered by insurance?

Can I use HSA or FSA if insurance doesn't cover GLP-1?

How long does GLP-1 prior authorization take?

Is Ro's GLP-1 Insurance Coverage Checker free?

What's the cheapest legal way to get Wegovy in 2026?

Will the BALANCE Model still launch in Medicare Part D?

Is the Medicaid side of BALANCE still on track?

What we actually verified for this guide

Health and insurance content moves fast. Transparency is a requirement on this page.

Verified directly from primary or high-authority sources:

- Medicare GLP-1 Bridge timeline, three-tier eligibility criteria, eligible drugs, copay rules, and the April 21, 2026 extension — CMS Medicare GLP-1 Bridge program page, CMS HPMS memo, confirmed by KFF, AHA News, and Avalere Health Advisory.

- Medicaid covering-state count (13) and four states that eliminated coverage (CA, NH, PA, SC) — KFF’s “Medicaid Coverage of and Spending on GLP-1s” (January 2026).

- Employer coverage statistics (19% of large firms; 43% of firms with 5,000+; 34% requiring lifestyle programs) — KFF’s 2025 Employer Health Benefits Survey.

- Marketplace coverage rarity (1% Wegovy coverage in 2024) — KFF Marketplace coverage analysis.

- Appeals statistics (fewer than 1% appealed; 66% of appealed denials upheld) — KFF Marketplace claims and appeals data, 2024.

- Cash-pay prices for Wegovy, Zepbound, and Foundayo through NovoCare, LillyDirect, TrumpRx, Costco/Sesame, and Ro — verified against manufacturer/retailer pricing pages Feb–April 2026.

- Specific 2026 commercial-plan changes (Mass General Brigham, Health New England, BCBS of Massachusetts, Fallon Health) — verified against insurer official pages and Find Honest Care 2026 tracker.

What we did not verify (where you’d want to do your own check):

- Your individual plan’s formulary or exclusion language — only your plan documents or a coverage checker can answer this.

- 2026 default coverage stance for UnitedHealthcare, Humana, Kaiser Permanente, Express Scripts, and OptumRx across all states and plan types.

- State Medicaid managed-care plan policies — these vary by MCO within a state.

- Specific employer-plan riders, exceptions, or add-ons.

- 2026 TRICARE formulary detail at the plan-class level.

Last verified: . Next review: Quarterly and after significant CMS/OPM announcements. This page does not replace medical or insurance advice from a licensed provider or your plan administrator.

Why we built this page

The RX Index is a pricing intelligence and comparison resource for GLP-1 telehealth providers. We built this page because “does insurance cover GLP-1?” is the wrong question to walk into a pharmacy with. The right question is “does my plan cover this drug for this diagnosis, and what does the prior authorization need?” We laid out the answer by plan type, decoded the most common denial language, gave you the cash-pay map, and pointed you to free tools where they exist.

Your next step

Still not sure which path is right for you?

We’ll ask 6 questions about your insurance, BMI, comorbidities, and budget, and give you a personalized 1-page action plan with the next concrete step for your situation.

Take the free 60-second GLP-1 path quiz →