Does COBRA Cover Wegovy? Yes — But Only If Your Plan Covered It Before (2026 Guide)

Published: · Last reviewed:

By The RX Index Editorial Team · Last verified: May 13, 2026 · Informational only — not medical, legal, tax, or insurance advice.

The short answer (read this first)

Does COBRA cover Wegovy? Yes — but only if your old employer's health plan covered Wegovy before you lost coverage. COBRA isn't a new policy. It's the same group health plan continued, so the formulary, prior authorization, copay, and pharmacy network generally stay in place. If your plan covered Wegovy before, COBRA usually keeps that coverage. If it didn't, electing COBRA won't add Wegovy to the benefit.

The catch is the price tag. Under COBRA the plan can charge up to 102% of the full plan premium — the share you used to pay through payroll, the share your employer was paying on your behalf, and a small admin fee. Applied to Kaiser Family Foundation's 2025 employer-plan premium benchmark, that works out to roughly $793/month for single coverage and $2,294/month for family coverage. Your COBRA election notice is the source of truth.

So the real question isn't “does COBRA cover Wegovy.” It's whether keeping COBRA just to protect your Wegovy makes financial sense — or whether you'd be better off with an ACA Marketplace plan, a manufacturer-direct prescription through NovoCare Pharmacy ($149–$399/month for FDA-approved Wegovy), or a telehealth path like Ro or Sesame Care.

Will COBRA cover your Wegovy?

| Your situation | Does COBRA cover Wegovy? | Likely best move |

|---|---|---|

| Old plan covered Wegovy + active prior authorization (PA) | Usually yes -- same coverage continues | Run the cost math. COBRA may still lose to ACA. |

| Old plan covered Wegovy but no PA yet | Usually yes, with PA approval needed | Elect only if math beats alternatives. Verify first. |

| Old plan excluded weight-loss meds | No -- exclusion continues | Skip COBRA for Wegovy. Use NovoCare direct or an ACA plan that covers it. |

| Employer had fewer than 20 employees | Federal COBRA doesn't apply -- check state mini-COBRA law | Usually ACA Marketplace Special Enrollment is the move. |

Run your numbers before you commit

→ Run the COBRA + Wegovy MathOr check Wegovy coverage on any plan — free

→ Check Wegovy Coverage on Ro (Free)Sponsored affiliate link · no commitment

How COBRA actually works (and why that determines your Wegovy answer)

COBRA isn't a new health plan you sign up for. It's a federal law that lets you keep your employer-sponsored group health plan after you lose it due to a qualifying event. Because COBRA continues the same group plan, you generally keep the same prescription-drug benefits, copays, deductibles, coverage limits, claims process, and appeal rights that apply to similarly situated active employees.

Who can elect COBRA

COBRA applies to private-sector and most state and local government employers with 20 or more employees in the prior year. Federal employees, churches, and certain church-affiliated organizations are excluded. If your employer had fewer than 20 workers, most states have mini-COBRA laws.

Qualifying events

Voluntary or involuntary job loss (other than gross misconduct), reduced hours below eligibility threshold, divorce or legal separation, death of covered employee, aging off a parent's plan at 26, or the covered employee becoming entitled to Medicare when that causes a dependent to lose coverage.

The two deadlines you cannot miss

You have 60 days to elect COBRA from the later of coverage loss or notice receipt. After electing, 45 days to make your first payment. Ongoing monthly payments have a 30-day grace period. Coverage is retroactive to your coverage-loss date if you elect and pay on time.

Sources: Department of Labor, “An Employee's Guide to Health Benefits Under COBRA” (29 CFR Part 2590); CMS, COBRA Continuation Coverage fact sheet.

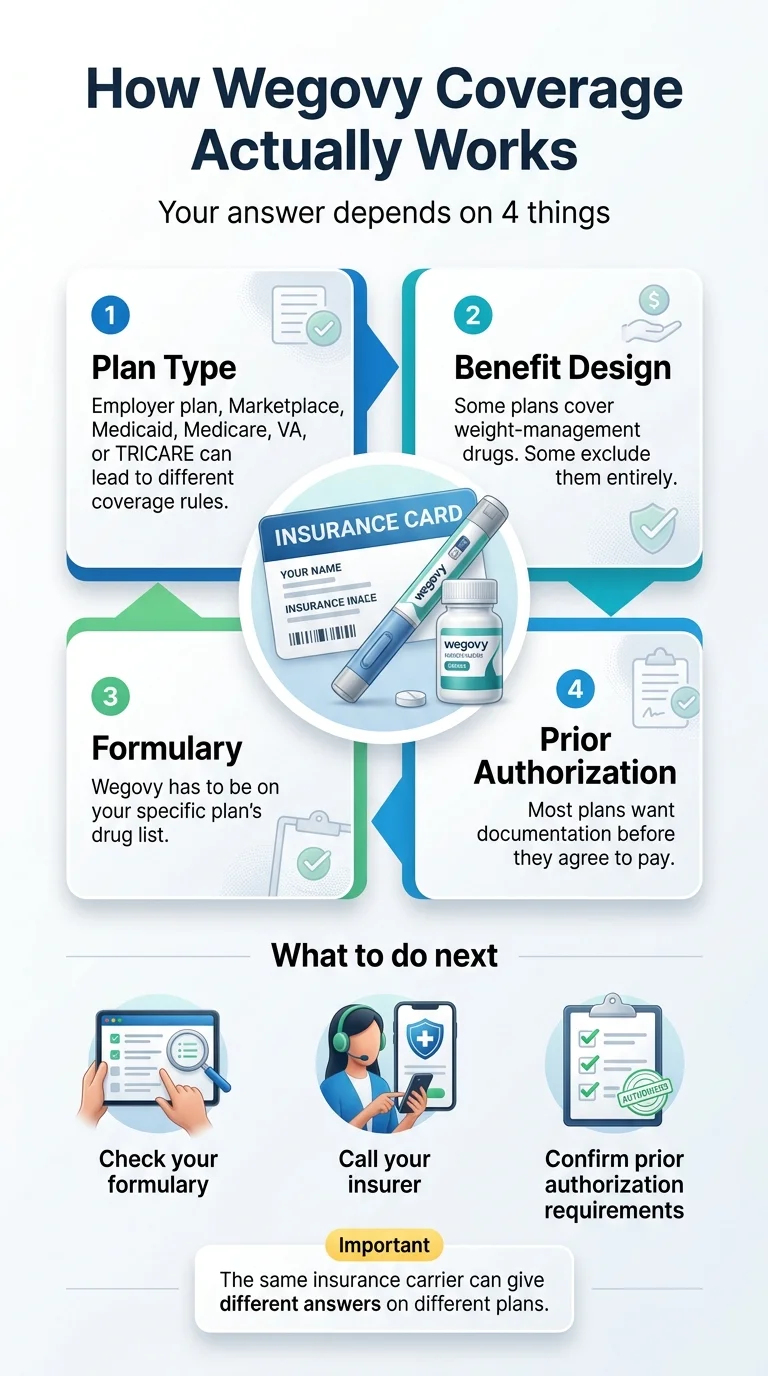

Does COBRA cover prescription drugs like Wegovy?

Yes — if prescription-drug benefits were part of your employer group health plan. COBRA generally continues the same group health benefits, including the same drug formulary, prior authorization rules, copays, deductibles, and pharmacy network that apply to similarly situated active employees. The continuation isn't permanent, though: if the active-employee plan changes its formulary, switches PBMs, or adds a weight-loss medication exclusion at plan-year renewal, those changes flow through to COBRA participants.

For Wegovy specifically, the real question isn't whether COBRA covers prescription drugs — it's whether your specific employer plan covered Wegovy on its formulary. Many employer plans cover everyday prescriptions but explicitly exclude weight-loss medications. The next section walks you through which scenario you're actually in.

Does COBRA cover Wegovy specifically? The honest answer

COBRA covers Wegovy if — and only if — your former employer's group health plan included Wegovy on its formulary before you lost coverage. The hard truth: most employer plans don't actually cover Wegovy for weight loss. Per Kaiser Family Foundation's 2025 Employer Health Benefits Survey, just 16% of firms with 200–999 workers, 30% of firms with 1,000–4,999 workers, and 43% of firms with 5,000+ workers cover GLP-1s for weight loss. If you worked for a mid-size or small employer, the odds are that your plan didn't cover Wegovy.

The 5-minute verification — what to check before deciding

Pull up your old plan's drug formulary.

Search it for "Wegovy" or "semaglutide" (weight management). Most plans publish this online via the insurer or PBM -- Blue Cross, UnitedHealthcare, Aetna, Cigna, CVS Caremark, Express Scripts, OptumRx.

Look at the exclusions list.

Many plans explicitly exclude "anti-obesity agents" or "drugs for weight loss." That language is the kill switch.

Find your active prior authorization.

If you've been filling Wegovy through your employer plan, you likely have a PA on file. Most PAs are valid for 6-12 months. Verify the expiration date before you assume it'll carry you through your COBRA period.

Note your current copay or coinsurance.

That number carries over.

Confirm your pharmacy network and PBM.

Same network, same rules.

For specific insurer guidance, see our Blue Cross GLP-1 guide or UnitedHealthcare GLP-1 guide.

The four scenarios that decide everything

| Scenario | Was Wegovy covered before? | What COBRA does | What you should do next |

|---|---|---|---|

| A. Plan covered Wegovy + you had an active PA | Yes | Generally continues the same coverage and PA | Run the cost math. Many people still lose to ACA. |

| B. Plan covered Wegovy, no PA yet | Technically yes | Coverage available; you need a fresh PA submitted | Elect COBRA only after you confirm (a) you'll be approved and (b) the math beats alternatives. |

| C. Plan excluded weight-loss medications | No | Same exclusion continues -- COBRA doesn't add Wegovy | Skip COBRA for Wegovy. Compare ACA + a GLP-1-friendly plan, NovoCare direct, or Ro cash-pay. |

| D. Plan covered Wegovy only for cardiovascular risk reduction | Partially | CV indication continues; weight-loss indication doesn't | Talk to your prescriber about whether your diagnosis qualifies for the CV indication. |

The honest admission most pages won't make

If your employer plan didn't cover Wegovy, COBRA is almost never the right move for the Wegovy question alone. You'd be paying $793/month on average for a plan that still excludes the one medication you care about, and then paying for Wegovy on top of that. If you're in scenario C and Wegovy is the only reason you're considering COBRA, the rest of this page is about how to skip COBRA entirely and still keep your Wegovy without a missed dose.

What COBRA + Wegovy actually costs per month in 2026

During standard COBRA, the plan can charge up to 102% of the total plan cost: the employee share, the employer share, and up to a 2% administrative charge. Applied to KFF's 2025 employer-plan averages, that benchmarks at roughly $793/month for single coverage and $2,294/month for family coverage. Your Wegovy out-of-pocket layered on top depends on your formulary status.

The 2026 COBRA + Wegovy total cost matrix

Single-coverage examples use the KFF 102% national benchmark (~$793/month). Your COBRA election notice is the source of truth.

| Path | Monthly health premium | Monthly Wegovy out-of-pocket | Total monthly outlay | Best for |

|---|---|---|---|---|

| COBRA + plan covered Wegovy + Savings Card | ~$793 benchmark | As little as $25 (max savings $100/fill) | ~$818 | Already approved, have a spouse/family on the plan, or have other care needing continuity |

| COBRA + plan covered Wegovy + standard copay/coinsurance | ~$793 | $50-$200+ | $843-$993+ | Same as above with a weaker copay structure |

| COBRA + plan did NOT cover Wegovy (pen) | ~$793 | $199-$399 NovoCare direct | $992-$1,192+ | Almost never the right move for Wegovy alone |

| COBRA + plan did NOT cover Wegovy (pill) | ~$793 | $149-$299 NovoCare direct | $942-$1,092+ | Almost never the right move for Wegovy alone |

| ACA Marketplace + plan covers Wegovy + Savings Card | $0-$500+ (subsidy-dependent) | As little as $25 | $25-$525+ | Person with a valid Wegovy Rx whose income may qualify for premium tax credits |

| No insurance + NovoCare direct (pen) | $0 | $199-$399 | $199-$399 | Person with a valid Wegovy Rx who does not need broader health-plan continuity |

| No insurance + NovoCare direct (pill) | $0 | $149-$299 | $149-$299 | Same as above |

| Sesame Care + Costco Pharmacy (Costco members) | $0 | $349 Wegovy injection; Wegovy pill from $149 | $149-$349 | Existing Costco members who want a self-pay branded route |

| Ro Body cash-pay (first month) | $39 first month | $149-$399 via NovoCare integration | $188-$438 | Wants a provider managing dose escalation and insurance coordination |

| Ro Body cash-pay (ongoing monthly) | $149/mo | $149-$399 medication | $298-$548 | Same as above ongoing |

| Ro Body cash-pay (annual prepay) | ~$74/mo equivalent | $149-$399 medication | $223-$473 | Same as above, with annual commitment |

Provider-stated vs. RX Index-verified pricing

| Source | What the provider/source states | What we verified | Verification date |

|---|---|---|---|

| COBRA premium | DOL: up to 102% of plan cost; KFF 2025: $9,325 single annual / $26,993 family annual employer-plan average | RX Index calculated monthly 102% benchmark: ~$793 single / ~$2,294 family | May 13, 2026 |

| NovoCare Pharmacy | Wegovy pill $149/month starter doses, $299/month higher doses; Wegovy pen $199/month starter promo (through December 31, 2026), $349/month standard pen, $399/month Wegovy HD 7.2 mg | All ranges verified directly from NovoCare.com pricing page | May 13, 2026 |

| Wegovy Savings Card | "Pay as little as $25/month," maximum savings $100/month per fill; commercial insurance required; government beneficiaries excluded | Card structure and exclusions verified on Wegovy.com | May 13, 2026 |

| Ro Body | $39 first month, $149/month monthly, as low as $74/month with annual prepay; medication billed separately | Membership tiers and medication-separate billing verified at ro.co | May 13, 2026 |

| Sesame Care + Costco | Wegovy injection $349/month at Costco Pharmacy for Costco members with valid Rx; Wegovy pill starting at $149/month | Pricing and Costco member requirement verified at sesamecare.com | May 13, 2026 |

The “real cost” gut-check question

Ask yourself: Is the only reason you're considering COBRA to keep your Wegovy access? Or do you also have a spouse on the plan, ongoing specialist care, a planned surgery, year-to-date deductible progress, or a chronic condition that needs continuous coverage?

- ✕If Wegovy is the only reason → COBRA almost never wins the math. A NovoCare direct prescription, a marketplace plan with the Savings Card, or Sesame/Costco's self-pay path beats it for less than half the cost.

- ✓If you also need broader coverage continuity → COBRA may absolutely be worth the premium, especially if your plan covered Wegovy and you have an active PA.

COBRA + Wegovy Cost Calculator (2026)

Enter your numbers to get a personalized verdict

National benchmark ~$793/mo single. Your notice has the real number.

Leave blank if you haven't checked yet.

Decision point

If your COBRA plan covered Wegovy and the total cost works, your next move is making sure your prior authorization transfers cleanly. If the math doesn't work, Ro's free GLP-1 Insurance Coverage Checker can help you see whether any plan you're considering covers Wegovy and whether prior authorization may be needed, in about five minutes.

→ Check Wegovy Coverage on Any Plan — Free (Ro)Sponsored affiliate link · no commitment

When COBRA is actually worth paying just to keep Wegovy

When COBRA probably makes sense

| Situation | Why it matters |

|---|---|

| Short gap before new employer coverage starts | Avoids plan disruption, formulary reset, new PA process |

| Wegovy is covered with a low copay | Protects a benefit that may be hard to replace on the Marketplace |

| You already met your deductible or OOP max | A new plan resets cost-sharing to zero |

| You have active medical care -- specialists, surgery, other expensive medications | COBRA protects far more than just Wegovy |

| Your PA is active and refill timing is tight | Skipping COBRA risks a missed dose |

| Spouse or kids are on the plan and need continuity | Same as above, multiplied |

When COBRA usually isn't worth it

| Situation | Why it matters |

|---|---|

| Your old plan excluded Wegovy | COBRA keeps the exclusion |

| Your PA was denied or expired | Premium alone doesn't solve the PA problem |

| COBRA premium > cash-pay Wegovy + program fee | You'd be overpaying to protect a benefit you can buy directly |

| You don't need the broader health plan | You're effectively buying insurance for one medication |

| Income dropped enough to qualify for ACA subsidies | A subsidized marketplace plan often costs a fraction of COBRA |

| You qualify for Medicaid | Likely free or near-free coverage |

Your Wegovy prior authorization on COBRA — what carries over and what doesn't

If you had an active Wegovy prior authorization under the same plan and PBM, it will often remain on file through its original approval window once COBRA is active. Verify the PA expiration date and claim status with the PBM before paying the premium. PA renewal, formulary changes, PBM changes, delayed COBRA processing, and premium lapses can still bounce a refill at the pharmacy counter.

What generally carries over without you doing anything

- ✓Your existing prior authorization (within its original validity window)

- ✓Your formulary tier and copay or coinsurance

- ✓Your pharmacy network and preferred pharmacy

- ✓Your PBM (CVS Caremark, Express Scripts, OptumRx, etc.)

- ✓Year-to-date deductible and OOP maximum, in most plans, if you elect COBRA without a coverage gap -- verify with your administrator

The “no-gap” rule that saves a lot of people

COBRA coverage is retroactive to the date your employer coverage ended if you elect within 60 days and pay within 45 days of election. The pharmacy may not process Wegovy as active coverage while your election or first premium is still pending, so don't rely on a refill working at the counter until the COBRA administrator or PBM confirms coverage is active.

Where COBRA Wegovy claims actually fail

| Failure point | What the pharmacy/PBM may show | What it usually means | Who to call | Exact next action |

|---|---|---|---|---|

| PA expired | "Prior authorization required" | Your PA's original window ran out | Your prescriber's office | Submit a renewal PA with documented weight loss of ≥5% from baseline |

| COBRA election still pending | "Coverage not active" or "Member not found" | Your election or first payment hasn't been fully processed | COBRA administrator | Confirm processing status; ask if a test claim can be run after payment posts |

| Refill too soon | "Refill too soon" with a future date | Plan's day-supply rule blocks early refill | Pharmacy first; PBM if pharmacy can't override | Ask if a vacation or coverage-transition override applies |

| Formulary exclusion added | "Drug not covered" | Plan changed at renewal and dropped Wegovy or added weight-loss exclusion | Your former HR or COBRA administrator | Confirm the change in writing; review alternatives (ACA, NovoCare direct, Ro/Sesame) |

| PBM switched | Old PBM card rejected | Plan switched PBMs at renewal | COBRA administrator; new PBM | Get the new card; resubmit prior authorization if required |

| Plan-year reset | New deductible applies | Plan year rolled over; cost-sharing reset | Plan administrator | Verify your new deductible and tier; plan for higher OOP until deductible is met |

| Pharmacy out-of-network | "Pharmacy not contracted" | Network changed or you're using a non-network pharmacy | PBM | Transfer the prescription to an in-network pharmacy |

The 30-minute Wegovy + COBRA verification call script

Before you elect COBRA or drop it, verify three things with three separate calls: that Wegovy is on your formulary and your PA is active (call your PBM), that your COBRA premium and timing are what you think they are (call your COBRA administrator or HR), and that the pharmacy can actually process the claim cleanly (call your pharmacy). The full script below takes about 30 minutes and prevents the worst-case “I paid $800 and my refill bounced” outcome.

Find the PBM phone number on your prescription insurance card.

- 1."Is Wegovy on my current formulary, and at what tier?"

- 2."Will that coverage continue if I elect COBRA?"

- 3."Is there an approved prior authorization for Wegovy on file for me?"

- 4."What date does my PA expire?"

- 5."What's my exact copay at my current Wegovy dose?"

- 6."Does mail-order pricing differ from retail?"

- 7."Does my plan require participation in a weight-management program?"

- 8."Is there an exclusion in my plan for weight-loss medications?"

Your COBRA election notice has the administrator's number.

- 1."What's my exact monthly COBRA premium for my coverage tier?"

- 2."What date does my current job-based coverage end?"

- 3."What's my COBRA election deadline?" (Federal minimum is 60 days from the later of coverage loss or notice receipt.)

- 4."What's my first payment deadline?" (Federal minimum is 45 days after election.)

- 5."Will my prescription benefits continue under the same group number and PBM?"

- 6."Are there any plan changes coming at the next plan year that I should know about?"

Walk into your pharmacy or call the prescription line.

- 1."Can you run a test claim for Wegovy under my current coverage?"

- 2."What does the claim show -- copay amount, PA required, refill too soon, or plan exclusion?"

- 3."Can I fill a 30-day or 90-day supply before my coverage status changes?"

Three cheaper paths to keep Wegovy without COBRA

For most people whose main reason to continue coverage is Wegovy, three paths often beat COBRA on cost: the ACA Marketplace under your post-job-loss Special Enrollment Period (which can come with premium tax credits when your income drops), Novo Nordisk's direct NovoCare Pharmacy at $149–$399/month for FDA-approved Wegovy with no insurance required, and a telehealth provider like Ro or Sesame Care that prescribes FDA-approved Wegovy with insurance coordination or self-pay support.

Path 1 — The ACA Marketplace Special Enrollment Period (often the clear winner)

Losing employer-based health coverage triggers a 60-day Special Enrollment Period on HealthCare.gov or your state Marketplace — applicable both before and after your last day of job-based coverage.

- ✓The 60-day SEP runs from 60 days before your coverage ends through 60 days after.

- ✓Pick a plan: before enrolling, search for "Wegovy" or "semaglutide" on each plan's drug formulary.

- ✓Subsidies are based on estimated full-year 2026 household income for everyone in your tax household -- that includes income earned before you left your job.

- ✓This path can stack: an ACA plan that covers Wegovy plus the Wegovy Savings Card can drop a copay to as little as $25/month (max savings $100/month per fill).

Path 2 — NovoCare Pharmacy (Novo Nordisk's own direct pharmacy)

NovoCare Pharmacy is Novo Nordisk's manufacturer-direct cash-pay program. With a valid Wegovy prescription, you can get FDA-approved Wegovy shipped to your door at flat self-pay prices. No insurance required, no membership fee, no prior authorization process — but the program excludes anyone enrolled in Medicare, Medicaid, TRICARE, or VA.

Verified NovoCare pricing (May 13, 2026):

- Wegovy pill: $149/month for 1.5 mg and 4 mg doses; $299/month for higher doses. The $149/month 4 mg price runs through August 31, 2026.

- Wegovy pen: $199/month for new patients on starter doses (promo through December 31, 2026); $349/month standard ongoing; $399/month for Wegovy HD 7.2 mg.

- HSA and FSA eligible. See our Wegovy HSA/FSA documentation guide for what to keep on file.

The government-insurance exclusion is federal anti-kickback law, not a Novo policy choice. Government insurance beneficiaries should review our Medicare Wegovy guide instead.

Path 3 — Telehealth providers that prescribe FDA-approved Wegovy

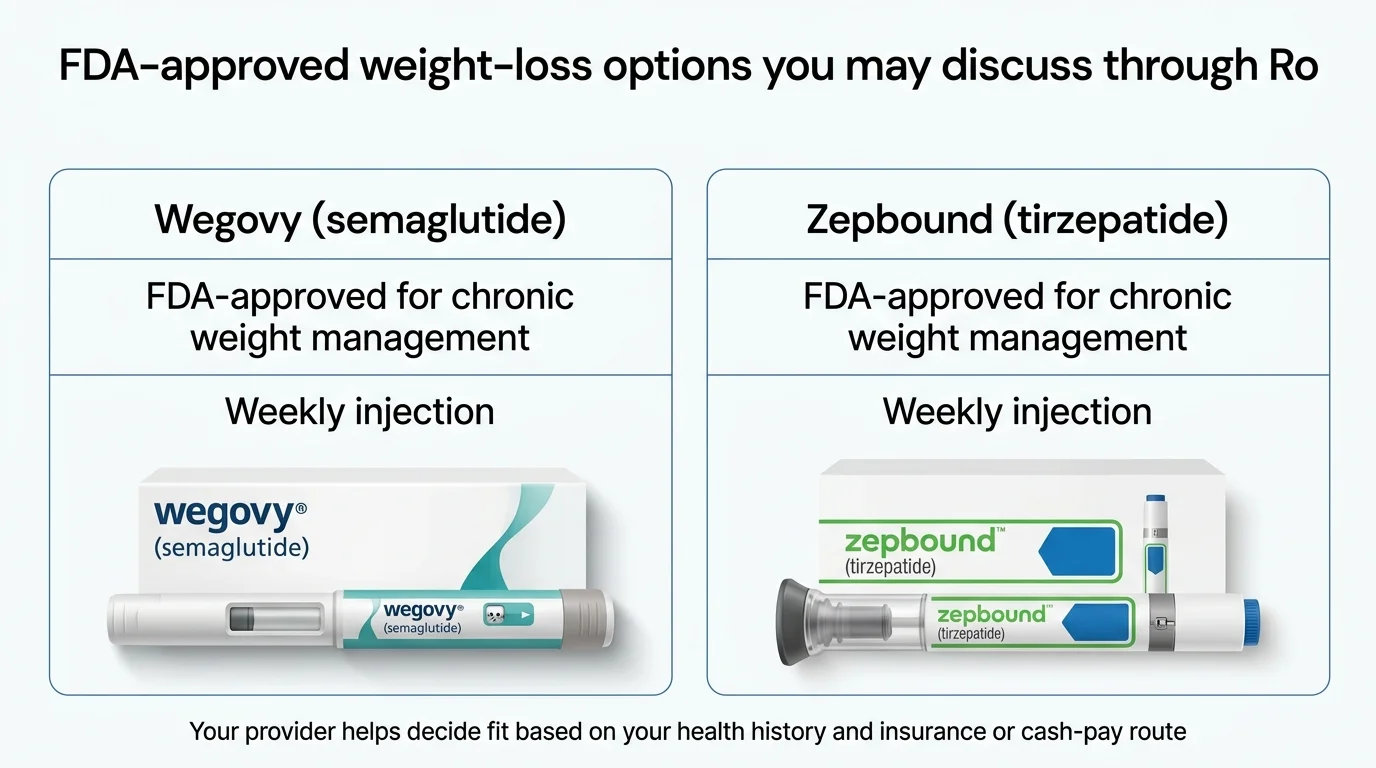

Ro Body

Strongest fit for someone who wants a provider managing treatment and an insurance team handling prior authorization paperwork when new coverage comes online. Carries FDA-approved Wegovy pill and pen, matches NovoCare's cash-pay pricing, and runs a free GLP-1 Insurance Coverage Checker. Also helpful for insurance billing when you do get a new plan.

Pricing (verified May 13, 2026)

- Get started: $39 first month

- Ongoing: $149/month — or ~$74/month with annual plan

- Medication billed separately at NovoCare cash-pay prices

Sponsored affiliate link

See our Ro Body reviews guide for the full breakdown.

Sesame Care + Costco Pharmacy

Particularly strong if you're a Costco member. Through Sesame's Costco partnership, Costco members with a Wegovy prescription can access Wegovy injection at $349/month when self-paying at the Costco Pharmacy, and Wegovy pill prescriptions available starting at $149/month. Success by Sesame clinical care is as low as $59/month with an annual subscription — fee is separate from medication cost.

Use Sesame instead of Ro when:

- You want explicit provider choice

- You specifically want the Zepbound vial or formulations Ro doesn't carry

- You're a Costco member and prefer the Costco Pharmacy path

Ro and Sesame both offer FDA-approved brand-name Wegovy — not compounded semaglutide. For compounded options, see our GLP-1 path quiz.

The three paths side by side

| Factor | ACA Marketplace SEP | NovoCare Direct | Ro Body | Sesame + Costco |

|---|---|---|---|---|

| Best for | You need other coverage; income dropped | Wegovy is your only reason for coverage | You want a provider + insurance coordination | Existing Costco members who want self-pay branded Wegovy |

| Monthly premium | $0-$500+ depending on subsidy | $0 | $39 first month / $149 ongoing / ~$74 annual prepay equivalent | $0 |

| Monthly Wegovy | Copay/coinsurance (as little as $25 with Savings Card on covered plans) | $149-$399 cash | $149-$399 cash | $349 injection / $149+ pill |

| Insurance handling | Self-managed | None | Insurance concierge included | None |

| Time to first dose | Plan effective 1st of next month | After prescription is processed and shipped | After clinical review, prescription, and shipping | Variable based on visit and pharmacy timing |

Decision point

If you want FDA-approved brand-name Wegovy without paying the COBRA premium just to protect a copay, Ro is the cleanest path. Their team helps you check whether your COBRA plan (or any new plan you're considering) covers Wegovy, handles insurance paperwork, and if coverage doesn't come through, transitions you to their NovoCare-integrated cash-pay path starting at $149/month.

→ See If Ro Can Help With Your Wegovy CoverageSponsored affiliate link · if you're on Medicare, Medicaid, TRICARE, or VA, see our Medicare Wegovy guide instead

How to bridge the gap without missing a Wegovy dose

During the 60-day COBRA election window you're technically uninsured until you actually elect, which can panic anyone whose Wegovy refill is days away. Three strategies prevent a missed dose.

Move 1 — Refill before your last day

Move 2 — Use the COBRA retroactive election rule strategically

Move 3 — Start a cash-pay prescription during the gap

Decision point

If you're days away from running out of Wegovy and don't want to gamble on COBRA paperwork processing in time, the lowest-risk option is starting a cash-pay prescription through Ro while you finalize your longer-term decision. If your COBRA election eventually goes through, you can switch back to insurance billing for your next fill.

→ Start a Cash-Pay Wegovy Prescription on RoSponsored affiliate link

COBRA vs. ACA Marketplace — which path wins for Wegovy in 2026

For many people losing employer coverage, the ACA Marketplace can beat COBRA on price, especially when the income change qualifies you for premium tax credits. COBRA's structural disadvantage: you pay up to 102% of the full plan cost with no subsidy. ACA's structural advantage: subsidies scale with income. The exception: when your old plan covered Wegovy and a comparable ACA plan in your area doesn't.

| Factor | COBRA | ACA Marketplace SEP |

|---|---|---|

| Eligibility | Employer with 20+ employees; qualifying event | Loss of job-based coverage = 60-day SEP |

| Monthly premium | Up to 102% of full plan cost (~$793 single benchmark) | Subsidized based on full-year household income; can be $0-$500+ |

| Plan you get | Identical to former employer plan | New plan you pick from available Marketplace plans |

| Wegovy coverage | Same as employer plan (yes or no) | Depends on the plan you pick -- verify formulary before enrolling |

| Duration | Up to 18 months (29 if disabled, 36 in some cases) | Indefinite as long as you're enrolled |

| Tax treatment | COBRA premiums can be paid tax-free from an HSA; other deductibility depends on tax rules | Tax credits applied directly to monthly premium |

| Best for | Plan-specific continuity (specialist, surgery, family) | Most cases, especially when income drop affects subsidy eligibility |

How to decide in 10 minutes

- 1Get your exact COBRA premium from your election notice.

- 2Run an ACA quote at HealthCare.gov (or your state Marketplace) using your estimated full-year 2026 household income.

- 3Search "Wegovy" or "semaglutide" on the drug formulary of each ACA plan you're seriously considering.

- 4Compare total monthly cost under each path using the calculator above.

What if my plan denies Wegovy or says it needs a new prior authorization?

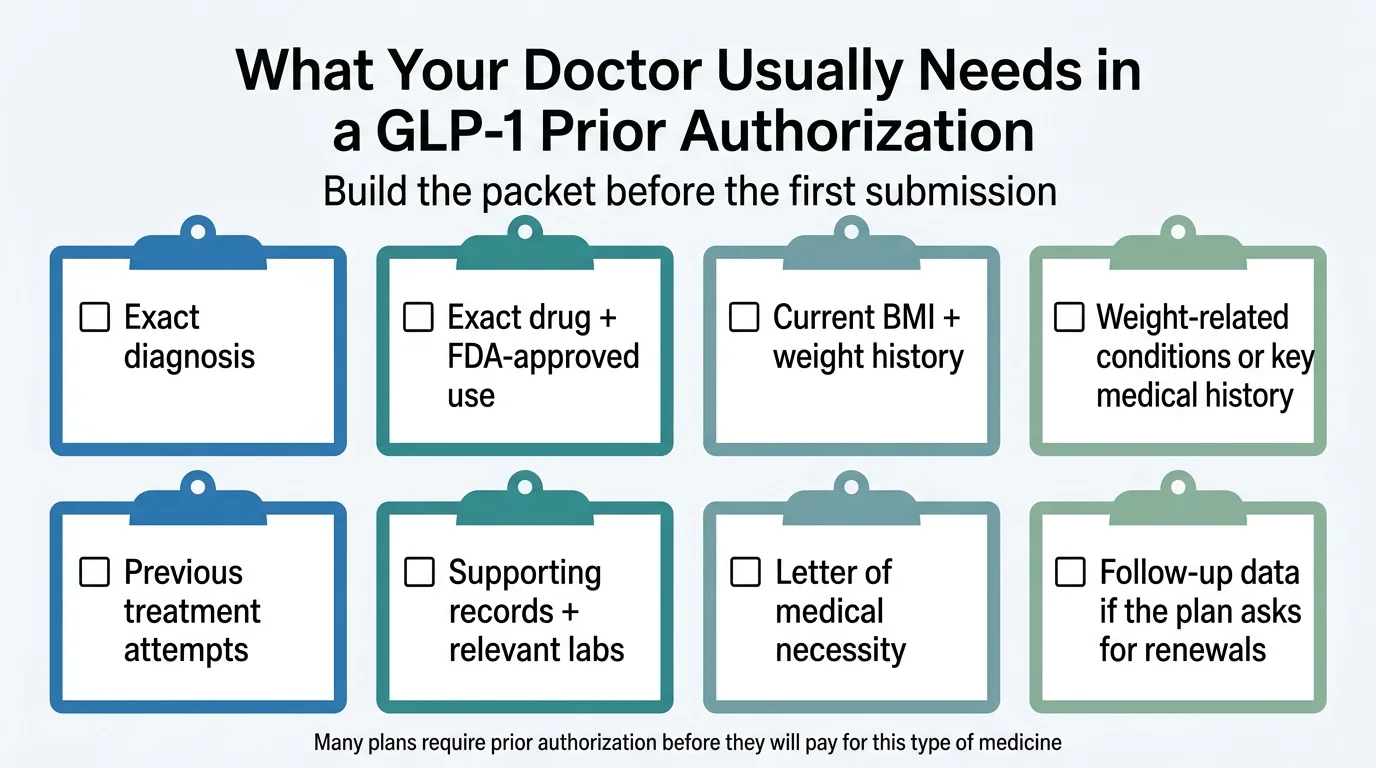

A denial doesn't end the process — but the next step depends on the denial reason. If the plan excludes weight-loss medications entirely, an appeal is hard but not impossible (especially if you have a qualifying cardiovascular risk indication). If the denial is missing documentation, your prescriber can usually fix it with a fresh PA, a letter of medical necessity, or a peer-to-peer review.

The most common Wegovy denial reasons

- 1The plan excludes weight-loss medications. Hard to appeal unless you have a different qualifying indication (e.g., cardiovascular risk reduction).

- 2PA paperwork is missing or incomplete. Easiest fix -- prescriber resubmits.

- 3BMI or comorbidity criteria not documented. Prescriber documents and resubmits.

- 4Required lifestyle program not completed. Some plans require 3-6 months of documented diet/exercise attempts.

- 5Step therapy not met. Some plans require trying a cheaper weight-loss medication first.

- 6Wrong diagnosis code. The coding on the prescription matters -- a CV indication vs. weight management indication can be the difference between approval and denial.

- 7Coverage isn't active yet. Especially common during a COBRA election or insurance transition.

Decision point

If your COBRA plan or your new plan denies Wegovy and you don't want to spend weeks navigating it alone, Ro's insurance concierge handles the insurance paperwork and follow-up and routes you to a cash-pay path if coverage doesn't come through. If their team helps you get insurer approval and your medication cost drops from cash-pay pricing to a low copay, the Ro Body membership ($149/month, or as low as $74/month with annual prepay) can become financially worthwhile quickly.

→ See If Ro Can Help Check Wegovy CoverageSponsored affiliate link

Can I use my HSA to pay COBRA premiums?

Yes. The IRS explicitly allows you to use Health Savings Account (HSA) funds to pay COBRA premiums tax-free — it's one of four exceptions in IRS Publication 969 that lets you pay health insurance premiums with HSA dollars without penalty. You cannot use a regular Flexible Spending Account (FSA) for COBRA premiums, but you can use FSA funds for your Wegovy copay or out-of-pocket cost.

What this changes for your math

If you have a $5,000 HSA balance and your COBRA premium is $793/month, you can cover roughly 6 months of COBRA tax-free. For someone in a 22% marginal federal tax bracket, that's effectively a 22% discount on the COBRA premium versus paying with post-tax dollars. Add in state income tax and the discount can climb in higher-tax states.

Wegovy Savings Card + COBRA: COBRA counts as commercial insurance for the Wegovy Savings Card. As long as your plan covers Wegovy, the Savings Card can drop your copay to as little as $25/month, with maximum savings of $100/month per fill. See our Wegovy Savings Card guide for the full eligibility and enrollment details. Government program beneficiaries (Medicare, Medicaid, VA, TRICARE) remain excluded from the Savings Card and the NovoCare direct savings program — that's federal anti-kickback law.

What Wegovy safety facts should not get buried in an insurance decision?

Important safety information

Insurance coverage doesn't make Wegovy the right medication for everyone. Wegovy is a prescription medication with specific contraindications and warnings. It should not be used with other semaglutide-containing products or other GLP-1 receptor agonist medicines. It should not be used if you or your family have had medullary thyroid carcinoma or Multiple Endocrine Neoplasia syndrome type 2 (MEN 2).

Pregnancy planning, breastfeeding, pancreas or kidney problems, diabetic retinopathy, diabetes medications, and procedures using anesthesia or deep sedation should all be discussed with a licensed clinician before starting or continuing treatment. This information comes from Wegovy's official prescribing information. This is an insurance decision guide — not medical advice.

Compounded semaglutide is not a Wegovy substitute — important clarification

FDA clarification

- !Compounded semaglutide products are not FDA-approved finished drugs. FDA has warned that some compounders use semaglutide salt forms that are different active ingredients from those used in approved semaglutide drugs.

- !Wegovy is FDA-reviewed as a finished product with labeled doses, delivery formats, indications, safety information, and manufacturing controls; compounded products are not interchangeable with Wegovy.

- !As of FDA's April 2026 update, semaglutide does not appear on the 503B bulks list or FDA's drug shortage list, and FDA restricts compounding of products that are essentially copies of commercially available FDA-approved drugs.

- !On April 30, 2026, FDA proposed to exclude semaglutide, tirzepatide, and liraglutide from the 503B bulks list.

If you want to stay on the medication you started on under your employer plan — branded Wegovy — your paths are the ones in this guide: COBRA (if your plan covered it), the ACA Marketplace with a plan that covers it, NovoCare direct, Ro, or Sesame Care.

If you're researching all GLP-1 options including non-Wegovy paths, our GLP-1 path quiz routes you to the option that fits your situation and budget.

What real people are getting stuck on

These quotes come from public Reddit threads in r/HealthInsurance and r/Semaglutide. They are public forum examples, not evidence or medical/insurance advice.

“I'm currently on COBRA, and my previous employer's plan covers Wegovy -- [is it] cheaper to stay on COBRA or switch to a Marketplace plan and pay for the medication out of pocket?”

Context: The exact decision the cost matrix above is designed to answer.

“Should I ask someone to loan me $800 to keep my Cobra covering my August Wegovy...”

Context: The answer: almost never borrow $800 to protect a $25 copay when NovoCare direct is $199-$349/month with no insurance.

“I just don't understand how it can be full retail with it being approved.”

Context: This happens when a PA expires unnoticed, or when a formulary change moves Wegovy off the covered list at plan renewal. The verification call script above prevents this exact scenario.

Frequently asked questions

Does COBRA cover Wegovy?

COBRA covers Wegovy if your former employer plan covered Wegovy and you continue that plan through COBRA. Coverage stays subject to the same formulary, prior authorization, copay, deductible, and plan rules -- and to any changes the active-employee plan makes at renewal.

Does COBRA cover prescription drugs in general?

Yes, if your employer group plan included prescription drug benefits. COBRA continuation coverage continues the same health benefits you had as an active employee, which typically includes pharmacy benefits.

Does COBRA cover Wegovy if my employer plan didn't?

Usually no. COBRA generally continues the same plan design, including any exclusions. If your plan excluded weight-loss medications, COBRA keeps that exclusion in place.

Will my Wegovy prior authorization transfer to COBRA?

Often yes, if there's no break in coverage and the same plan and PBM stay in force. Verify with your PBM before assuming -- PA expiration dates, formulary changes, and plan-year renewals can all affect whether your PA still applies.

Can my employer remove Wegovy coverage while I'm on COBRA?

Yes. COBRA participants get whatever benefits the active employees get. If the plan changes Wegovy coverage at the next plan year -- moves it to a higher tier, adds a weight-loss exclusion, switches PBMs -- those changes apply to COBRA participants too.

Is COBRA cheaper than paying cash for Wegovy?

Sometimes. Compare your full COBRA premium plus Wegovy copay against your cash-pay alternative (NovoCare direct or telehealth) plus any program fee. For many people whose only continuity concern is Wegovy, NovoCare direct at $149--$399/month beats the COBRA benchmark premium even before adding the copay.

Can I switch from COBRA to a Marketplace plan?

It depends on timing and circumstance. HealthCare.gov allows switching when your COBRA runs out, when your former employer stops contributing to the premium, or when you're still within the original 60-day SEP from your job-based coverage loss. Voluntarily ending COBRA early outside open enrollment usually means waiting until the next open enrollment period.

Does Medicare cover Wegovy?

Medicare Part D generally covers GLP-1 drugs only for medically accepted FDA-approved indications other than obesity -- for example, type 2 diabetes or cardiovascular risk reduction when the patient and drug meet coverage rules. CMS says the Medicare GLP-1 Bridge will operate from July 1, 2026 through December 31, 2027 for eligible Part D beneficiaries who meet prior authorization criteria; covered Bridge drugs include Wegovy injection and tablets, Foundayo, and Zepbound KwikPen, with pharmacies collecting a $50 copay.

Does Medicaid cover Wegovy?

Coverage varies by state. KFF reports that only 13 state Medicaid programs covered GLP-1s for obesity treatment under fee-for-service as of January 2026, and when covered they typically apply utilization controls such as prior authorization. Medicaid must generally cover GLP-1 drugs for medically accepted FDA-approved indications other than obesity, but coverage for obesity treatment remains optional for states.

Can I use my HSA to pay my COBRA premium?

Yes. IRS Publication 969 explicitly lists COBRA continuation premiums as one of four insurance-premium categories eligible for tax-free HSA distribution. You can pay your COBRA administrator directly from your HSA debit card or reimburse yourself after paying out of pocket.

Can I use my HSA or FSA to pay for Wegovy?

Yes. Wegovy is a qualified medical expense for both HSAs and FSAs when prescribed for an approved medical use. Keep your itemized pharmacy receipt and your prescription documentation in case of audit.

What if my employer had fewer than 20 employees -- is there still COBRA?

Federal COBRA doesn't apply, but most states have mini-COBRA continuation laws for smaller employers. Duration and rules vary by state. Check with your state Department of Insurance or ask your former HR for the specific state continuation rules that apply to your former plan.

Will COBRA premiums increase while I'm enrolled?

Generally only at your former employer's plan-year renewal, when the group plan rates reset for active employees. The 11-month disability extension can be charged at a higher rate -- up to 150% -- if you or a dependent qualify under that rule.

Can my spouse keep Wegovy on COBRA if I don't elect for myself?

Yes. Spouses and dependents are independently eligible to elect COBRA even if the covered employee declines. Each adult in the household has their own 60-day election window.

Are COBRA premiums tax-deductible?

COBRA premiums count as a medical expense for federal income tax, but they're only deductible to the extent your total medical expenses exceed 7.5% of your adjusted gross income -- and only if you itemize. Most people don't reach that threshold from premiums alone. Using HSA dollars is usually the better tax move if you have a balance.

What's the first thing I should do today?

Call your PBM and ask four questions: Is Wegovy on my formulary? Is my prior authorization active? What's my copay at my current dose? When does my PA expire? Those four answers, plus your COBRA premium from your election notice, are everything you need to run the math.

The bottom line and your next move

Does COBRA cover Wegovy? Yes, if your employer plan covered Wegovy before. The plan generally continues — same formulary, same copay, same prior authorization — though plan changes for active employees flow through to COBRA participants too. The trap most people fall into is paying ~$793/month for a COBRA premium just to protect a $25 copay, when NovoCare direct or an ACA Marketplace plan with subsidies would have cost a fraction of that.

The right move depends on three things you can verify in 30 minutes: whether your old plan actually covered Wegovy, what your exact COBRA premium is, and whether you have other coverage needs (a spouse, a planned procedure, a deductible already met). If COBRA wins on the math, elect it with confidence. If it doesn't, the ACA Marketplace Special Enrollment Period, NovoCare direct, Ro, and Sesame Care all give you access paths to FDA-approved Wegovy without the COBRA premium.

Still not sure which path is right for you?

Take our free 60-second GLP-1 matching quiz and get a personalized 3-step action plan.

Related guides on The RX Index

- Wegovy Savings Card: Qualify, Cost & Enroll (2026)

- Does Medicare Cover Wegovy for Weight Loss? 2026

- Wegovy Pill vs. Injection: Cost & Results 2026

- Ro Body Reviews (2026): Cost, Complaints & Verdict

- GLP-1 Providers That Accept Blue Cross: 7 Options

- Wegovy Providers That Take HSA or FSA (2026)

- GLP-1 With UnitedHealthcare: Every Path (2026)

What we actually verified for this guide

What we verified, dated May 13, 2026

- ✓COBRA continuation rules, including the up-to-102% premium cap, 60-day election window, 45-day initial payment window, and 30-day ongoing payment grace period -- verified directly with the U.S. Department of Labor's 'An Employee's Guide to Health Benefits Under COBRA' and the CMS COBRA Continuation Coverage fact sheet.

- ✓ACA Marketplace Special Enrollment Period (60 days before and after losing job-based coverage) and the rule that subsidies are based on full-year household income -- verified at HealthCare.gov.

- ✓NovoCare Pharmacy 2026 Wegovy self-pay pricing ($149-$399/month depending on dose, formulation, and promotional terms; starter pen $199/month promo runs through December 31, 2026; 4 mg tablet $149/month promo runs through August 31, 2026) -- verified directly at NovoCare.com on May 13, 2026.

- ✓Wegovy Savings Card 2026 terms (as little as $25/month, $100/month maximum savings per fill, government beneficiaries excluded) -- verified at Wegovy.com.

- ✓Employer GLP-1 coverage rates (16% / 30% / 43% by firm size) and 2025 employer-plan premium averages ($9,325 single / $26,993 family annual) -- Kaiser Family Foundation 2025 Employer Health Benefits Survey.

- ✓Ro Body membership pricing ($39 first month, $149/month ongoing, as low as $74/month with annual prepay) and insurance concierge scope -- verified at ro.co.

- ✓Sesame Care Costco partnership pricing ($349/month Wegovy injection / Wegovy pill from $149/month / Success by Sesame from $59/month annual) -- verified at sesamecare.com.

- ✓HSA eligibility for COBRA premiums -- IRS Publication 969 and IRS Publication 502.

- ✓FDA-approved Wegovy indications, safety, and contraindications -- Wegovy.com prescribing information.

- ✓FDA guidance on compounded semaglutide and salt-form distinctions -- FDA press announcements.

- ✓Medicare GLP-1 Bridge eligibility and 2026 launch details -- CMS Medicare GLP-1 Bridge program page.

Sources and citations

- 1.U.S. Department of Labor, "An Employee's Guide to Health Benefits Under COBRA" (29 CFR Part 2590)

- 2.U.S. Department of Labor, "FAQs on COBRA Continuation Health Coverage for Workers"

- 3.Centers for Medicare & Medicaid Services, COBRA Continuation Coverage fact sheet

- 4.HealthCare.gov, "COBRA coverage when you're unemployed" and "If You Lose Job-Based Health Insurance"

- 5.NovoCare.com, Wegovy cost and coverage pages (verified May 13, 2026)

- 6.Wegovy.com, "Wegovy Cost & Coverage Information" and prescribing information

- 7.Novo Nordisk press release, November 17, 2025, "Novo Nordisk Launches Introductory Self-Pay Offer for Wegovy and Ozempic for $199 per Month"

- 8.Kaiser Family Foundation, 2025 Employer Health Benefits Survey

- 9.Kaiser Family Foundation, "Medicaid Coverage of and Spending on GLP-1s"

- 10.GoodRx Research, "Live Updates: Insurance Coverage for GIP and GLP-1 Agonists Like Zepbound & Wegovy in 2026" (January 2026)

- 11.Ro Body pricing and insurance pages (ro.co, verified May 13, 2026)

- 12.Sesame Care, Costco Weight Loss Program announcement (sesamecare.com)

- 13.IRS Publication 969 (Health Savings Accounts and Other Tax-Favored Health Plans)

- 14.IRS Publication 502 (Medical and Dental Expenses)

- 15.CMS, "Medicare GLP-1 Bridge" program page

- 16.U.S. Food and Drug Administration, press announcements and consumer updates on compounded GLP-1 products and semaglutide salt forms

- 17.Public Reddit threads (r/HealthInsurance, r/Semaglutide) -- used for voice-of-customer reference only, not for medical, legal, or insurance claims

About The RX Index: The RX Index is a pricing intelligence and comparison resource for GLP-1 telehealth providers. We verify pricing, coverage, and policy directly from primary sources and update our guides quarterly or sooner when material changes occur.

Affiliate disclosure: This page contains affiliate links to Ro. When you enroll with a provider through our links, we may receive compensation. This does not influence our editorial conclusions, our pricing verification, or which providers we feature for a specific search intent.

Editorial standards: We do not pay for placement, do not accept paid testimonials, and do not include “medically reviewed by” claims unless a real, named clinician with verifiable credentials actually reviewed the content. This page was researched and written by The RX Index editorial team and is informational only — not medical, legal, tax, or insurance advice. Consult a qualified professional for advice specific to your situation.

Last verified: May 13, 2026. This page is updated quarterly minimum, and more often during NovoCare promotional pricing windows (through December 31, 2026 and August 31, 2026).

Your situation changes the answer

Find My GLP-1 Path

The right GLP-1 provider isn't the same for everyone. It depends on your state, your insurance and formulary, whether you want an FDA-approved or compounded medication, your preferred route (injection or oral), and your budget. Because a general answer can't resolve those for you, use The RX Index's Find My GLP-1 Path tool to get a personalized provider match with source-verified pricing before you choose.

- What it asks: your state, insurance situation, medication preference, budget, and support needs

- What you get: a personalized shortlist of GLP-1 providers matched to your situation, with verified pricing and the right questions to ask

- Cost: free · about 60 seconds · no signup