How to Bypass Step Therapy With UnitedHealthcare for GLP-1s

Published:

Updated monthlyThis guide reviews UnitedHealthcare and OptumRx public provider documentation, CMS Medicare Part D rules, the May 6, 2026 CMS announcement on the Medicare GLP-1 Bridge, current Lilly and Novo Nordisk cash-pay offers, U.S. Department of Labor benefit-claim regulations, and analysis from the Kaiser Family Foundation. We are not your lawyer or your doctor. We’re a team that maps how the rules work so you don’t waste weeks fighting a wall that has a door.

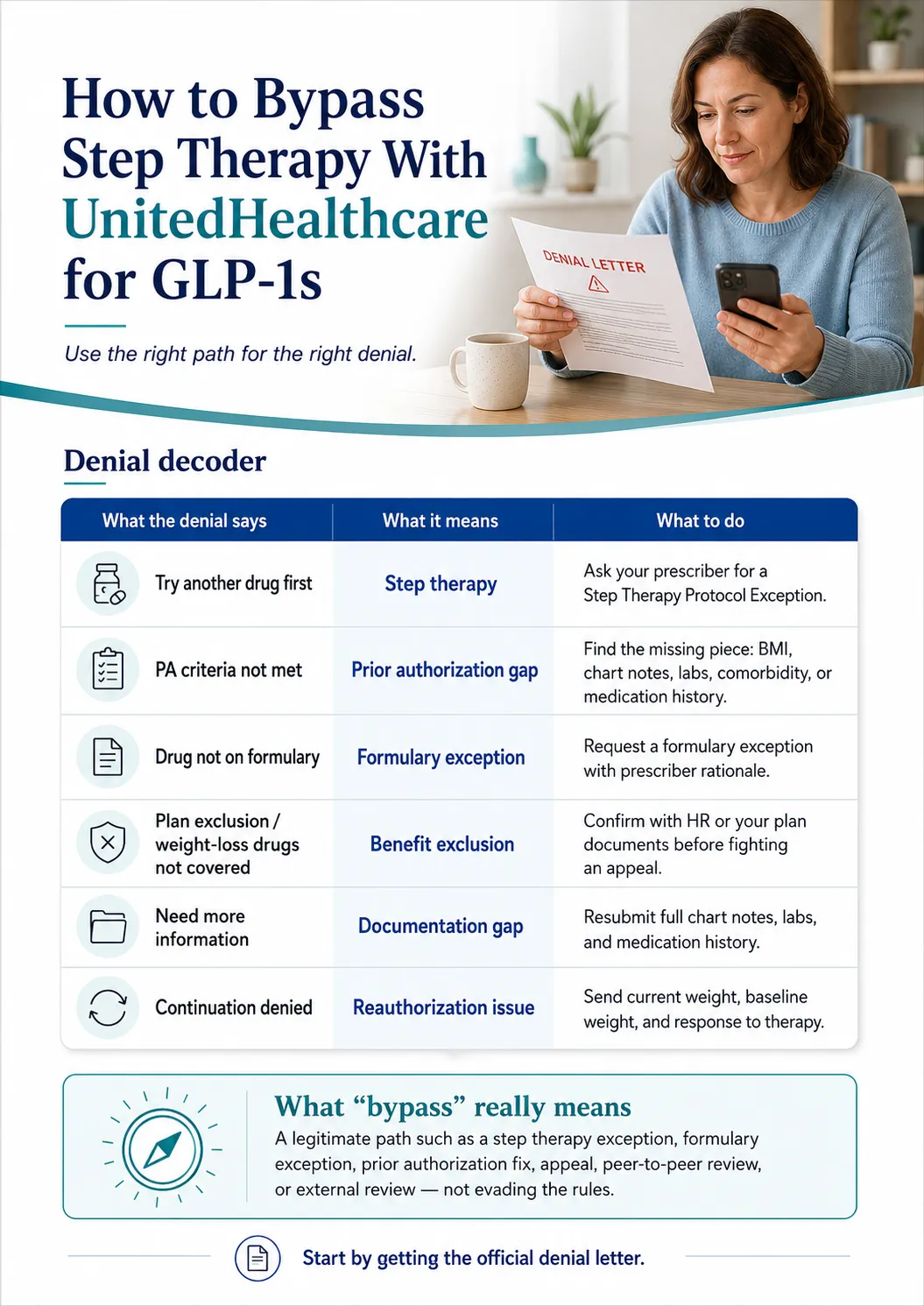

Got hit with a step therapy denial from UnitedHealthcare for your GLP-1? You’re not stuck. “Bypass” means using a legitimate path — a step therapy exception, formulary exception, prior authorization fix, internal appeal, peer-to-peer review, or external review. Once you know which kind of denial you actually got, the right next move usually becomes obvious.

| What your denial says | What it probably is | What to do first |

|---|---|---|

| “Try and fail another drug first” | Step therapy | Ask prescriber for a Step Therapy Protocol Exception |

| “Prior authorization criteria not met” | PA criteria gap | Find the missing piece (BMI, comorbidity, chart notes) and resubmit |

| “Drug not on formulary” / “nonformulary” | Formulary exception | Request formulary exception with prescriber rationale |

| “Plan exclusion” / “weight loss drugs not covered” | Benefit exclusion | Confirm with HR before fighting an appeal that can’t win |

| “Need more information” | Documentation gap | Resubmit with full chart notes, labs, medication history |

| “Continuation denied” | Reauthorization issue | Submit current weight, baseline weight, response to therapy |

Not sure which bucket your denial falls into? Take our free 60-second matching quiz and we’ll show you the right next step based on your plan, your medication, and your denial wording.

Decode my denial in 60 seconds →What “Bypass” Actually Means Here

Standalone answer: “Bypass” doesn’t mean evading insurance rules or lying on a form. It means asking UnitedHealthcare to waive or override the step therapy requirement using a process the plan is required to offer. The strongest exception requests are supported by your prescriber documenting that the required step drug failed, is unsafe, caused side effects, would likely be ineffective, or that UHC applied the wrong criteria.

Anyone selling you a “secret loophole” is selling you nothing. What actually exists is a structured appeal and external-review process for many private plans, a Medicare Part D formulary-exception process for Part D enrollees, and step therapy override rules in several states. UnitedHealthcare's own provider materials reference “Step Therapy Protocol Exception” requests when preferred-product criteria aren't appropriate for a patient.

The honest part — the one thing this page can’t fix

If your employer’s plan flat-out excludes weight-loss medications, no exception letter will save you. Step therapy says “Try this drug first.” A benefit exclusion says “We don’t cover this whole category.” A stronger letter doesn’t move that needle — only your employer changing the plan does. We’ll show you the cash-pay math near the bottom of this page. But most readers benefit from confirming which bucket they’re actually in first.

Step 1: Decode What UnitedHealthcare Actually Denied

Standalone answer: A “denial” from UnitedHealthcare can mean six different things, and each has a different fix. The fastest path is to read the exact wording on your denial letter or pharmacy rejection slip and match it to the right category before you ask your doctor to do anything.

The 6 Categories of UHC GLP-1 Denial

| Denial wording you might see | Category | Best next action |

|---|---|---|

| “Try and fail Wegovy/Saxenda/phentermine first” | Step therapy | Step Therapy Protocol Exception |

| “Prior authorization denied — criteria not met” | PA criteria gap | Identify missing piece, resubmit |

| “Drug is nonformulary” or “not on covered drug list” | Formulary exception | Formulary exception with rationale |

| “Plan exclusion” / “weight loss drugs not a covered benefit” | Benefit exclusion | Confirm plan document; HR route |

| “Insufficient information” / “missing documentation” | Documentation gap | Resubmit chart notes, labs, history |

| “Continuation/reauthorization denied” | Reauth issue | Send current weight + baseline + response |

Pharmacy Rejection vs. Official Denial Letter

A pharmacy counter rejection is almost never your final denial. It’s a real-time message from OptumRx saying “this won’t process under current rules.” It might mean PA required, wrong code, wrong pharmacy, step therapy required, or true exclusion.

Your appeal rights and deadlines almost always start from the official adverse determination letter — not the pharmacy rejection. So before you do anything else: call UnitedHealthcare or OptumRx and ask for the formal denial letter or coverage determination in writing. The number on the back of your card is the right one. For OptumRx prior authorization questions specifically, providers use 1-800-711-4555.

Why “not covered” is often fixable

When the pharmacy says “not covered,” that’s shorthand for any one of: PA required and not on file; tier mismatch; wrong pharmacy network; diagnosis code missing; quantity limit hit; or excluded category. Only the last one is unfightable through an exception. The other five may be fixable if your prescriber can submit the missing criteria, records, or exception rationale through the correct route. Don’t give up at the counter. Get the formal denial.

Step 2: Figure Out Which UnitedHealthcare Plan You Actually Have

Standalone answer: The UnitedHealthcare logo isn’t enough. Your real path depends on whether your denial came through OptumRx pharmacy benefits on a commercial employer plan, an Individual Exchange marketplace plan, Medicare Part D, a Medicaid/Community Plan, or a self-insured employer plan governed by ERISA. Each has different exception rules, deadlines, and rights.

The 3 Questions That Tell You Everything

1. Where did you get your UHC coverage?

- HealthCare.gov or a state marketplace → Individual Exchange plan (state law applies)

- Through your employer → continue to question 2

- You’re 65+ on UHC Medicare Advantage or Part D → Medicare plan (CMS rules apply)

- State Medicaid / managed Medicaid → Community Plan / Medicaid (state + federal rules apply)

2. If through your employer, ask HR: “Is our plan self-funded or fully insured?”

- Self-insured (ERISA) → Federal ERISA law applies. State step therapy override laws generally don’t. Your rights run through the plan document and federal external review.

- Fully insured → State insurance department regulates the plan. Your state’s step therapy override law (if it has one) applies.

3. If you’re not sure, look at your insurance card.

- “Administered by UnitedHealthcare” usually means self-insured (UHC just processes claims; your employer pays them)

- Cards that show UnitedHealthcare as the insurer usually mean fully insured

- If a third-party administrator is named, it’s likely self-insured

Your Plan Type → Your Path

| Plan type | Exception process | Appeal authority | Big caveat |

|---|---|---|---|

| Commercial fully insured | UHC + OptumRx + state law | State DOI external review | State step therapy override may apply |

| Commercial self-insured (ERISA) | UHC + OptumRx + plan document | Federal external review | State law generally doesn’t apply |

| Individual Exchange (marketplace) | OptumRx PA/exception per state | State DOI external review | State-specific timing rules apply |

| Medicare Part D | CMS coverage determination + exception | IRE → ALJ → MAC → Federal Court | Federal CMS timelines (72hr / 24hr expedited) |

| Medicare Advantage Part B drug | Medicare Advantage appeal rules | IRE → ALJ | Different timelines from Part D |

| Community Plan / Medicaid | State + UHC Community Plan rules | State Medicaid fair hearing | Program-specific; can vary by state |

Two coworkers in the same state, same diagnosis, same UHC card design can have completely different exception rights. The ERISA preemption rule keeps most state insurance protections from applying to self-insured employer plans — the single most underexplained fact for UHC members fighting denials.

Step 3: The 5 Medical Reasons UHC Accepts for a Step Therapy Exception

Standalone answer: Federal CMS rules and most state step therapy override laws recognize five medical grounds for an exception: contraindication, prior failure or intolerance, expected ineffectiveness, stability on current therapy, or that the step requirement is not in your medical interest. The strongest exception requests cite the specific ground, attach proof, and use the language UHC’s reviewers are trained to scan for.

Ground 1

Contraindication

The required step drug is medically dangerous for you.

Examples: Personal or family history of medullary thyroid carcinoma (MTC) or MEN2. Documented severe allergic reaction to phentermine. Documented severe GI disease. Pregnancy.

What your doctor needs: Chart note documenting the contraindication. If family history, the family member, condition, and date documented.

Ground 2

Documented prior failure or adverse reaction

You’ve already tried the step drug and it didn’t work, or it caused side effects that made you stop.

Examples: Tried Saxenda 2023, lost less than 3% body weight after 6 months. Tried phentermine, developed insomnia and elevated blood pressure, stopped at week 4. Tried Wegovy 2024, severe persistent nausea preventing dose escalation.

What your doctor needs: Pharmacy fill history, prior chart notes, weight log if available, dates and doses, reason for stopping. Always request prior records before submitting.

Ground 3

Likely to be ineffective

The step drug is unlikely to work for your specific clinical profile.

Examples: Severe insulin resistance with T2D requiring stronger glycemic control. PCOS with metabolic features the lower-tier drug doesn’t address. BMI well above the threshold where a particular AOM typically performs.

What your doctor needs: Chart note with reasoning, ideally referencing a clinical guideline (ADA Standards of Care, AACE/ACE Obesity Algorithm).

Ground 4

Stable on current therapy

You’re already on the requested drug — through samples, a prior insurance plan, cash-pay, or any other path — and forcing a switch would destabilize your treatment.

Examples: Started Wegovy on a previous insurance plan, lost 18% body weight, maintained for 9 months — switching back to Saxenda risks weight regain.

What your doctor needs: Current prescription record, weight progression chart, side-effect tolerability log, documentation that you’re meeting clinical goals.

Ground 5

Step requirement is not in your medical interest

The catch-all. Use it when the first four grounds don’t quite fit but the prescriber can argue clinical inappropriateness.

Examples: History of disordered eating where stimulant-class drugs (phentermine, Qsymia) carry elevated risk. Documented anxiety where phentermine could worsen symptoms.

What your doctor needs: A detailed letter of medical necessity stating why the step protocol is wrong for this specific patient, citing relevant clinical considerations.

Need help organizing your prescriber’s exception packet? Answer 5 questions and we’ll generate a one-page document you can email to your doctor’s office today.

Build my prescriber checklist →Step 4: What Evidence Your Prescriber Actually Needs to Gather

Standalone answer: UHC’s reviewers don’t read every word of a generic appeal letter. They scan for specific data points that match the plan’s criteria: diagnosis with ICD-10 codes, BMI, comorbidities, prior medication trials with dates, lifestyle modification documentation, and a specific exception ground.

Editorial checklist based on UHC’s published criteria and common documentation gaps. Not every item is required for every plan — your denial letter and your specific UHC criteria control what’s actually needed.

| Evidence item | Why UHC reviewers look for it |

|---|---|

| Denial letter or PA denial reason | Shows the exact rule being challenged |

| Requested medication and FDA-approved indication | Connects the drug to a covered diagnosis |

| Recent BMI and weight record | UHC commercial weight-loss criteria use BMI thresholds (typically ≥30, or ≥27 with comorbidity) |

| Comorbidity documentation | Hypertension, dyslipidemia, type 2 diabetes, sleep apnea, established cardiovascular disease for certain Wegovy requests, MASH with F2/F3 fibrosis for Wegovy injection where applicable, moderate-to-severe obstructive sleep apnea for Zepbound where applicable |

| Prior medication trials | Drug names, doses, dates started/stopped, outcome, reason for stopping |

| Lifestyle modification documentation | UHC criteria reference adjunct use with reduced-calorie diet and physical activity for many AOMs |

| Recent labs if relevant | Tied to denial reason, diagnosis, or prescriber rationale |

| Pharmacy fill history | Especially if the exception relies on prior failure |

| Letter of medical necessity | Names the exception ground and ties facts to UHC’s criteria |

What NOT to include

- Internet template language without patient-specific facts

- Exaggerated symptoms not supported by the chart

- Claims your doctor can’t actually verify

- Anything misleading about your medical history

False or unsupported information on an insurance form isn’t a “bypass” — it’s fraud. Every exception ground above is winnable with truthful, well-organized documentation.

Step 5: How to Submit the Exception to OptumRx

Standalone answer: Your prescriber’s office submits the exception — usually electronically through OptumRx’s provider portal, CoverMyMeds, by fax, or by phone. The OptumRx prior authorization line is 1-800-711-4555. Your job is to call UHC for the formal denial reason and exact criteria, gather your records, and make submission as easy as possible for your doctor’s staff.

Exact Script for Your Doctor’s Office

“My UnitedHealthcare/OptumRx denial says the medication requires step therapy. Could you submit a Step Therapy Protocol Exception or appeal? I have my denial letter, my prior medication history, and my chart notes ready to send. I can fax or email everything today. The submission can go to OptumRx through the provider portal, CoverMyMeds, or by fax.”

Saying the words “Step Therapy Protocol Exception” matters. That’s the term UHC uses internally. Doctors’ offices recognize it.

Exact Script for UnitedHealthcare or OptumRx

“Can you confirm exactly why this prescription was denied? Is it step therapy, prior authorization, nonformulary, quantity limit, or a plan exclusion? Please send me the written denial, the exact criteria used, the appeal deadline, and the submission route for a step therapy exception. Is expedited review available?”

Get a reference number for the call. Write down the rep’s first name. If the answer changes between calls (it sometimes does), you have a record.

Submission Routes for the Prescriber’s Office

- –OptumRx provider portal — Typically the fastest electronic option

- –CoverMyMeds — Electronic — used by many doctor’s offices

- –Fax — Slower but still common

- –Phone: 1-800-711-4555 — For prior authorization questions

Check your UHC coverage with Ro’s free GLP-1 Coverage Checker

Ro says its coverage checker contacts your insurance company and sends a personalized coverage report — including whether prior authorization is required and available copay or cost estimates. The coverage check does not submit a request for treatment or write a prescription.

Honest caveat: Ro can help check coverage and prepare prior-authorization paperwork, but no telehealth provider can guarantee UHC approval or override a true plan exclusion. What Ro can do is reduce the paperwork load on you and your doctor.

Get Ro’s free GLP-1 Insurance Coverage Checker → (sponsored affiliate link, opens in a new tab)Sponsored · We may earn a commission · No prescription submitted by using the checker

Step 6: How Long UnitedHealthcare Has to Answer You

Standalone answer: Federal CMS rules give Medicare Part D plans 72 hours for standard exceptions and 24 hours for expedited (urgent) exceptions after the prescriber’s supporting statement is received. Commercial and Exchange plan timelines vary by state and plan type. Self-insured employer plans follow ERISA timelines and the plan document.

| Plan type | Standard | Expedited (urgent) | Source |

|---|---|---|---|

| Medicare Part D exception | 72 hrs after supporting statement | 24 hrs after supporting statement | CMS |

| Medicare Part D redetermination | 7 calendar days | 72 hours | CMS |

| UHC Individual Exchange — Colorado | 3 business days | 24 hours | UHC QRG |

| UHC Individual Exchange — Florida | 15 days | 72 hours | UHC QRG |

| Commercial fully insured | Plan + state-specific | Plan + state-specific | Ask UHC; check denial letter |

| Commercial self-insured (ERISA) | Plan document controls | Plan document controls | Plan document; SPD |

| UHC pre-service appeal | Varies | Expedited may apply when standard review could seriously jeopardize health | UHCProvider.com |

When to ask for expedited (urgent) review

Federal rules and most state laws define “urgent” as: the standard timeframe could seriously jeopardize life, health, the ability to regain maximum function, or unmanaged severe pain. For most GLP-1 cases, expedited classification is rare. But it can apply in narrow situations — uncontrolled type 2 diabetes with rising HbA1c, documented cardiovascular event with ASCVD risk reduction need, severe untreated obstructive sleep apnea where Zepbound has an FDA-approved indication. If your clinical situation supports it, your doctor can request expedited review explicitly.

If they miss the deadline

A missed deadline is an escalation trigger — not a guaranteed approval. Ask for the written decision, cite the missed deadline, and request the next appeal or external-review route in writing. Save every reference number and confirmation. For Medicare Part D specifically: federal rules require that a missed exceptions deadline be treated as an adverse coverage determination that must be forwarded to the Independent Review Entity (IRE) — not as automatic approval.

Step 7: How to Write the Appeal / Letter of Medical Necessity

Standalone answer: A successful step therapy appeal letter maps your patient-specific facts to UHC’s exact denial reason. It identifies the requested drug, the covered diagnosis, the exception ground, the documented evidence, and asks for a specific action.

The 6-Part Structure

- 1Patient identifiers and plan info — Name, DOB, member ID, group number, RxBIN, RxPCN

- 2Requested medication and diagnosis — Drug name + strength + ICD-10 codes for the indication

- 3Denial reason and the exact criteria UHC cited — Quote the denial letter back at them

- 4The exception ground — Name one of the five and tie evidence to it

- 5Supporting records — Chart notes, labs if relevant, baseline and current weight, comorbidities, pharmacy history, prior trial documentation

- 6Specific request — “Please approve a step therapy exception / formulary exception / prior authorization for [drug name + dose]”

A Short Message You Can Send Your Prescriber

“Hi — I received a UHC/OptumRx denial for [drug name] because of [step therapy / PA / nonformulary]. I’ve attached the denial letter, my pharmacy fill history, and the chart notes from my previous prescriber. I think a [step therapy exception / formulary exception / appeal] may be appropriate — could you review and let me know what additional records you’d need to submit? I’m happy to help gather anything missing.”

The 4 Mistakes That Slow Appeals Down

- 1.Appealing without the formal denial letter — you’re guessing at what to address

- 2.Not knowing whether the denial is PA, step therapy, nonformulary, or exclusion — different denials need different fixes

- 3.Sending a generic template without patient-specific medication history — reviewers tune those out

- 4.Missing the appeal deadline. For ERISA group health plans, DOL guidance says claimants generally must be given at least 180 days after an adverse benefit determination to appeal. For Medicare Part D redetermination, the filing window is generally 65 calendar days. Don’t go from memory — read the letter.

Need a deeper walkthrough of the medical necessity letter itself? See our GLP-1 Letter of Medical Necessity guide.

Step 8: What If UHC Says Try Wegovy, Saxenda, Phentermine, or Metformin First?

Standalone answer: Your denial letter determines which drug UHC/OptumRx is treating as the required step. Whether the requirement is fightable depends on whether you’ve already tried the step drug, whether it’s clinically appropriate for you, and whether the prescriber can document a valid exception ground.

“Try phentermine or Qsymia before Zepbound”

Phentermine and phentermine/topiramate (Qsymia) can be required step drugs in some plans. UHC announced a 2025 update for certain Massachusetts Senior Care Options and One Care Community Plan members adding Zepbound prior authorization with phentermine as a step for new users. That policy is program-specific — your plan may not work the same way.

When to fight: Documented contraindication (uncontrolled hypertension, severe anxiety, history of substance use disorder), prior trial failure with side effects documented, or drug-drug interaction.

“Try Wegovy or Saxenda before Zepbound”

This denial pattern is reported frequently in patient communities. Real patients describe getting “rejected because I need to try 3 out of 4 (orlistat, Qsymia, Saxenda or Wegovy) before I can get Zepbound” and “denied my PA request for Zepbound saying I needed to try and fail at either Wegovy or Saxenda.”

When to fight: You’ve already tried Saxenda or Wegovy at a different practice or pharmacy (pull those records), you have a documented intolerance to liraglutide-class GLP-1s, or your prescriber documents why a Saxenda trial is clinically inappropriate for your specific case.

“Try metformin before Ozempic or Mounjaro”

If your diabetes GLP-1 denial requires metformin history, have the prescriber document prior use, intolerance, contraindication, or inadequate response with HbA1c and chart-note support.

When to fight: Chronic kidney disease with eGFR below 30 (metformin contraindicated), severe GI intolerance previously documented, or prior metformin trial with inadequate glycemic control documented in HbA1c records.

“Try Saxenda before Wegovy”

Less common but real. The exception grounds are similar to the Wegovy-before-Zepbound case.

When to fight: Prior trial, intolerance, contraindication, or clinical inappropriateness — same framework applies.

Step 9: When the Problem Is a Benefit Exclusion, Not Step Therapy

Standalone answer: A true benefit exclusion means your specific UHC plan doesn’t cover weight-loss medications as a category. A 2026 Business Group on Health survey found 67% of surveyed employers currently cover GLP-1s for weight management — meaning a meaningful share still don’t. If your plan is in the don’t-cover bucket, an exception letter generally cannot override the plan document.

How to Confirm a True Exclusion (in One Phone Call)

Call UnitedHealthcare and ask exactly this:

“Is this medication denied because prior authorization criteria weren’t met, or because weight-loss medications are excluded from my plan?”

You can also check your Summary of Benefits and Coverage (SBC). If it lists “weight-loss drugs” or “anti-obesity medications” under “What this plan does NOT cover,” you have an exclusion.

The Covered-Indication Path

The same brand can be covered for a different diagnosis, even on plans that exclude weight-loss-only coverage:

Wegovy

FDA-approved to reduce the risk of major adverse cardiovascular events in adults with established cardiovascular disease and obesity or overweight

Some plans that exclude weight-loss-only coverage will still cover Wegovy under that indication.

Zepbound

FDA-approved for moderate-to-severe obstructive sleep apnea in adults with obesity

Some plans that exclude weight-loss-only coverage will still cover Zepbound under the OSA indication.

Mounjaro / Ozempic

FDA-approved for type 2 diabetes

Typically evaluated under diabetes coverage criteria rather than weight-loss-only criteria — though prior authorization and plan rules can still apply.

This is a real path, and it requires honest medical documentation. Your prescriber decides if you actually qualify — not the internet, not us.

Employer-Sponsored Plan Escalation

If your plan is self-insured and excludes the drug class, the people who can change that are inside your company, not inside UnitedHealthcare:

- Formal request via HR — cite that 67% of large employers covered some form of GLP-1 for weight management in 2026 per the Business Group on Health survey

- Reference similarly-situated employer benefits — “Companies in our industry of our size are increasingly covering AOMs”

- Bring the ROI argument — productivity, absenteeism, downstream cardiovascular cost reduction

- Time it to open enrollment — self-insured employers can sometimes modify benefits mid-year, but most do it at renewal

Do State Step Therapy Laws Apply to Me?

Standalone answer: State step therapy override laws may help if your plan is fully insured or an Individual Exchange plan, but they generally don’t control self-insured ERISA employer plans because of federal preemption. Start by confirming plan type before relying on state-law override language.

State step therapy laws vary widely. What’s universal is this: if your plan is self-insured ERISA, the state’s law generally doesn’t bind your plan. Your plan document and federal external review do. Practical move: call your state insurance department’s consumer help line and ask whether your specific plan is regulated by the state. They can tell you in one call whether your state’s protections actually apply to you.

Step 10: If Your First Appeal Gets Denied

Standalone answer: A first denial is not the end. Depending on your plan type, you have access to internal appeals, peer-to-peer review with a UHC clinical pharmacist or medical director, Medicare Part D redetermination, and external review by an Independent Review Organization (IRO). Each route has its own deadline and its own documentation requirements.

Read the second denial carefully

“Information was missing” → Resubmit with the gap filled. Often faster than appealing. | “Reviewed and denied on clinical grounds” → Move to internal appeal, then peer-to-peer. | “Plan does not cover this category” → You’re in exclusion territory. Different path entirely.

Internal appeal

For ERISA group health plans, DOL guidance says claimants generally must be given at least 180 days after an adverse benefit determination to appeal. Medicare Part D redetermination is generally 65 calendar days. Strengthen with: updated letter of medical necessity, any new clinical information, pharmacy fill history not previously included, reference to clinical guidelines (ADA, AACE/ACE).

Peer-to-peer review

Your prescriber can request a peer-to-peer review — a phone conversation with a UHC clinical pharmacist or medical director. This is the often-overlooked move. If the denial notice offers peer-to-peer review, your prescriber can use that route to add clinical context that didn’t fit the original form fields. Always ask whether peer-to-peer is available when an appeal is denied for ambiguous reasons.

External review (IRO)

Under the Affordable Care Act, after exhausting internal appeals you have the right to external review by an Independent Review Organization — a third party not affiliated with UHC. Most state insurance departments publish IRO request forms; for ERISA self-insured plans the federal external review process applies. For Medicare, the appeal levels include reconsideration by the Independent Review Entity (IRE) and further appeal options.

What Changes for Medicare Readers After July 1, 2026

Medicare GLP-1 Bridge — $50/month (July 1, 2026 – Dec 31, 2027)

Standard Medicare Part D generally has not covered GLP-1s for weight loss alone. CMS announced the Medicare GLP-1 Bridge on May 6, 2026. This is the biggest Medicare coverage shift in years.

- ✓Eligible Part D beneficiaries may access certain GLP-1 medications at $50 per monthly supply

- ✓Eligible plans: beneficiaries must be enrolled in a qualifying PDP or MA-PD plan participating in the Bridge

- ✓Eligible medications: Foundayo, Wegovy injection and tablets, and Zepbound KwikPen. Zepbound single-dose vials and single-dose pens are NOT included.

- ✓PA criteria: eligible beneficiaries must meet criteria including age, BMI, lifestyle modification, and other qualifying clinical criteria

- ✓This operates outside the normal Part D benefit — confirm participation with your specific plan before July 1

For the full Bridge program breakdown, see our CMS BALANCE Model GLP-1 Explained (2026–2027).

Step 11: The Cash-Pay Math — When Skipping the Fight Is the Smart Move

Standalone answer: If your plan covers Wegovy or Zepbound at a low copay, fighting the denial is usually worth weeks of effort. If your plan would only get you to a high copay, or your plan excludes the drug class entirely, cash-pay branded GLP-1s may beat the appeal math. Current cash-pay starts at $199/month for certain Wegovy starter doses through NovoCare and $299/month for the Zepbound 2.5 mg vial through Lilly’s Self Pay Journey.

Source-checked May 8, 2026. Prices and offer conditions change — confirm directly with the manufacturer or provider before purchase.

| Path | Medication / Dose | Monthly cost | Key caveat |

|---|---|---|---|

| LillyDirect — Self Pay Journey | Zepbound vial 2.5 mg (initiation) | $299/mo | Self-pay; offer conditions apply |

| LillyDirect — Self Pay Journey | Zepbound vial 5 mg | $399/mo | Self-pay; offer conditions apply |

| LillyDirect — Self Pay Journey | Zepbound vial 7.5 mg | $449/mo when timing conditions met; $499/mo otherwise | Self-pay |

| LillyDirect — Self Pay Journey | Zepbound vial 10 / 12.5 / 15 mg | $449/mo when timing conditions met; $699/mo otherwise | Self-pay |

| NovoCare | Wegovy pens 0.25 / 0.5 mg | $199/mo first 2 fills (through December 31, 2026); then $349/mo | Cash offer; new patients |

| NovoCare | Wegovy pens 1 / 1.7 / 2.4 mg | $349/mo | Cash offer |

| NovoCare | Wegovy HD 7.2 mg | $399/mo | Cash offer |

| NovoCare | Wegovy tablets 1.5 mg / 4 mg | $149/mo (4 mg promo through Aug 31, 2026, then $199/mo) | Lowest verified FDA-approved monthly price |

| Ro Body Membership | Zepbound, Foundayo (orforglipron) | $39 first month, then $149/mo; or as low as $74/mo with annual plan upfront | Medication not included in membership fee |

| Sesame Care | Wegovy pill, Zepbound KwikPen, Wegovy pen, Foundayo | Member pricing varies | Verify availability on Sesame’s live page before purchase |

The Break-Even Calculation in Plain English

Scenario A — Your plan covers Wegovy at $50/mo copay

Cash-pay equivalent for ongoing 1–2.4 mg Wegovy pens is $349/mo. Difference: ~$300/mo.

→ Fight.

Scenario B — Your plan covers Wegovy at $250/mo copay

Cash-pay equivalent is $349/mo. Difference is ~$100/mo. If the appeal takes 8 weeks, the math is closer to a wash.

→ Fight if you have time, switch to cash if you don’t.

Scenario C — Your plan excludes the drug class

No appeal will win. Difference is $0/mo (not getting it through insurance) versus $199–$349/mo cash-pay for Wegovy or $299–$449/mo for Zepbound vials.

→ Skip the fight. Go cash-pay from day one.

Why Ro fits this specific reader

- Free GLP-1 Insurance Coverage Checker — Ro contacts your insurance and sends a personalized coverage report without submitting a prescription

- Cash-pay branded option — if the appeal fails or the plan excludes coverage, Ro offers Zepbound and Foundayo on the same platform with the same prescriber

- Ro Body Membership: $39 for the first month, then $149/month — or as low as $74/month with annual plan paid upfront. Medication is not included in the membership fee.

No telehealth provider — Ro included — can guarantee UnitedHealthcare approval or override a true plan exclusion. What Ro can do is take the paperwork burden off you and your doctor’s office, which is often the actual reason exceptions get stuck.

See what my UHC plan actually covers with Ro → (sponsored affiliate link, opens in a new tab)Sponsored · We may earn a commission · No prescription submitted by using the checker

Prefer a different platform?

Sesame Care lists Wegovy pill, Zepbound KwikPen, Wegovy pen, and Foundayo on its current online weight-loss page, with Costco-member pricing referenced for Ozempic and Wegovy. Verify current availability on Sesame’s live page before purchase.

Browse Sesame Care GLP-1 options → (sponsored affiliate link, opens in a new tab)Sponsored · We may earn a commission

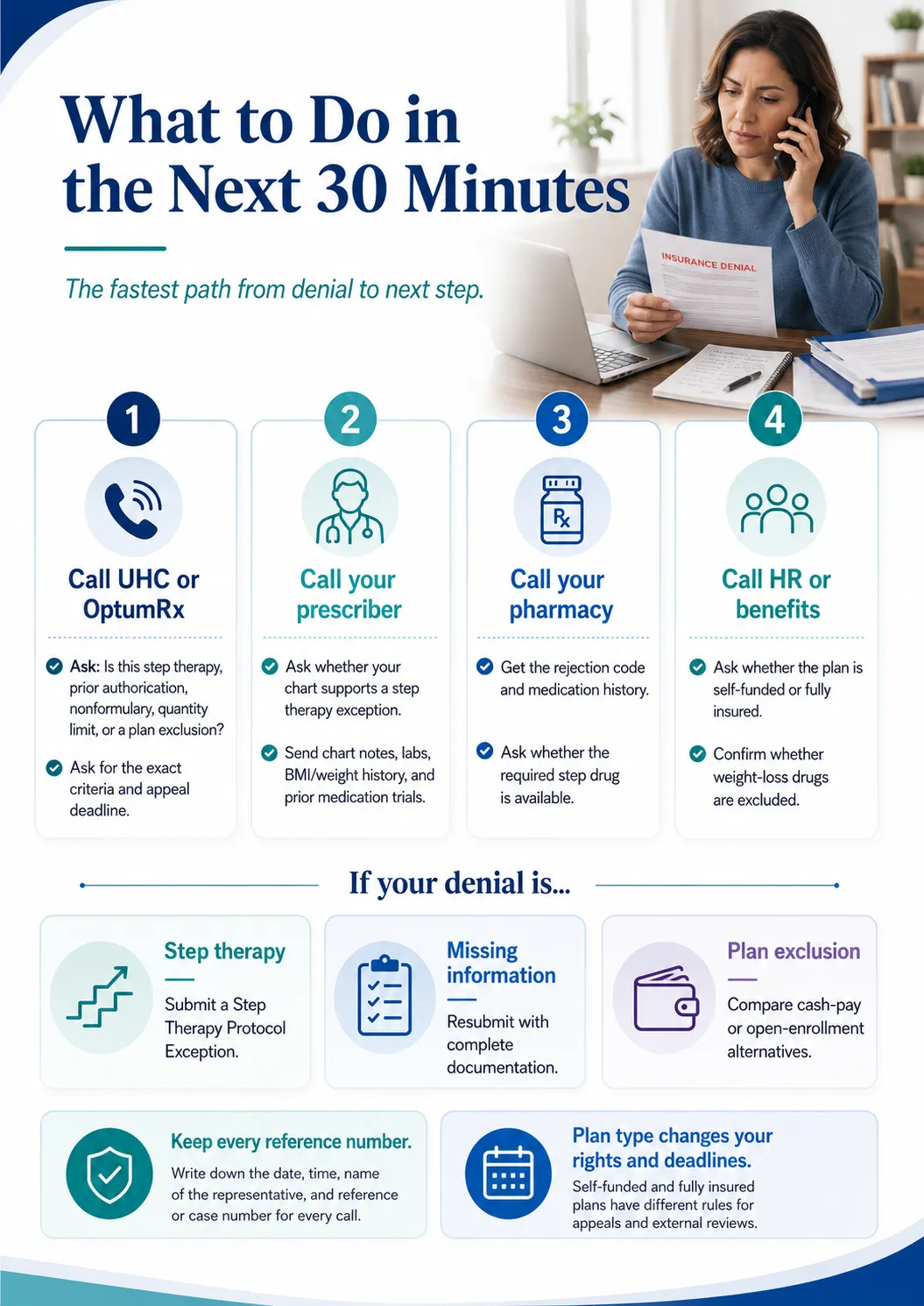

Step 12: The 4-Contact Checklist — Do This in the Next 30 Minutes

Standalone answer: The fastest move from “denial in hand” to “real next step” is a four-call sequence: UHC/OptumRx for the denial category and criteria, your doctor for the exception packet, your pharmacy for the rejection details and medication history, and your employer’s HR or benefits team to confirm whether the drug class is excluded.

Call 1

Call UnitedHealthcare or OptumRx

Number on the back of your card. For OptumRx PA questions specifically: 1-800-711-4555.

- “Is this denial step therapy, prior authorization, nonformulary, quantity limit, or a plan exclusion?”

- “What criteria were used?”

- “What is the appeal deadline?”

- “Where should the prescriber submit the exception?”

- “Is expedited review available?”

- Get a reference number. Write it down.

Call 2

Call your prescriber’s office

If the office tells you they “don’t do appeals,” ask whether they have an in-house pharmacist or PA coordinator. Most large practices do.

- “Can my chart support a step therapy exception?”

- “Do my records show prior failure, intolerance, contraindication, or clinical inappropriateness?”

- “Can you submit chart notes, labs, medication history, and a medical-necessity explanation?”

Call 3

Call your pharmacy

The call most readers skip. Pharmacies have your fill history in their system. Ten minutes can produce evidence your prescriber’s office didn’t have.

- “What was the rejection code on my last fill attempt?”

- “Is the required step drug actually available?”

- “Can you provide my medication history or documentation of previous fills?”

Call 4

Call your employer’s HR or benefits team

For a self-insured employer plan, this call sometimes matters more than the call to UHC.

- “Are weight-loss medications excluded from our plan?”

- “Is our plan self-insured or fully insured?”

- “Is there an employer exception process beyond what UHC offers?”

- “Is there a separate pharmacy-benefit administrator?”

The 30-Minute Action Plan

- 1Save the denial letter or pharmacy rejection details

- 2Identify the denial type (use the decoder table at the top)

- 3Identify your plan type — commercial fully insured, self-insured, Individual Exchange, Medicare Part D, Medicare Advantage, Medicaid

- 4Call UHC for the exact criteria, appeal deadline, and submission route. Get a reference number.

- 5Call your prescriber’s office with the denial in hand

- 6Pull your medication history — call old pharmacies and prescribers if needed

- 7Pull your chart notes, BMI/weight history, comorbidity documentation, and any relevant labs

- 8Have your prescriber submit a Step Therapy Protocol Exception if the records support it

- 9Track submission date, confirmation, and reference number

- 10If denied again, use the denial reason to choose the next route — fix-and-resubmit, internal appeal, peer-to-peer, redetermination, or external review

Ready to put this in motion? Take the 60-second matching quiz and we’ll generate a personalized appeal checklist based on your plan type, your medication, and your denial wording.

Take the free 60-second matching quiz →Real Reader Experiences

Three real, attributed examples pulled from public Reddit threads. We use these only to show how denials are worded in practice — not as policy evidence. Your situation will turn on your specific plan, diagnosis, prescriber, and documentation.

“Rejected because I need to try 3 out of 4 (orlistat, Qsymia, Saxenda or Wegovy) before I can get Zepbound. I have UnitedHealth. Sucks.”

r/Zepbound user describing a typical UHC step-therapy denialStep therapy

“Denied my PA request for Zepbound saying I needed to try and fail at either Wegovy or Saxenda…”

r/Zepbound user, illustrating the most common UHC step-therapy framingStep therapy

“Denied because PCP didn’t include chart notes and labs… specialist submitted… approved.”

r/Mounjaro user, illustrating the documentation-gap denial pattern and how a more thorough submission cleared itDocumentation gap → resolved

How We Built This Guide

The RX Index is a pricing intelligence and comparison resource for GLP-1 telehealth providers. We don’t sell medication. We don’t write prescriptions. We map how the rules work.

This guide was built from:

- UnitedHealthcare and OptumRx public provider documentation — the clinical pharmacy guide, weight-loss medication PA notification, and Individual Exchange pharmacy QRG

- CMS Medicare Part D rules — formulary exception process and redetermination requirements

- CMS Medicare GLP-1 Bridge — May 6, 2026 announcement and demonstration details

- U.S. Department of Labor — ERISA group health plan benefit-claims procedure regulation

- eCFR — federal external review and Part D adverse-determination rules

- FDA — Wegovy cardiovascular indication, Zepbound OSA indication, and compounded GLP-1 statements

- Kaiser Family Foundation — analysis of ERISA preemption for self-insured employer plans

- Business Group on Health — 2026 employer survey on GLP-1 coverage

- UnitedHealth Group SEC filing — fee-based vs. risk-based commercial membership

- Public Reddit posts — used only as voice-of-customer language, never as policy evidence

| Review cadence | Elements updated |

|---|---|

| Monthly | Cash-pay pricing and provider claims |

| Quarterly | UHC/OptumRx policy, state step therapy laws, and CMS rules |

Frequently Asked Questions

- Can I bypass step therapy with UnitedHealthcare?

- Yes — through a step therapy exception, formulary exception, prior authorization fix, internal appeal, peer-to-peer review, or external review. The strongest requests are supported by your prescriber documenting why the required step drug failed, is unsafe, is likely ineffective, or shouldn’t be required for your specific situation.

- What is a step therapy exception?

- A step therapy exception is a formal request asking UHC to waive the requirement that you try a preferred medication first. UnitedHealthcare’s own provider guidance refers to “Step Therapy Protocol Exception” requests when preferred-product criteria don’t fit a patient.

- Who files a UHC step therapy exception?

- Usually the prescriber or the prescriber’s office submits the request because it requires clinical documentation. Your job as the patient is to gather the denial letter, prior medication history, pharmacy records, chart notes, and the appeal deadline — and bring it all to your appointment.

- What number does OptumRx use for prior authorization questions?

- For prior authorization questions, providers use 1-800-711-4555, listed on UnitedHealthcare’s clinical pharmacy and specialty drugs page. Members should call the number on the back of their UHC card for member-side questions.

- How long does a Medicare Part D step therapy exception take?

- CMS requires Part D plans to issue exception decisions generally within 72 hours for standard requests and 24 hours for expedited requests, after the prescriber’s supporting statement is received.

- What if UHC says my GLP-1 is excluded from coverage?

- That’s a benefit exclusion, not step therapy — and it’s harder to fight. Confirm with HR whether it’s a true categorical exclusion. If it is, your realistic options are switching plans at open enrollment, advocating with your employer to add coverage, looking for another covered indication (cardiovascular risk reduction for Wegovy, OSA for Zepbound, T2D for Mounjaro/Ozempic), or moving to cash-pay branded.

- Can Ro or another telehealth provider guarantee UHC approval?

- No. Ro and similar telehealth providers can help check coverage and prepare prior-authorization paperwork, but the plan decides coverage based on your specific benefits and clinical criteria. Be skeptical of anyone who claims they can guarantee approval — that’s not how insurance works.

- What if my plan is self-insured by my employer?

- Self-insured employer plans are generally governed by federal ERISA, which preempts state insurance laws — meaning your state’s step therapy override law generally doesn’t apply. You still have rights through the plan document, the federal appeal process, and federal external review.

- Can I use compounded GLP-1s while appealing UHC?

- That’s a decision for you and your clinician. The FDA has stated compounded drugs are not FDA-approved and are not reviewed for safety, effectiveness, or quality. If you explore that path, do it eyes-open and don’t let anyone tell you it’s “the same medication” as Wegovy, Zepbound, or Foundayo.

- How long should I keep fighting before going cash-pay?

- Use the break-even math. If your covered copay would be meaningfully cheaper than cash-pay branded ($199–$349/month for Wegovy, $299–$449/month for Zepbound vials), fighting is usually worth the wait. If the gap is small — or if your plan excludes the class entirely — cash-pay from day one is often the smart move.

- What if I miss the appeal deadline?

- You generally lose the right to that level of appeal. But you may still have other paths — submitting a fresh exception request based on new clinical information, requesting peer-to-peer review through your prescriber, or going cash-pay while you regroup. Don’t assume one missed deadline ends everything; ask UHC what’s still available.

- What if UHC misses its response deadline?

- Treat a missed deadline as an escalation trigger, not as automatic approval. Ask for the written decision, cite the missed deadline, and request the next appeal or external-review route in writing. For Medicare Part D, federal rules require that a missed exceptions deadline be forwarded to the Independent Review Entity as an adverse coverage determination.

- Does Medicare cover GLP-1s for weight loss?

- Standard Medicare Part D generally has not covered GLP-1s for weight loss alone. CMS announced the Medicare GLP-1 Bridge on May 6, 2026. Beginning July 1, 2026, eligible Part D beneficiaries may access certain GLP-1 medications for $50/month through a time-limited demonstration that runs through December 31, 2027. CMS says eligible drugs currently include Foundayo, Wegovy injection and tablets, and Zepbound KwikPen — Zepbound single-dose vials and single-dose pens are not included. Medicare also covers Ozempic and Mounjaro for type 2 diabetes, and Wegovy is covered under Part D for adults with established cardiovascular disease and overweight/obesity for cardiovascular risk reduction.

One Last Thing

You came here looking for a way around a wall. The wall is real. So is the door — it’s just not always easy to find.

If you’ve read this far, you know more about UnitedHealthcare’s step therapy process than most patients ever learn. That’s the actual leverage. The vast majority of denied GLP-1 patients give up at the pharmacy counter. The ones who get covered are the ones who knew which call to make, what their prescriber needed, and where their plan type changed the rules.

Still not sure which path is right for you?

Take our free 60-second matching quiz — answer a few questions about your insurance, state, medication, and denial wording, and we’ll show you a personalized action plan within minutes.

Take the free 60-second matching quiz →