Blue Cross Foundayo Coverage · Verified April 21, 2026

Blue Cross Foundayo Prior Authorization: Is Your Plan a PA Lane or an Exclusion Lane? (2026)

Published: · Last updated:

Sources: Excellus BCBS Policy PHARMACY-03, BCBS Massachusetts Focused Formulary communications, Independence Blue Cross provider bulletin, BCBS North Dakota weight-loss drug bulletin, FEP Blue/CVS Caremark, CMS Medicare GLP-1 Bridge FAQ, Foundayo Prescribing Information, Ro, LillyDirect.

The short answer

Blue Cross Foundayo prior authorization only works if your specific BCBS plan still covers weight-loss GLP-1s — and not every Blue plan does in 2026. Some Blue plans show a real PA path (Excellus BCBS names Foundayo in its weight-management policy). Some Blue plans explicitly excluded weight-loss GLP-1s for 2026 (BCBS Massachusetts Focused Formulary members; Independence Blue Cross fully-insured commercial members). And some plans use the Blue Cross logo but set their own drug coverage rules as self-funded employer plans, meaning your HR team — not the insurer — controls the answer.

Best for: Blue Cross Blue Shield commercial, ACA marketplace, or FEP Blue members trying to get FDA-approved Foundayo (orforglipron) covered for chronic weight management.

Key numbers: With Blue Cross coverage + the Foundayo Savings Card, eligible commercially insured patients can pay as little as $25/month. Under Lilly’s self-pay savings program, Foundayo runs $149 (0.8 mg), $199 (2.5 mg), $299 (5.5 mg and 9 mg), and $349 (14.5 mg and 17.2 mg). Savings card terms vary — check lilly.com/foundayo for current expiry dates.

Ro’s GLP-1 Insurance Coverage Checker queries your specific plan’s coverage status and tells you whether prior authorization is required. If it is, Ro’s insurance concierge submits the paperwork on your behalf.

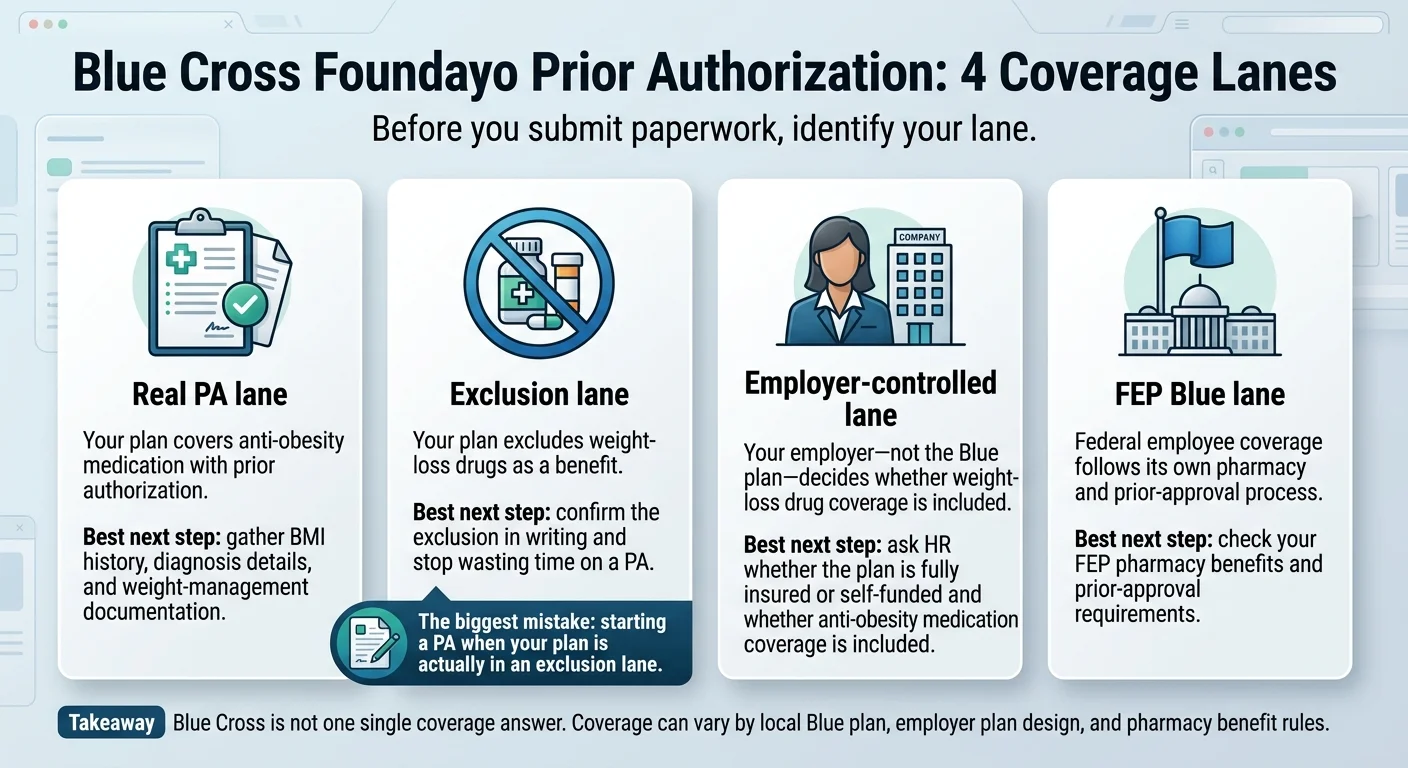

Blue Cross isn’t one answer. It’s four lanes.

Blue Cross Blue Shield is a federation of 33+ independent local companies, plus a separate Federal Employee Program administered through CVS Caremark, plus thousands of self-funded employer plans that carry the Blue logo but set their own drug coverage rules. That means “Does Blue Cross cover Foundayo?” has four different possible answers depending on which lane you’re in — and your first job is to figure out which lane your card belongs to before you or your doctor do any paperwork.

Your plan covers weight-loss GLP-1s with prior authorization. Meet the clinical criteria (BMI, comorbidities, documented weight-loss attempts, supervised program), submit the paperwork, get approved. Example: Excellus BlueCross BlueShield, whose weight-management pharmacy policy (Policy PHARMACY-03, last reviewed April 13, 2026) explicitly names Foundayo (orforglipron).

Next move: Gather BMI history, program enrollment proof, comorbidity codes; submit PA

Your plan removed weight-loss GLP-1s from the benefit entirely. No PA will approve what the plan doesn't cover. Example: BCBS Massachusetts notes that GLP-1 and GLP-1/GIP agonist drugs for anti-obesity management are not a covered benefit for members with the Focused Formulary effective January 1, 2026. Its broker materials confirm these exclusions can't be appealed through the medical-necessity review process.

Next move: Confirm exclusion in writing; pivot to Savings Card cash-pay path

Your plan is self-funded by your employer, which means the insurer is just processing claims — the employer decides whether weight-loss GLP-1s are included. A fully-insured plan and a self-funded plan with the same Blue Cross logo can give opposite answers. Example: BCBS North Dakota published that fully-insured non-grandfathered large-group plans remove weight-loss drug coverage at 2026 renewal, while self-funded groups choose.

Next move: Ask HR: "Is our plan fully-insured or self-funded? Did we include weight-loss drug coverage for 2026?"

You're a federal employee on the Blue Cross Blue Shield Service Benefit Plan. This is a separate beast administered through CVS Caremark with its own formulary and prior-approval process. The Retail Pharmacy Program routes PA questions through 1-800-624-5060.

Next move: Call FEP Retail Pharmacy Program at 1-800-624-5060; provider submits PA

Knowing which lane you’re in turns a frustrating maze into a 15-minute triage. We go deeper on Blue Cross GLP-1 coverage across the full drug class in our Blue Cross GLP-1 prior authorization guide. For a broader view of Foundayo insurance outside the BCBS system, see Does Insurance Cover Foundayo?

The Blue Cross Foundayo Lane Checker (2026)

Built from publicly available weight-management drug policies, member communications, and provider bulletins from major Blue Cross Blue Shield subsidiaries, verified April 2026. Rows marked policy pending mean the subsidiary hasn’t yet updated its published formulary documents to explicitly name Foundayo — the drug was FDA-approved on April 1, 2026, so many formularies are still catching up. Plan-level variance and employer customization can override the defaults shown.

Last verified April 21, 2026. Confirm your specific plan before acting on any row.

| Blue Cross lane | 2026 public signal | What it means for Foundayo | Fastest next move |

|---|---|---|---|

| Excellus BCBS (NY) | Policy PHARMACY-03 reviewed 4/13/2026 explicitly names Foundayo. BMI ≥40 OR BMI 35–39.9 with qualifying comorbidity. 3+ months in comprehensive weight-management program. 5% physician-verified weight loss needed at first recertification. Will not approve concurrent use with another GLP-1/GIP agonist. | Real PA lane. Meet criteria, submit documentation, get approved. | Gather BMI history, program enrollment proof, comorbidity codes; submit PA |

| BCBS Massachusetts (Focused Formulary) | GLP-1 / GLP-1-GIP anti-obesity drugs listed as non-covered benefit for Focused Formulary members effective 1/1/2026. Broker materials confirm the exclusion isn't appealable via medical-necessity review. Larger employer groups may add coverage as a buy-up rider. | Exclusion lane for affected members. Foundayo-specific listing policy pending. | Confirm exclusion in writing; ask HR about buy-up rider; cash-pay fallback |

| Independence Blue Cross (IBX, PA) | Effective January 1, 2025, fully-insured group and individual commercial members lost coverage for drugs prescribed solely for weight loss. GLP-1s remain covered with PA for other FDA-approved indications (type 2 diabetes, cardiovascular risk reduction). Still in effect for 2026. | Obesity-only exclusion lane. Foundayo for weight loss = not covered on affected IBX plans. Foundayo-specific formulary listing policy pending. | Confirm exclusion via member portal; explore diabetes-indication path if applicable |

| BCBS North Dakota | 2026 policy removes weight-loss drug coverage (GLP-1s and oral weight-loss meds) from fully-insured non-grandfathered large-group plans at renewal. Self-funded groups can include or exclude at the employer's discretion. Small-group and individual EHB plans retain coverage. | Employer-controlled lane for large-group members. | Ask HR: "Is our plan fully-insured or self-funded? Did we include weight-loss drug coverage for 2026?" |

| FEP Blue / FEHB Service Benefit Plan | Pharmacy benefits administered by CVS Caremark. Published weight-loss prior-approval framework for eligible members meeting criteria. PA submitted via Retail Pharmacy Program. Foundayo-specific listing on FEP materials reviewed policy pending as of April 2026. | Live prior-approval framework. Foundayo-specific listing policy pending. | Call FEP Retail Pharmacy Program at 1-800-624-5060 for formulary confirmation; provider submits PA |

| Blue Shield of California | Published fact sheet states GLP-1 weight-loss coverage restricted to Class III obesity members (BMI ≥40) enrolled in a comprehensive weight-management program (diet, exercise, behavior therapy). | Real but narrow PA lane. Foundayo-specific listing policy pending. | Confirm BMI ≥40; get program enrollment documented; submit PA |

| Anthem Blue Cross Blue Shield (multi-state) | Coverage varies significantly by state and employer plan. Anthem BCBS Nevada large-group fully-insured plans do not cover GLP-1 weight-loss benefit. Other state plans typically cover for diabetes with PA; weight-loss coverage usually requires employer opt-in. | Mixed — mostly employer-controlled or excluded. | Check Anthem member portal drug lookup tool for your specific plan |

| BCBS Michigan | GLP-1 weight-loss coverage ended for fully-insured large-group commercial members effective January 1, 2025. Still in effect for 2026. Self-funded employer plans may retain coverage. | Exclusion lane for most large-group plans. | Ask HR about self-funded status; cash-pay fallback if excluded |

| BCBS Illinois / Texas / Oklahoma / Montana / New Mexico (HCSC) | PA processed via Prime Therapeutics ePA. Typical weight-loss GLP-1 PA criteria: BMI ≥30, or ≥27 with comorbidity; documented prior weight-loss attempts. Self-funded employer opt-out is common. Foundayo-specific listing policy pending. | Real PA lane on covered employer plans. | Check Availity portal; provider gathers documentation and submits PA |

If your specific subsidiary or employer plan isn’t shown, the safer answer is: don’t assume coverage or exclusion — verify directly.

Skip the matrix hunt — get your specific Blue Cross Foundayo coverage checked in 2 minutes.

Run the free coverage check with Ro → (sponsored affiliate link, opens in a new tab)Ro queries your plan directly and tells you whether a PA is required before you or your doctor lift a finger.

What does the public Blue Cross paperwork actually say?

Across the Blue Cross system, published weight-management drug policies reveal five distinct coverage patterns for Foundayo in 2026: explicit inclusion (Excellus), benefit- category exclusion on specific formularies (BCBS Massachusetts Focused Formulary), obesity-only exclusion with other-indication coverage retained (Independence Blue Cross), employer-controlled rollback (BCBS North Dakota), and a separate federal prior-approval framework (FEP Blue). Understanding what each one actually says — not what a phone rep summarizes — is what separates a successful PA from a wasted month.

Excellus BCBS: the real PA lane, in detail

Excellus’s weight-management pharmacy policy (Policy PHARMACY-03, last reviewed April 13, 2026) is the single clearest public document we found that explicitly names Foundayo. The criteria are tighter than you’ll see in older Wegovy-era policies.

Initial approval requires ALL of the following:

- ✓Class 3 obesity (BMI ≥40 kg/m²), OR Class 2 obesity (BMI 35–39.9 kg/m²) with at least one qualifying comorbidity: cardiovascular disease, dyslipidemia, gallstones, gynecological abnormalities, hypercholesterolemia, hypertension, metabolic syndrome, MAFLD, pulmonary hypoventilation, obstructive sleep apnea, stress incontinence, type 2 diabetes, or weight-bearing joint arthropathy

- ✓Documentation of current enrollment in a qualified comprehensive weight-management program for at least 3 consecutive months

- ✓Proof of current and prior participation in the program (receipt, certificate, dietary/exercise logs)

- ✓Will not be approved for concurrent use with any other GIP or GLP-1 receptor agonist

Recertification requires:

- ✓Physician-verified 5% weight loss from baseline at the initial recertification window

- ✓Continued enrollment in the weight-management program

- ✓Ongoing attestation of lifestyle modification participation

BCBS Massachusetts: the Focused Formulary exclusion

BCBSMA’s broker/account FAQ confirms that GLP-1 and GLP-1/GIP agonist drugs for anti-obesity management are a non-covered benefit for members with the Focused Formulary effective January 1, 2026 — and that this benefit exclusion isn’t reviewable through the medical-necessity appeal process. Larger employer groups may add weight-loss drug coverage as a buy-up rider, which means the same BCBSMA card can mean coverage or exclusion depending on the employer’s rider election. For Foundayo specifically, BCBSMA’s policy document hasn’t yet been updated to explicitly name orforglipron (policy pending). But the Focused Formulary exclusion pattern is what would apply: if your employer didn’t buy the rider, Foundayo for weight loss is not covered, and no paperwork will change that answer.

Independence Blue Cross (IBX): the obesity-only split

IBX’s public provider communications confirmed that effective January 1, 2025, fully-insured group and individual commercial members no longer have coverage for drugs prescribed solely for weight loss. That exclusion remains in effect for 2026. The nuance: GLP-1s remain covered with prior authorization when prescribed for FDA-approved indications other than weight management — type 2 diabetes and cardiovascular risk reduction being the main ones.

Practical implication for Foundayo: Foundayo is currently FDA-approved only for chronic weight management. Affected IBX members can’t pivot to a different indication for Foundayo itself. Alternative GLP-1s like Ozempic or Mounjaro retain a covered path through the diabetes indication where applicable.

BCBS North Dakota: the employer-choice reality

BCBSND’s 2026 weight-loss drug change bulletin is the cleanest public explanation of the employer-controlled lane. Fully-insured non-grandfathered large-group plans lose weight-loss drug coverage at 2026 renewal. Small-group and individual metallic plans keep coverage because essential health benefit (EHB) requirements mandate it. Self-funded employer groups decide. If you’re on a North Dakota Blue plan, “Does BCBSND cover Foundayo?” is the wrong question. The right question: “Is my employer fully-insured or self-funded, and if self-funded, did we include weight-loss drugs in the 2026 plan design?” HR can answer that in one email.

FEP Blue / FEHB: the live federal framework

FEP Blue (the Blue Cross Blue Shield Service Benefit Plan for federal employees) handles retail pharmacy benefits through CVS Caremark. FEP’s published member materials describe a weight-loss prior-approval process for eligible members; electronic PA submissions can receive decisions faster than fax or phone. As of April 2026, Foundayo had not yet appeared in the FEP formulary exception lists we reviewed (policy pending), but the existing weight-loss prior-approval framework would logically apply. FEP retail pharmacy questions route through 1-800-624-5060.

What Blue Cross prior authorization for Foundayo usually requires

On Blue Cross plans that cover weight-loss GLP-1s, Foundayo prior authorization typically requires clinical documentation that the member meets FDA-aligned criteria: a BMI of 30 or higher (or 27+ with a weight-related comorbidity), documented prior weight-loss attempts through lifestyle modification, and current or recent enrollment in a supervised weight-management program. Criteria tighten on some Blue plans to BMI ≥40 or BMI ≥35 with comorbidity (Excellus, Blue Shield of CA).

The documentation your prescriber needs to submit breaks into five buckets. Get all five right on the first submission and your PA lands in the approval lane. Miss one and you’re in the denial-for-missing-documentation loop.

BMI documentation with dates

Not just "the patient has obesity." The PA needs height, weight, and BMI calculated with a measurement date, plus BMI history data points showing the trajectory. Several plan policies explicitly require documentation of the patient's clinical status at the time the drug was originally initiated, regardless of the date of the current coverage request.

ICD-10 diagnosis codes

| ICD-10 code | Description |

|---|---|

| E66.01 | Morbid (severe) obesity due to excess calories |

| E66.811 | Obesity, class 1 (BMI 30.0–34.9) |

| E66.812 | Obesity, class 2 (BMI 35.0–39.9) |

| E66.813 | Obesity, class 3 (BMI ≥40) |

| E66.9 | Obesity, unspecified |

| Z68.xx | BMI codes paired with the obesity code |

| E11.9 | Type 2 diabetes (if comorbidity) |

| I10 | Hypertension (if comorbidity) |

| G47.33 | Obstructive sleep apnea (if comorbidity) |

| E78.5 | Dyslipidemia (if comorbidity) |

A PA that lists only “weight loss” as the indication without obesity ICD-10 codes is a classic cause of denial on the first pass.

Prior weight-loss attempts

Dates, methods, outcomes. Not "patient tried diet and exercise" — "patient completed a 6-month structured weight-management program at [clinic name] from [dates] with documented 2% weight loss, then plateaued." Supervised program enrollment letter attached. Food/exercise logs if available. Prior medication trials with specific reasons for discontinuation.

Comorbidity documentation

If you're leveraging a BMI 27–34.9 coverage path, the comorbidity needs to be documented with supporting labs or diagnostic records. A checkbox that says "patient has hypertension" is not enough. The PA reviewer wants the ICD-10 code, the A1C or blood pressure reading that supports the diagnosis, and ideally the diagnosis date.

Letter of medical necessity

The LoMN is where your prescriber argues for Foundayo specifically. A strong LoMN addresses: why Foundayo specifically (oral pill, no injection required, no food/water timing constraints per the FDA label); why alternatives failed or are inappropriate if step therapy applies; the specific behavioral plan surrounding the medication; and the expected clinical benefit for this patient. Weight-management clinics and obesity-medicine specialists write these routinely. General PCPs sometimes don't, and that's where PAs get weak.

Auto-denial triggers to avoid

- ×BMI measurement without a recent date, or no BMI history

- ×Obesity indication without obesity ICD-10 codes

- ×Skipped step therapy where the plan requires it

- ×Active concurrent GLP-1 Rx flagged in the patient's claims history

- ×Supervised program asserted but not documented with an enrollment letter

- ×Incomplete provider form or missing signature

Let Ro’s insurance concierge handle the PA paperwork. Ro’s clinical team prescribes Foundayo; its insurance concierge handles the PA submission for your Blue Cross plan when required. You answer a few questions online. They do the rest.

Start with Ro → (sponsored affiliate link, opens in a new tab)What if Foundayo isn’t on my Blue Cross formulary yet?

Because Foundayo was FDA-approved on April 1, 2026, many Blue Cross formularies and drug-search tools haven’t been updated to explicitly list orforglipron yet. If your plan’s drug lookup returns “not found” for Foundayo, that doesn’t automatically mean non-coverage — it usually means the formulary hasn’t refreshed. You have three paths: (1) call the Rx benefits number on your card and ask for the current formulary status of orforglipron by name; (2) have your prescriber submit a formulary exception request (distinct from a standard prior authorization); or (3) wait for the formulary update, which for most plans lands within 30–90 days of new-drug approval. The fastest path is to confirm status by phone first, then act based on the verbal — but always request the answer in writing.

Prior authorization

Applies when the drug is on the formulary but requires clinical documentation before the plan will cover it. Your prescriber submits BMI, comorbidity, program participation, etc., and the plan approves or denies based on clinical criteria.

Formulary exception

Applies when the drug is not on the formulary at all and you’re asking the plan to cover it anyway based on medical necessity. The approval bar is higher and the timeline is sometimes longer.

If your plan covers a different FDA-approved GLP-1 already (Wegovy or Zepbound), sometimes the fastest legitimate path isn’t fighting the exception — it’s taking the covered drug while Foundayo works its way onto formulary. For more guidance, see our Foundayo insurance coverage guide.

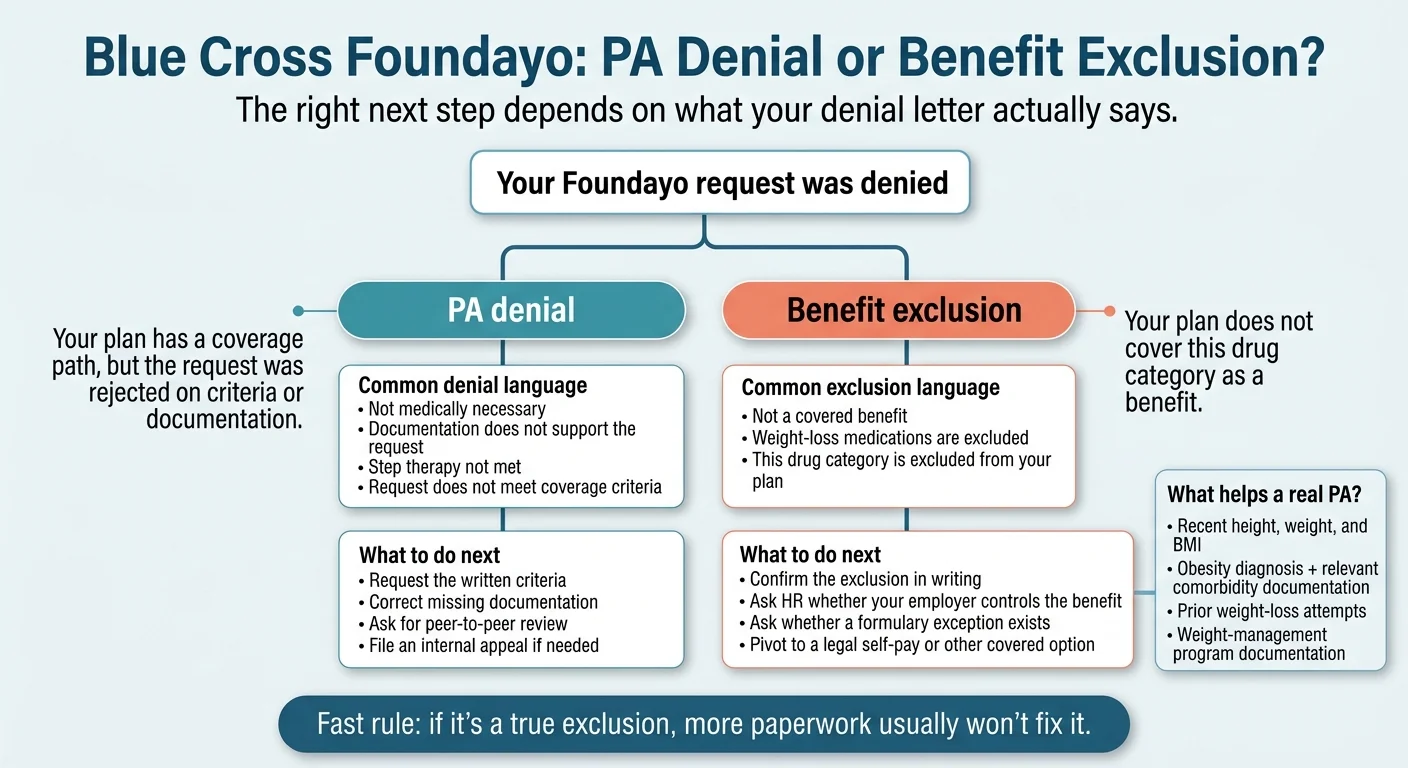

How do you tell a Blue Cross PA denial from a benefit exclusion?

A prior-authorization denial means your plan has a coverage path but rejected the request on clinical or paperwork grounds — these are appealable. A benefit exclusion means the plan design itself doesn’t cover the drug category — BCBS Massachusetts states explicitly that benefit exclusions aren’t reviewable through the medical-necessity process. The first thing to do with any denial letter is identify which one you’re holding.

You’re looking at a PA denial when the letter says:

- •Not medically necessary based on the clinical criteria for this medication

- •Documentation does not support the requested medication

- •Step therapy requirement has not been met

- •Request does not meet coverage criteria

These are appealable. Your prescriber can request a peer-to-peer review or file an internal appeal within 180 days.

You’re looking at a benefit exclusion when the letter says:

- •This service/drug is not a covered benefit under your plan

- •Weight-loss medications are excluded from your benefits

- •Your plan does not include coverage for this category of drug

These aren’t typically reviewable through the appeal process. Confirm the exclusion in writing, ask HR about a rider, and pivot to a cash-pay path.

When the plan is self-funded, the logo on your card is misleading.

Self-funded plans use Blue Cross as the ASO (administrative services only) vendor to process claims, but your employer wrote the coverage rules. Here’s how to figure it out in one HR email:

“Hi [HR contact], can you confirm whether our [company name] health plan is fully-insured or self-funded (ASO)? And does our 2026 plan design include coverage for anti-obesity medications / weight-loss GLP-1s?”

Get the answer in writing. Save that email.

Not sure if you have a PA denial or benefit exclusion? Ro confirms your plan’s actual coverage status, so you’re not guessing from a phone rep’s summary.

Run the free Ro coverage check → (sponsored affiliate link, opens in a new tab)Exclusion already confirmed in writing? Skip the appeals rabbit hole — we break down the cheapest legal way to get Foundayo without insurance.

See Foundayo cash-pay paths →What Foundayo actually costs with Blue Cross Blue Shield

With Blue Cross coverage and an approved prior authorization, eligible commercially insured members can pay as little as $25/month using the Foundayo Savings Card. Under Lilly’s self-pay savings program, Foundayo prices are $149/month (0.8 mg starting dose), $199/month (2.5 mg), $299/month (5.5 mg and 9 mg), and $349/month (14.5 mg and 17.2 mg) — with a current $299/month offer on the 14.5 mg and 17.2 mg doses if refill check-in is completed within 45 days. Current Lilly savings programs are set to expire December 31, 2026.

If your Blue Cross plan covers Foundayo (Lane 1)

Expected monthly cost: $25–$100 depending on copay tier

- •Foundayo Savings Card allows eligible commercially insured members to pay as little as $25/month

- •Savings Card discount caps: up to $100 off a one-month prescription, $200 off two months, or $300 off three months, for up to 10 fills per year

- •Medicare, Medicaid, TRICARE, and other government-insurance members are not eligible for the Savings Card

- •HSA/FSA dollars can cover your actual out-of-pocket prescription spending, but per Lilly's Savings Card terms, you may not seek HSA/FSA reimbursement for the value of savings received through the card itself

- •Current Lilly Foundayo savings programs expire December 31, 2026

If your Blue Cross plan does NOT cover Foundayo (Lanes 2 or 3)

Expected monthly cost under Lilly’s self-pay savings program: $149–$349 depending on dose

| Dose | Self-pay price/month |

|---|---|

| 0.8 mg (starting dose) | $149 |

| 2.5 mg | $199 |

| 5.5 mg | $299 |

| 9 mg | $299 |

| 14.5 mg | $299 with 45-day refill check-in; $349 without |

| 17.2 mg | $299 with 45-day refill check-in; $349 without |

Foundayo HSA/FSA eligibility: Foundayo is a prescription medication, so your actual out-of-pocket spending is HSA/FSA-eligible whether or not your plan covers it. For a member in the 24% federal tax bracket, paying $149/month with pre-tax HSA dollars effectively runs about $113/month after the tax benefit.

If you’re on Medicare Part D

The Medicare GLP-1 Bridge runs July 1, 2026 through December 31, 2027 (18 months) and covers Wegovy (all formulations), Zepbound KwikPen, and Foundayo (CMS added April 6, 2026) for eligible Part D beneficiaries. BALANCE did not launch for Medicare Part D in 2027 — CMS extended the Bridge. Eligible Bridge beneficiaries pay $50/month for covered products.

Bridge eligibility tiers (same criteria for Wegovy, Zepbound KwikPen, and Foundayo):

- •BMI ≥35 alone, no additional diagnosis required

- •BMI ≥30 with heart failure with preserved ejection fraction (HFpEF), uncontrolled hypertension (systolic >140 mm Hg or diastolic >90 mm Hg on at least two antihypertensives), or chronic kidney disease stage 3a or above

- •BMI ≥27 with pre-diabetes (per ADA guidelines), prior myocardial infarction, prior stroke, or symptomatic peripheral artery disease

For Foundayo and Medicare, your real timeline is the Bridge through December 2027. BALANCE did not launch for Medicare Part D in 2027 — the 80% plan participation threshold was not met. CMS extended the Bridge. Foundayo is on the Bridge drug list. Both Eli Lilly and Novo Nordisk have agreed to participate in BALANCE when it eventually launches. The most accurate planning window: use Wegovy or Zepbound via Bridge in the second half of 2026 if you qualify, then switch to a BALANCE-participating Part D plan during fall 2026 open enrollment and transition to Foundayo in 2027 if that’s what your prescriber recommends.

The stack: Savings Card + commercial Blue Cross coverage is the lowest legal cost. If your Blue Cross plan covers Foundayo, your copay might be $50–$100 on a typical tier-2 or tier-3 formulary. The Foundayo Savings Card stacks with commercial insurance to reduce that copay to as little as $25. The card is explicitly blocked from government-insurance use.

Get your lowest verified Foundayo price with Blue Cross. Ro shows transparent cash-pay pricing if coverage isn’t available, or routes you into the PA path if it is.

Get free coverage check & transparent pricing on Ro → (sponsored affiliate link, opens in a new tab)How to get your Blue Cross Foundayo prior authorization approved (step by step)

Confirm coverage BEFORE anyone does paperwork

The biggest waste of time in this entire process is submitting a PA for a drug your plan doesn't cover. 30 minutes on the phone up front saves three weeks of back-and-forth.

- •Portal check (3 minutes): Log into your Blue Cross member portal (MyBlue, Blue Access for Members, FEP Blue portal, Anthem portal). Go to "Pharmacy benefits" or "Drug coverage." Search for orforglipron or Foundayo. Note the tier, PA requirement flag, any step-therapy requirement, and quantity limits. If the drug doesn't appear yet, proceed to the phone call.

- •Phone call (15 minutes): Use the Rx benefits number on the back of your card. Use the 7-question script in the next section — don't freestyle.

Book a visit with a PA-savvy provider

Your options: Your existing PCP (works if they handle weight-management PAs routinely); a weight-management clinic or obesity-medicine specialist (these providers submit GLP-1 PAs constantly); telehealth providers like Ro (offers Foundayo + dedicated insurance concierge) or Sesame Care (marketplace of providers including Foundayo prescribers). LillyDirect is fine if you're paying cash but does not handle insurance or PA work.

Submit the PA through the plan's preferred channel

- •Availity ePA portal — HCSC plans (BCBS Illinois, Texas, Oklahoma, Montana, New Mexico), Highmark, some others

- •Prime Therapeutics ePA — most Blue plans use Prime as the PBM

- •CVS Caremark ePA — FEP Blue, Anthem, some others

- •Direct subsidiary portals — Blue Shield of CA's AuthAccel; BCBSMA's medical portal

- •Fax — still common; less efficient

Track the decision and respond immediately to any information request

PA timelines depend on the plan, channel, and urgency flag. Electronic PA decisions can come back in minutes to hours; non-electronic PA typically runs hours to days. ACA federal rules allow up to 72 hours for non-urgent prescription drug decisions and 24 hours for urgent. Check PA status daily in the member portal and have your provider's office check the ePA system. If the PBM requests additional information, respond the same day — every day lost is a day the PA sits pending. Ro states that getting started using insurance takes about two to three weeks end-to-end.

Fill it — and apply the Savings Card

Once the PA approves, call the pharmacy before you show up. Sometimes the system takes 24–48 hours to propagate the PA approval from the PBM to the pharmacy. Run the Foundayo Savings Card at the counter — your pharmacist knows how to process it. Keep your 45-day refill window in mind if you're on the higher doses through Ro.

Prefer a lower program fee? Try Sesame Care.

Sesame Care offers a marketplace of Foundayo prescribers at $59/mo annual subscription. Labs at Quest included in most states. HSA/FSA reimbursement supported.

Check Foundayo on Sesame Care → (sponsored affiliate link, opens in a new tab)The 7-question Blue Cross call script

When you call Blue Cross or your PBM to verify Foundayo coverage, you need answers to seven specific questions. Going in without a script is how members end up with vague verbal assurances that get contradicted by the actual PA decision. Ask for written confirmation of each answer.

Before you dial, have ready: your member ID, group number, date of birth, prescription drug plan details (Prime Therapeutics? CVS Caremark? Optum?).

Say: “Hi, I’m trying to verify prescription coverage for a specific medication. Can you help me?”

Ask these 7 questions in order, and write down the answer + the date + the rep’s name for every one:

- 1Is Foundayo — that's F-O-U-N-D-A-Y-O, the brand name for orforglipron — on my plan's formulary? If not listed yet, is my plan accepting formulary exception requests?

- 2What tier is it on, and what's the estimated copay after my deductible?

- 3Does my plan require prior authorization for Foundayo, and if yes, what are the specific clinical criteria?

- 4Is there a step-therapy requirement? If so, what medications must I try first and for how long?

- 5Is there a quantity limit or day-supply limit on Foundayo?

- 6If prior authorization is denied, what are my appeal options, and what's the timeline to file?

- 7If my plan doesn't cover Foundayo, is it because of a plan-level benefit exclusion or because the drug is non-formulary? Can I request a formulary exception?

That last question is critical. Get the reference number. If the PA decision later contradicts the phone rep’s verbal assurance, you have a record.

What to do if your Blue Cross Foundayo PA is denied

If Blue Cross denies your Foundayo prior authorization, you have four paths. Which path is right depends on whether you’re fighting a PA denial or a benefit exclusion.

Peer-to-peer review (often the fastest option for clinical denials)

PA denials onlyA peer-to-peer (P2P) review is a direct phone conversation between your prescribing physician and a medical director at Blue Cross. Your prescriber requests it using the phone number on the denial letter. The conversation typically lasts 15–30 minutes. Two clinicians discuss the case in real time — your prescriber can address the specific denial reason, cite clinical literature, and respond to questions on the spot. Best for: denials based on "not medically necessary," "documentation insufficient," or "step therapy not met with adequate justification." Timeline: usually scheduled within 1–3 business days of request.

Written internal appeal (180-day window)

PA denials onlyIf P2P doesn't resolve it, file a written internal appeal within 180 days of the denial date. What makes an appeal stronger: specific response to the denial reason cited (not a generic resubmission); additional documentation the initial PA didn't include (weight-history chart, comorbidity lab results, prior medication trial details); a revised letter of medical necessity from the prescriber; citation of the plan's own written criteria where you meet them. Timeline: plans generally have 30 days for non-urgent appeals, 72 hours for urgent.

External review

After internal appealIf the internal appeal fails, you have the right to an independent external review conducted by a reviewer not affiliated with your plan. Your state insurance commissioner runs the process. External reviewers can overturn plan decisions, and the decision is binding on the plan. Timeline: 30–45 days for standard external review, expedited in urgent cases.

The cash-pay pivot

Exclusions + urgent casesSometimes appealing isn't worth it. If you're looking at a benefit exclusion (not a clinical denial), or if you need to start Foundayo now and don't want to wait through 60 more days of appeals, the Foundayo Savings Card still works without insurance coverage and caps your out-of-pocket under Lilly's self-pay program at $149–$349/month depending on dose. Ro's cash-pay path bundles medication with the Ro Body membership: $39 intro month + $149/month ongoing, or as low as $74/month with annual prepay. LillyDirect offers the same medication at the same transparent self-pay pricing without a membership layer — the cleaner route for pure price-minimizers who don't need insurance coordination.

Don’t appeal an exclusion.

If BCBS Massachusetts’s own broker materials say benefit exclusions aren’t reviewable through medical-necessity review, a formal appeal uses your time and delays getting the medication. Confirm exclusion in writing, then pivot to Path 4. See our Foundayo denial appeal guide for a full playbook on which denials are worth fighting.

Frequently asked questions

- How much will I pay for Foundayo if Blue Cross doesn't cover it?

- Under Lilly's current self-pay savings program, Foundayo is $149/month for the 0.8 mg starting dose, $199/month for 2.5 mg, and $299/month for 5.5 mg or 9 mg. For the 14.5 mg and 17.2 mg doses, the price is $299/month under the current 45-day refill check-in offer and $349/month without it. HSA or FSA dollars can be applied to your actual out-of-pocket spending. LillyDirect and Ro both offer Foundayo at these medication prices; Ro adds the Ro Body membership fee for insurance-concierge work and ongoing care, while LillyDirect is membership-free for pure cash-pay.

- When will Foundayo be covered by Medicare?

- Foundayo IS covered by the Medicare GLP-1 Bridge — CMS added it to the Bridge drug list on April 6, 2026. The Bridge runs July 1, 2026 through December 31, 2027 (18 months) at $50/month for eligible Part D beneficiaries. BALANCE did not launch for Medicare Part D in 2027 — CMS extended the Bridge instead. Watch for BALANCE 2028 announcements during fall 2027 open enrollment.

- Is Foundayo covered by Blue Cross for type 2 diabetes?

- Not yet. Foundayo (orforglipron) is currently FDA-approved only for chronic weight management in adults with obesity or overweight with weight-related conditions. Eli Lilly has indicated an FDA submission for a type 2 diabetes indication is planned later in 2026. When that approval comes through, Blue Cross coverage for Foundayo under the diabetes indication is likely to follow patterns similar to existing coverage for Ozempic and Mounjaro. Members with type 2 diabetes seeking a GLP-1 now have covered paths through Ozempic, Mounjaro, Rybelsus, or Trulicity.

- Can my regular doctor handle the Foundayo PA, or do I need a specialist?

- Your regular prescribing provider can submit the PA, and many do. Weight-management clinics, obesity-medicine specialists, and PA-experienced telehealth services submit these forms constantly and understand each plan's quirks. If your PCP's office doesn't regularly handle GLP-1 PAs, consider a dedicated weight-management provider or a telehealth service like Ro that includes insurance-concierge PA handling as part of the membership.

Still not sure which Blue Cross Foundayo path fits your situation?

Take our free 60-second GLP-1 matching quiz. We’ll factor in your coverage situation, budget, and goals and return a personalized action plan — which provider to use, what your PA criteria look like, and what you’ll actually pay.

Get my personalized Foundayo + Blue Cross action plan →Related guides on The RX Index

- Blue Cross Wegovy Prior Authorization (2026) →

- Blue Cross Zepbound Prior Authorization (2026) →

- Does Insurance Cover Foundayo? (2026 Guide) →

- Who Qualifies for Foundayo? 2026 Eligibility Rules →

- Foundayo Prior Authorization: Full PA Playbook →

- Foundayo Cost Without Insurance (2026) →

- Foundayo Savings Card: Eligibility and How It Works →

- How to Appeal a Foundayo Denial →

- The Medicare GLP-1 Bridge Program Explained →

- Foundayo Reviews: What Patients Report →

Sources

- Excellus BlueCross BlueShield, Weight Management Pharmacy Policy PHARMACY-03, reviewed April 13, 2026.

- BCBS Massachusetts, GLP-1 drug policy and Focused Formulary communications, effective January 1, 2026.

- Independence Blue Cross, provider bulletin on weight-loss drug coverage, effective January 1, 2025; confirmed in effect 2026.

- BCBS North Dakota, 2026 weight-loss drug change bulletin.

- FEP Blue / Blue Cross Blue Shield Service Benefit Plan, CVS Caremark Retail Pharmacy Program, member materials reviewed April 2026.

- Foundayo (orforglipron) US Prescribing Information, Eli Lilly and Company, April 2026.

- CMS, “Medicare GLP-1 Bridge” FAQ page (cms.gov), updated March 2026.

- Eli Lilly press release, “FDA approves Lilly’s Foundayo,” April 1, 2026.

- LillyDirect Foundayo page and Foundayo Savings Card terms and conditions, foundayo.lilly.com/coverage-savings.

- Ro.co Foundayo product page and press release, April 9, 2026.

- BCBS Association, company member directory.

- BCBSMA broker/account FAQ on Focused Formulary exclusions, 2026.

- FDA, new drug approval notification for orforglipron (Foundayo), April 1, 2026.

- Blue Shield of California, GLP-1 weight-loss coverage fact sheet, 2026.

- Anthem Blue Cross Blue Shield state plan materials, Nevada and other states, 2026.

- BCBS Michigan, commercial large-group GLP-1 coverage notice, effective January 1, 2025.

- HCSC (BCBS Illinois/Texas/Oklahoma/Montana/New Mexico), Prime Therapeutics ePA guidelines, 2026.

- ACA and ERISA federal appeal timelines, 45 CFR §147.136.

- KFF, “What Medicare’s Temporary Program Covering GLP-1s for Obesity Means for Beneficiaries,” March 2026.

- CMS, “BALANCE Model” page, cms.gov/priorities/innovation/innovation-models/balance.

- BCBS Association, prior-authorization reform commitment announcement, 2024.

By The RX Index Editorial Team. The RX Index is a pricing intelligence and comparison resource for GLP-1 telehealth providers. Published April 21, 2026. Last verified: April 21, 2026. Next scheduled review: May 21, 2026.

Medical disclaimer: This page is for educational purposes only and is not medical advice. A licensed prescriber makes all final eligibility and treatment decisions. This page contains no information about compounded orforglipron — there is no FDA-approved compounded Foundayo; do not treat any compounded orforglipron product as equivalent to FDA-approved Foundayo.

Your situation changes the answer

Find My GLP-1 Path

The right GLP-1 provider isn't the same for everyone. It depends on your state, your insurance and formulary, whether you want an FDA-approved or compounded medication, your preferred route (injection or oral), and your budget. Because a general answer can't resolve those for you, use The RX Index's Find My GLP-1 Path tool to get a personalized provider match with source-verified pricing before you choose.

- What it asks: your state, insurance situation, medication preference, budget, and support needs

- What you get: a personalized shortlist of GLP-1 providers matched to your situation, with verified pricing and the right questions to ask

- Cost: free · about 2 minutes · no signup