How to Get Foundayo Covered by Insurance in 2026

Published: · Last updated:

How to get Foundayo covered by insurance depends entirely on which lane you’re in — and most people get stuck at the pharmacy counter because nobody shows them the lanes. Short version: if you have commercial insurance that covers Foundayo, eligible patients can pay as low as $25 for a 1-, 2-, or 3-month fill using Lilly’s savings card. If your plan excludes weight-loss drugs, that $25 headline is not your lane, and self-pay through LillyDirect at $149–$349/month is your realistic floor. Below is the full playbook.

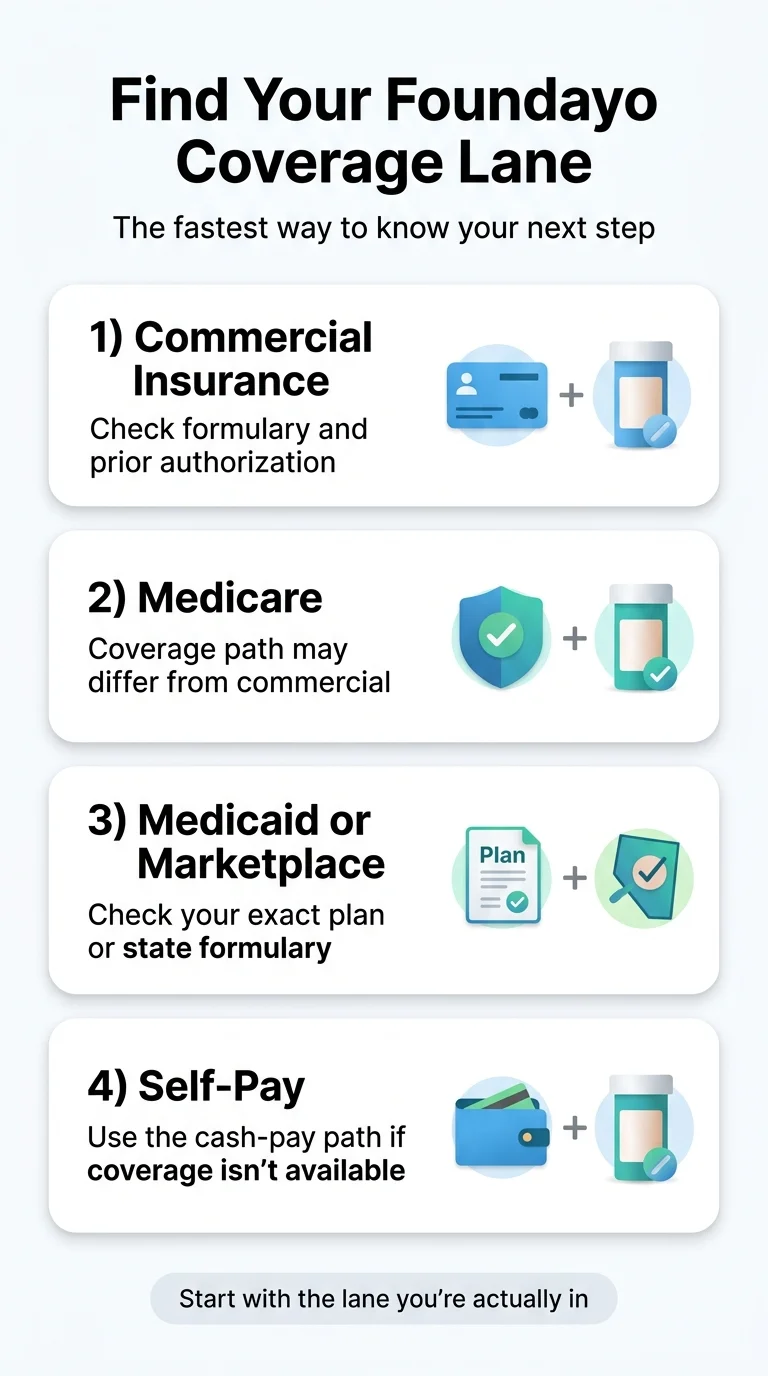

Pick your lane to see your next move:

- Commercial insurance or FEHB? → Check your Foundayo coverage free with Ro (sponsored affiliate link, opens in a new tab) (Ro calls your insurer; no charge; $50 credit for new Ro accounts)

- Medicare Part D? → Jump to the Medicare GLP-1 Bridge section

- Medicaid? → Jump to the Medicaid section

- TRICARE, VA, DoD, or IHS? → Jump to government non-Medicare plans

- Uninsured or paying cash? → Jump to LillyDirect self-pay

What changed in 2026 that makes this different from last year

Two things. First, Foundayo was FDA-approved on April 1, 2026 under the Commissioner’s National Priority Voucher Program — the first new molecular entity approved under that program, and one of the fastest NME approvals since 2002. It’s the only once-daily GLP-1 pill that can be taken at any time of day without food or water restrictions. That matters for coverage because when a drug is less than a month old, PBMs and state Medicaid programs haven’t finished writing their policies — some denials you receive today will resolve by late 2026 without you doing anything.

Second, on April 6, 2026, CMS updated the Medicare GLP-1 Bridge program to officially include Foundayo. That’s the specific rule change most pages haven’t caught up to yet. If you’re on Medicare Part D, a page written two weeks ago probably told you Foundayo wasn’t in the Bridge. As of April 6, it is — and the Bridge is available as of July 1, 2026.

The Foundayo Coverage Path Matrix — every insurance lane, every cost

This is the single table that answers most searches. Each row tells you what to realistically expect and what to do next. Updated monthly, and more often when Lilly, CMS, or major PBMs change terms.

| Your insurance situation | Realistic monthly cost | Savings card applies? | Next action |

|---|---|---|---|

| Commercial plan covers Foundayo + PA approved | As low as $25 per 1-, 2-, or 3-month fill | Yes — commercial tier | Activate card, fill |

| Commercial plan covers Foundayo + PA pending | As low as $25 once approved; $149+ if bridging self-pay | Yes once approved | Submit PA; consider LillyDirect bridge while waiting |

| Commercial covers weight-loss drugs but Foundayo off formulary | $149–$299 self-pay while appealing | Yes — self-pay tier | File a formulary exception |

| Commercial plan excludes weight-loss drugs entirely | $149–$349 LillyDirect self-pay | Yes — self-pay tier | Internal appeal is low-yield for category exclusions; consider self-pay or employer benefits conversation |

| FEHB (Federal Employee Health Benefits) | Depends on carrier | Plan-specific — verify at foundayo.lilly.com | Ro confirms FEHB support; Ro can coordinate the coverage check |

| Medicare Part D (standard — Bridge not applicable) | No coverage under standard Part D; $149–$349 self-pay | No (government insurance excluded) | Apply for Bridge (if eligible) or self-pay |

| Medicare Part D (July 1, 2026+) via GLP-1 Bridge | $50 copay | No (Bridge is a separate program) | Provider submits PA to CMS central processor, not Part D plan. TrOOP does not count. LIS does not apply. |

| Medicaid | Covered by ~13 state FFS programs for obesity (Jan 2026); excluded in most states | No | Check state preferred drug list |

| ACA Marketplace plan | Obesity-drug coverage is rare; varies by plan | Plan-specific | Pull exact formulary before assuming coverage |

| Uninsured / cash-pay | $149 / $199 / $299 via LillyDirect; $349 for 14.5 or 17.2 mg if refill >45 days | Yes — self-pay tier | No PA needed |

| TRICARE / VA / DoD / IHS | Varies by program and diagnosis; weight-loss coverage has narrowed | No | Check your specific plan’s formulary; self-pay is the fallback |

If you have commercial insurance that covers Foundayo

Answer capsule: If your commercial plan covers Foundayo, you’re in the as-low-as-$25-per-fill lane — assuming you clear prior authorization. Most commercial plans with GLP-1 coverage require PA for weight-loss drugs. Under federal rules for ACA-regulated plans, non-urgent PA decisions are generally made within 15 days and urgent requests within 72 hours.

Here’s what the covered path looks like, start to finish:

| # | Action | How |

|---|---|---|

| 1 | Confirm Foundayo is on your formulary | Log into your insurer’s member portal. Search “Foundayo” then “orforglipron.” Note coverage tier, PA requirement, and whether step therapy applies. |

| 2 | Your prescriber submits prior authorization | BMI, documented weight-related conditions, clinical rationale for Foundayo specifically. Full checklist in the PA section below. |

| 3 | PA gets approved | Standard: up to 15 days. Urgent: 72 hours. Ro reports its insurance-path averages 2–3 weeks end to end. |

| 4 | Activate the Foundayo Savings Card | foundayo.lilly.com/coverage-savings or 1-800-545-6962 |

| 5 | Fill at pharmacy — as low as $25 | Card covers up to $100/1-month fill, $200/2-month fill, $300/3-month fill. Cap: $1,000/year, 10 fills max, expires 12/31/2026. |

Covered path, FEHB path, or step-therapy workaround — end-to-end. $39 first month. (Partner link — does not change what you pay.)

If your commercial plan doesn’t cover Foundayo

Answer capsule: If your plan doesn’t cover Foundayo, the $25 headline doesn’t apply — but the savings card still drops your self-pay price to its self-pay tier: $149/month for 0.8 mg, $199/month for 2.5 mg, and $299/month for 5.5 mg, 9 mg, 14.5 mg, or 17.2 mg. There are two versions of this scenario, and the right move depends on which one you’re in.

What Foundayo actually costs — with insurance and without

Answer capsule: With commercial insurance that covers Foundayo, eligible patients pay as low as $25 per fill with the savings card (caps: $100/$200/$300 per fill, $1,000/year, 10 fills max, expires 12/31/2026). Without coverage, self-pay through LillyDirect is $149/$199/$299 depending on dose — the 14.5 mg and 17.2 mg doses rise to $349 if the 45-day refill window is missed. Medicare Bridge access starts July 1, 2026 at a $50 copay.

| Price tier | Monthly cost | Requirements |

|---|---|---|

| Commercial covered + savings card | As low as $25 per fill | Commercial insurance covering Foundayo + active card (10 fills/$1,000 cap, expires 12/31/2026) |

| Not covered, self-pay — 0.8 mg starter | $149 | Any insurance or uninsured; card self-pay tier |

| Not covered, self-pay — 2.5 mg | $199 | Card self-pay tier |

| Not covered, self-pay — 5.5 mg, 9 mg | $299 | Card self-pay tier; no 45-day refill constraint on these doses |

| Not covered, self-pay — 14.5 mg, 17.2 mg | $299 if refilled within 45 days; $349 if missed | Purchase-offer terms apply to these two doses only. Set a calendar reminder at day 30 and day 40 — missing the window costs $600/year. |

| Medicare GLP-1 Bridge (from July 1, 2026) | $50 copay | Eligible Medicare Part D plan + Bridge PA. Does not count toward TrOOP. LIS does not apply. |

If you’re on Medicare: how the GLP-1 Bridge changes your path on July 1, 2026

Answer capsule: Medicare Part D does not cover Foundayo today — federal law excludes weight-loss drugs from standard Part D coverage. That changes on July 1, 2026 via the CMS Medicare GLP-1 Bridge, which CMS updated on April 6, 2026 to officially include Foundayo. Eligible Part D beneficiaries will pay a $50 copay through Bridge PA requests submitted to a CMS central processor — not to their Part D plan. Per CMS, the Bridge copay does not count toward Part D TrOOP and LIS does not apply. The Bridge runs July 1, 2026–December 31, 2027 (18 months). BALANCE will not launch for Medicare Part D in 2027 — watch for BALANCE 2028 announcements during fall 2027 open enrollment.

Eligible Part D plan types for the Bridge

| Eligible for Bridge | Not eligible for Bridge |

|---|---|

| Standalone PDP · MA-PD (HMO, HMOPOS, Local PPO, Regional PPO) · Special Needs Plans (SNPs) · Employer/Union Group Waiver Plans (EGWPs) · LI NET | PACE · Private fee-for-service plans (unless also in a PDP) · Section 1876 cost contracts · Section 1833 health care prepayment plans · Fallback plans · Religious fraternal benefit plans |

Which GLP-1s are in the Bridge as of April 6, 2026

| Drug | Formulations in Bridge | Note |

|---|---|---|

| Foundayo (orforglipron) | All formulations | Added to Bridge on April 6, 2026 |

| Wegovy (semaglutide) | All formulations (injection and tablets) | — |

| Zepbound (tirzepatide) | KwikPen formulation only | Single-dose vials and single-dose pens are not in the Bridge. If you’re on Zepbound single-dose pens and expected the Bridge to cover your July 1 refill, it won’t. |

If you’re on Medicaid

Federal law treats weight-loss drugs as an optional coverage category for Medicaid. About 13 state fee-for-service Medicaid programs covered any GLP-1 for obesity as of January 2026 (KFF). Foundayo specifically wasn’t on any of the seven state Medicaid PDLs we checked. The commercial Foundayo Savings Card does not apply to Medicaid enrollees under federal anti-kickback law.

For the full Medicaid picture including state-by-state PDL status and the CMS BALANCE Model timeline, see: Does Medicaid Cover Foundayo? 7 States Checked →

TRICARE, VA, DoD, and IHS

TRICARE’s weight-loss drug coverage varies by diagnosis, medical necessity, and plan type. TRICARE Prime, Select, For Life, Reserve Select, and Young Adult all have different rules. VA and IHS coverage also varies significantly. The commercial Foundayo Savings Card does not apply to any of these programs.

- Check your specific plan’s formulary and PA rules directly — “TRICARE” is not one coverage category.

- If covered under your specific plan, work through that plan’s PA process.

- If not covered, LillyDirect self-pay at $149/month for the starter dose is the same floor available to everyone else.

ACA Marketplace plans

KFF’s analysis of Marketplace formularies found that obesity-drug coverage is rare, and plans that do cover weight-loss GLP-1s typically require prior authorization with strict clinical criteria. For Foundayo specifically, pull your exact plan’s formulary before assuming access. If you’re shopping 2027 Marketplace plans (open enrollment November 2026) and GLP-1 coverage matters to you, ask each plan whether Foundayo, Wegovy, and Zepbound are on the formulary and what tier and PA requirements apply — the difference in annual cost can be $3,000+.

What your doctor needs for prior authorization

Answer capsule: A Foundayo prior authorization packet almost always requires BMI (30+, or 27+ with a weight-related condition), documented comorbidities in the medical chart, evidence of prior lifestyle interventions, and a clinical rationale for Foundayo specifically. Under federal rules for ACA-regulated plans, PA decisions are generally made within 15 days (standard) and 72 hours (urgent). Complete documentation on the first submission is the single biggest lever to cut wait time.

| Category | What to include |

|---|---|

| Demographic & eligibility | Current BMI (measured height + weight at prescribing visit) · BMI history over last 12–24 months if available · Confirmation of no personal or family history of medullary thyroid carcinoma (MTC) or MEN2 syndrome (boxed warning contraindication in Foundayo’s FDA label) |

| Clinical justification | Documented weight-related comorbidities with ICD-10 codes: type 2 diabetes, prehypertension or hypertension, dyslipidemia, cardiovascular disease, obstructive sleep apnea, MASH/NAFLD, PCOS, osteoarthritis · Evidence of prior lifestyle interventions (reduced-calorie diet, structured physical activity, formal weight-management counseling, prior pharmacotherapy) · Weight trajectory despite lifestyle changes |

| Rationale for Foundayo specifically | If step therapy required: documented prior failure or intolerance of the preferred step agent (typically Wegovy or Zepbound) · If applicable: injection aversion, injection-site complications, clinical reasons an oral GLP-1 is preferred · If applicable: documented issues with oral semaglutide’s strict fasting/water restrictions (Foundayo has none — any time of day, no food or water restriction) |

The three provider paths ranked for this specific problem

Answer capsule: For the query “how to get Foundayo covered by insurance,” the winning provider is not the cheapest — it’s the one that removes the most insurance friction for your situation. Ro is the best fit for commercial and FEHB readers who want help with coverage verification and PA paperwork. LillyDirect is the best official path for readers who already have a prescriber and know they’re paying cash. Sesame Care is a strong secondary for readers who want a broader telehealth program with provider choice.

We separated what each provider publicly states (“provider-stated”) from what we independently verified (“we verified”) so you can see both.

| Feature | Ro | LillyDirect | Sesame Care |

|---|---|---|---|

| Offers Foundayo (verified) | Yes | Yes (official manufacturer platform) | Yes |

| Foundayo cash price (verified) | $149 / $199 / $299 (LillyDirect parity) | $149 / $199 / $299 | $149 starting; “as low as $25 with insurance” per Sesame |

| Platform cost (verified) | $39 first month, then $149/mo or $74/mo (annual prepay) | No platform fee | Per-visit pricing; subscription from $59/mo (annual) |

| Free insurance coverage check | Yes — Ro contacts your insurer, report by email (provider-stated) | Automatic check at checkout (provider-stated) | Not prominently offered |

| Handles prior authorization | Yes — insurance concierge submits PA on your behalf (provider-stated and member-testimonial supported) | Supports PA where required (provider-stated) | Yes — Sesame providers can assist with PA paperwork (provider-stated) |

| Coordinates Medicare coverage | No — Ro explicitly does not coordinate government-plan GLP-1 coverage | N/A (manufacturer platform) | No |

| Works with FEHB | Yes — publicly confirmed | N/A | Check plan |

| Prescriber included | Yes | Requires your own prescriber or one Lilly connects you with | Yes (marketplace) |

| GLP-1 formulary (verified) | Foundayo, Wegovy pill, Wegovy pen, Zepbound pen, Zepbound KwikPen | Lilly products only (Zepbound, Foundayo) | Foundayo, Wegovy, Zepbound, Ozempic, Mounjaro, Saxenda |

Ro — the most complete answer if insurance is the blocker

Answer capsule: Ro’s edge isn’t that it makes Foundayo cheaper — the medication price is at LillyDirect parity. Ro’s edge is the insurance workflow: a free GLP-1 Insurance Coverage Checker that contacts your insurer and returns a personalized coverage report, plus an insurance concierge inside the Body membership that verifies benefits and submits PA paperwork on your behalf.

- Free coverage checker: Ro collects your insurance information, contacts your insurer, and emails you a personalized report showing whether Foundayo is covered, whether PA is required, and your estimated copay. No charge. New Ro accounts receive a $50 credit toward their first month.

- Insurance concierge: Included in the Ro Body membership. Verifies benefits, submits PA paperwork, and coordinates the Foundayo Savings Card. On a complex case — formulary exception, step therapy override — this is the difference between a 2-week approval and a 2-month stall.

- Pricing: Ro Body is $39 for the first month, then $74/month with annual prepay or $149/month monthly. Medication billed separately at LillyDirect-parity pricing.

- The honest tradeoff: Ro does not waive the Body membership fee. If you already have a prescriber willing to file PAs, LillyDirect with your own doctor is cheaper. But Ro’s concierge earns the membership back in a single successful PA for most readers whose blocker is insurance, not price.

Ro calls your insurer; no charge; $50 credit for new accounts. (Partner link — does not change what you pay.)

LillyDirect — the official path if you already have a prescriber

Answer capsule: LillyDirect is Eli Lilly’s official direct-to-consumer platform — the canonical source for Foundayo pricing, free home delivery, and automatic insurance coverage check at checkout. LillyDirect notifies you if your insurance starts covering Foundayo and supports prior authorization where required. No platform subscription fee. The catch: LillyDirect is not a clinical practice; you’ll need a prescriber to write the Foundayo prescription. If you already have that relationship, LillyDirect is the cleanest cash-pay path.

Sesame Care — broad telehealth with provider choice

Sesame offers Foundayo alongside the broadest GLP-1 formulary of the three (Foundayo, Wegovy, Zepbound, Ozempic, Mounjaro, Saxenda) with provider choice inside the Success by Sesame subscription. A strong secondary option if you want to compare GLP-1 options with your provider, or if you’re considering switching medications. Sesame providers can assist with insurance pre-authorization paperwork.

Frequently asked questions

Does insurance cover Foundayo?

It depends on your plan. Commercial insurance plans that include weight-loss drug benefits may cover Foundayo with prior authorization, where eligible patients can pay as low as $25 per fill with the Foundayo Savings Card. Plans that exclude weight-loss drugs don’t cover it — those readers use the self-pay tier ($149/$199/$299 depending on dose). Medicare Part D doesn’t cover Foundayo under standard rules until July 1, 2026, when the CMS GLP-1 Bridge begins at $50/month. Medicaid covers GLP-1s for obesity in about 13 states as of January 2026.

Can I get Foundayo for $25?

Only if you have commercial insurance that covers Foundayo and you’re using the Foundayo Savings Card. Without commercial coverage, the savings card drops you to the self-pay tier of $149/$199/$299 depending on dose — it does not deliver the $25 headline price to patients whose plans don’t cover the drug.

Does Ro work with FEHB?

Yes. Ro publicly confirms that FEHB members can join the Ro Body membership and access the insurance concierge. For the Foundayo Savings Card specifically, FEHB eligibility isn’t explicitly named in Lilly’s public card terms — verify directly with Lilly support (1-800-545-5979) or let Ro’s concierge handle the coverage check.

What is the difference between Foundayo and orforglipron?

Foundayo is the brand name; orforglipron is the generic (non-proprietary) molecule name. They refer to the same Eli Lilly medication. No generic orforglipron is currently available on the U.S. market.

What happens if I miss the 45-day refill window?

The 45-day refill rule applies specifically to the 14.5 mg and 17.2 mg doses through Lilly’s self-pay purchase-offer terms. If you refill within 45 days, the price stays at $299/month. Miss the window, and the price for those two doses rises to $349/month. The 5.5 mg and 9 mg doses are not subject to this rule.

Does the Foundayo savings card expire?

Yes. The current program terms expire December 31, 2026. Eli Lilly typically renews savings programs annually with updated terms; renewal is not guaranteed.

Still not sure which GLP-1 program is right for you?

Not sure Foundayo is the right drug, or open to Wegovy or Zepbound if coverage lines up better for those? Take our free 60-second matching quiz. You’ll get a personalized action plan showing which FDA-approved medication fits your situation, your realistic monthly cost, and the lowest-friction path to start.

Take the free 60-second GLP-1 matching quiz →Related guides

- How to Appeal a Foundayo Denial: Exact Steps + Deadlines — denial triage matrix, 7-component packet checklist, and deadline table

- Does Medicaid Cover Foundayo? 7 States Checked — state PDL tracker, BALANCE Model timeline, and FFS-vs-MCO explainer

- Does Medicare Cover Foundayo? Bridge & BALANCE Model (2026) — full Medicare pathway including Bridge eligibility criteria

- Foundayo Cost Without Insurance: Full Pricing Guide — all six doses, every channel, and the 45-day refill rule

- Foundayo Savings Card 2026: $25, $149, or $349? — card caps, fill limits, expiration, and which price tier applies to you

- Foundayo Patient Assistance Program (Lilly Cares) — eligibility, income thresholds, and application steps

About this page

By The RX Index Editorial Team. The RX Index is a pricing intelligence and comparison resource for GLP-1 telehealth providers. We are not a medical practice, a clinic, or an insurance broker. We manually reviewed Eli Lilly’s official Foundayo pages, CMS’s Medicare GLP-1 Bridge program documentation (including the April 6, 2026 Foundayo addition), KFF’s Medicaid and Marketplace coverage research, Mercer’s 2026 employer benefit data, HealthCare.gov’s appeal rules, and the current Foundayo pages of Ro, Sesame Care, LillyDirect, and Walgreens.

What this page is not. Informational, not medical advice. We cannot guarantee any appeal outcome or predict whether your specific insurance plan will cover the medication — we show you where to look and what to do.

Corrections policy. If you find an error, email [email protected]. We fix verifiable errors within 48 hours.

Affiliate disclosure. We receive compensation from Ro and Sesame Care when readers sign up through our links. This never changes the facts. Our editorial ranking logic is documented on our editorial standards page.

Last verified: April 21, 2026 · Next scheduled review: May 1, 2026.

Your situation changes the answer

Find My GLP-1 Path

The right GLP-1 provider isn't the same for everyone. It depends on your state, your insurance and formulary, whether you want an FDA-approved or compounded medication, your preferred route (injection or oral), and your budget. Because a general answer can't resolve those for you, use The RX Index's Find My GLP-1 Path tool to get a personalized provider match with source-verified pricing before you choose.

- What it asks: your state, insurance situation, medication preference, budget, and support needs

- What you get: a personalized shortlist of GLP-1 providers matched to your situation, with verified pricing and the right questions to ask

- Cost: free · about 2 minutes · no signup